Everyone knows that the American consumer is deleveraging … living more frugally, and paying down debt.

Right?

Well, actually, as CNBC’s Diana Olick pointed out in April, many consumers are stopping their mortgage payments, and then blowing the money they would usually pay towards their mortgage on luxuries:

I opened up a big can of debate Monday, when I repeated some chatter around that consumer spending might be juiced by all those folks not paying their mortgages.

They have a little extra cash, so they’re spending it at the mall.

Some of you thought the premise had some validity, others, as is often the case, told me I was an idiot.

Well after the blog went up Erin Burnett put the question to Economist Robert Shiller, of the S&P/Case Shiller Home Price Index, during an interview on Street Signs.

He didn’t deny the possibility, and added:

“In some sense there might be a silver lining in that.”

Then I decided to ask Mark Zandi, of Moody’s Economy.com, who will often shoot down my more ridiculous theories.

I asked him if this was a crazy idea:

No, not crazy. With some 6 million homeowners not making mortgage payments (some loans are in trial mod programs and paying something but still in delinquency or default status) , this is probably freeing up roughly $8 billion in cash each month. Assuming this cash is spent (not too bad an assumption), it amounts to nearly one percent of consumer spending. The saving rate is also much lower as a result. The impact on spending growth is less significant as that is a function of the change in the number of homeowners not making payments.

I’m not sure I would say this is juicing up spending, but resulting in more spending than would be the case otherwise.

Many of these stressed homeowners (due to unemployment) are reducing their spending, just not as much as they would have if they were still making their mortgage payment.

Okay, so 6 million American homeowners are not being super frugal about either paying their mortgages or saving the money for another investment.

But surely the hundreds of millions of other Americans are reducing debt and deleveraging, right?

In fact, as the Wall Street Journal notes today, the overwhelming majority of debt reduction by consumers is not due to voluntary debt reduction, but due to defaulting on their debts and having them involuntarily written down by the banks:

The sharp decline in U.S. household debt over the past couple years has conjured up images of people across the country tightening their belts in order to pay down their mortgages and credit-card balances. A closer look, though, suggests a different picture: Some are defaulting, while the rest aren’t making much of a dent in their debts at all.

First, consider household debt. Over the two years ending June 2010, the total value of home-mortgage debt and consumer credit outstanding has fallen by about $610 billion, to $12.6 trillion, according to the Federal Reserve. That’s an annualized decline of about 2.3%, which is pretty impressive given the fact that such debts grew at an annualized rate in excess of 10% over the previous decade.

There are two ways, though, that the debts can decline: People can pay off existing loans, or they can renege on the loans, forcing the lender to charge them off. As it happens, the latter accounted for almost all the decline. Over the two years ending June 2010, banks and other lenders charged off a total of about $588 billion in mortgage and consumer loans, according to data from the Fed and the Federal Deposit Insurance Corp.

That means consumers managed to shave off only $22 billion in debt through the kind of belt-tightening we typically envision. In other words, in the absence of defaults, they would have achieved an annualized decline of only 0.08%.

The Journal graphically shows that virtually all debt reduction is due to loan charge offs:

Karl Denninger notes:

From a peak in 2005 of $13.1 trillion in equity in residential real estate, that value has now diminished by approximately half to $6.67 trillion!Yet outstanding household debt has in fact increased from $11.7 trillion to $13.5 trillion today.

Folks, those who claim that we have “de-levered” are lying.

Not only has the consumer not de-levered but business is actually gearing up – putting the lie to any claim that they have “record cash.” Well, yes, but they also have record debt, and instead of decreasing leverage levels they’re adding to them.

In short don’t believe the BS about “de-leveraging has occurred and we’re in good shape.” We most certainly have not de-levered, we most certainly are not in good shape, and the Federal borrowing is what, for the time being, has prevented reality from sticking it’s head under the corner of the tent.

Indeed, as I’ve pointed out repeatedly, the government has done everything it can to prevent deleveraging by the financial companies, and to re-lever up the economy to dizzying levels.

As Jim Quinn wrote last month:

You can’t open a newspaper or watch a business news network without seeing or hearing that consumers and businesses have been de-leveraging. The storyline as portrayed by the mainstream media is that consumers and corporations have seen the light and are paying off debts and living within their means. Austerity has broken out across the land.

***

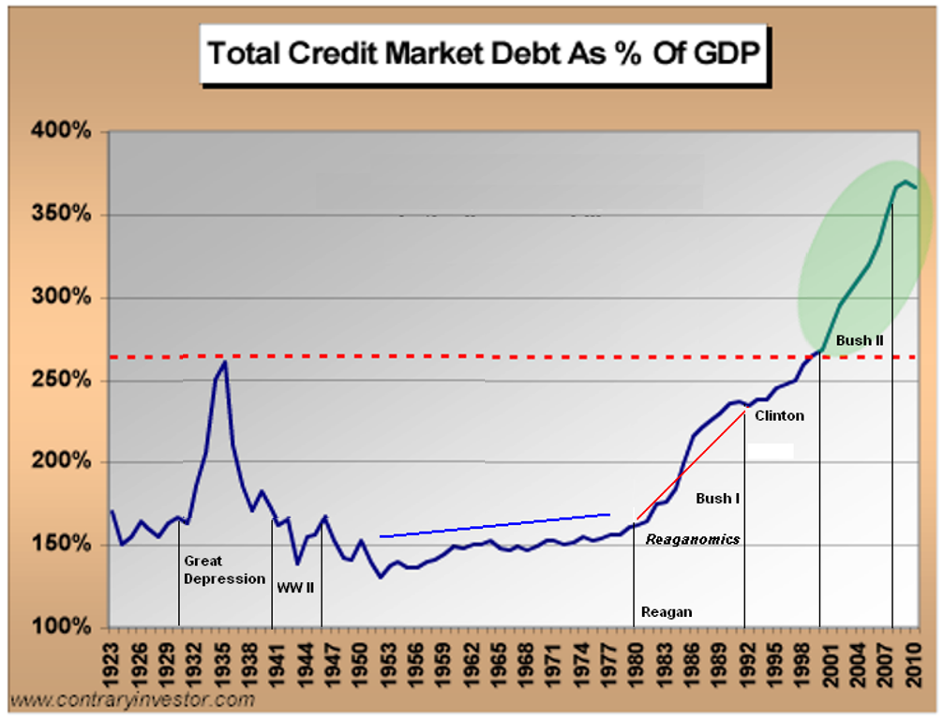

Below is a chart that shows total credit market debt as a % of GDP. This chart captures all of the debt in the United States carried by households, corporations, and the government. The data can be found here:

http://www.federalreserve.gov/releases/z1/current/accessible/l1.htmTotal credit market debt peaked at $52.9 trillion in the 1st quarter of 2009. It is currently at $52.1 trillion. The GREAT DE-LEVERAGING of the United States has chopped our total debt by 1.5%. Move along. No more to see here. Time to go to the mall. Can anyone in their right mind look at this chart and think this financial crisis is over?

During the Great Depression of the 1930′s Total Credit Market Debt as a % of GDP peaked at 260% of GDP. As of today, it stands at 360% of GDP. The Federal Government is adding $4 billion per day to the National Debt. GDP is stagnant and will likely not grow for the next year. The storyline about corporate America being flush with cash is another lie. Corporations have ADDED $482 billion of debt since 2007. Corporate America has the largest amount of debt on their books in history at $7.2 trillion.

Indeed, as this chart courtesy of Zero Hedge confirms, traditional banking liabilities are higher than ever:

Granted, the liabilities of the shadow banking system have fallen off of a cliff.

But Tyler Durden argues:

The latest plunge in the shadow banking system is merely the most recent confirmation that the deleveraging in America is only just beginning.

So what does it all mean?

The government, big financial companies and the American consumer are all guilty of fighting deleveraging instead of voluntarily paying down their debt.

Like a junkie looking for “one last score”, the entire country has sold out our future to try to keep the artificial high going a little longer.

As I pointed out in July 2009:

Every independent economist has said that too much leverage was one of the main causes of the current economic crisis.However … the Federal Reserve and Treasury have, in fact, been encouraging massive leveraging.

***

Economists pushing voodoo theories justifying the tremendous increase in leverage were promoted and lionized, while those questioning such nonsense were ridiculed.In other words, economists and financial advisors – in academia, government and elsewhere – have been subservient to the financial elites, and have trumpeted the safeness and soundness of cdos, credit default swaps, and all of the rest of the shadow economy which allowed leverage to get so out of hand that it brought the world economy to its knees.

This is no different from the promotion of sports doctors to become team doctor when they are willing to inject various painkillers and feel-good drugs into an injured football star so he can finish the game. If he is willing to justify the treatment as being safe, he is promoted. If not, he’s out.

Economists have acted like team docs for the financial giants. When the football team doctor who gives the injured patient steroids and stimulants and tells him to get back in the game, it might be good for the team in the short-run, but the patient may end up severely injured for decades.

When economists have prescribed more leverage and told the banks to go trade like crazy to get the economy going again, it might be good for the banks in the short-run. But the consumer may end up being hurt for many years.

Using another analogy, this is like prescribing”hair of the dog” to the suffering alcoholic or heroin to the withdrawing junkie.

And as I wrote in August 2009:

In an essay entitled “The risk of a double-dip recession is rising”, Nouriel Roubini affirms two important points:

This is a crisis of solvency, not just liquidity, but true deleveraging has not begun yet because the losses of financial institutions have been socialised and put on government balance sheets. This limits the ability of banks to lend, households to spend and companies to invest…

The releveraging of the public sector through its build-up of large fiscal deficits risks crowding out a recovery in private sector spending.

In other words, Roubini is confirming what Anna Schwartz and many others have said: that the problem is insolvency, more than liquidity, that the government is fighting the last war and doing it all wrong, and that we should let the insolvent banks fail.

Roubini is also confirming that incurring huge deficits in order to have the federal government itself act as a super-bank is causing a reduction in – and “crowding out” a recovery in – private sector spending. [Roubini also said last year: “Deleveraging requires the writing down of debt as reflationary policies are not a free lunch and won’t solve the debt overhang problem”].

As I have repeatedly pointed out, a recovery cannot occur until we move through the painful deleveraging process. But instead of allowing this to occur, the government is trying to increase leverage as a way to try to re-start the economy and save the insolvent banks. See this, this and this.

Of course, all of the massive government spending might also be putting governments themselves at risk . . . but that is another story.

Yves … thanks for another brilliant post … but for you I wouldn’t have understood what this crisis is all about. Listening to our much touted economists would leave a person ignorant forever …

thanks

mmckinl

“Listening to our much touted economists would leave a person ignorant forever … ”

Other sources that leave a person ignorant forever include reading news at Yahoo. com as I did from when I first came online in 1998.

Likewise Google.com.

or Associated Press

or Washington Post

Or LA Times

Or the Economist

Or Newseek

Or Time magazine

or . . .

And yes even the wonderfully well informed, much touted New York Times will leave a person clueless.

I have been trying to follow this blog for the last seven to ten months and am finally catching on to the scheme of lies that Greenspan, Bernanke, Paulson, Geithner & Co are spreading everywhere. The & Co part of that partnership includes the likes of Goldman Sachs, Citigroup et al who profit mightily each time a sixteen wheeler loaded with US treasury notes pulls away from the loading dock at the US Treasury building, heading towards the nearest beneficiary somewhere in the financial sector.

I would encourage you to look beyond that beneficiary somewhere in the financial sector and attempt to understand the players behind the curtain that those beneficiaries work for.

Jim Quinn writes, “Can anyone in their right mind look at this chart [debt to GDP] and think this financial crisis is over?”

Another glaring question is how could Greenspan, Bernanke, Paulson, Geithner & Co in their right minds have ignored that same chart for thirty years, since the advent of voodoo reaganomics? And worse, how could the very same crew still be left in charge of hole-digging? Oh, one more: how did Greenspan manage to land an advisory post in Paulson & Co, the same company that made a killing shorting CDOs popped by Greenspan’s own bubbles?

“how could Greenspan, Bernanke, Paulson, Geithner & Co in their right minds have ignored that same chart for thirty years, since the advent of voodoo reaganomics?”

Read Steve Keen (http://www.debtdeflation.com/blogs): for mainstream economists debt is a totally irrelevant parameter. Because of that they can’t understand our current mess on principle.

This is going to end up very, very badly.

The failure of leadership and creativity http://bit.ly/a5xjdK during this crisis has been colossal.

The consequences promise to be colossal too.

So Francois, not do disagree strongly with you, but I’m not sure that ‘very badly’ is the phrase that will describe our outcome in, say, fifteen years. Very _differently_ from the set of conditions we came to see as the norm in the 1980-2007 period, yes. The Anglo-American duopoly will look and live smaller, but how much, and with how much disruption is far from certain.

Consider France, 1947-75 or so. Currency collapse with considerable losses for the upper class. End of Great Power-dom (hooray!). Withdrawal from most colonies. Great reduction in the army (though increase in nuclear forces). Implementation of a sociable social policy, practically a socialist one. Very different than before. ‘Less’ than before in the eyes of many. Worse? Hmmm. As another example, consider Argentina 1988 versus Argentina 2008 to present. Is everything fixed? No. Are things better managed (somewhat) and more just (somewhat more).

What is a likely result of the American refusal to deleverage and restructure in a timely way, in the determination to coddle the superrich, is that the US will lose significant competitive advantage relative to other countries which manage this transition better. Those unemployed now and over the next long while will have the financial course of their lives significantly and permanently indexed down in consequence [which I see as a bad thing, though also an opportunity to re-evaluate goals]. If there is a Monster Correction out there, and there may well be, the biggest snap will be born by those with the most to lose, those holding crap mega-assets. But however the wash looks when it comes out of the turbulence, it won’t look as nice as those who had actual growth and development in the interim. Thus to me the big question is, how does the US take _this_ potential/probable outcome? By getting to work sanely? By chucking bombs and scapegoating designated ‘social undesirables? by getting a clue? By the coming of the rapture?

We can hit bottom, pick ourselves up, and get on fairly well if we choose. Or start firing off a gun in a crowded phone booth of a world. The latter, for me, constitutes ‘very badly.’ But that outcome isn’t a lock. It’s more probable than it was five years ago, though, and I can’t say I feel too good about that.

Richard,

I can see two differences between France’s Trente Glorieuses (1947-1975) and the coming era for America, although obviously I’m speculating on what future conditions will be in the US. The first is that, as the name implies, France’s transition took place during a time of economic expansion. I think most would agree this will not be the case for the US. The second is that much of this transition was accomplished under excellent leadership, namely Charles de Gaulle, who was that rarest of geniuses in both the political and military realms. Now of course it is possible that some American political genius could arrive in power but the current US system and its concentration of power into such a small elite make it doubtful that any substantial changes against the interests of this elite are possible. Perhaps a semi-coup d’etat that introduces a Second American Republic (along the lines of De Gaulle coming to power in 58 and creating the French Fifth Republic) would make it possible to have sound leadership in the US.

But what struck me was your comment about the reduction of military forces in France. In fact, from a long term historic view, this could in fact be the problem. Historically, in broad terms, military technology toggles between the one extreme of being so powerful and expensive that only a small elite can be armed (and therefore dominate the masses), all the way to the other extreme of being so low tech that mass armies are required (where elites are less able to dominate). The former case, expensive, elite arms, tends to coincide with concentrations of power and Dark Ages. The second condition, inexpensive arms for the masses, tend to coincide with Golden Ages and relative equality.

A few examples of this are Greece during its Dark Ages vs. Classical times. During the Greek Dark Ages a very small number of elites mounted on horses were able to overpower and subjugate large numbers of peasants. The arrival of the phalanx (highly trained but relatively inexpensive to equip) meant that numbers now mattered and we saw a spreading of relative equality in many of the Greek City States. The German tribes described by Tacitus were very egalitarian, the adult freemen were always armed in public and during their counsels would signal approval by clashing their spears. In such a situation it was difficult for potential elites to amass enough power to enslave their masses.

But eventually the pendulum swung back, with the power and expense of armour, mounted solders, and moated strongholds, elites were again able to dominate the masses during feudal times. But with the advent of fire arms and artillery, and Napoleon’s mass state-backed armies, equality slowly started spreading out. I would say this process peaked somewhere between just after WW2 up until the end of the sixties. Ironically, perhaps it was the Vietnam war protests, combined with huge leaps in technological potential, and of course nuclear weapons, that convinced American elites to go with smaller, more high-tech professional armies. The masses were no longer required to project strength, a huge manufacturing base was not longer required, and we are just beginning to feel the real results of this shift in power. With the possibility of robotic weapons this process may have much further to run. One possible countervailing current could be electromagnetic pulse weapons that could eventually make high tech weapons obsolete.

I don’t see EMP as changing anything. Isn’t EMP expensive and bulky? Not something you could build in a garage, I don’t think. Biological weapons CAN be built in a garage, but I suspect bioterrorism (which is definitely coming) will result in a total surveillance society, as the only way to keep the terrorism under control. Bioweapons can definitely neutralize nuclear power, which means we are back to conventional weapons.

“Weapon Systems and Political Stability” at carrollquigley.net for more on this topic.

I don’t think EMP weapons are all that expensive or difficult to construct if you know what you are doing. The hurdle with EMP weapons isn’t expense, it’s knowledge of physics and electronics.

Thanks for the link. As you can probably tell my ideas are influenced by Quigley’s “The Evolution of Civilizations” so I will definitely check out his “Weapons Systems and Political Stability” which I didn’t know about.

On EMP, whether there is a high entry level or not, if these weapons were successfully deployed they may render high tech weapons (and the associated control systems) too expensive or too vulnerable.

Very clean speculation about the probable course for the next several years (decades?). Just one question about your examples. Do you or any other reader know what the private savings rate in France and Argentina was during the relevant periods? It seems that, at least in the case of Japan, the private savings rate has allowed the government to continuously prop up the economy. So it may be that high private savings allow a society to go through a prolonged period of economic disquietude with some equanimity. Although Argentina did have the “dirty war” somewhat earlier than the period cited.

Where’s the data in this post to support the longstanding MSM talking point that people who walk away are using the cash freed up to “binge” on “luxuries”?

Every piece I’ve ever seen based this propaganda on one or two dubious anecdotes, never data, and commentators like Ritholz have attacked this lie many times.

That’s right. And let’s not forget the fact that very low interest rates are driving people with equity (mostly outside CA, NV, AZ, and FL) to refinance and reduce their monthly payments. Maybe it is these people who have a little extra cash and are spending it at the mall.

Refinancings, according to the latest MBA survey, make up about 80% of new mortgage applications. Surely this is also having an affect too.

This piece is very troubling to me, but for reasons that do not appear explicitly here.

In true prophetic tone I say… if people are defaulting on their mortgages and using the money to buy “luxuries”, well that represents… the ULTIMATE (ultimate for one point in time, not ultimate for all time, nuance…) default on the social contract.

That means that… people don’t BELIEVE in the capacity of U.S. debt-money to STORE value and the possibility of holding on to it for FUTURE exchanges, and they are CASHING IN on the abstract debt in order to pick up REAL MATERIAL COMMODITIES in exchange for their “debt”. They feel NO SOCIAL OBLIGATION to INDIVIDUALLY RESPECT the social contract. Bad news, folks…

I also think that the concept of “fiat” money is inaccessible for a society that has… LOST FAITH. Logical, right ? And “credit” comes from the word, BELIEF.

Fiat currency works in a society and an economy that BELIEVES in something, and that certainly.. BELIEVES IN MAN. I see.. NO (or little…) evidence for such belief in modern American society at this time. No belief in man, NO FIAT. NO ECONOMY EITHER, while we’re at it. Melancolic implosion.

I would also say that such behavior (defaulting on mortgages) is.. LIGHT YEARS away from the behavior of our grandfathers (my grandmother, at least..) in the Great Depression (if it is going on..).

For my grandmother.. PAYING BACK A DEBT WAS SACRED.

Maybe because… “In God we TRUST” was marked on the MATERIAL CURRENCY that she handled all the time ?? (SHE certainly believed in God…)

Unfortunately, the long term effect of idolatry of money, which consists in the ABSENCE OF BELIEF IN ANYTHING BESIDES MONEY… is the loss of belief in money itself.

Let’s face it.. how the hell could MONEY ALONE support our incredible human need to believe in something ? It is supposed to be.. a TOOL that we use.. not a GOD that we serve.

“Science” is not doing so well today.

“Economic” “science” is doing even worse..

As far as buying luxuries is concerned… not at the shopping mall, I hope.

ARE LUXURIES STILL TO BE FOUND in the U.S. ?

In MY book.. luxuries are not MASS MANUFACTURED at any rate…

The definition of luxury is tied up in the concept of aristocracy. We would need a book to start dealing with this subject.

A book that would take us back to “luxury” in the Middle Ages (not the Dark Ages..).

Sorry, attempter..

Excuse me while I get back to Charlie and Cindy… ;-)

I’m assuming your pretty young since for your grandmother to have always handled paper money that contained the phrase “In God We Trust” she would have had to have led her adult life completely after 1957 because:

“IN GOD WE TRUST was first used on paper money in 1957, when it appeared on the one-dollar silver certificate.”

Source: http://www.ustreas.gov/education/fact-sheets/currency/in-god-we-trust.shtml

As for your larger concern about a default on the social contract, you might better focus your energies on why the leader of the American banking system went on their knees to the Federal Reserve and Congress where they received trillions of dollars in public funds and guarantees to prop up and conceal trillions of dollars of their own past mistakes rather than face the music of the free markets they purport to believe in.

Could the “luxuries” being mentioned here refer to gold and silver jewelery and coins, as a form of investment during a time of uncertainty?…

Psychoanalystus

It is intellectually and ideologically incorrect to talk about “the masses” during feudal times.

“The masses” is a concept that emanates from our post industrial revolution conceptions of political power. They are inappropriate to talking about, and thinking about our ancestors who lived before such concepts appeared.

A remark of.. SCIENTIFIC METHOD.

THERE WERE NO MASSES under the “Ancien Regime”.

ON THE CONTRARY : human society was highly DIFFERENTIATED, and different people assumed different and DISTINCT FUNCTIONS in society.

Funnily enough.. the ideology behind the monarchy gives a capital, NOBLE, and extremely IMPORTANT role to the peasants. THEY are the ones working closest to the earth. And.. the earth, and LAND, were SACRED to our ancestors. THEY WERE A SOURCE OF INTRINSIC VALUE. (Not exclusively… filthy lucre…)

Now.. if you want to look at history through MODERN rose coloured glasses, go ahead.

Funnily enough… EVEN JACQUES BARZUN, who is an intellectual that I cannot hold a candle to made a TELLING MISTAKE in a phrase that he used to talk about the European cathedral builders…

He spoke about ANONYMOUS workmen.

This is UNTRUE. The INDIVIDUAL stones of Notre Dame Cathedral have the INITIALS of the INDIVIDUAL workmen who were NOBLY putting THEMSELVES into the service of a collective good that brought together many DIFFERENT PEOPLE in a collective project : the cathedral, TO THE GLORY OF GOD (and man, incidentally…).

Our conceptions about.. INDIVIDUAL NAMES have evolved considerably over 1000 years.

If EVEN Jacques Barzun makes mistakes like this.. what kind of mistakes are the people on the blogs making ??

I have seen this happening – people aren’t deleveraging at all, they are blowing their money as fast as they can.

And it might be appropriate to ask – why is it that banks and corporations can walk away from commercial property – but it isn’t ok for a homeowner to walk away??? The banks are spending up big – with no cash reserves. That seems to be ok – but a homeowner can’t do the same thing? And then they do the mantra “do as I say not as I do”. Really????

I would recommend all underwater homeowners to default. And blow the money on a nice holiday somewhere. At least you will have that. And while you are at it – drop health insurance en masse – may as well make that change as well. As those insurance co’s are really taking blood on what they charge.

Wake up America – you are getting screwed by the oligarchs. Just do as to them as they do unto you. Seeing as everyone loves that religious view – exploit it.

You misrepresent “that religious view” — at least if you refer to the Christian religion. The Christian precept is not “do unto others as they do to you” but “do unto others as you would wish them to do to you” — which provides no endorsement for the desperate kind of bloody-mindedness you advocate.

To me this represents the result of faith based anything.

I pine for reason, logic, critical thinking, rational discourse of transparent information and democratic consensus driving our political economy rather than whatever it is we have today.

Where are the “Enlightened” humanistic adults among the sociopaths behind the curtain?

>>> I would recommend all underwater homeowners to default. And blow the money on a nice holiday somewhere. At least you will have that. And while you are at it – drop health insurance en masse – may as well make that change as well. As those insurance co’s are really taking blood on what they charge. <<<

I like the way you think, anne. :)

But how about taxes? Should we keep paying that?

Psychoanalystus

What’s a luxury good or service?

I hear economists talk of basic goods as being “sticky” in an economic environment of deflation. Well, the same can be said for people reducing their lifestyles. Many of their material consumption choices can said to be “sticky”. Reducing our lifestyles is a slow process, much of it forced on us, and this is what the government and fed are trying to manage. Perception of certain goods move from necessity to a luxury.

But as the incessant economic erosion continues, more and more goods and services we have taken for granted will become “luxury” goods, so our material standards of living will continue to erode. At points in time, critical mass will have been reached and ever larger chunks of the economy will slide down hill, but without structural change in the U.S., the erosion process will continue. We’ve all seen the movie scene, where a bus crashes and slides to the edge of the cliff, all is quiet in the immediate aftermath, until a creak and large groan is heard, and the bus settles to an even more precarious position.

After a crash, people will take stock, and continue to adjust or be forced accept a new lifestyle in a slow, drawn out process. Gaps will occur in the family budget, alternative sources of cash will spring up such as default strategies on mortgages, borrowing from Gramps and Gram, part-time jobs, temporary work, etc, etc. This money will be used to plug the gaps, but more and more consumption choices will move from necessity to luxury.

They will squeeze by until it gets down to paycheck to paycheck and finally find themselves sliding out of being “middle class”. But ever so slowly, hope will fade, anger will pursue, and when critical mass is finally reached demand will made. Until that time consumer spending will continue to fall in fits and spurts, but always and ever falling.

Oh, I forgot to add the good news. As we get poorer and poorer, people will begin to realize it isn’t how many toys you own, it how many toys you own in relation to your neighbor. This is where our sense of self comes from in America (and probably everywhere else in the world). So that warm fuzzy feeling from being one step ahead of our neighbors, it’s still attainable, just more difficult achieve.

There is some distance between “not de-levering” and “binging at the mall on luxury goods”. If it is reported in the Murdoch rag it is likely propaganda. The Journal’s editorial page would certainly prefer that workers simply disappear along with pay checks when jobs vanish.

People, workers, don’t disappear. So they are not paying their mortgage but continuing to purchase clothes, food, school supplies. They mostly continue to pay their credit card bills too, and to eat and see friends and provide themselves small entertainments.

People are not spending money on goods rather than debt service because they are loosing faith in money as a store of wealth: they are spending money because in a non-agrarian, monetized civilization one must spend money or get someone else to spend it to feed and house yourself.

If you are part of the majority of Americans who have a lot of debt, debt that several large industries who profit from it spent a lot of money to promote for the last thirty years, the service of which has eaten away your margins as your income for whatever reason has declined, at a certain point you stop servicing your debt in favor of your daily needs that do not disappear simply because your income has.

With 5 applicants for each job on offer, 4 job seekers are by definition structurally denied the opportunity to work for income with which to de-lever. When your income goes down, what may have appeared to be a prudent level of debt service at some point proves not to be.

You are in a lease or mortgage for your dwelling space that has cash flow implications as well. You and your dependents have periodic needs: transportation, three meals a day, health care, insurance etc. etc.. None of this stops because of a crimp in your income stream.

For the last two years as all of the economic institutions of our civilization have insisted that the Financial Industry that got us into this mess needs all of our resources to get us out of this mess, what has really been happening is the last minor flows of cash through the real economy have been drawn down forcing the liquidation of whatever wealth remains for the unemployed our underemployed.

Working Americans have a better picture of what tomorrow holds than most economic commentators: they see no prospect for any significant improvement in their cash flow in the foreseeable future. As a consequence they are saying screw the debt, I need to go on living until things improve whenever that may turn out to be. I’m headed to the mall (between the mall and Walmart, where else is there to head?).

I’m not sure that people who are defaulting on their mortgages are spending the money on luxuries. They may be spending the money on health insurance, car repairs, food, school supplies for their children. We don’t know. The end result is the same: people are not paying down debt. But it is possible that they really can’t afford to pay down debt.

Having said that, I will add that I was at the Mall of America yesterday, and it looked pretty busy. However, if people were not spending money there, the nice vendors would be out of business. So, the American consumer can spend no money except on absolute necessities and deepen the current recession, or he/she can spend extra money, help the economy and be guilty of financial irresponsiblity.

Are defaulters spending their former mortgage payments? Judging from personal experience and the stories of friends in similar situations, I would say definitely YES!

Why? Let’s run through a few of the big reasons. First, we know that most defaulters are people who have lost jobs/income AND are underwater. For instance, if a couple loses one income and decides it isn’t worth trying to keep their underwater house, but they need to stall for time (or sincerely believes HAMP will help them, despite all the evidence to the contrary). They will shift into emergency mode, dropping their biggest expenses (mortgage, probably property taxes, basic maintenance/home repair) and spending much of the savings.

People who are downwardly mobile but remain in place do not wish to appear downwardly mobile and will try to go on spending as before but with greatly reduced income.

What people not in their shoes need to understand is that defaulters are worried about their lenders taking any pot of savings from them. Thus there is really no incentive to save the mortgage money, as they are worried the bank will find it and demand it and some point in the future.

In sum, every aspect of their lives dictates that they spend whatever income and savings they have (and even rack up further debts on credit cards) because defaulters know they are quite likely headed for bankruptcy anyway and the best strategy they can devise is to maintain appearances right up to the day (or night) when a van appears to pack up their belongings. You might get lucky. A new job. A raise or promotion. A big contract. The market might rebound. Or the government might finally hit upon a program that will actually (against all odds) help you. Or the world might end and you needn’t have worried about all that other stuff.

Take it from me. Olick is right. And if you were in their shoes, you would likely behave just the same way.

At the same time it is calling for “shared” sacrifices to reduce the budget, America’s elite is reacting with horror to having tax rates return the relatively low rates of last two years of Clinton’s administration. Apparently, sacrifice for them is having to read about people eat cat food to pay for medical care in the N.Y. Times or Washington Post.

By the way, most of that deleveraging that occurred in 1929-1933 was the result of defaults in the private sector. Government debt indreased in those years, as Amity Schales and others like to point out, however without the context that it increased despite severe austerity and tax increases due to the fact that tax revenues collapsed faster than the Government under Hoover could cut. In fact most of the current debt is due to the collapse of tax revenues.

Government debt, as Alexander Hamilton pointed out, is different then a private person’s debt. As long as the credit of the State is maintained, it can go on indefinitely, and in fact creates an interest in the stability of the State. Although we are still suffering from the poor economic management of the last 45 years (and to some extent, as long as Obama shares the views of Goolsbee, Geithner, and Summers we still be economically mismanaged), the long term trend of economic growth of the U.S. should be between 2.5 to 3.5 percent, based on population growth of 1% a year and productivity 1.5 to 2.5 percent. Retrenchment in defense spending, allowing all of the Bush tax cuts to expire, a trade policy based on the reality of the Japan’s and China’s mercantilism, infrastructure spending (roads, railroads, bridges, tunnels, airports, air-traffic control, and pollution control (waste water and superfund clean-up) and following through on the current policies to restrain the growth of medical care will probably lead to surpluses by the end of this decade. The biggest current negative is the Democratic neo-liberal view of the importance of Finance capitalism, and the Government subsidy to finance, and the unimportance of manufacturing, infrastructure, and agriculture, a view which pretty much epitomizes Obama and his top three economic advisers/officials.

a recent WSJ study put that deleveraging myth to rest…although the total value of home-mortgage debt and consumer credit outstanding has fallen by about $610 billion, to $12.6 trillion, according to Fed stats, the WSJ research of that data showed that all but .08% of that has been banks and other lenders charging off mortgage and consumer loans…it aint deleveraging, its defaulting…

http://feedproxy.google.com/~r/wsj/economics/feed/~3/_8QrLdFX1Nk/

I always respect what people like “GW” and Karl Denninger have to say, but I cannot shake the feeling that they are seeking facts to fit a narrative that is already fixed in their minds.

I saw Karl’s post yesterday, and the part that bothered me the most is exactly what GW quoted. That quoted text mixes two very distinct metrics, outstanding household debt and household net worth, in an attempt to prove the point that households are not deleveraging. If anybody but Karl, who I find to be scrupulously and brutally honest, had said that, I’d question their integrity.

How precisely, can household debt, which relies on the value of the home at time of purchase, go down as quickly as net worth, which relies in part on the value of that home today, which in some cases is off by 80% and has wiped out any equity in the home? Outstanding debt can only fall as quickly as net worth if banks write off the debt, which is only being done in cases of default.

The fact is that U.S. households have reduced outstanding debt by $162 billion from the peak of July 2008 through July 2010, and the last Flow of Funds report shows further reduction (see tables D.1 and D.3, for example). Although the Fed used to tell us exactly how much debt was extended and how much was retired (I’ve found examples that flowed through Census reports), it no longer does so, which means that any conclusions about where the household debt reduction is actually coming from is a guess.

In that same period of time, the financial sector has reduced its outstanding debt by almost 10x that of the households, or $1.4 trillion. These write-offs are for loans extended financial players like hedge funds, who more likely than not used that leverage to increase their bets in the casino.

While there is no doubt that certain segments of the household sector are horribly overleveraged (i.e., anybody below the top decile) and need to deleverage, it appears that the financial sector’s own bad debts were the cause of the financial crisis, so the fact that it is deleveraging is a good sign.

What I fear most is that the banks are using myth-to-market on non-performing household debt they are holding because any write-downs of those debts will also result in write-downs of 10x or more of financial sector debt used to purchase junk derivatives.

The “binge” on “luxuries” is anecdotally true here (southern California). The defaulters I know live large — trips to Hawaii, new cars — while non-defaulters, despite higher incomes, scrape by.

But attempter is right: it would be far better to see data to back it up on a larger scale.

Yet even if the binge is widespread, is it irrational? If high inflation is the nearly certain endpoint of trillion-dollar deficits, then why wait? Why save to buy a car or trip to Hawaii that may cost 10 times as much 10 years from now?

In personal finance, for those born after 1960 or so, debt-fueled profligacy has usually outperformed conservatism. Did this end with the housing crash? No, the profligate now live in their homes free, and keep going to Hawaii. High inflation will rescue them yet again, by reducing the real cost of a fixed mortgage.

Moral hazard is not just for banks.

The mere fact that the defaulters you know are living large does not mean they have not, in fact, deleveraged. Even if they have incurred more debt on paper, if they are defaulting on non-recourse mortgage debt, it is far more likely than not that they have actually “deleveraged” in real terms (i.e., a net decrease in debt). Moreover, the defaulters you know likely can afford to live large without incurring additional debt, if they are defaulting on non-recourse mortgages.

The fact that these defaulters continue living in their homes without paying their mortgages seems to confirm my fear that banks are pretending that many defaults remain as performing loans on their books. In other words, in real terms, there has been a lot more consumer deleveraging than is apparent.

One final point, which is that according to neoliberal principles, defaulting on a non-recourse mortgage that exceeds the value of the property is the right thing to do economically and morally, if doing so yields a reduction in overall debt level or increase in savings. If a corporation’s only social responsibility is to maximize its profits, it would seem that a real person’s only social responsibility is to maximize her net worth.

This is what is known as reaping what you sow, and it may very well prove to be the death knell of neoliberalism.

Yet even if the binge is widespread, is it irrational? If high inflation is the nearly certain endpoint of trillion-dollar deficits, then why wait?

The answer is to spend the money on useful things for the coming Depression. Tools, skills, spare parts, a piece of land for a large garden or small farm, a small biodiesel converter to run a tractor, a tractor…..

But anyone still bingeing on crap is not just irrational but insane.

You may want to add guns to your list too. And, like I said above, buying a little gold and silver may not be a bad idea either. Do you think the “masses” are smart enough to do that?…

Psychoanalystus.

Just a simple, maybe stupid question: If the economy is not deleveraging then how come M3 is declining? How does the money supply shrink other than debt repayment?

Good question.

Another good question is how is it that an almost $500 billion dollar reduction in outstanding household debt doesn’t count as “deleveraging? when a large majority of Americans have no savings and live paycheck-to-paycheck?

http://ampedstatus.com/census-bureau-poverty-rate-drastically-undercounts-severity-of-poverty-in-america

In California, if they’ve defaulted on a real estate loan that secured by real property, it doesn’t matter (for 99%+ of debtors) if the debt is recourse or non-recourse. California’s “one action” rule says that the debtholder must choose to collect the debt non-judicially or judicially, not both. It can sell the underlying asset (e.g., house) at a non-judicial sale and keep the proceeds but not collect anything else or it can go to court and foreclose in a judicial proceeding and also try to get the debtor’s other assets. But a judicial foreclosure takes a lot longer, is a lot more expensive, allows the debtor to “redeem” (i.e., buy back) the property for a year (which essentially means the debt-holder can’t sell it during that time), and credit the debtor with the “fair value” of the house which usually exceeds the price it will get at a foreclosure sale (and gives the debtor leverage in negotiations with the debt holder). Unless the debtor has a lot of unemcumbered assets to grab, the debtholder will use a non-judicial foreclosure. Virtually all foreclosures are done non-judicially.

The above was in reply to Tao Jonesing

September 19, 2010 at 2:21 pm

I hope that ppl are smart enough to buy physical gold and silver with the money they spare not paying their mortgage.

Very cogent and insightful reporting. Thank you very much.

One observation I’d like to make (and yes, it’s based on anecdotal evidence) is that I see more and more people paying with cash, rather than plastic. To me this is indicative that these people are defaulters (and credit card max-out-ers) who have already ruined their credit (bravo!!!) and thus no longer enjoy credit “privileges”.

Psychoanalystus

TheftOpen theft and open corruption is the biggest problem. The U.S. has legalized bribery (13,000 ++ lobbyists bribing the Congress) even though taking a bribe is a treasonous offence. Not in the U.S.; here it’s mere lobbying.

Well, Napoleon taught us the best value for your investment is always a political contribution and The Financial Crime Cartel knows that better than anyone. And the Boiled Frogs nation that Americans have become is gobbling up political propaganda baloney and handsomely and meekly pays the thiefs to rob them.

With some 6 million homeowners not making mortgage payments (some loans are in trial mod programs and paying something but still in delinquency or default status) , this is probably freeing up roughly $8 billion in cash each month. Assuming this cash is spent (not too bad an assumption),

Actually that is a terrible assumption. Mr. Zandi’s figures suggest he is assuming that most of those homeowners are “ruthless defaulters” (i.e., someone who could pay but isn’t because their home is worth less than the mortgage, and his numbers work out to an average $1333/month mortgage payment). I’ve never seen good data on what percentage of defaulters are “ruthless” but it seems to me a better assumption that the minority are ruthless and the overwhelming majority are facing a financial crisis like the loss of a job. In that case, there is no money for either the mortgage payment or shopping sprees.

There is no evidence that the recent increase in government debt has “crowded out” private investment. This is another myth that is often repeated ad nauseum.

In fact, given that our economy is demand constrained, policies that boost overall demand would result in increased investment, as we have seen happen in the case of stimulus spending. This has been repeatedly pointed out by the likes of Krugman and Delong, but to no avail.

I am just amazed that with all the intelligent people I see posting, no one is talking about globalization which is the root of the problem. There is no why the the American worker can compete with the cheap labor that corporations are now buying overseas. We have no labor because we produce nothing. This is simply the balancing of the GLOBAL economy, and there is a lot more grief coming down the road.

I grant the premise that people not paying their mortgage have more cash then they would if the paid their mortgage. And if they are unable to pay their mortgage, one would imagine they have more pressing bills, such as paying for food. So yes, there is still a ton of debt on the books and people are spending money they don’t have. Please don’t pretend, however, that there is a large portion of the population out their who is buying luxury goods rather than paying their mortgage. That is ridiculous, ridiculously callous.

“Easy money is a hell of a drug.”

“The storyline about corporate America being flush with cash is another lie. Corporations have ADDED $482 billion of debt since 2007. Corporate America has the largest amount of debt on their books in history at $7.2 trillion.”

This is not a automatic contrary position – that you have no cash and you have debt. The question really is how much debt *and* cash is held by corporations. Wasn’t there a previous post saying the S&P 500 companies had almost $400B in cash on hand?