It’s been so long that America has had a regulator that is serious about regulating that it’s hard to remember how they operate. Former Federal prosecutor, now superintendent of New York State’s Department of Financial Services, provides a long-overdue and welcome reminder. Lawsky has taken a role that is usually toothless, that of a state banking regulator, and in an impressively short period of time, has made himself a force to be reckoned with. He stunned and outraged Federal regulators when he took a money-laundering probe of Standard Chartered a tad more seriously than anyone expected.

To make a long story short, the other regulators were preparing to sign off on a deal based on Promontory Group piously reporting that only $14 million of transactions were out of compliance (this after Standard Chartered had defied previous consent orders). Lawsky issued a blistering order that documented in detail the willful defiance of US rules (including the bank’s US general counsel overruling the strong recommendation of outside counsel regarding the need to change procedures and drop a lot of the business they were doing). The bank settled with New York for $350 million and admitted to $250 billion of transactions being in violation. That’s four orders of magnitude more than what Promontory found. Lawsky also fined Standard Chartered’s accountant Deloitte $10 million for its role in this scheme.

Needless to say, it’s a safe bet that Lawsky hasn’t been invited to participate in any bank investigations since then. But he’s getting his nose into the tent despite them. For instance, the BBC’s famed business commentator Robert Peston wrote on Thursday:

New York’s Department of Financial Services is very much the late arrival to the worldwide investigation into whether up to 15 huge global banks manipulated the foreign exchange market.

But its request for documents from banks will disturb them, because it has a reputation for being particularly aggressive – as the UK bank Standard Chartered found to its cost when the Department of Financial Services pursued it for breaches of money laundering rules.

And we see that confirmed today in one of top Bloomberg headlines, Currency Market Unsettled by Trader Exits on Lawsky Probe. Key sections:

The foreign-exchange trading business was in upheaval across Wall Street as senior executives resigned and others were fired amid an expanding probe of possible currency manipulation.

Benjamin Lawsky, superintendent of New York’s Department of Financial Services, asked more than a dozen firms including Deutsche Bank AG (DB), Goldman Sachs Group Inc. (GS) and Citigroup Inc. (C) for documents on their currency-trading practices, said a person with knowledge of the matter. Deutsche Bank, the top foreign-exchange trader, fired four dealers after an internal probe, people with knowledge of the move said. Goldman Sachs lost two partners while Citigroup said its foreign-exchange chief will leave in March….

Lawsky, who has authority over financial institutions chartered in his state, including several non-U.S. banks that do business in the country, asked for traders’ e-mails and instant messages to review whether they manipulated currency rates, according to the person. While he isn’t authorized to bring criminal charges, he can make referrals to prosecutors.

“You have a law enforcer with zeal who no doubt has numerous weapons, and he’s prepared to deploy them on behalf of the law and on behalf of consumers,” said Bartlett Naylor, a lobbyist for Washington-based consumer group Public Citizen. “The record shows that’s missing in so many other places including the federal level.”

Unfortunately, even if Lawsky uncovers grotesque abuses, prosecutions are unlikely. Lawsky was appointed by Andrew Cuomo, and the rivalry between Cuomo and New York Attorney General Eric Schneiderman is fierce.

Lawksy is moving on a second front that is more germane to most citizens, that of servicing. Readers may recall that all the so-called mortgage settlements did little to change an incompetent and abusive servicing industry. Servicers are set up as factories. They send out bills to customers on a large-scale basis, record payment information and remit that to securities administrators who then compile reports for investors. But as a low-margin business, they’ve never invested in the infrastructure to do much (really anything) customized, such as correcting errors or handling delinquent loans and foreclosures properly. Worse, as loans have been transferred multiple times and servicers fired their experienced personnel during the crisis, their systems are simply not up to the job. And rather than force servicers to fix that in the various settlements, the agreements instead went through the pretense of imposing new standards but allowed astonishingly high error rates, including 1% wrongful foreclosures. That would have amounted to 22,000 homes from 2008 to early 2012.

And since these agreements were signed, servicers have thumbed their noses at them, ignoring requirements to provide a single point of contact for delinquent loans and on a widespread basis and failing to stop dual tracking (the process of continuing to foreclose while evaluating a borrower for a mortgage modification or other relief). And it’s easy to see why. In their contracts with mortgage trusts, servicers are paid to foreclose and not to do modifications or other borrower handholding.

The Feds apparently hoped to finesse this problem (which is rooted in deficient computer systems and records) by getting banks to move their servicing over to new players, particularly smaller “combat” servicers who specialize in handling portfolios with lots of delinquencies. But there’s a big fly in that ointment. High quality servicing does not scale. And Lawsky has apparently figured that out.

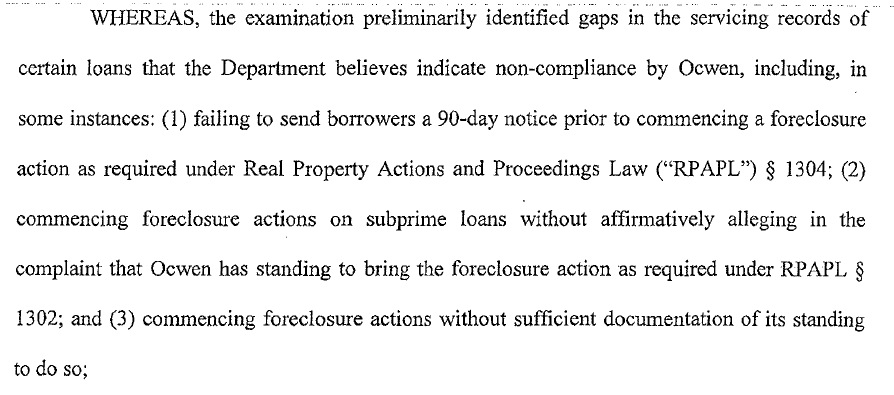

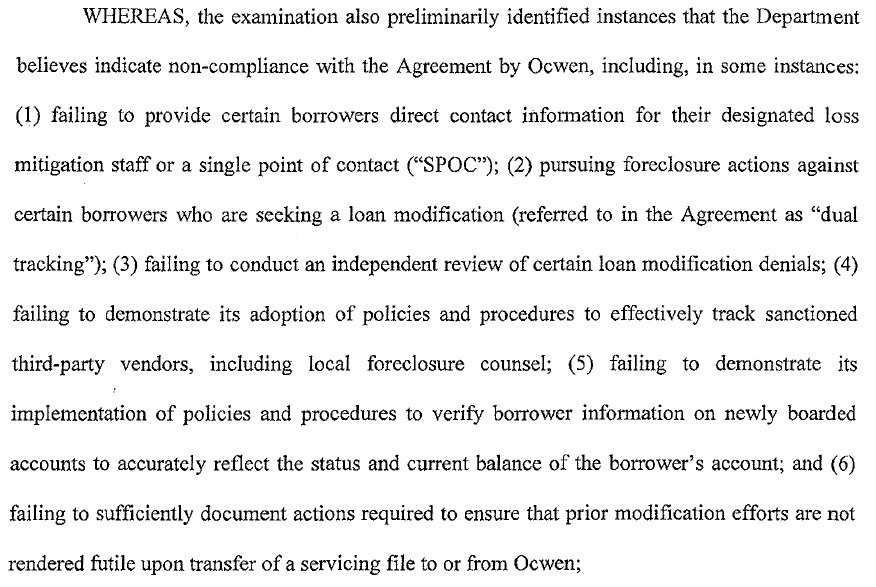

Much to the consternation of the mortgage industry, Lawsky is blocking the transfer of mortgage servicing rights to $39 billion from Wells Fargo to Ocwen. Ocwen is already subject to two orders from Lawsky’s office, one in 2011 and one in 2012. The December 2012 order is based on a limited exam earlier that year that uncovered a number of deficiencies:

In other words, there was evidence of serious deficiencies in the handling of delinquent mortgages and even in current ones (failing to verify information on newly boarded loans). Lawsky ordered that an independent compliance monitor conduct a comprehensive review and report back to the Department. The monitor was to develop a list of needed corrective measures and oversee their implementation. Lawsky’s freezing of the Wells Fargo deal suggests that either the process was not completed or that Ocwen and the Department are still arguing over some of its findings.

And Lawsky is hardly alone in finding fault with Ocwen. The Financial Times notes:

The DFS halt follows a state and federal settlement announced two months ago by the Consumer Financial Protection Bureau and authorities in 49 states. The CFPB sued Ocwen accusing it of years of “significant and systemic misconduct that occurred at every stage of the mortgage servicing process.”

CFPB said: “This misconduct included unfair shortcuts, unauthorised fees, deception, and other illegal practices.”

As part of that settlement, Ocwen was required to provide $2bn in loan modification relief to homeowners and $125m to consumers that were foreclosed upon.

Not surprisingly, the industrial is in denial that the way servicers routinely operate isn’t up to snuff. Again from the Financial Times:

The halt of this sale is likely to force banks to think more closely about who they seek as buyers of their mortgage-servicing rights. “It’s not like you have an infinite pool of entities wanting to buy them,” said Greg Lyons, partner at law firm Debevoise and Plimpton. “You wouldn’t think that selling a bunch of MSRs to Ocwen would create a problem, they’re not a fly-by-night company.”

While Ocwen is indeed not “fly by night” in the sense that they don’t operate out of a strip mall, don’t change the fact that their conduct has fallen well short what various settlements mandate, even with their big loopholes. But the servicers continue to get away with so much bad behavior so often that mortgage industry incumbents are shocked and offended when they are told to toe the line.

So I hope those of you in New York State will call or write Lawsky’s office to tell him you applaud his work. Although as a former prosecutor, he’s presumably thick-skinned, Lawsky is getting heat from the mortgage-industrial complex. A show of support would be welcome.

I’ll write him a letter. And my home residency is in Massachusetts.

And the beat goes on. Servicers such as Ocwen continue to thumb their nose at the law and the Promontory’s of the world continue to blow smoke up our asses that the banks and servicers are “mainly” in compliance.

While I applaud Lawsky’s work, until these banks and servicers are met with more than fines the looting will continue.

In the days of the S&L collapse, state regulation was important. While the fraudulent practices infected institutions everywhere, it was in the South and Southwest where state regualtion was most loose that both failed institutions and actual dollar damage were concentrated. The fraud was limited in number of institutions and dollar size in places where regulators had a modicum of resources and paid some attention. Kudos to Mr. Law’s for earning his taxpayer funded paycheck. It looks like his salary will prove a bargain for ordinary citizens in NY while the other victims are getting a free ride on his activism.

What happened to the AG? He started out so young and strong only to surrender.

My guess is that someone found a skeleton in his closet. Just like LBJ did in Chief Justice Earl Warren’s case when the president finally made him an offer he could no longer refuse to head up the commission investigating JFK’s assassination after he’d turned it down twice before.

I should have noted that my comment pertains to the last paragraph of arby’s comment:

Let’s hope Lawsky is not a “Pretender”…:)

Simple. The AG wants to be governor, and too much of New York’s coffers are derived from Manhattan being trendy driving up property values and exorbitant incomes in the city. Would an AG gain much traction running state wide when school funding is being slashed because of his actions? It’s why we need an active federal government because the states can be too easily captured.

Schumer’s behavior in the Senate isn’t surprising, and since Obozo went with Larry summers on the paltry stimulus,a state like new York can’t realistically join a good government lobbying effort without attacking their roads, schools, and infrastructure.

When W. was in office Democrats were the beneficiaries of much of his defense pork because they wouldn’t object if it was in their district and we old support him on other issues. Even the Teabaggers are vaguely aware of this and a re e annoyed the pork wasn’t in their district.

New York will never produce a liberal champion until the state’s economics or how we fund the states change. Politics is local. Detroit won’t produce advocates of mass transit, Idaho won’t produce Atkins diet users, and Vermonters will not put corn syrup on pancakes. The solutions won’t be found in states dominated by an industry.

I seem to recall medical marina outlets in California lobbying against looser laws because their value comes from running a controlled but cheap to produce product. States with smaller medical marina lobbies have moved past California on legalization.

New York also has a crazy-ass system of state government which has proven very hard to clean up. The legislature is the worst in the nation. Our “checks and balances” consist of Governor vs. Comptroller vs. Attorney General — which usually works fairly well, actually, but it has its downsides.

Well before the S+L crisis most consumer banking was intrastate. But when the regulators seized insolvent thrifts there was little reason for a potential buyer to take on a business with negative net worth, EXCEPT the legal authority to operate in a different state. Once there were a fair number of these effectively interstate banks created, congress started looking at whether the depression era regulations against interstate banking still made any sense, and voila, another round of deregulation.

I live on the other side of the park, Yves, and I’ll write the aptly named Mr. Lawsky a letter.

New York State Department of Financial Services

One State Street

New York, NY 10004-1511

Good for him…I’ll write.

It’s been known ever since In re Jones that Wells Fargo’s accounting software is designed so that mortgages are routinely mis-amortized. I have seen no indication that this problem has been resolved…has anyone else? So not only is WF selling MSRs to a shady company, Ocwen, but we have no assurance (so far as I can tell) that the loan amounts are actually correct. In fact, we have every reason to assume that some (possibly large) portion of the loans that WF wants to hand-over to Ocwen, have been miscalculated. And adding another layer of corporate bureaucracy between themselves and the borrowers they’re screwing over is no doubt seen as a benefit by WF. Just sayin’…

Indeed, more cases should cite In Re Jones. Frankly, I’d consider the crimes proven in that case sufficient grounds to revoke Wells Fargo’s permission to operate in New York State entirely — its operations would pass into a state-appointed receiver in that case, I believe.

What Mr. Lawsky is doing is great! I hope he doesn’t have any private activities that are none of our business, but which would be embarrassing if publicly revealed. We can be quite sure that the Powers-That-Be have people looking into his personal life.

Peston famed Yves? Now that made us giggle here. BBC economic coverage would benefit from claymation. Indeed, Sue and I thought Peston such a character, until we realised Wallace and Grommet weren’t on set. Lawsky seems to stand out as unique across all regulatory activity. Can we cope with someone telling us the truth from the molten pit of reality? Good luck to the guy. We could do with a successful model. I remain a bit sceptical he is that, but have fingers crossed. Thanks for the case material.

So Lawsky was appointed by Cuomo? All I need to know. Rest assured that Lawsky will either sell out, be blackmailed into backing down, or fired before anything of real substance happens. My personal guess is that he’s just working himself up the ladder to the point where the payoff will be really generous. Another year or two, he’ll be a senior exec for Citi or GS. However could I possibly know this, and how could I possibly be so cynical?

Simple: Because he’s in government. There is no one — NOBODY, not one single person — at any level of regulatory, legislative, judicial, or executive government who is not a crook and a sellout. Even those like Judge Rakoff are just making a show, knowing they will ultimately be overruled by appeals courts. They are ALL just playing a game of “look good while letting the looting and lawlessness continue unabated”.

Um, so far not. Geithner and the Fed wanted Lawsky’s head over his intervention in Standard Chartered, and Cuomo didn’t withdraw his support.

With all due respect, it’s about cover. Cuomo and all the other officials near the top of their respective pyramids have to give some appearance of doing the right thing. Just as the Dems have rotating villains, so do TPTB have their little marionettes that they let perform to distract the masses. Obama, Holder, Cuomo, Schneiderman, Warren, Lawsky, etc., differ only in that the first four have been shown to be sellouts while the true nature of the last two has yet to be revealed for all to see. But…patience!

Cuomo’s actually kind of stupid. This means he’s perfectly likely to have appointed people without knowing exactly what they were going to do. His administration lacks consistency.

Schneiderman has not been demonstrated to be a sellout — he’s just not done very much.

You are appallingly wrong. He sold out each and every homeowner in the US by abandoning the attorney generals who were fighting the mortgage settlement. Obama flipped him to his side and the opposition collapsed, allowing the Administration to push the deal over the line. I felt like I had been punched in the gut by Schneiderman’s betrayal.

He sold out WAY WAY too cheap…..for being on a bullshit Federal task force (one of five co-chairmen) which Obama no doubt winked and nodded would set him up for better things and sitting in Michelle’s box in the 2012 SOTU.

Thank you for this unvarnished truth, Yves. I unsubscribed to the Schneiderman newletter which reports his meaningless “achievements.” In a storm of forgery, perjury and massive securities fraud, the New York AG has chosen the path of no resistance.

Wish you were wrong, Jess but I agree. All of these “settlements” are nothing but big time wrestling. Not one homeowner has been made whole and not one bankster will ever be indicted save a few low level mortgage brokers and others doing their Master’s bidding.

He got $350 million for New York State and embarrassed the Feds into getting more.

How much do you think they would have gotten on the path they were on, with the Promontory claim that only $14 million in transactions were out of compliance? That would have gotten a free pass were it not for Lawsky.

It’s not just the servicers, of course. A Lee Cty, Fl rocket docket judge(?) just issued sale dates on stacks of cases based on the bank’s lawyers just showing up. A credible source said when one of them was asked for the note, he shrugged his shoulders and said I don’t know, it’s lost. The judge stamped the paperwork anyway while exclaiming “next!”

It’s surfacing that there’s a partnership between some so-called foreclosure defense lawyers in Fl and foreclosure mill lawyers. No wonder everybody loses.

They key to regulation is to be able to get in quick, do the investigation with authority to interrogate and be able to present findings in a transparent form of public scrutiny. Nicked in the UK you get held in unsavoury conditions and are told if you don’t say anything you later rely on in court it probably won’t be believed. This is almost the opposite of the process involved in investigations into ‘authority’ – cops, government, finance. In the latter we get all kinds of assurance on due process, see almost no ‘convictions’, loads of ‘lessons must be learned’ assurances (usually followed by another series if the same mistakes), plenty of evidence of cover-up and lying, enquiries that take 25 years and cycles of regulatory change that produce no change at all, even in the reasons for regulatory change.

I can’t judge Lawsky, but I can judge the lack of simple criminal investigations of various financial frauds against the crimes of those I once brought to book. The former are nearly all more damaging to victims, the processes of decent business and involve more criminal intent. We have already missed the point once we need a Lawsky. Much of this could have been dealt with by some empowered flat-foots we allow to investigate teeming, lading, blackmail and murder. Small teams of low ranking officers have brought down £50 million plus fraudsters once allowed to act by the authorities, usually because the offenders have become politically disposable.