Even though foreclosures and bank servicing abuses have virtually disappeared in the eyes of the media, it’s quite a different story in the courtrooms of America. Banks continue to proceed with foreclosures, too many of which are based on bogus charges or other servicing abuses. And as we’ve stressed, when the initial foreclosure action is justified, servicers too often charge impermissible fees or refuse to engage in good faith remediation efforts, as is now required for under new servicing standards.

One of the recidivist bank abusers is Wells Fargo. Not only does the bank engage in many of the common bad servicing practices, like force placed insurance, whistleblowers have charged that the bank also engages misapplying payments when borrowers fall in arrears, a practice known as “pyramiding fees.” Yet Wells is remarkably brazen, and has repeatedly tried to paint itself as virtuous and its critics as ill-informed.

This case, sent to us by April Charney, gives a more accurate picture of Wells’ behavior in foreclosures. We’ve embedded it at the end of the post and encourage you to read it in full.

Here, the borrower, Emily Harlin, had fallen behind and Wells initiated a foreclosure. Harlin and Wells reached a settlement in December 2010 in which Harlin would stay in the home but would be required to make no payments. Since the bank still retained its other rights under the mortgage, it would be able to recover the principal balance plus applicable charges from the proceeds of the sale of the house. The settlement also stipulated that Wells would repair Harlin’s credit record.

The very next month, in January 2011, Wells filed a new foreclosure action against Harlin. The bank also started to hound her via debt collection notices and even visits to her home, and refused to remove the information in her credit record related to the past foreclosure effort. Harlin sued Wells.

Harlin’s suit included a cause of action based on South Carolina’s Unfair Trade Practices Act (SCUPTA). Wells sought to have claims based on SCUPTA dismissed. The argument? That Wells had already settled all those claims in the National Mortgage Settlement and Harlin had no right to bring them.

The judge rejected Wells’ motion on the SCUPTA issue without explaining his reasoning. Wells filed a motion to reconsider. The judge roused himself to explain his logic in denying the motion to reconsider. While his decision maintains a suitably unruffled tone, it’s evident that issued a relatively long ruling on a comparatively minor matter to establish a clear precedent and to make it difficult for Wells to make similar bad-faith arguments in similar cases (his calling some of Wells’ arguments “disingenuous” is a tell).

This is the key background:

Having already received ample briefing on the meaning of the Consent Judgment [the National Mortgage Settlement], this court requested additional briefing on the adequacy of the South Carolina Attorney General’s alleged representation of the Plaintiff [Harlin], considering that the vast majority of the monies obtained by South Carolina in the National Mortgage Settlement went to the state’s general fund, and not to victims of unfair mortgage practices.

Translation: the judge wasn’t buying what Wells was selling. This part is priceless:

The South Carolina Attorney General filed two letters with this court, the first opining that South Carolina specifically reserved private causes of action citizens may have under SCUPTA, and the second opining that the Attorney General’s representation in obtaining the Consent Judgment was, therefore, constitutionally adequate, regardless of how the monies from the settlement were used.

In other words, the South Carolina Attorney General said that Wells’ argument was patently false.

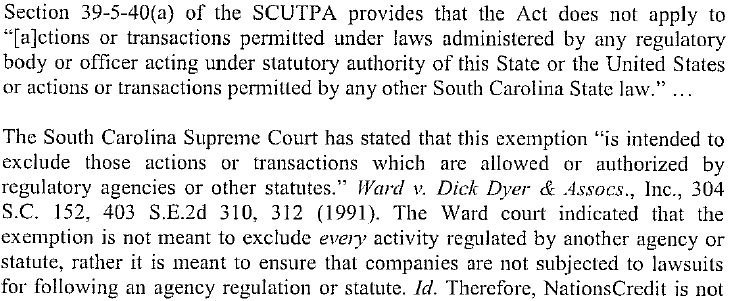

Beaten on that front, Wells tried the new tactic that it was exempted from SCUPTA “because banks are part of a regulated industry.”

In the ruling, the judge cited the section of the Consent Judgment that exempted individual borrower claims from the mortgage settlement, and dissed Wells’ argument that those claims had to be settled because it paid $5 billion and it would never have paid so much if it didn’t get that too (I am not making this up). He also cited other decisions in other Federal courts that reached the same conclusion.

As for the argument that banks were exempted from their bad conduct under SCUPTA by virtue of being regulated entities, Wells had tried relying on an unpublished Fourth Circuit case to strike references to pleadings in the National Mortgage Settlement. The judge pointed out that:

The Fourth Circuit ‘ordinarily do[es] not accord precedential value to [its] unpublished decisions…and they are ‘entitled only to the weight they generate by the persuasiveness of their reasoning.

Amusingly, the judge used that very same case to hoist Wells on its petard as far as the “we banks are above SCUPTA” argument. It cited this portion of the ruling:

The judge drily noted” “Although an unpublished decision, the court finds Beattie to accurately state and apply the law, and also finds the reasoning of Beattie persuasive on this point.

Consider what Wells did here. It made a simply ridiculous argument before the judge, and then tried another (that the bank didn’t have to obey South Carolina consumer protection laws) when the judge made his skepticism clear. This may simply be reflex on behalf of the bank’s attorneys, that if they keep throwing enough motions at borrowers, some won’t have the acumen to beat them back, and others will be overwhelmed by the cost of fighting a war of attrition. The judge appears to understand full well what is going on and isn’t cutting Wells any slack.

I mentioned this case to a colleague who has been contesting mortgage and foreclosure abuses since 2010. He said he thought it was a sign of a continuing shift in attitude among judges. Even though there is still a large cohort of judges who will rubber stamp bank foreclosures, there is another contingent that thought the mortgage settlements would end or at least reduce bank bad conduct and sloppy paper trails. The fact that all the pre-settlement foreclosure abuses are continuing just as before is leading some judges to take a much less forgiving stance with banks. But while an important step in the right direction, it must seem like cold comfort to wronged borrowers who have to fight tooth and nail for justice.

Order-denying-Def-Motion-to-Reconsider

Order denying Def Motion to Reconsider

Pretty well. It is high time that the big banks are leashed by the courts. “Even though foreclosures and bank servicing abuses have virtually disappeared in the eyes of the media, it’s quite a different story in the courtrooms of America” an apt statement.

Cindy

Yves,

You left out the best part. Wells argued that the private party claims reserved by the National Mortgage Settlement were claims brought by the state of Oklahoma, the state that opted out of signing onto the Consent Order.

From Judge Anderson’s decision:

“The court also reject Defendant’s argument that the third parties–‘individual mortgage loan borrowers on an individual or class basis’, refers to the state of Oklahoma.”

How many times do the courts need to sanction Wells for misapplying payments before either a meaningful penalty is imposed or some asses get thrown in jail?

Courts should refer to previous punitive damage awards when assigning punitive damages.

As in, “it is clear that a $3 million punitive damage award was not enough to deter Wells Fargo from its behavior, so we will have to apply a $30 million punitive damage award.”

Next case “It is clear that a $30 million punitive damage award was not enough to deter Wells Fargo from its behavior, so we will have to apply a $300 million punitive damage award.”

You get the idea.

Race is always an underlying issue in policy making in the US. Housing policy is probably at the top of the list.

Wells Fargo was/is notorious at steering blacks into mortgage loans they could not afford which would soon blow up. Banks like Wells Fargo are still in business because the government wants to keep the revolving door open with the criminals. Sure, Wells Fargo gets a small slap on the wrist on occasion by Uncle Sam but their crimes outweigh the impacts to the lives they affected. The puny fines are simply tax write offs.

I think the big bank attorneys all have some kind of betting pool going to see who can make the most absurd argument in court–and it looks like Wells is gonna win it. Between this and the in re Jones case, where they admitted to misapplying mortgage payments as a matter of course, it’s a wonder that anybody is still doing business with them. It’s almost like your run-of-the-mill bank customer is unaware of these practices…wonder how that could be?…

Diptherio,

I’m one of those doing business with Wells. I got my original mortgage in 2007 with Wachovia, and refi’d in Jan 2010 with WFC before I fully understood the game. WFC had the best deal for me, and unlike the first lender I applied to, approved the refi in spite of my lack of employment. Had I already been introduced to NC at the time, I don’t know that I still wouldn’t have done the refi to save over two points. In theory I may have swapped a bad note for a good one but from a practical perspective (and recent precedence), both notes would be fully enforced by local courts. Unless somebody has the money to pay off their mortgage, what choice is there but to deal with our corrupt and broken system. It’s the only one we have. Are there any ethical lenders? AFAIK, they all use the same conforming paperwork required for Fannie/Freddie/GSE sale/guarantee, and then with judicial blessing, do as they damn well please.

Nonconforming mortgages from credit unions are the best way out I can see.

“Conforming” paperwork which mentions MERS is illegal and invalid.

Note that this case is before a federal judge. This sort of bs argument sometimes flies with state court trial judges, but most federal judges are pretty good at sniffing out bs.