Yves here. Economists seldom take note of the fact that the degradation of skills at major banks has had serious macroeconomic effects. One issue has been described by Andrew Haldane: that as banks have become deregulated, they all have come to use very similar methods for making loans and taking other risks. This is particularly true in retail and small business lending, where individual and often character-based decisions made by loan officers have now been superceded by FICO-based models. The heavy reliance on FICO means that too many banks make similar lending decisions, exacerbating the tendency of banks to run lemming-like off cliffs all together. Haldane used a biological metaphor: that previously specialized types of financial firms and more autonomy in branch lending decisions led to more diversity in an ecological sense, which produced a more stable system. Less biological diversity, and less diversity among firms, increases systemic risk.

A second issue is that the abandonment of training of credit officers means that banks have effectively abandoned the small business lending market. Mind you, that does not mean that small businesses can’t get credit, but the sources consist of small credit lines associated with business accounts, credit cards, and secured lending (equipment lending, borrowing against real estate owned by the enterprise). The dearth of bona-fide small business lending is one of the big reasons why the Fed’s super low interest rates didn’t lead to much in the way of increased lending to smaller companies (note that the biggest reason was still lack of loan demand. Businesses don’t borrow unless they see a good use of funds).

As we wrote in 2013:

The comment above discusses the lack of small business demand for loans. Although that is the primary driver, there is a second one I’ve been remiss in not mentioning: banks are pretty much not in that business any more, and why the Fed ignores that and pretends to act as if putting money on sale will lead to more small business lending is beyond me.

The barrier to small business lending isn’t the economics; it’s that most banks no longer have that skill. I’m not making that up. In the stone ages of my youth, all the big banks (and the industry was less concentrated, so there were more “big banks” back then) had two year credit officer training programs. Those credit officers would do the analysis and make recommendations on big corporate loans. Some would eventually become branch managers, and way back then, branch managers would have the authority to approve loans up to a certain level. They used not only their formal analytical skills, but also local information about the health of the economy, the reputation and stability of important local businesses. If the local hardware store owner came in looking for a loan to expand, the branch manager would have an informed view on whether his estimates of how much and how fast his top line would increase after his build-out. He’d even probably know if his cost assumptions were realistic based on prior experience.

That capability has been abandoned in large banks. Branches are just retail stores; lending is productized and based on whether the borrower meets certain criteria set at much higher levels in the bank. You might still find the old-fashioned case-by-case type of small business lending in small banks, but it’s as dead as a dinosaur in the big ones, and the big ones dominate the industry.

This VoxEU article looks at whether loan officers are worth what they cost. It finds that they do in China and provides a framework for looking at that issue in other markets.

By James Wang, PhD candidate in Economics, University of Michigan. Originally published at VoxEU

Many lenders hire loan officers to screen soft information that may otherwise be ignored by credit scoring. However, in addition to their compensation costs, loan officers may have characteristics, such as being overly cautious, that could distort their decisions. This column documents the performance of loan officers using data from a Chinese lender. Despite the distortions, the loan officers contribute three times their pay in annual profits above what the lender could have earned by itself, even with the benefit of hindsight.

With the success of peer-to-peer lenders like Lending Club and Prosper, many lenders have experimented with alternative mechanisms beyond credit scoring.1 One such alternative is the increased reliance on soft information, which is subjective data that is difficult to interpret without loan officers. Loan officers, however, are not just costly in terms of compensation. Their characteristics – such as being cautious or having low ability – could distort their loan decisions to the detriment of the lender.

I consider the value of these loan officers using loan and repayment data from 2010–2013 for approximately 32,000 borrowers from a Chinese lender. This large lender specialises in unsecured, cash loans to households and small businesses. Loan officers view the borrower’s entire file including financial statements, references, notes, credit scores, and even photographs before choosing an approved loan amount.2

My job market paper calculates the value of hiring these loan officers by comparing them to an alternative where the lender only uses hard information such as income and credit scores (Wang 2014). It is important to note that this is not measuring the value of credit scoring. Risk-based pricing has been extensively used since at least the early 1990s (Johnson 1992) and their effectiveness is not in doubt. Einav et al. (2013) and Edelberg (2006) both provide compelling evidence of the strength of credit scoring versus exclusively subjective underwriting. My paper compares loan officers operating in conjunction with credit scoring versus credit scoring alone.

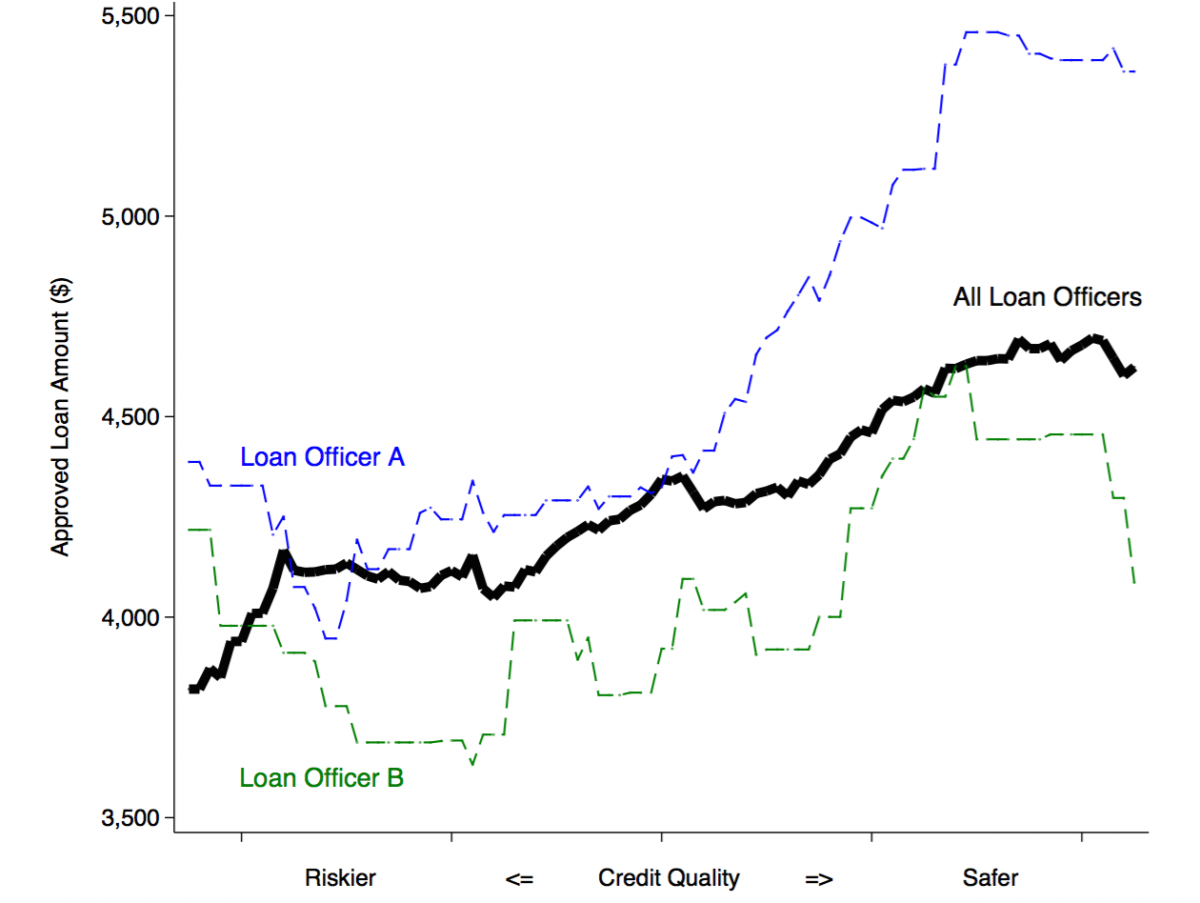

Despite the fact that loan applications are randomly assigned,3 there are differences across loan officers. Figure 1 shows the average approved loan amount plotted against credit quality. Notice that loan officer A approves a higher loan amount than loan officer B at every level. There are also differences in the variance of loan sizes as well as loan performance. To explain this, I lay out an empirical framework in the paper that can explain their behaviour, accounting for differences in risk attitudes, ability, and even overconfidence.

Figure 1. Average loan amount by credit quality

Notes: The graph displays the average approved loan amounts for 282 loans made by loan officers in June 2012 for a 48% APR, 24 month loan. Borrowers apply for a loan amount with a pre-set APR and payment length, and loan officers decide on an approved loan amount. Over 90% of borrowers are given loans much smaller than the amount applied. Credit quality is the lender’s internal proprietary measure of borrower risk. Higher values indicate safer borrowers.

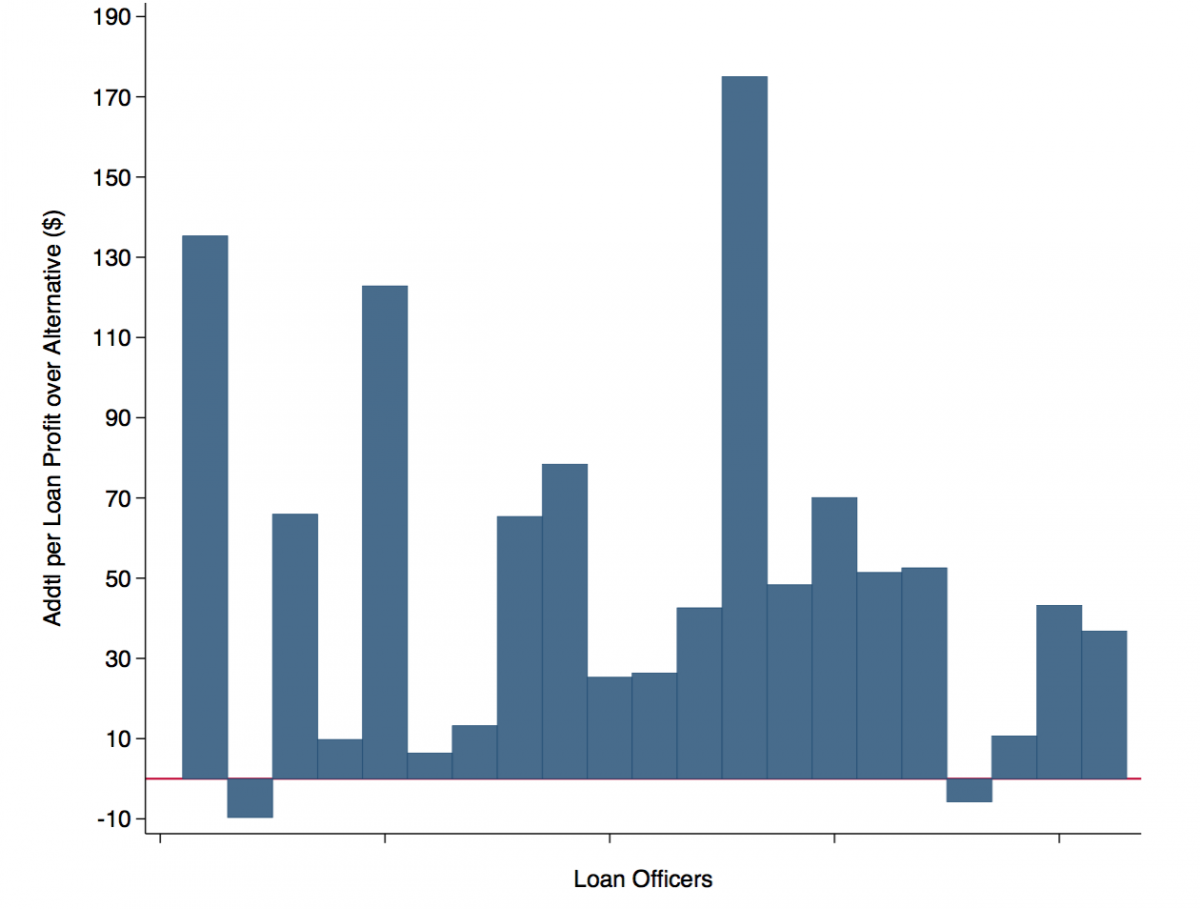

Using the insights from the empirical framework, I calibrate an algorithm that takes into account only the borrower’s hard information, and then I compare to the loan officers’ actual performance. Figure 2 shows the additional profit per loan in dollars that each loan officer contributed above and beyond this alternative. While some loan officers are not profitable, the main result of the paper is that the average loan officer contributes three times his pay in additional annual profits.4 This implies that these loan officers are much more profitable than the lender operating by itself.

Figure 2. Loan officers’ additional per loan profit over algorithm

Notes: The graph displays the difference between the loan officers’ loan profits compared to an algorithm that only takes into account hard information for approximately 32,000 borrowers. The algorithm is calibrated using over 700 data points about each borrower and the actual repayment data. The average loan officer is paid roughly $11 per loan, and the average additional profit is just over $35.

One may wonder how much of this result comes from the effectiveness of the algorithm. Could a more predictive algorithm outperform these loan officers? The answer is likely to be no, because the algorithm is calibrated using the borrower’s actual repayment data.[5] This idealised algorithm is analogous to picking an investment portfolio in 2013 after observing data from 2014, which means that alternative algorithms developed at the time of a loan’s origination are likely to be worse. In addition, the algorithm takes into account more than 700 data points about each borrower including many that may be excluded in some settings such as gender, age, and ethnicity.

Conclusion

I have argued here that these loan officers are valuable. This is despite their biases and an automated lending model with access to extensive amounts of hard information and repayment data. More broadly, my job market paper provides an empirical framework for evaluating the contributions of subjective expertise that can be applied in other contexts such as asset managers or even admissions counsellors. While experts have been beaten in many fields such as chess and mutual fund management (Gruber 1996), this is one area where man can still beat the machines.

See original post for references

You mean there’s no loans?

but.. but.. the Recovery! Yellen said we’d have Lift-Off!

meh, loan volume has risen at a pretty steady clip lately. I think people are so driven by credit based currencies, they can’t even “remember” what “normal” volume looks like.

Here pull on this for me greenie

https://twitter.com/SaraEisen/status/549704059826233344

My father managed the Banker’s Trust branch in the affluent Queens neighborhood of Bayside from 1969 to 1983. Not only did he have a ton of doctors and lawyers as clients, he massacred the local Chase branch in getting and keeping the commercial and real estate businesses along Queens and Bell Boulevards (he had College Point Savings Bank, many car dealerships, a major hotel, a big plumbing and heating company, and numerous restaurants and shops as customers, and handled coins coming in from the Throgs Neck Bridge). Back in the 1970s he could extend a line of credit or cover a check with insufficient funds up to $10,000 on his signature–more might take a single call to the regional HQ in Farmindgale on Long Island. His desk sat on “the Platform” in plain view and anyone could ask his secretary to see him or give him a call, and he was at his desk from 7:30 AM to 4:30 or 5 PM (no “banker’s hours” for Ed Levy). He was President of Kiwanis and sat on the board of the local hospital and the Bayside Boy’s Club. Dad knew people and they knew and trusted him (the renowned pianist Alfred Brendel depended on him to always cover his bounced checks). When people today blather on about “service”, what they mean, if they could even conjure up the image, is what my dad provided. After his retirement, he was stunned to watch his old job turned into a cypher, a powerless parody of what it was. He would come back from the bank infuriated at what the branch people could no longer do. Everything had been centralized and all the humanity drained from the job.

James:

Interesting comment. I worked for Bankers Trust from 1972-1980 in the international division. We made commercial loans to borrowers in Latin America. After I receive my MBA I spent 14 months in the Bankers Trust credit program (not generating a penny for the bank). It was a course in practical corporate finance on steroids.

I’m sure that your father was well prepared for his job as “lender in residence” in the Bankers Trust Bayside branch.

Every time I enter my local bank I shake my head and wonder how it can operate without a loan officer sitting on ‘the platform’. But credit scores and telecommunication technology give the illusion that “local underwriting” still exists.

Great comment, JL! One of my friends and classmates from Ithaca High School is now the president and CEO of Tompkins County Trust Company, founded in 1836 and still going strong. He would be too modest to take any credit for this, but I’m convinced that his bank is one of the important reasons that Tompkins County consistently has one of the lowest unemployment rates of any county in New York State.

Of course, having a large, stable employer like Cornell University is very important, but Greg and the people at the bank under him are able to help local small businesses get started and flourish. They know the community very well and people know and trust them. They have been blessed with good leadership from the beginning. In 1857, for example, Josiah Williams stopped a potentially disastrous run on the bank by pushing a wheelbarrow full of gold and silver into the bank. This little piece of theatre reassured panicky customers and the bank, and the locals who relied on it, survived.

Bank of America spent a lot of money opening up a huge branch in Ithaca, btw, and recently left town with their tail between their legs because the locals basically refused to do business with them!

The graph displays the average approved loan amounts for 282 loans made by loan officers in June 2012 for a 48% APR, 24 month loan.

Either that’s a typo, missing the decimal between the 4 and 8 or WTF. Loan sharks charge less.

The average loan officer is paid roughly $11 per loan, and the average additional profit is just over $35.

Comedy, from a PhD candidate in economics.

Loan officers stand in the way of bank CEO fraudulent lending, although in China it doesn’t seem to matter, where it’s all fraud all the time.

Loan sharks do not charge less. Maybe you know some really nice loan sharks in China of all places, but in NYC at least, loan sharks will regularly charge rates of 120% – 300% APR. And people pay it without batting an eye, because they are desperate and have no other way of accessing credit. Maybe loan sharks in China are super nice. I don’t know.

Consumer credit in developing economies is not cheap. I don’t claim to know anything about consumer credit in China, but I have some knowledge of South America, and loan rates there can easily be 48%. It’s not unimaginable that consumer credit would cost that much in China, either. “There are more things in consumer credit systems, NC Readers, than are dreamt of in your banking philosophy”

A second issue is that the abandonment of training of credit officers means that banks have effectively abandoned the small business lending market.

——–

When you’ve got TBTF policies, bailouts and QE, why bother with training loan officers? Make the loans and collect the bailout money when they fail.

As I keep on stating and keep on getting lambasted… we are moving towards a form of MMT that will have no way of monitoring the quality of investments due to the lack of training or talent and the structure of the system.

As I keep on stating and keep on getting lambasted… we are moving towards a form of MMT that will have no way of monitoring the quality of investments due to the lack of training or talent and the structure of the system.

We may be moving towards, or at, a point where there is “no way of monitoring the quality of investments due to the lack of training or talent and the structure of the system.” But there is no reason to call that “a form of MMT.” What is the point of “criticizing”, labeling bad things by “MMT”, without understanding it? Grosso modo, “MMT” was (half) understood and applied in the USA from the 30s to the 70s, and basically everywhere else postwar. The neoliberal era since then is anti-MMT. Not understanding that means not understanding MMT.

One prickly issue with ‘meat computer’ loan officers is the potential for bias, such as favoring applicants from their own ethnic group while denying those from other groups. Letting a computer decide based on [allegedly] objective credit scores provides some liability protection.

But does it lead to poorer lending decisions? If so, there’s a niche for lendingclub et al to exploit.

Banks (the evolutionary equivalent of stegosauri with brains the size of a pea) survive only by virtue of their government-sponsored cartel. Abolish the freaking Fed … send Citigroup to the tar pits to die.

Examining fig 2, the histogram, I take it that 21 loan officers were used in the study. Am I correct in this?

Sorry, my error. It’s not a histogram but a bar graph.

“The heavy reliance on FICO means that too many banks make similar lending decisions, exacerbating the tendency of banks to run lemming-like off cliffs all together. Haldane used a biological metaphor: that previously specialized types of financial firms and more autonomy in branch lending decisions led to more diversity in an ecological sense, which produced a more stable system.”

Excellent post. The need for bona-fide credit analysis at commercial banks and effective training for both large and small businesses has never been greater, as you say–“tendency of banks to run lemming-like cliffs all together…”

That is exactly what happened with VaR and the abandonment of counter party credit risk analysis, by entity. As a trained commercial bank analyst, I was responsible for counter party credit risk analysis for “swaps” at a major commercial bank, back in the 1980’s. If I had brought AIG’s CDS exposures and argued for an increase in the line before the major bank’s Senior Credit Committee in Fall 2007, along with AIG’s cash flows and exposures, guess what a rationale conversation would have been about credit extension, credit risk, market risk and counter party credit risk would have been. AIG’s major creditors, approving the lines, would have done the responsible thing—shut down the lines and move to responsibly unwind the excessive risk, between the counter parties, without involving the taxpayer. Mr. Geithner and Mr. Paulson testified these were new “risks”,” we just did not understand.” As you know, counter party credit risk and market risks had been properly managed by commercial banks prior to 1999. The notion that the taxpayer could pick up the tab for failed bank speculation is just too brilliant an idea to go back to the honest, old way of making a nickel.

Thank you for bringing up this most basic argument for a return to bona-fide commercial banking at not only the small business banking level, but at the level for complete rationale analysis of cash flows, systemic risks, counter party risk and market risks. With the increase in “shadow banking” and interlocking guarantees and lack of responsibility for credit analysis, the next financial crisis is lurking, as soon as interest rates start the inevitable climb. Algos and mathematical formulas are no substitute for common sense and old-fashion balance sheet/cash flow analysis.

The Derivative Project

As a junior loan officer at Bankers Trust in the 1970’s I had some dealings with Philipp Brothers (later known as Phibro, the acquirer of Solomon Bros.). In those days even a junior loan officer understood counterparty risk. The sad saga of Solomon Bros. should have been a life-lesson, but unfortunately, traders have short memories. And classically-trained commercial bankers were replaced by credit originators and traders.

Banking careers evolve differently when you have to “live with” your borrower/customer through thick and thin.

” You might still find the old-fashioned case-by-case type of small business lending in small banks, but it’s as dead as a dinosaur in the big ones, and the big ones dominate the industry”

yes.

I think community banks still adhere to the older, saner, “know your community” system of loan origination. One problem smaller banks have had in stepping into the void left by the TBTF banks leaving the small business loan area is that the smaller banks (by value) lending limit is often too low to pick up this lending for the larger small businesses. Recently I’ve seen in the midwest many smaller community banks merging in order to increase their size (by value) and their lending limit. I think part of the reason is to better serve the small business community that’s been pretty much abandoned by the TBTFs. Just a guess.

This is why we need State Banks. The Bank of North Dakota does loan participations with local banks to allow them to make much larger loans than they would normally be able to. BND is not, as a rule, in the business of handing out loans on its own–its works mainly through partnerships. Which is why North Dakota has the highest concentration of local banks, and the fewest multi-nationals, of any state. Local bankers in ND love the BND.

The capital gains tax rate in effect is part of the small business story. It makes a difference in how small businesses are managed, either as a continuous source of income, or as something to eventually sell to a larger business. I would argue that when the rate was reduced to 21 percent from 29 percent in 1997, and then to 16 percent in 2003, small business owners had an incentive to sell out, and managed accordingly. They didn’t borrow a lot of money to invest for the long-term. Did this make a difference in lending to small business by banks? The banks were happy to lend money to bigger businesses to buy out the smaller businesses. It returns to the theme in play since the 1970s, that bigger is better. It isn’t true, but it is assumed by many. Since 2013, the capital gains tax rate has gone up to 25 percent. Maybe the higher rate will encourage more small business owners to invest for long-term profitability and seek out the financing.

My husband is a credit officer in commercial banking at one of the big behemoths, and he verified Yves’ remark about lack of training. The credit officers receive virtually no training, and the quality of what little they do receive is very poor. He’s had about 10 days of training in several years. He also said: trainings are perceived as social gatherings and people don’t take them seriously; trainings are more about being able to say to regulators that people have been trained rather than learning something valuable; some people get longer training, but it’s mostly about learning how to navigate the IT systems required for credit analysis; and there is little knowledge transfer between more senior bankers and newer staff. In the actual business, they are taught to follow the higher ups and never question decisions, effectively making credit officers ‘robosigners’. When assessing credit risk for a company, analyzing economic fundamentals, industry fundamentals, and market dynamics is frowned upon and ignored, because it would often lead to the deal not closing if true risks were considered.

Just so you know, by contrast, in the 1970s, credit officer training took two years. It was seen as a great credential by business schools.

Yes, and the funny thing is he already has two Masters degrees including an MBA. They’re hiring people far overqualified for the role instead of training them on the job, but that’s a whole other job market related issue. .

The excuse always seems to be “new risks, we didn’t understand”.

Personally it is time to revitalize the Admiral Byng Rule.

Yes, and the funny thing is he already has two Masters degrees including an MBA. They’re hiring people far overqualified for the role instead of training them on the job, but that’s a whole other job market related issue. .

I do not doubt the rationale that asserts that well trained and experienced loan officers are an important human asset to cultivate at any bank engaging in small business commercial loans . However drawing conclusions from the paper presented would have one flaws; the time frame of the study is too short 2010 to 2013. Furthermore China banks were still engaged in a credit and construction boom, which dominated the economic activity of the nation, hence small businesses formed during that time would have benefited from the boom, and hence would have a greater chance of repaying the loan.

B) the major economic trend of the place where the study occurred. China is fundamentally a growing country; hence newly formed business that support the growth or the growing aspirations of the workers should have a greater chance of prospering than in a situation where the economy is experiencing long term decline such as Detroit.

I believe a study that spans over 15-20 years, studying loan officer performance in different parts of a nation would be much more conclusive than the study presented in this article.

I shook my head many times while reading this post, there are so many things wrong with the assumptions of the author.

1) a good credit officer takes much more than two years to train. She/he needs to go through one or two credit cycles to realize that lending (especially unsecured) based on financial projections is hazardous indeed.

2) using as a data point a country and a period that has seen the most monumental increase rate of bank loan in economic history is likely to lead to biased conclusions.

3) There is a reason why banks retreat from unsecured business lending for SME : It us simply bad business for the bank AND for the customer. A SME that has to use unsecured credit is extremely likely to fail and nobody wants that. . What banks can provide are first, good payment services and second, secured lending against good collateral, mostly real estate and customers receipts. This kind of lending requires skills that are NOT what is required from corporate credit officers. It is a different job, much closer to individual retail business risk management.