This is Naked Capitalism fundraising week. 683 donors have already invested in our efforts to combat corruption and predatory conduct, particularly in financial realm. Please join us and participate via our Tip Jar, which shows how to give via check, credit card, debit card, or PayPal. Read about why we’re doing this fundraiser, what we’ve accomplished in the last year, and our fourth target, 24/7 coverage, 365 days a year.

By Lambert Strether of Corrente.

As readers know, ObamaCare is going to have another “Open Enrollment” period starting November 1. The White House could be lowballing the estimates to look good, or at least better, when the final numbers come in, but consensus seems to be that enrollment is becoming increasingly difficult:

Health and Human Services Secretary Sylvia Mathews Burwell announced Thursday that an expected 10 million Americans will be covered by late 2016 by health plans they bought on the federal and state insurance exchanges created under the law.

That figure is just half the most recent forecast by congressional budget analysts, who have long expected 2016 to usher in the biggest surge in enrollment. The number represents a marginal increase from the 9.1 million Americans the administration believes will have ACA health plans by the end of this year.

And:

But questions linger over whether it can reach deep into the pockets of the nation’s most intractable uninsured populations and whether people who currently have health plans through the marketplaces will decide that the coverage is worth keeping.

Yes, “whether [the administration] can reach deep into the pockets of the nation’s most intractable uninsured” is a precise description of the problem. Although pockets can be found in many places, as we shall see.[1]

Introduction

At the highest possible level, there are three things to be said for ObamaCare, and Obama, in his speech atKnox College in Galesburg, Illinois, July 24, 2013, hit all three:

If you don’t have health insurance, then starting on October 1st, private plans will actually compete for your business, and you’ll be able to comparison-shop online.There will be a marketplace online, just like you’d buy a flat-screen TV or plane tickets or anything else you’re doing online, and you’ll be able to buy an insurance package that fits your budget and is right for you.

That is, ObamaCare is a neoliberal, market-based policy.

And if you’re one of the up to half of all Americans who’ve been sick or have a preexisting condition — if you look at this auditorium, about half of you probably have a preexisting condition that insurance companies could use to not give you insurance if you lost your job or lost your insurance — well, this law means that beginning January 1st, insurance companies will finally have to cover you and charge you the same rates as everybody else, even if you have a preexisting condition.(Applause.)That’s what the Affordable Care Act does.That’s what it does.(Applause.)

In other words, ObamaCare ensures that pre-existing conditions are covered. (Just as a troll prophylatic, I think this is humane, although it has unexpected side effects I’ll get to.)

Now, look, I know because I’ve been living it that there are folks out there who are actively working to make this law fail.

And Republicans (“folks”) vehemently oppose it; by February of this year, the House had voted to repeal ObamaCare 56 (!) times.

As usual with Obama, he sounds so good you might actually believe him if you didn’t know the detail. So, I’m going to re-order and recombine Obama’s points just a little. First, I’ll review the neoliberal history of Obamacare, because that really can’t be explained too often; then, I’ll look at ObamaCare’s failures as a marketplace, which are, if not mortal, grave; and lastly I’ll look at some unexpected, or possibly expected, consequences of ObamaCare’s (praiseworthy) coverage of pre-existing conditions. Spoiler alert: Those consequences are not adverse selection, at least not completely; and the consequences could be said to affect the neoliberal project generally. This last point will be a research project more than an indictment, and I very much hope knowledgeable readers will participate.

ObamaCare as a Neoliberal Program

Let’s review. Quoting a great slab from an earlier post at Naked Capitalism because, as I said, we can’t hammer this point home too often:

Make no doubt. Romneycare was the model for Obamacare.

And Brad DeLong writes in 2010:

The conservative DNA of ObamaCare is hardly a secret. “The Obama plan has a broad family resemblance to Mitt Romney’s Massachusetts plan,” Frum wrote. “It builds on ideas developed at the Heritage Foundation in the early 1990s that formed the basis for Republican counter-proposals to ClintonCare in 1993-1994.”

Now let’s consider those Heritage “ideas,” because they ended up setting the boundaries for acceptable discourse in the policy debates that followed. In a 1989 Heritage Foundation brief, Assuring Affordable Health Care for All Americans, Heritage Foundation’s director of domestic policy strategies, Stuart M. Butler, Peter J. Ferrara (George Mason), Edmund F. Haislmaier (Heritage), and Terree P. Wasley (U.S. Chamber of Commerce) proposed the essence of ObamaCare: “[E]very resident of the U.S. must, by law, be enrolled in an adequate health care plan to cover major health care costs.” However, from the “political advantage” standpoint, the key goal of the Heritage plan was to fend off single payer. From the conclusion:

The mandate made its political début in a 1989 Heritage Foundation brief titled “Assuring Affordable Health Care for All Americans,” as a counterpoint to the single-payer system and the employer mandate, which were favored in Democratic circles.

So, reminding ourselves of Jeff Sessions’ strictures on “anything goes” post-modernism, we have Democrats (Obama + Gruber) adopting a Heritage-inspired plan pioneered by Republicans (Romney + Gruber), whereupon the Republicans turn around and fight their own plan tooth and nail, while the Democrats, fighting back furiously, never mention they adopted the Republican plan. However, we also find Democrats, Republicans, Heritage, and Gruber in simultaneous agreement that “single payer” is verboten, taboo, unmentionable, “off the table,” and not politically feasible. So all parties noisily and venomously seek “political advantage” at a level of mind-boggling illogic and contradiction, but the real policy conflict — the policy both parties and the political class seek to avoid — is buried, and never mentioned at all.

Political point the first: The party that voted to repeal their own plan 56 times is, indeed, crazy pants.[2] But if you were a Martian just come to Earth, wouldn’t you ask the obvious question: How crazy pants is the party that adopted the crazy pants party’s plan as their own? Pretty crazy, you might say, although, to be fair, in a more rational-seeming and hair-raisingly subtle way.

Political point the second: We can also see that ObamaCare, as a neoliberal program, is firmly inside the Overton Window in official Washington, and that both parties are fighting to keep the Overton Window from being dragged left to include single payer, very much including Presidential candidate Hillary Clinton.

Policy point: All of which is too bad, because single payer would save the country a boatload of money. Oh, and some lives.

ObamaCare as a Failing Neoliberal Program

We’ve had two rounds of “open enrollment” for ObamaCare, and we’re closing in on the third. That’s time enough to gather evidence on how the program really works. (The first two of these points I’ve cited before, but it’s useful to gather them together in once place. The third is new.)

ObamaCare Policies are Sketchy Policies. (See Naked Capitalism here for ObamaCare’s narrow networks, and here for how ObamaCare crapifies policies). The Los Angeles Times describes Covered California’s narrow networks:

A new study finds that 75% of California’s Obamacare health plans have narrow physician networks — more limited choices than all but three other states… Nationwide, 41% of networks were labeled narrow, meaning they included 25% or less of the physicians in a rating area…. But [Dan Polsky, executive director of the Leonard Davis Institute of Health Economics at Penn] said consumers still don’t have an easy way to tell whether a health plan is narrow or not before enrolling… Consumers often have the ability to search for specific doctors before picking out a policy. But that information doesn’t tell a consumer how restricted an overall network may be for primary-care doctors or specialists.

Even with subsidies, ObamaCare premiums are high given that you can’t know in advance what you’re buying in exchange for having your pocket reached into. (I’m not saying all ObamaCare policies are bad; I’m saying it’s too hard to tell in advance whether they’re going to be bad or not. And see below on “false statements or representations.” Why are these issues being treated under the heading of “communication,” rather than fraud?)

ObamaCare is a Bad Deal (for Many). From Mark Pauly, Adam Leive, Scott Harrington, all of the Wharton School, NBER Working Paper No. 21565:

This paper estimates the change in net (of subsidy) financial burden (“the price of responsibility”) and in welfare that would be experienced by a large nationally representative sample of the “non-poor” uninsured if they were to purchase Silver or Bronze plans on the ACA exchanges. The sample is the set of full-year uninsured persons represented in the Current Population Survey for the pre-ACA period with incomes above 138 percent of the federal poverty level. The estimated change in financial burden compares out-of-pocket payments by income stratum in the pre-ACA period with the sum of premiums (net of subsidy) and expected cost sharing (net of subsidy) for benchmark Silver and Bronze plans, under various assumptions about the extent of increased spending associated with obtaining coverage. In addition to changes in the financial burden, our welfare estimates incorporate the value of additional care consumed and the change in risk premiums for changes in exposure to out-of-pocket payments associated with coverage, under various assumptions about risk aversion. We find that the average financial burden will increase for all income levels once insured. Subsidy-eligible persons with incomes below 250 percent of the poverty threshold likely experience welfare improvements that offset the higher financial burden, depending on assumptions about risk aversion and the value of additional consumption of medical care. However, even under the most optimistic assumptions, close to half of the formerly uninsured (especially those with higher incomes) experience both higher financial burden and lower estimated welfare; indicating a positive “price of responsibility” for complying with the individual mandate. The percentage of the sample with estimated welfare increases is close to matching observed take-up rates by the previously uninsured in the exchanges.

Shorter: The dog doesn’t want to eat the dog food. Or have its pockets reached into, if it has pockets.

ObamaCare is a PITA. (You might say that ObamaCare puts the PITA into caPITAlism when it comes to health care.) I mean, we knew this, but now we really know it. Washington Times:

Most filers who received government subsidies to buy Obamacare plans had to pay money back to the IRS this year, according to an H&R Block analysis released Monday that looks at the health law’s first full tax season.

The tax-prep giant studied its own massive customer base and concluded that two-thirds of its filers who got subsidies from Obamacare were overpaid during the course of the year, and owed money back to the IRS on the April 15 deadline.

It’s hard to imagine a more unwelcome surprise — other than a ginormous bill because you accidentally went out-of-network for medical care — than finding out in an H&R Block office that you owe more money than you thought you did, and after jumping through all ObamaCare’s income eligibility hoops to begin with. Could this have contributed to the administration’s difficulties reaching into people’s pockets? I’m guessing yes.

ObamaCare as an Engine of Fraud?

I freely admit that this portion of the post is speculative; but as the great Peggy Noonan once wrote: “It would be irresponsible not to speculate.” Basic proposition: Under neoliberalism, experience tells us that if there can be fraud, there will be fraud[3]. In the neoliberal dispensation that began, in this country, in the mid-70s, we’ve seen this proposition prove out in the Enron scandal, engineered bubbles in Silicon Valley, “the intelligence and facts” that were “fixed around the policy” in Bush’s march to war in Iraq, in charter schools,in “robosigning” scandals, and in accounting control frauds generally.

That’s quite a list of #FAILs, and they are both enormous and in major, major social structures; if government were like a household, they’d be equivalent to failures in the electrical system, or serious water damage from a plumbing break. They are #FAILs in American corporate accounting, both American stock markets, the entire American military establishment, the entire American public school sytem, the entire American housing market, and the American C-suite. All these #FAILs were very expensive — or lucrative — and they all have fraud and corruption at their rotting hearts. Now, one might argue that these #FAILs are one and all accidents — after all, the market can never fail, it can only be failed — but it is not my purpose here to assign causes[4], but rather to point to probabilities, based on our experience (rather as one might infer the likelihood of cockroaches, even if as yet unseen, if food is left out).

So our question becomes: Does ObamaCare enable fraud? And the answer — hold on to your hats, here, folks — is “Why yes. Yes, it does.” Why? Because HHS’s Secretary Kathleen Sebelius ruled, in 2013, that a key Federal Statute preventing fraud does not apply to health insurance policies purchased through the ObamaCare “marketplace.” From her 2013 letter to Representative Jim McDermott:

Thank you for your letter regarding whether qualified health plans (QHPs) are considered federal health care programs under section 1128B of the Social Security Act. Section 1128B(f) of the Social Security Act defines “Federal health care program” as “any plan or program that provides health benefits, whether directly, through insurance, or otherwise, which is funded directly, in whole or in part, by the United States Government…. or any State health care program….”

The Department of Health and Human Services does not consider QHPs, other programs related to the Federally-facilitated Marketplace, and other programs under Title I of the Affordable Care Act to be federal heatlh care programs. This includes State-based and Federally-facilitated Marketplaces; the cost-sharing reductions and advance payments of the premium tax credit; Navigators for the Federally-facilitated Marketplaces and other federally facilitated consumer assistance programs, consumer-oriented and operated health insurance plans; and the risk adjustment, reinsurance, and risk corridors program.

What are the implications of determining that ObamaCare is not a “health care program” (!) within the meaning of the act? Robert M. Radick, former Chief of Health Care Fraud Prosecutions and Deputy Chief of the Public Integrity Section in the U.S. Attorney’s Office for the Eastern District of New York, explains:

The Anti-Kickback Statute And The Affordable Care Act: A Law Enforcement Tool Suddenly Goes Missing

[L]ess than two weeks ago, one of the most potent resources that law enforcement has had at its disposal in the fight against health care fraud suddenly fell out of the government’s toolbox.In fact, while many in Congress and the mainstream media have focused on problems with the Healthcare.gov website and the cancellation of policies that do not meet the requirements of the Affordable Care Act, another critical development has attracted considerably less attention:HHS Secretary Kathleen Sebelius’s announcement, in an October 30, 2013 letter to Representative Jim McDermott (D-Wash.), that insurance offered through the Affordable Care Act’s new health insurance exchanges do not constitute “Federal health care programs” and thus are not within the scope of the federal anti-kickback statute.

The significance of Secretary Sebelius’s decision is underscored by the critical role that the anti-kickback statute has long played in the government’s ability to impose significant penalties and obtain massive recoveries in the health care industry.

And Radick points to the statute that Sibelius has determined should not apply to health insurance policies[5] sold under ObamaCare. 42 U.S. Code § 1320a–7b – Criminal penalties for acts involving Federal health care programs:

(a)

Making or causing to be made false statements or representationsWhoever—

(1)

knowingly and willfully makes or causes to be made any false statement or representation of a material fact in any application for any benefit or payment under a Federal health care program (as defined in subsection (f) of this section),

And there’s a lot else. Now, I don’t even play a lawyer on TV, but to my simple mind, it would seem that when health insurance companies sell policies on the ObamaCare Marketplace that list doctors as in network when they aren’t, or adopt titles that suggest they are affiliated with hospitals when they aren’t, or use artful language to conceal the benefits actually offered, or even make it impossible to acquire accurate information because of differences between the summary language proferrred on the website, and the actual multipage policy delivered after sign-up, that all these are “false statements or representations,” and that if you get tripped up by any of them, that they are “material facts.” Odd that Sebelius should exempt ObamaCare from the statute, then.

Or not so odd (and this is the spoiler I foreshadowed in the Introduction). Consider the incentives. ObamaCare — again, this is praiseworthy, because humane — forces health insurance companies to accept all comers, regardless of their pre-existing conditions[6]. That means health insurance can’t do underwriting any more. That, in turn, means that one of their main sources of profit has been outlawed. How will they recover their lost profits? Experience suggests the answer.

They’ll make their money the old-fashioned way. Fraud. (In this connection, it’s worth noting that Covered California awarded $142 million in no-bid contracts. “The no-bid contracts represent about $2 of every $10 that Covered California awarded to outside agencies.” Ka-ching! Covered California also, rather like Hillary Clinton, doles out email as it chooses. And Covered California contract negotiaions are exempt from the Public Records law. How con-v-e-e-e-n-ient. Seriously, can anyone think of a good reason for this, from the standpoint of public purpose?)

Now, to be fair, this is speculation. Which is why I called for a research project!

Readers, it would be useful if you could supply examples of “false statements or representations” by health insurance companies on the ObamaCare marketplace what would be considered fraud if a rational determination of fraud, rather than Sibelius’s, were to be used. It would be even better if some whistleblowers threw some documents over the Naked Capitalism transom — as they did with the “robosigning” scandal — that showed how “false statements or representations” are specified, drafted, and approved.

Conclusion

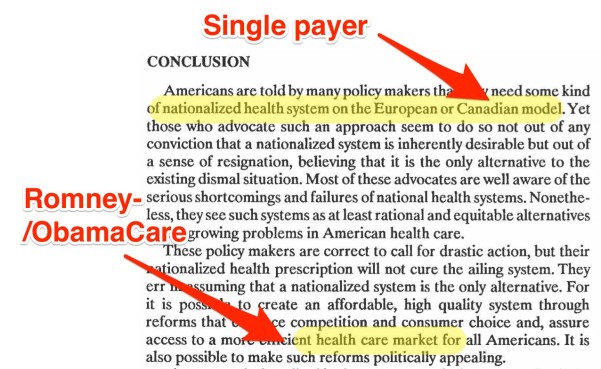

The failures of ObamaCare’s Marketplace are the failures of neoliberalism itself. There are public purposes that cannot be achieved by market-based solutions: Provisioning health care is one such, as the experience of the civilized world should tell us, if we would look:

[S]ince the mid-70s, when Canada adopted its single payer system, we’ve conducted the largest controlled experiment in the history of the world. We’ve had two political systems spanning the same continent, both nations of immigrants and once part of the British empire, both mainly English-speaking but multicultural, both with Federal systems, and both with a free market system backed by social insurance. And the results of the experiment? The “evidence”? Canadian-style single payer wins hands-down.

What neoliberalism can achieve — has demonstrably achieved, over its forty-year dominance of the world’s political economy — is fraud. There is good reason to think that same will be true for ObamaCare. Readers?

NOTES

[1] To be fair, the WaPo reporter might have intended a military metaphor, like “pockets of resistance.” Marketers often think in terms of warfare (“marketing campaign”).

[2] The seventy-five cents way to say “crazy pants” is “presenting with a case of epistemic closure.”

[3] Qualifying with “under neo-liberalism” to avoid discussion of human nature, first causes, original sin, and so forth.

[4] One might argue that under neo-liberalism, there is no principled reason for the regulatory functions of the State not to be “on the market” along with everything else. Hence the three-card monte aspect of affairs at Justice, the SEC, and so forth: We have the crooks dealing the cards, the shills roping in the marks, and the marks (that is, us). We also have the cop on the beat, who, every so often, collects a portrait of Andrew Jackson from the dealer. The parallel between the cop collecting a twenty to keep the game going and Justice collecting a cost-of-doing business fine is exact. It’s rather like Dostoevsky’s Crime and Punishment, where Raskalnikov comes to believe that “everything is permitted.” Except without the punishment part, of course.

[5] There are plenty of other anti-fraud provisions in the PPACA statute, including anti-kickback. Just not for health insurance policies.

[6] It’s true that health insurance companies can game this requirement by manipulating drug regimens, but its unlikely they can recoup all their “lost profits” that way.

87 comments

The only thing worse than the disaster of Obamacare would be the catastrophe of replacing it with fully government run health care.

See, they call it “single payer” because it’s — follow me closely, here — single payer. (Back-office functions, and bargaining power on prices.) Single payer is not “government run.” You’re thinking of Britains’s National Health Service (which the neoliberals are busy gutting, but that’s another story). Single payer, by the standards of the civlized world, is centrist.

Mogden prefers to pay his taxes directly to the insurance companies. Cuts out the middleman.

Single payer, by the standards of the United States, would be the scam of all scams topping even the Military.

Unless, there’s some part of the US government that you know about that is NOT run for the benefit of the smart-n-savvy scam artists. Is there such a thing?

Why would single-payer be run morally when nothing else is?

I believe that the political effort — and resulting power — needed to pass it is the answer to your question.

Obviously, NOTaREALmerican, you are not a Social Security or Medicare beneficiary.

Good point! Indeed, what most Americans would appreciate from the Federal government is MONEY – they can figure out how best to spend it.

Need a different algorithm and code for further rounds of money ejaculation by the gubmint — seeing as how what gets out only, somehow, for gee I can’t imagine why or for what reason, only almost entirely goes to people, natural and bzzzzt! corporate, who are nothing better than cancerous tumors that will happily grow until they kill the “host…”

They know best how to spend it: in addition to buying up all the rentable channels of necessities and real-wealth creation, buying up and suborning all the parts of finding, there’s the asymptotic prices of Great Art, those on the way to billion dollar condos and estates, private jets and private islands and private armies and megayachts and “timepieces”… Proof, irrefutable, that too much is never enough…

And the rest of us are supposed to feel SORRY for these lonely Croesuses? Eat your gelt, Fokkers. We starve so you can stuff your guts and apotheosize your ” class…”

…I see Bill Gates has some solution in mind: http://www.theatlantic.com/magazine/archive/2015/11/we-need-an-energy-miracle/407881/, and http://m.youtube.com/watch?v=IsRlN1oDm60

…how much longer, and just where, does he expect to live? His old man is 89, he is 60, and I’m sure he’s hoping that the Squillionaires Immortality Or At Least Methusalen Longevity Projects pan out. In 2030 he’ll be what, 75? Musk? Brandon? Russian dudes? They give a fig, as long as there’s house slaves to peel their grapes for them? The Gates Estate, largely underground on the north shore of Lake Washington, is in a seismic zone though with serious engineering and airlocks…

Well, you see, when things are run by government, you have a hope in hell of seeing what is going on, and perhaps even influencing it, through elections and representatives and such. Someday, maybe, but still a hope. FOIA and all that (when it works).

With private industry you have *absolutely no chance of ever finding out* how you were ripped off. If something does happen to leak out, ie, mortgage robo-signing, illegal foreclosures, you still won’t get your house back. I’ll take my chances with the govt, thanks.

The National Park Service. If the question was intended as a serious question, you just got a serious answer. Which shows the possibility exists.

Lambert,

Help me out here.

Who, exactly, is the single payer?

Not to answer for Lambert, but my understanding is that the single payer would be the federal government. I look at it as Medicare-For-All, cradle to grave. Medicare is actually one of the most efficient programs of the federal government. The administrative costs are in the single digit range as a percentage of total cost; vastly more efficient than the 35-40% of additional costs imposed on healthcare by the private insurance system.

John, You get an A+ and get to sit on the front row.

Single payer Medicare is our ONLY solution. Q.E.D!

Single payer is the answer when our healthcare delivery system is seen as a fiscal problem largely limited to the 3rd party payers (which is a big part of the problem, no doubt).

What single payer will not fix (and risks making worse) are all the problems resulting from fraudulent or ethically compromised medical practices. Single payer without strong regulatory enforcement would pour gasoline on the already significant problem of fraud by providers/healthcare facilities.

You must like being ripped off then. So long as its corporations robbing you blind I suppose. As it was once said, “Free markets do not fail, you can only fail the free market.”

Yes, though a free market would only work as long as the government can be trusted to break up large entities. But as long as lobbying is endemic, it will never ever be a free market. Ever.

In fact, like the theory of communism, I’m not sure a completely free market would ever really work in theory, because someone/something has to make laws, and that ‘thing’/entitity/person will always be targeted by corporations to gain bigger market caps and circumvent more laws. In America’s case, it was the tax code, which is thoroughly compromised.

Obama’s plan was to simply give the insurance companies anything they agreed with, the history of the act, and where it came from, doesn’t really matter IMO. What matters is the fact that by donating 23 million to his campaign, insurance companies bought an Act. That’s the current price of buying a complete act passed by Congress.

In theory, truly free markets transfer all the money to a single agent. Asymmetrical information and differences in purchasing power color every exchange, and rational actors work those discrepencies to their advantage. Monopoly (the board game) was invented to make this point. It always ends with one rich guy and everyone else owing him.

I think the only thing worse than Obama Care is the word neo-liberal. It’s very tough to look a normal person in the eye and use the word neo-liberal.

For example: “Dude, you know why Obama Care is crap? Because of those neo-liberals”.

The Dude’s translation: “Bro, you know why Obama Care is crap? Because of those liberals”.

The Dude’s response: “Bro, those liberals, dude… wanna get a beer!”.

Sure wish the intellectuals could come up with a “Bro friendly” word for corporate-fascism.

It is troublesome, and can often lead to confusion, as you describe. I don’t think “corporate fascism” would work, even though it might be accurate, because its World War II connotations would be distracting. Perhaps simply “corporatism”, “financialism”, or “corporate conservatism” (as opposed to social conservatism).

I have heard National Guard members and other such “regular bro-guy” type guys use the word Corporate Feudalism. So maybe try Corporate Feudalism.

The Dude’s translation is correct. Both “liberals” and career “progressives” supported ObamaCare’s market-based solution. It was in the Overton Window, as I said.

Repetition wears away the awkwardness… I don’t know who these “intellectuals” might be. Do you know any? Perhaps you could put your question to them, and report back.

When speaking to the non-news junkies I always harken back to George Carlin:

“There’s a BIG CLUB, and YOU AIN’T IN IT.”

I live in a rural area that has a GOP congressman in a safe seat. The common man understands that Clinton/Bush/Obama/etc are members of the “Big Club” and they are not.

It’s a really bipartisan way to break it down, without resorting to words with 3 or more syllables that the common man might resent you for using if he doesn’t understand them. He’s not going to rise to your level, you’ve got to speak on his.

I also like “enemies of human dignity” but it’s a mouthful…

How about “corporatists” and “corporatism”?

Fascism is simply top fraught with preconceptions and baggage.

“Useful Idiots” continue to be useful. I’m a recipient of VA medical services and now old enough to also have Medicare. I am also a nurse serving patients with chronic and often awful ” preexisting conditions,” in a clinical practice with doctors who take their oaths and commitment to care seriously enough to serve Medicaid patients. I’m almost retired now, and fixed income and puny savings are my future — at 70 I’m out of workday gas.

What I see is that “Government-run health care works pretty well, bearing in mind the sh_t that ñeolibs/WRONG-wingers and the quantum of thieves present in any population have been doing to bleed out and crapify the good and decent elements of actual health care as opposed to treatment-and-billing machinery and chicanery.

There’s too much wrong and evil with Big UNsurance to list. My little corner involves multiple calls to UNsurance ” customer DISservice, ” to try to beat down the walls of presumption-against-coverage and “prior authorization” nightmares. UNsurance functionaries and their algorithms revise formulary list of meds that are “covered” and the tiering and thus copayment costs to patients on a seemingly random but always narrower and more profitable axis. The “patient care representatives might as well be coached to open the conversation with ” Department of Denial, how may I dis-serve you today?” I can sense the psychic, spiritual costs to a lot of these job- needing mopes, who no doubt take endless abuse and develop pretty thick armor and conversational tactics to deflect and defer calls for “care.” (Because, of course, “This call may be monitored and recorded for training purposes…”)

Obviously, all the incentives and momentum and inertia in the whole effed-up mess are wrong, sick, destructive and dare I say it, evil, from the standpoint of affording ( in all the senses of that word) decent, humane and even just competent health and medical care, unwarped by stuff like fundamentally flawed electronic medical record scams and the billing insanities that go along with, abetted currently by the profit-taking imposition of the ” new, improved” regime of the ridiculous big-data-is-our-God ICD-10 coding scam.

The horror for me is my sense that this, along with so much else of what ordinary people are blindly, blandly and unresistingly being forced into at an accelerating pace by the Owners, will just collapse, crushing billions of us. Yet the fu__ers who are getting some us to cooperate in erecting their f—ing Elysiums and escape pods from our earnest, dedicated labor and the wealth they are stealing from us in so many artful ways, will get to skate. Like all those Nazi “leaders” who took boats or submarines to South Amer, as the Owners’ armies closed in on them… Skated, taking the gold from the fillings of dead millions’ mouths, pried out by the desperate Sonderkommandos hoping for a few more days of life and a little extra teaspoon of gruel…

Brava. One of the best essays I’ve ever read. Thank you, JT. You are a national treasure.

brava indeed!

i suspect on the basis of my interactions over the last couple of years with healthcare “providers” and their staffs that most of them feel exactly as you do, JT. they merely are not as articulate and outspoken about it as yourself. in my small town, i’ve been quite surprised lately by what some M.D.s and other health care personnel are actually complaining of out loud to me, their patient. it’s unprecedented in my experience.

the question remains, when will many more of them become willing to simply speak out in public about what they are so angry about? the answer must be when the costs exceed the benefits for them–just as is the case for myself. the hierarchical medical tradition has kept them in an excellent silence. when healthcare practitioners begin to protest significantly more widely and loudly, this will be a powerful moment in our history.

i hope JT that in your “retirement” you are or will be able to find some energy and time to invest in the fight for the values you so eloquently express here.

How can you keep criticizing Obama’s ACA? I mean even the great Milton Friedman would probably have approved of it. Because Markets! and Romneycare.

Friedman once said, “The most important single central fact about a free market is that no exchange takes place unless both parties benefit.”

If enrollments are falling, if people aren’t buying, that must mean, uh, that must mean…. um….

There can’t be fraud in the neoliberal market because Dr. Friedman tells us, “[The consumer’s] most effective protection is free competition at home and free trade throughout the world. The consumer is protected from being exploited by one seller by the existence of another seller from whom he can buy and who is eager to sell to him. Alternative sources of supply protect the consumer far more effectively than all the Ralph Naders of the world.”

So markets are self-policing and self-correcting and virtuous by way of structural limits. Business collusion and kickbacks? Can’t exit. This is a Health Care Market. Markets are a perfect world. (OK, so the bank mortgage markets weren’t perfect, but this is a Health Care Market. Entirely different.) /s

Milton Friedman would have abhorred the ACA for its complexity. He believed in a basic income guarantee (BIG) replacing all other forms of government assistance to the individual exactly because of its simplicity. No doubt he saw the BIG set at a level at which healthcare needs could be accommodated.

How could he believe in a BIG when he stated, “I am in favor of cutting taxes under any circumstances and for any excuse, for any reason, whenever it’s possible.” Where was the BIG to come from?

Thank you very much for this work, Lambert.

Thank you Lambert for this excellent post and your other outstanding work here. I’m happy to support you, Yves and the others who make this site possible.

The day after Obamacare passed, insurance company stocks rose by something like 20%-25%. ’nuff said.

It was a bailout for the health insurance industry. Nothing more, nothing less.

Not INsurance, rather UNsurance, one might offer. UNsure if they will honor their “contracts,” UNsure if you doctors are or will be able to stay “in network,” UNsure if necessary treatments, therapies, medications will be “covered” even partially, UNsure what the costs are or will be shortly or next year, on and on…

A lot of smart, shrewd, calculating schmucks are working, working away every hour of the day to crapify and extract and abuse…

Yes, thanks for all your work on this, Lambert. I just listened to an interview Doug Henwood did with Trudy Lieberman (Columbia Journalism Review) about a recent article of hers in Harper’s that was critical of the ACA. They were both dismayed at the lack of critical coverage by what Lieberman characterized as a press that was very willing to be snowed by the administration. Who else is adequately covering this?

Lambert’s ACA reporting has been excellent. I also listened to that informative T Lieberman/D Henwood podcast.

Lambert, perhaps you could write an “ACA Survival Guide” type article, linked at the NC front page, perhaps updated once per year or however frequently is required as the 0bama Admin/HHS random non-announced changes occur. Said article could be used as a reference to naive ACA apologist friends who earnestly believe “the ACA is a good earnest first step”, as opposed to a 2nd barbaric system, distinct from the 1st pre-ACA barbaric system, that randomly helps some cohorts of USian & hurts other cohorts USians.

BTW, perhaps you may consider highlighting your ACA coverage as a unique attribute, in your fundraising posts. The naive “ACA is a good earnest first step” crew includes weekdaily progressive pundit shows like Thom Hartmann, The Young Turks, Sam Seder; as well as “alternative progressive media” newsshow Democracy Now. I would be interested in seeing Lambert or Yves interviewed on the ACA topic by one/some of these shows.

seconded.

I wish you would address the cost of Obamacare from the standpoint of the consumer. I am thinking of premiums and deductibles. I have heard that the deductibles alone could force one to bankruptcy and may mean many effectively have no insurance. They just pay a premium to the insurance company.

I know a horror story about those narrow networks and out of network costs. It seems they deliberately make you travel some distance for care.

I don’t really know the difference with single payer but Medicare for all would seem like a good model with no or small deductibles and no in network requirement. What we have now seems to be little more than legal theft. I would also like to see it funded in large part through taxes. ( I like to dream!! )

Most people have only about $1,000.

Any deductible over that, or even just below, is a huge burden, a huge, huge burden.

High deductible plans are not really meant to provide individual health expense protection. They are meant to insure admitting hospitals against loss due to catastrophic care when the admitted insured has avoided care due to a high deductible.

Very interesting. Glad to know this. That’s not the pitch given by employers to employees when they try to get employees to switch/sign up for high deductible plans.

“single payer” the mechanism == Medicare for All the program.

Now, I should qualify that by saying that Medicare is infested with rent-extracting neo-liberal gotchas too, but in principle it’s a single payer program of universal coverage that begins at age 65, instead of the age it ought to begin: 0.

ObamaCare always at its base been about a trade: In exchange for getting a huge block of new customers thanks to government required coverage, the insurance companies agreed to a bunch of regulations regarding things like not being rejected for pre-existing conditions and minimum coverage standards. And when the insurance companies violate those regulations, expect the government to come down on them as hard as Eric Holder did on the Wall Street criminals.

Spit on Obama care all you want. I agree wth many of the critiques. I loathe insurance and pharma with every fiber of my being for what those bastards have put my family through.

But my 28 year old college student with severe dyslexia, a high IQ and a love of learning would be shit out of luck without the provisions of O-care. It has been life saving as well as saving our home and retirement monies.

. He has severe kidney issues since early teens. He has, because of his severe dyslexia, to take every college class twice to pass it but he will not give up on a classics major and a Latin minor with a secondary teaching certificate . ( and he gets no grants or scholarships and attends an excellent public university – we pay full in state freight at PSU main campus ).

He has no hand/eye skills ( another LD issue) so please don’t anyone carp how ‘he could have been a plumber’ instead. He can’t.

He will graduate at the end of August 2016 and has several schools who have made job offers after hearing about his amazing story and interviewing him.

He was able to stay on our excellent insurance until 26 thanks to ACA, and now he can not be turned down for his very expensive prior condition which he absolutely would have been before, thanks to ACA. And the policy he has now through ACA is pricey but with him just exiting his FOURTH hospitalization this year it has been worth its weight in gold. ( we pay most of it as he cannot work during the school year but only working double restaurant waitstaff shifts while on breaks.)

Not perfect by ANYONE’s measure but it has saved his life and frankly ours as well because we would have spent every cent we have of retirement money to keep him alive at 68,000$ and up PER hospitalization rather than have him at the mercy of Medicaid level treatment….

Please think – all you people ranting against this here over these past few years – these are real live people you are toying with and cavalierly dismissing their real needs while you rant about the ‘ the terrible ACA’.

What does your child winning the lottery have to do with the public interest? Congratulations. You’ve been bribed. You’ve sold out the public interest in your own personal and class interests. That’s the textbook definition of corruption, in saner corners. Want a cookie?

Why are YOU considering it okay to play lemonade stand with MY life? How about rights instead of lotteries? At long last where is your sense of solidarity?

Hunkerdown–you’d be singing a different tune if you had a handicapped child or you developed a debilitating disease.

Or not. Sentimentality and special “I’ve got mine, Jack” pleading aside, don’t we all deserve health care?

I sympathize with your analysis, and I know there are plenty of good outcomes like yours. I’ll just point out that you would have gotten similar results under Medicare for All, or a seriously tight regulatory scheme, or even with a Public Option.

Lambert has consistently pointed out that Obamacare has benefited some people. Your college student is one of the lucky ones. But for many who are not so lucky, it is a dismal and expensive failure. That is a travesty. A humane health care system should cover all persons equally, no exceptions. The passage of Obamacare has almost certainly made that goal even more difficult to reach.

Oh, you and yours are too good for Medicaid, a real life-saving program, but just fine with the rest of us paying off the insurance bandits so that you can look down your nose at Medicaid?

Amazing, isn’t it? How easily us mopes at the bottom can be brought to savage one another, to just seek some idiot comparative advantage, to smugly congratulate ourselves on “making smart investments” and purchases, instead of closing ranks and making common cause against the predators and vultures we so quickly lose sight of down here in the sewers, and fail to acknowledge as the real source of our diminution and woes?

It is; that’s the goal and it has worked quite well. Instead of wanting to make sure that Medicaid works well for all, s/he is happy that she got hers, and be damned with the rest of us. I get my care at the VA, same as you. It is not perfect, but it is better than any private insurance I’ve had and the best part is that, being covered by my wife’s Big Law insurance, the VA gets reimbursed and thus can provide care for more people. I want more people to have what you and I have, rather than to be content that I got mine. It’s here today, some people work damn hard to try take it away from us tomorrow, so vigilance is in order.

Do you follow military.com? In among the macho and fanboy stuff there’s regular attention to the activities of the neoliberals and chickensh-t chicken hawks who as you say are busily undermining not just what you and I have for health care (VA, as you say, not perfect, but at least as good as what I’ve seen as nurse and patient in the “private sector” of HCA and BCBS and IN-Humana, etc.) but every growing bit of the Grand AAUGH! Bargain bullsh-t Obama wants to force-feed us, like we were Gitmo “detainees?”

Maybe the dissociation and atomization and trivialization and all are the best we can do, us humans? Looking at what’s shakin’ in the world, like Kashmir where Enthusiasts of the Hindu flavor are killing fellow humans because rumor says they might have some gustatory connection with beef…

Best we can do is take care of the people we care about, and care for? While the Big Stuff rolls down on us like the proverbial Jaganath?

Do you think those of us who were fortunate enough to have decent, affordable insurance before Obamacare should have refrained from “ranting against” the system and instead constantly pointed out how well it was working for us?

Hello, I live in Ontario, that’s in Canada, if you don’t know, and we have single-payer (ie, govt/tax paid) health care. We call it OHIP. We used to pay for it separately, but no longer, and it is really hard not to be covered for about anything. Except augmentation mammoplasty and such. Well, and dental, glasses, naturopathy and chiropractic, which I think should be covered. Oh, and prescriptions. So we have much room for improvement — I write my MPP about it. But look, see how easy it is? See how little it costs? We are paying $5,718 per capita for life expectancy of 81 years, you are paying $9,146 per capita for life expectancy of 79 years. Go ahead, look it up yourself. And yes, ACA is highly rantable.

ObamaCare may be better than a fist in the eye, but just barely. Are you happy to be a mug? It is pathetic to see how grateful some Americans can be for not being beaten. You could have had single-payer, and you still can. There is this candidate with funny hair…

Everybody should have the same good luck as you did.

Why is that so hard to understand, or to say?

How do you feel about “cavalierly dismissing” the 50% of uninsured for whom — as the study I quoted shows — ObamaCare would leave worse off?

“In other words, ObamaCare ensures that pre-existing conditions are covered. (Just as a troll prophylatic, I think this is humane, although it has unexpected side effects I’ll get to.)”

Jumping ahead (sorry if this duplicates your point later on), what it does is demonstrate the fundamental insanity of using insurance to pay for health care. Requiring insurance to cover pre-existing conditions is logically equivalent to allowing you to buy retroactive coverage AFTER you have the accident. The only way to make up for this fundamental irrationality, humanitarian or not, is on volume. Hence the Mandate, which I still think is both unconstitutional (there is no authority for it) and an unconscionable intrusion.

Medicare or single-payer, OTOH, aren’t actually insurance. They’re transfer systems, based directly on the taxing authority. They’re insurance-like in benefiting from the largest possible risk pool (everybody), but they don’t need to make money, so they have little reason to restrict needed care. Plus other benefits, like the ability to regulate the practice of medicine. The chief disadvantage is that they are the government, so are vulnerable to political malice, as Canada and Britain are discovering. But that’s democracy for you.

“so are vulnerable to political malice, “

If we were all roughly equal, economically speaking, then we would all have roughly the same class interests, economically speaking.

But we aren’t and that devolves largely from the money system whereby the rich and other so-called credit worthy have been/are allowed to borrow without permission or adequate compensation the purchasing power of everyone else.

People hate Progressives and why not? They supported the Federal Reserve and every other device to save the banks from themselves including sops to the public to prevent/delay a revolution instead of justice and fundamental reform. Indeed, what are calls for regulation but more attempts to save the banks?

Malice indeed and understandable.

“and that devolves largely from the

moneypolitical system whereby the rich and other so-called credit worthy have been/are allowed to borrow without permission or adequate compensation the purchasing power of everyone else.”See US history 1880 – 1910. We’ve been here before.

Calls for regulation are attempts to regain control of the political system by the 99%.

The lack of a risk-free fiat storage and transaction service has, from the beginning, been a HUGE implict subsidy of private banks, even without and, most decidedly, with government deposit insurance.

Regulate the Hell out of banks if you want but for Heaven’s sake DE-PRIVILEGE THEM too!

“The lack of a risk-free fiat storage and transaction service ..”

Eg. a Postal Savings Service or equivalent that had nothing to do with the banking cartel, ie. did not participate in inter-bank lending – leaving that to individual account holders if they so choosed.

make that “if they so chose”.

The writers at FDL predicted all these problems. In particular, Marcy Wheeler, Dave Dayen, Jane Hamsher, and the brilliant John Chandley (Scarecrow) pointed out that the cheaper plans were bound to be disasters. I focused on the gains to health insurance companies, which have profited mightily.

It’s nice to be able to say I told you so. Too bad no one was listening. In fact, it’s more than too bad. It really sucks.

Wishing the old FDL of those days was still around. Started going downhill when David left, then Scarecrow and Southern Dragon died. But it definitely had it’s place in the sun.

Masaccio, I was listening!

As did, though I say it, the writers at Corrente.

At a time when I thought I must be paranoid, because everything I read in the mainstream sources had me going ‘here lie dragons’, FDL became a god send. I was functioning on instinct, but they provided sources and information that showed me that the American people were being lied to and manipulated by the people they elected to change things for the better. And I will be blunt, just as we were lied to repeatedly about Iraq, we were lied to repeatedly about ACA. Sadly, the most of the folks pushing the invasion of Iraq were true believers of the garbage, we can’t even say that about the betrayal of the American public and Democratic voter regarding ACA. They knew it was a means of making the American public pay more for less actual health care, it is just called things like ‘bending the cost curve’. See they weren’t bending it for the public, they were bending it for the For Profit Health and Insurance Industry.

I thank everyone who helped educate me at FDL daily during that period.

I had an ObamaCare (less) policy with Anthem Blue Cross. On their website my doctor was on the preferred in-network list, I downloaded a pdf to that effect. After my appointment Anthem didn’t even deny the claim. It never appeared in my online Anthem web admin account at all- it was if the event never happened. (Winston Smith) About 60 days later I received a single piece of paper in the mail notating my name, the doctors name, and the date of the appointment with the simple phrase “No Insurance Coverage” Anthem wouldn’t discuss it with me.

I paid for an insurance policy where the only working component was the billing system!

If that doesn’t represent fraud then I don’t what would.

That’s a good example. Readers, do you have others?

I don’t know about fraud, Lambert, but I do know that a friend (she and her husband are over 50) are paying $25,000 per year, to cover premiums only , for themselves and two teenage children. They don’t qualify for subsidies, and they have what would be called a bronze plan. Imagine the boost to the economy if they, and thousands of others like them, paid, say, an extra $5000 per year in taxes for universal health care, freeing up $20,000 to pay down credit card or mortgage debt, buy new clothes for themselves and the kids (which they can’t afford to do right now), bought new tires for their cars, or whatever. Spending on infrastructure is nice, but a huge decrease in medical expenses would lead to an unprecedented economic boom, IMHO.

I’ve always asked these questions regarding “health ‘insurance'”:

1. How can I shop/ check network coverage when I’m in an ambulance strapped to a board and marginally lucid following a high speed car crash or aortic dissection, and

2. Is getting low-bid care in my best interest?

The only way to spread the risk to get the lowest premiums and maximizing bargaining power with providers is to have ONE pool. Any more than that reduces bargaining power for everyone and makes at least some people’s cost to rise a lot.

Some people will object to a single payer as it gives the impression that some people are freeloaders. So to mitigate that, if necessary (and I think it isn’t) a tax on some universally used product (e.g. toilet paper) could be applied to ensure everyone – rich, poor, natives and non-natives – have a financial skin in the game.

I’v quite literally been there… in the back of an ambulance, with insurance card in my wallet, and having the paramedics ask the equivalent of “where to?” It was pretty surprising to me that there’s no signage, no informed person present to tell you which hospital takes blue cross or what have you. If I had to make one change to the health landscape, it’d be that there’s an easy way for first responders to know what hospital to go to.

“Readers, it would be useful if you could supply examples of “false statements or representations” by health insurance companies on the ObamaCare marketplace…”

On the Washington State Health Exchange,

https://www.wahealthplanfinder.org/

BridgeSpan Exchange Silver HSA UW Medicine

Silver (PPO)

in fact does not have the main University of Washington hospital,

UW Medical Center

1959 NE Pacific St Seattle

WA 98195,

or related doctors and offices, in-network

It does have in-network something called UW Medicine Northwest,

which seems to have no overlap with UW central.

I frequently interact with those in the health care sector, and I have noticed an increasing push from the high levels (never from the ones actually providing medical care) towards “smart consumers in health care”. The whole idea is an absurdity, and has been known to be an absurdity to economists for years. There is a well-known paper by a famous economist (Kenneth Arrow) that basically says there is no way to make markets work in health care. A summary of the paper is here: http://hspm.sph.sc.edu/Courses/Econ/Classes/Arrow.html, and the paper is here http://public.econ.duke.edu/~hf14/teaching/socialinsurance/readings/Arrow63%282.3%29.pdf.

There are some smart and humane provisions in Obamacare, and many of the better aspects are quite technical and so do not get publicized. However, Single Payer really would be a far superior solution to health care in the United States.

Sources of fraud:

Pharmacy Benefit managers Associations. Kickbacks (i.e., a ‘stocking’ fee) determines what drugs get on the shelf. More expensive drugs pay a bigger bribe hence driving cheap, effective medication off the market. This was legalized during the Reagan administration, when costs started rocketing up. It creates the same set of incentives underlying 19th century railroad cartels. They tried to do this with Internet ISPs just recently. Charging the supplier AND consumer creates incentives for cartels to manufacture scarcity – which is exactly what’s happened recently, epic shortages in cost-effective generics like methotrexate and doxycycline, which has killed plenty of people but the press doesn’t cover it (these are their advertisers) and doctors euphemistically tell their oncology patients they’re getting the best “available” drugs.

FDA is in the midst of slowly strangling compounding pharmacies, the last group outside of PBMs that buys direct from chemical manufacturers and sells direct to customers. Health insurers are creating their own compounding pharmacies and directing their customers there to collect rents. Absolutely nothing about recent changes in pharmacy regulation has anything to do with safety or cost. It’s all about middlemen price fixing and kickbacks to politicians.

Take a look at the drug formularies for insurers. They often don’t cover very cheap and effective drugs like low-dose naltrexone. So what determines how something winds up on that list if it’s not science and economis? Ads? Lobbying?

Nothing about medical treatment in America is determined by what’s cheapest, most effective & least risky for the patient. Think patient advocacy groups will tell you multiple sclerosis is an invented disease caused by fraud and malpractice that doesn’t exist in normal Paleolithic lifestyle societies? Drug companies, not patients, pay for “patient” advocacy. They won’t tell you deworming, broad-spectrum antibiotics and bad food (low fiber, high sugar) drive autoimmunity, allergy and insulin resistance in America. Companies confiscate public goods you need for your health, give you diseases and then sell you inadequate, expensive treatments you never needed in the first place.

Good update on the O-care train wreck, Lambert. Thanks for posting.

But to pick a nit, while you rightfully point out the Beltway’s narrow Overton Window, your own Overton window needs a little more width, too, to include public health care, rather than limiting the debate to publicly insured for-profit health care-for-all, which is what Medicare-for-All is.

The Overton Window is a collective entity, not an individual one (it doesn’t scale, in other words).

That said, I’m a single payer (as opposed to a national health service) advocate for two reasons: (1) I’m really rather conservative, and in Canada we have as near as possible an analog to the US political economy; we can go with what is proven to work, rather than experiment; (2) I am unpersuaded that health care ought to be delivered by civil servants, even leaving political feasability aside. We have to start from where we are, and where we are isn’t post-World War II Britain.

But I don’t have objection to the topic being raised; in that sense, my Overton Window, were I able to have one, meets your requirement, since the Overton window is about the bounds of acceptable discourse. (It’s important to remember that during the passage of ObamaCare, career “progressives” actively suppressed and banned single payer and its advocates, as did the White House, thereby nailing the Overton Window firmly in place. It would be nice if that didn’t happen again and perhaps, thanks to the Sanders candidacy, it won’t.)

When I turned 65, I tried to compare Medicare Advantage plans and regular Medicare with a Medigap plan.

I called and called and called and called and tried to learn what doctors were in the Med. Adv. plans in my area. I tried to find out out what was actually covered. I tried to be a “good health care insurance” consumer.

It was utterly frustrating, as no one would give a solid or clear answer to my questions. I would be told to get diagnostic codes; if I got them, I would be told that there might be other applicable codes so the company reps could not tell me if the treatment or whatever in question was actually fully covered.

Now, this is for the fairly clear cut health care under Medicare. I know from previous managed care insurance I’d had that it was never clear how fully something was covered until…several bills later.

Damn Obama for having no guts to go for Medicare for All, Improved.

Hi, Jawbone!!! Sounds like there’s a neo-liberal infestation in Medicare, too. We’ll have to clean it out….

Not so much neoliberal as just the effluvium of bureaucracy. You must have seen this at work in a thousand ways. Creation of lists of categories, the constructing of forms that control the categories and hence access to resources, managers scrambling to increase their budgets and staff and relative stature of their programs, the push to gather and dominate ever more data and information, rules and policies and position papers and memorandums of understanding and agreement, manuals to prepare and endlessly propagate and update, the probably irresistible tendency even without corruption and lobbying to drift off from the nominal duties and mission. It takes a probably rare set of administrators and staff to keep something large and complex with a whole lot of misdirectible wealth from running right off the rails. IMVHO. with a little personal experience from inside the beast.

I have had ACA since its inception. It did make retirement possible but my wife and I are healthy and have enough for the bronze out-of pocket. Our insurance premium has double- billed every month this year except for the last when they triple-billed. They have, of course, out-sourced billing. Now as I look for my medicare options for next year, there are enough holes drilled in it that my best choice has virtually the same premium and huge out of pocket as my ACA. I’ve investigated medigaps and part D Plans as well but this is the only way to protect house and 401k. I’m for single payer with civil servant leadership but the commercial holes in Medicare need repair.

Tests of New Features on HealthCare.gov Go to the Wire

With the Affordable Care Act’s third open enrollment period to begin in less than two weeks, federal officials are racing to fix new features of HealthCare.gov that are supposed to make it easy for consumers to find insurance plans that cover their doctors and prescription drugs. …

Insurers said the government had not adequately tested the new search tools, which are still yielding incorrect search results in some dry runs. Administration officials said many insurers had still not submitted data on their health care providers and their drugs in the correct format.

Some insurers had expected HealthCare.gov’s “window shopping” feature to go live early this week, but because the tests are incomplete, consumers are not yet able to see the benefits, prices and other details of health insurance plans that will be offered for sale through the federal marketplace.

Every time you see “racing” in a headline or a story, you know there’s a bullshit narrative, or a clusterf*ck, or, in ObamaCare’s case, both.

What neoliberalism can achieve — has demonstrably achieved, over its forty-year dominance of the world’s political economy — is fraud.

Well.. what it’s done is erode the ideas of quality, reliability, durability, to the point where nobody really blinks when an insurers change the provider network in mid-stream… because the contracts say they can. It’s not fraud in the technical sense, because it’s explicitly stipulated, and consumers have no recourse but to accept the contracts as given. The fact that this can, and does, degrade the level of service and incur unforeseen costs is implicitly dismissed.

I think the use of the term fraud is too vulnerable to dissecting argument, and doesn’t do justice to the magnitude of the case: neoliberalism has destroyed value, and the (reasonable) expectation of value, not just in health care but pretty much across the board. Cellular service providers choke transmission bandwidth right to the point where voice quality hovers around intelligibility. Industry representatives are appointed to regulatory and oversight positions, on the basis of “experience”. For-profit enterprises gut education, converting it into a vehicle for debt generation (not dissimilar to the scenario of health care, ACA not particularly withstanding). Boondoggles, carpetbaggers, “investment opportunities” that aren’t, but even without the cases of over-reach into outright fraud, it’s a collapse of the economy as a vehicle for value, into the economy as a vehicle for leaching and rent collection.

“Horizon Pharma, has figured out a way to circumvent efforts of insurers and pharmacists to switch patients to the generic components, or even to the over-the-counter versions… It is called ‘Prescriptions Made Easy.’ Instead of sending their patients to the drugstore with a prescription, doctors are urged by Horizon to submit prescriptions directly to a mail-order specialty pharmacy affiliated with the drug company”

“Drug Makers Sidestep Barriers on Pricing”, New York Times, ANDREW POLLACKOCT. 19, 2015

(It ate my bibliographic reference)