One of the big downsides of this hotly contested Presidential race is that it’s diverted attention from legislation, allowing noxious bills to move forward. One is HR 5424, which would allow the hedge fund and private equity industry, which are rich enough to pay for the few parking-ticket-level fines the SEC hands out, to escape from virtually all enforcement efforts. Worse, it would considerably weaken protections meant to stop Madoff-type frauds, and leave retail investors exposed.

This bill was nevertheless approved by the House Financial Services Committee last week, with 12 Democrats voting in favor.

As readers know, Dodd Frank stipulated that private equity and hedge funds beyond a modest size be regulated as investment advisers. That subjected them to SEC examinations. The initial round exposed widespread misconduct in private equity, including what would normally be called embezzlement.

Yet the agency has fined remarkably few sanctions, and the fines have been light relative to the extent of the misconduct alleged by the SEC and unearthed by the press.

To make a bad situation worse, the SEC retreated from its tough enforcement talk within months, and more recently, has been trying to fool the chump public into believing that its weak enforcement actions are having an impact when private equity form ADV filings with the SEC reveal the reverse, that many firms are continuing to engage in precisely the same conduct that the SEC has deemed to be a securities law violation.

But even this cronyistic enforcement charade is an offense to these Masters of the Universe. HR 5424 would gut Dodd Frank oversight. I’ve attached a letter from Americans for Financial Reform at the end of the post, which sets forth how this bill makes a mockery of the idea of investor protection. Let me highlight some of the elements of the bill that I found particularly troubling. From its text:

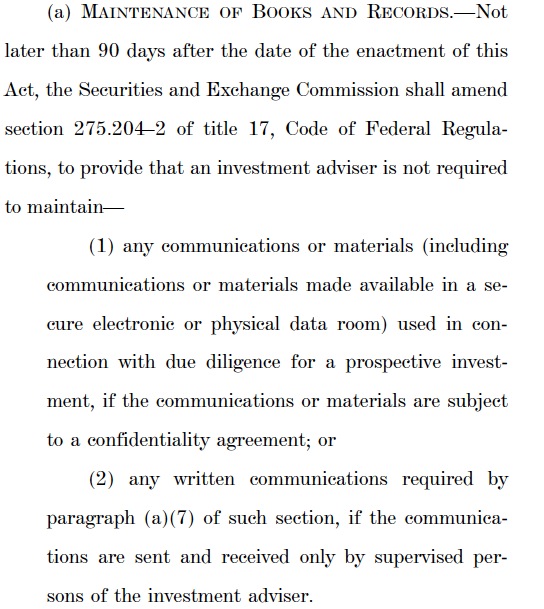

The reason this section eviscerates enforcement is that one of the very few things the SEC has been willing to do is (sometimes) punish private equity firms who have made misrepresentations when marketing their funds to investors. This provision would allow private equity firms and hedge funds to purge all their electronic files of any and all records of what they said or wrote when peddling their wares. This would make it well-nigh impossible to prove misrepresentations.

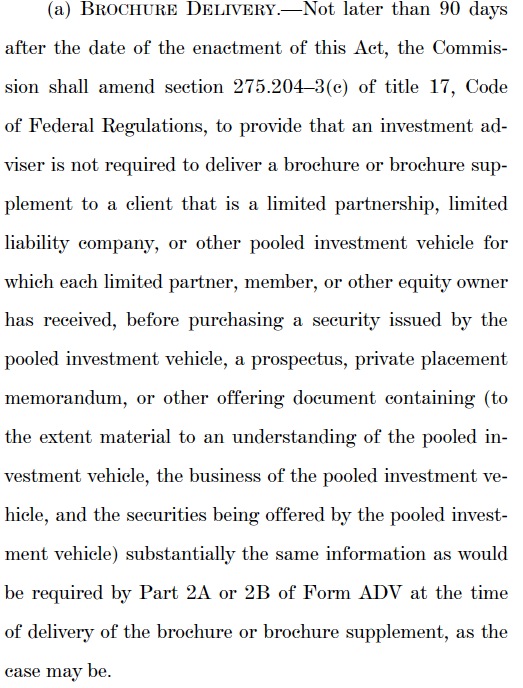

This provision may also seem reasonable but isn’t:

This provision says, “If the information is in our Form ADV, it’s effectively in our marketing materials.” But as we’ve seen, even investors with large, dedicated private equity teams, like CalPERS and CalSTRS, do not read their Form ADVs. So this is a way to evade disclosure by removing it from fund prospectuses, which historically have been the required medium for making disclosures, and relegating it to documents that investors seldom if ever consult.

Fund managers will be allowed to make misleading advertisements to accredited investors. The bar for being an accredited investor is not very high. It includes individuals who make more than $200,000 a year. In high cost cities like New York and San Francisco, where salaries are also correspondingly elevated, that includes quite a few people. In addition, certain groups of wealthy individuals who are routinely targeted by fraudsters because they are unsophisticated, such as professional athletes, top entertainers, and widows and former wives of rich men.

Finally, the bill creates exemptions to the requirement that investment advisers have their holdings independently audited at least annually. The exemptions on the surface appear to apply to closely-held funds. It carves out ones whose investors are “officers, directors, and employees” of not just the fund manger, but also of “affiliated persons,” their “officers, directors, and employees,” current and former family members, and “officers, directors, and employees,” who provide or have entered into contracts to provide services….and not just to the investment vehicle itself, but to any of its clients!

It’s easy to see how this provision could be abused by, say, having someone enter into a sham or trivial service agreement to get access to a supposedly hot manager. You can even hear the patter: “The only people who can invest are friends and employees, and OMG have they made boatloads, but the SEC will allow you to invest if we are your client. And that’s really easy to do. Just sign this contract…”

As professor Jennifer Taub stated in her testimony on the bill last month:

Just when private equity funds are in the sunlight thanks to Dodd-Frank and many have been exposed in SEC examinations as in violation of the law, you are now proposing that they be able to hide their tracks. Instead of encouraging a culture of compliance, this bill would provide a loophole for investment adviser recordkeeping requirements. Subjecting communications to confidentiality agreements or keeping them in-house would allow advisers to destroy critical investment records…

The Investment Advisers Modernization Act of 2016 is misnamed. Instead of ushering in modernity, it would send the SEC and investors back to the Dark Ages. Like the other bills today, it is misaligned with the hearing’s title, “Legislative Proposals to Enhance Capital Formation, Transparency, and Regulatory Accountability.” This bill would not enhance capital formation. Instead it would undermine investor protection and trust, which could inhibit or drive up the cost of capital. It would not promote transparency, but allow certain private equity advisers and other private fund advisers

that have been exposed as lacking in recent SEC examinations to hide their tracks. It would not encourage regulatory accountability. Instead it would punish regulatory success, depriving the SEC of the information and tools it has been using to monitor system-wide risks, identify firm-specific risk, investigate fraud, and enforce the law.

These Democrats supported HR 5424:

Brad Sherman, California

Gregory W. Meeks, New York

David Scott, Georgia

Ed Perlmutter, Colorado

James A. Himes, Connecticut

John C. Carney, Jr., Delaware

Terri A. Sewell, Alabama

Bill Foster, Illinois

Patrick Murphy, Florida

John K. Delaney, Maryland

Kyrsten Sinema, Arizona

Joyce Beatty, Ohio

Juan Vargas, California

If any of them are your Representative, I strongly urge you to call or e-mail them and tell them that this vote establishes that they are captured by the financial services industry and you will be voting against them in November as a result. You can find their contact information here. Thanks for your help!

AFR-Investment-Advisors-Letter-5.17.16

AFR-Investment-Advisors-Letter-5.17.16

Nice. This is what Liberals and Conservatives vote for, isn’t it?

https://therulingclassobserver.wordpress.com/2016/06/15/ruling-class-axioms/

Great catch. Where’s CFPB?

“The Investment Advisers Modernization Act of 2016 is misnamed. Instead of ushering in modernity, it would send the SEC and investors back to the Dark Ages.”

Of course it’s misnamed, as are all bills in Congress.

Mercifully, the dreaded word “Reform” is absent. “Reform” invariably signals a bipartisan consensus to destroy all transparency and accountability.

Have you hugged a Depublicrat today?

Thanks, Yves, interesting and germane articles today, now that the election has been handed off to the late night comedians we can peruse the more interesting fantastic and paradoxical shadows of the animal spirits dancing on the cave walls.

Sadly, both Himes and Foster were touted as progressives when they first ran for Congress,

and some suckers (like me) contributed to their campaigns.

Patrick Murphy (a former Republican) is the DSCC’s chosen candidate in the FL Senate race this year.

This is why seeing Clinton throw DWS under the bus to placate Sanders, as cathartic as that might be,

wouldn’t even begin to address the rot that has infected the Party.

I grew up in CT-4th and remember (vaguely) Himes first campaign. He was the first dem to win in the richest part of CT, beat Shays, but I don’t think anyone was under any delusions that he was anything but a wall street stooge; thats probably the only reason those snobs considered voting for him. That and voting for the GOP was going out of style since they were socially conservative.

Tweeted this to Grayson with the hope he’ll use it against Murphy in their Senate fight.

Foster while he represents a district w/lots of financial industry interests, would’ve been protected by a liberal base in primaries and a moderate district that won’t use financial de-regulation as a litmus test in an election v. a Republican.

Guess Foster is owned by the DNC and/or just rubber stamps anything put in front of him that’s outside his core interests.

Foster didn’t just vote for the bill in committee, he’s one of the 5 Congress critters who co-sponsored it! See the second of my links at1:33 PM in reply to Jame Levy. Click the tab marked “Cosponsors” in the middle of the screen.

Foster was recruited by Rahm Emanuel. Known Blue Dog. ‘Nuff said.

Is Meeks also one of the TPP turncoats?

Good catch! He certainly is. Himes of Connecticut, Delaney of Maryland, and Sewell of Alabama are also Trade Traitors.

http://www.nakedcapitalism.com/democrats-who-voted-for-fast-track

Typical of the corporate CBC flunkies. In my district Rangel is retiring, and the Dem machine is already eagerly positioning another one to take over from his worthy tradition of service to FIRE.

Himes ties to wall street is the worst kept secret in DC case and point.

That is a bad video, but that channel did do this one too and I could watch it over and over and over…. Other good ones on that channel too Check it out.

are also Trade Traitors.

Could we call them traders?

We need something which will get people to pledge to never vote for any Congress Critter who votes for any of these trade treaty abominations.

Electronic notification, with follow up form or handwritten letter with actual signature.

And let Hillary know over and over that we know she’s a weasel and weaseled in saying she could not back the TPP — in its current form. Which could be made supportable by a few grammar and word usage changes, but still be the abomination of all abominations.

Brad Sherman, California

~~~~~~~~~~~~~~~~~~~~~~~~~~~~~Just left a message with the person who answered Mr. Sherman’s phone that I will not be voting for Mr. Sherman in November if he’s supporting this bill.

Thank you!

I just sent an email to Sherman and will call on Monday! Too bad Patrea Patrick didn’t make the top 2 runoff.

Thanks!

What a fine kettle of corrupt insider-trading traitors we elect……..

just shows that wall street is just plain rigged, and gets help from Congress to rig it, this means your 401k, IRA,ESP, are all just waiting to be gutted.

I think ‘Corzined’ is the appropriate term…..

Precisely.

I tried to find the full vote online but could not. Might you give us a link or tell us who voted against this monstrosity? I see it was proposed by a Republican from Virginia with the tell-tale bipartisan co-sponsoring that only Oligarchs can muster.

Fortunately, it hasn’t passed the full House yet. Here’s a PDF file with a listing of how the House Financial Services Committee voted (47-12):

http://financialservices.house.gov/uploadedfiles/crpt-114-hmtg-ba00-fc109-20160616.pdf

Here’s the bill’s information on the Congressional web site:

https://www.congress.gov/bill/114th-congress/house-bill/5424/

Thank you!

I see two NY Dems who actually voted No. Given where they are from, good for them. Is that Ms. Waters Maxine Waters? If so, good for her, too.

BTW, there are only 435 Reps for us 310+ million Americans, but we have 59 of them on one Committee? I dimly remember (I was a kid) the House Judiciary Committee voting to propose impeaching Nixon. I can’t imagine there were much more than half that many people on the Committee, but my memory may be faulty.

Rather than post, I looked it up: 38 members of that committee in 1974. Odd that an older and broader committee like Judiciary would have had so many fewer members than Financial Services (or was that once Banking? even so).

There’s a link in the post:

http://financialservices.house.gov/uploadedfiles/bills-114hr5424ih.pdf

Not surprised to see this name:

Kyrsten Sinema, Arizona

The local opinion of her can’t be shown on a family blog.

My in-laws are contacting newspapers, local bloggers, etc with a link to your story. This might leverage the impact of emailing directly the congressman. Terri Sewell. Sewell is from one of the rotten boroughs, but we mentioned that this has long term impact on safety of state and local government pension schemes to put a bit of bite in the message.

But as stated there are the forms ADV which investment advisors don’t bother to read, which IMHO says find another advisor. Tell that advisor you want a summary of the ADV. The fact that major public investment vehicles hire advisors that don’t read all the materials is the big issue IMHO. The agencies have hired at a minimum incompetent folks, and a worst out and out crooks. Since the powers that be want to go let the buyer beware (which is always a good idea adding a dose of financial paranoia) then make the directors of the investing funds personally liable for making the bad investments.

This follows my thinking that the financial crisis was caused by buy side advisers incompetence, or criminality. (And the directors of the funds willingness to defer to their incompetent advisors, and not ask the hard questions they are supposed to ask)

Your thinking is correct , financial crises was definately caused by fradulent criminal activity on industrial scale. Watch documentary “Inside Job”, if you haven’t already.This Documentary is conclusive on causes of financial crises.

*Sigh*. Not true. I was in Japan during its bubble years, and its bubble and bust were much worse than ours. Their aftermath was different was that the reckless credit expansion was limited to domestic Japanese institutions (very little spillover to global economy), they were a big exporter and global growth was strong in the 1990s, buffering the impact of their bust, and their society is much more cohesive and many measures were taken to share the pain.

Their crisis was the result of very rapid deregulation…at the insistence of the US. And I’ve written a book on the crisis, and deregulation and bad incentives were much bigger causes (as in what made this a global financial crisis, as opposed to a mere S&L level crisis, was derivatives, specifically CDS written on risky subprime tranches. That was not criminal).

Some crises are the result of crooked conduct. The railroad speculation of the later 1800s had lots of stock manipulation and fraud. But the tulip bubble was a pure and simple speculative frenzy. Charles Kindleberger has written the book on manias and crashes.

But yes, there was plenty of criminal behavior in the making of the loans, the selling of them, and in the foreclosures. And merely being reckless and greedy (in the cases where that was the main conduct, it varied by bank) should have led to the replacement of the boards of all the firms that were rescued and their top executives being fired and barred from ever working for or with a regulated financial institution again.

And still no significant prosecutions of the perps. Worse, no one seems to care or notice any longer.

Yesterday, the AUSA for Los Angeles announced that Angelo Mozilo, everyone’s favorite umpa loompa, would not be charged for the rampant fraud he directed while heading up Countrywide. CNBC had a very short blurb which only showed briefly before falling off the home page. WaPo, to my knowledge, still hasn’t reported it.

http://www.cnbc.com/2016/06/17/ex-countrywide-ceo-mozilo-to-not-face-us-fraud-case-source.html

Well , It seems that my poor understanding of English grammer has caused misunderstanding. What I meant is that crises of 2007-08 was caused by fraudlent activity and not that all crises are caused by frauldlent activity. I believe first bubble with criminal activity was south sea bubble happaning around 70 years after tulip mania. And you are right that not all bubbles are result of criminal activity some are merely result of human irrationality and herd behavior. What is surprising is though that even after a number of crises in different part of the world , excessive deregulation is still supported and probably with much more intensity than before. Instead of of imposing reforms and regulation , some are proposing to opt for “helicopter money”.