A raft of stories at the Financial Times verges on funny, in that they affect consternation that EU bureaucrats are intent on taking a big chunk out of the City’s business. It was obvious that this would happen and we said so repeatedly over the summer. Yet it’s been astonishing to see Brexit boosters, the few that wander into Naked Capitalism and the ones who are well represented in Fleet Street, act as if the UK somehow has the upper hand. As we’ve written, Brexit fans have chosen to ignore repeated, crystal clear, and surprisingly unified warnings from EU leaders that they will give the UK no quarter if it really does go through with a Brexit.

The current cause celebre is that France and the ECB are working to expedite a plan to move Euroclearing from the UK to the Continent in the event of a Brexit. This was an obvious target: the ECB had already tried to extract Euroclearing from London. Britain fought back and the European Court of Justice ruled that the ECB could not discriminate against the UK because it was an EU member.

No EU membership, no impediment to moving Euroclearing. And the new wrinkle is the Europeans plan to set the process in motion more or less contemporaneously with the UK’s planned date for invoking Article 50.

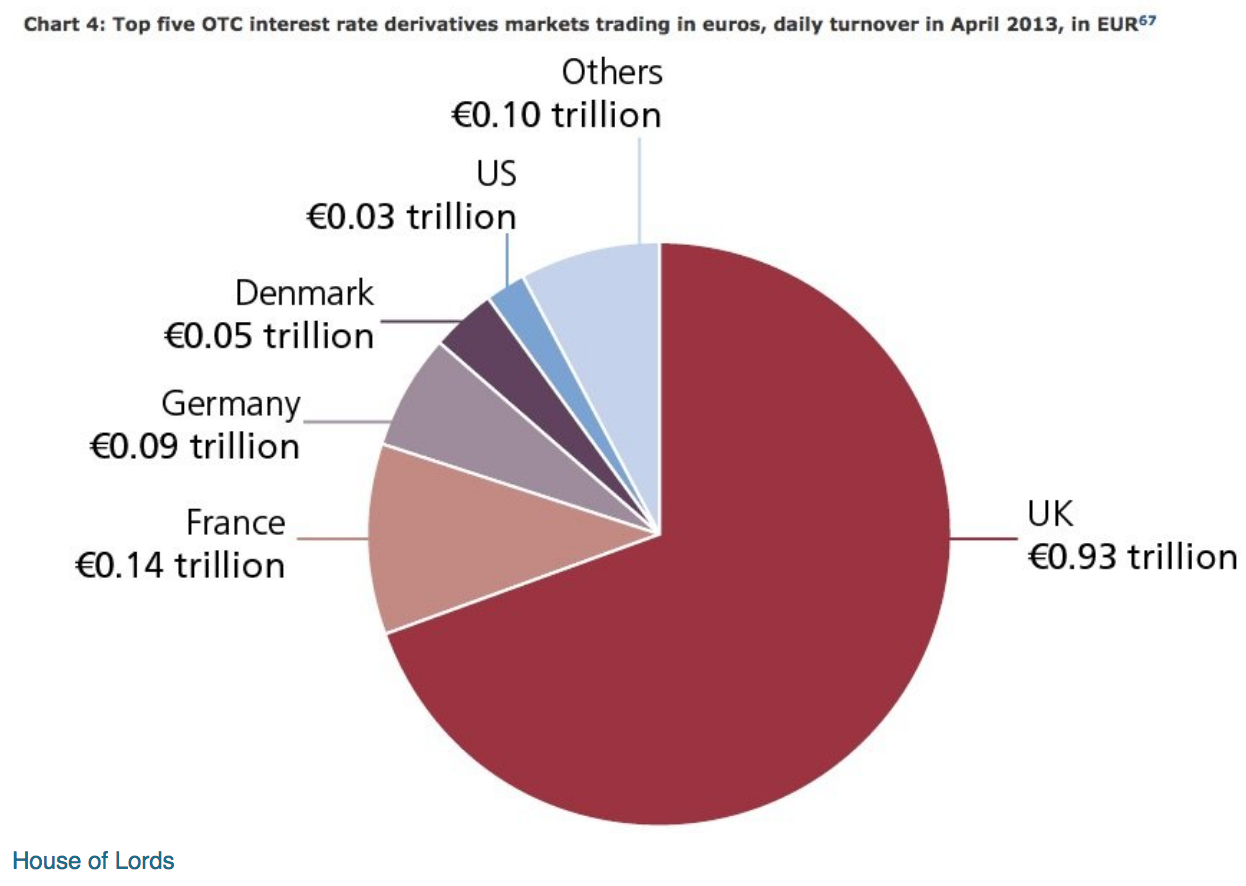

Defending London’s cornerstone euro clearing business has been a totemic issue for UK governments. London is the world’s biggest centre for clearing euro derivatives, handling three-quarters of all transactions, with an average daily value of $573bn, according to an Intercontinental Exchange (ICE) paper recently circulated to EU member states.

The paper, seen by the Financial Times, argues that “forced repatriation” of euro clearing would “deprive European banks of access to liquid trading and clearing facilities and create fragmentation”. ICE, the largest operator of exchanges and clearinghouses in European utilities, added: “This would increase costs considerably for banks and customers.”

Simon Kirby, the UK’s City minister, has also warned that the euro clearing business would probably move to New York if the EU attempted to undermine the UK’s dominant position, leaving Europe “worse off”.

But France’s President François Hollande has called for euro-denominated clearing to be relocated to the euro area after Brexit, saying that such an outcome would “serve as an example for those who seek the end of Europe”.

Now of course, the issue is “cost for whom and measured how?” London is the premier foreign exchange center of the world due to its time zone advantage and also being a hub for UK and one-time British empire banks (Barclays and HSBC) that had very extensive foreign branch networks. That meant they not only dealt in large volumes of foreign exchange, but they also dealt in exotic currencies. As a customer, if you are dealing strictly in Euros, it’s hard to see much efficiency difference whether clearing in London or the Continent. It’s customers that are dealing in multiple currencies who might see efficiency losses. Needless to say, the ECB is concerned about customers who deal in Euros.

And there is a policy argument that high liquidity and super low transaction costs merely encourage speculation. If as some commentators whinge, moving Euroclearing to the Continent will make derivatives transactions more costly, that could be desirable. But you’d need to look further to see which type of transactions would be most affected and whether they had social utility or not.

The EU also has a national sovereignity argument of its own: banking is a strategic asset. Having more banking operations under domestic control is politically sound. If London is out of the EU, and therefore out of EU regulators’ control, then it is foolish to be dependent (or have significant dependencies upon) banks outside your political and regulatory purview. That is arguably more important than efficiency (meaning cost) considerations.

For those new to this topic, Business Insider provides some helpful background and data:

Clearing houses in London manage credit risk, acting as a middle-man in swaps and derivatives trades to guarantee the contract in the event that one of the parties involved in the trade goes bust.

The acceptance of English law and widespread use of English language has made London a hub for clearing globally. The charts below, from the House of Lords select committee report on Brexit’s effect on financial services published this week, shows just how dominant Britain is in the market:

In the Financial Times comments section, a reader provides a high-level overview of the implications for banks:

Coase Theorem

Ok – so what’s going on is that

1. The UK has a very lax regime (by global standards) for letting non-EU entities do business from London on the basis of their authorisation in Japan, USA wherever (you can, to put it simply, register with the FCA etc on the basis of your home country status)

2. If the UK is in the EU the entities that are doing business in London can then passport into the EU

3. So a US entity (not a European subsidiary, the US entity itself) can do business across the EU via a London branch

4. The US entity will trade across Europe via its London branch, often under the same trading documents as they use out of NY (which means you’re netting all these trades) and via clearing houses (which also means youre netting) (the big two in Europe are LCH and Eurex – and they both have big US trading businesses hence netting across European based US dollar trades as well as Euro trades)

4. So capital deployed in the US entity can be used to access the European market – this is more efficient than setting up a new bank and capitalising it because you won’t have netting if the trades are divided between legal entities (separate to the cost of the separate entity)

5. Thus, London is how the New York dollar liquidity pool is accessed by the European market (and gets netted against Euro trading to boot)

Passporting is one half of the raison d’etre for trading and thus clearing out of London because it is a reason to trade out of London.

The ECB probably can, IMO, stop non-EU entities clearing but hasn’t done so till now because doing discourages the use of Euros as a reserve currency. Also, the EU has had most of its Euro trades taking place in the EU (the UK) so its relaxed about not having a restriction. The US doesn’t restrict either but about 80 per cent of dollar trades by value take place in the US – the issue for the EU post Brexit is that most of the trades in its currency will be taking place outside of its supervision. I don’t think they will accept that and I think the US certainly wouldn’t.

If the EU doesn’t restrict clearing to the EU, London branches of US entities still won’t be able to access the European market due to passporting being gone so one of the benefits of doing business in London falls away – the other key benefit, that London trades can be netted against US trades (because they are done by the same entity) remains but there will be fewer trades you can do from London. So the argument for trading moving to the US is simply to do with redeployment of capital and personnel to NY since, in relative terms, capital will be more efficiently deployed in NY since one the raison d’etres for London has fallen away.

So this is why clearing matters, not the small number of people who work at CCPs

I expect another winner will be Singapore, particularly on the derivatives side.

In another proof of how deep denial about Brexit impact runs in some quarters of Britain, the lead story in the US edition of the Financial Times as of this hour is Japanese banks warn of leaving London without Brexit clarity. From the top of the story:

Japanese financial institutions have warned they need clarity on the UK’s future relationship with the EU or they will begin moving some functions from London within six months.

Executives from Japanese groups including investment banks Nomura and Daiwa Capital Markets laid out their position at a “frank” meeting on December 1 with the UK City minister Simon Kirby and Mark Garnier, international trade minister with responsibility for financial services, according to two people with knowledge of the meeting.

One senior executive of a big Japanese bank said this week that the uncertainty surrounding London’s future as a gateway to Europe meant it “would be better for our EU-based customers to have an alternative hub”.

The funny bit here is that is is hardly a secret that foreign banks in London started scouting for real estate and getting licenses in various spots in the EU almost immediately after the Brexit vote was tallied. And several have made loud noises about how many jobs they will pull out of London.

The only difference is that the Japanese have a different way of going about things. The ritual of the “frank chat” (which they can have only in a foreign tongue) is to respect the form of maintaining a relationship while telling the other side that Something Has to Change. That is to give the other side the opportunity to shift their position. The ritual of formality, in other words, is to precipitate a negotiation if one can be had, or otherwise to bend over backwards in being polite by giving a type of formal notice.

The only part that may look like a surprise is that the Japanese say they will start moving operations so soon. But again, it’s almost certain other foreign banks are on the same, if not earlier timetables, via measures like suspending hiring in London, accelerating attrition, and adding staff in other centers. The one big difference with the Japanese is that they need to have Japanese nationals in senior positions. Relocating that level of employee (deciding who goes where) is a fraught and difficult process (as in the internal politics are even messier than in Western firms).

So the really noteworthy element is that the Brits are so offended that the EU is playing nasty, as one pink paper commentor wrote. This isn’t beanbag, and EU officials have said from the very outset that they were not going to be nice. Shame on the British pols, press and public for not taking them at their word.

I’ll take a stab at the pro-Brexit position. First off I see Brexit as a power struggle between the British elites and the British working classes. For decades the British elites have hidden behind the Brussels boogeyman as they lowered the standard of living of their working classes. I would say these elites (at least on the Tory side) didn’t really want Brexit and played to lose like the Washington Generals but Boris Johnson just went a little too far with that Independence Day speech…

So seen as a British power struggle the more Brexit hurts the elites and urban bourgeoisie – the better. Yes the working classes will take some collateral damage but so be it. The key thing is for the working classes to develop self-awareness and an identity. They should use their combined power to hammer the British elites every chance they got until these elites learn to respect the interests of the working classes.

So contrary to what a British tabloid might say, in a strange sense the British working classes and the Brussels elites are on the same side. Of course Europe should threaten to pummel elite Britain if they do a full Brexit. Europe should loot as much as they can from The City. And the British working class should cheer their betters’ comeuppance. London is basically a no-go zone for the working classes with its wealthy 1st world globalist elite being serviced by a 3rd world proletariat. Might as well drain the swamp of many of those banksters and other non-productive elites. Who knows, if Europe strips enough banksters out of London maybe real estate prices would come down a bit.

And yes when banks leave tax receipts would drop but then, I suppose, so would immigration. Currently the banking industry pays around 31 billion in taxes a year while mass immigration is costing 17 billion. So the impact of cutting the UK banking sector by 30-40% while stopping most immigration would be more or less revenue neutral.

The other side of the equation is that Donald Trump’s victory gives the possibility of a US/UK free trade deal. So in a sense this makes a real Brexit more possible since what Britain loses from their relationship with Europe they might gain back from their new relationship with the US. And US manufacturers may have a new market to expand into and vice versa if Britain moves away from finance and starts concentrating on actually making things, they would have privileged access to the huge US market.

So where is that 17 billion figure from?

Brexit is being driven by the far right free market fundamentalist elite who see EU regulation as a barrier to their wet dream fetishes. The most important are Rich people with something to gain: murdoch and a few hedge fund types. They are supported by vain self serving politicians who see the EU as a limit to their powers.

These guys promise a golden era of free trade, just as they are leaving the worlds most successful free trade area.

They promise deregulation while exiting the EU will create the biggest mountain of red tape ever seen by British business.

The working class are their pawns, nothing more. They have no agency save that given them by the right wing press.

Sadly the UK is split on Brexit irrespective of class: the “lumpenproletariat” may well have intended that Brexit be anti-finance, but then there are the workers who actually make or transport stuff who know that they are part of a European supply chain. Similarly among the elite, there are those who feel that the Eurocurrency was marginalizing the UK anyway, and could end badly so it was time to bail out, while others focus on the economic and networking losses associated with Brexit. Then there are some pensioners who do not need to work and nostalgically “want their country back” while others value the freedom to retire elsewhere. Finally in finance, there are those involved in money-centre traditional banking and wanted in and those who are on the investment side dealing with the whole wide world…

I say sadly, because a split country whose finances are precarious is unlikely to get the best deal. And even if the UK starts with a good deal, they may find that Europe renegotiates the terms more sourly later (“we can’t manage special deals with 150 countries – take it or leave it”).

The EU and Eurozone are doomed anyway. Anything that hastens its destruction is probably a good thing in the long run.

I believe the £17bn figure comes from a Migration Watch report but the use made of it by Trumpening ignores two important points.

It refers to calculations made with reference to all migration. The ‘cost’ arises as a result of immigration from non-EU sources, principally large-scale immigration from Asia and the Caribbean, not EU sources, so stopping immigration from the EU would not affect the ‘cost’.

Most immigrants to the UK have come from countries other than the EU.

The figure is in any event potentially highly misleading as it excludes payments to the Exchequer made prior to the period covered by the calculations. Thus it includes the ‘cost’ figures for pensioners who migrated to the UK, say in the 1950s, without taking account of their contributions made to the taxman prior to the period of the calculations.

Pensioners are always going to feature as a cost to society because of their pensions and health care costs.

So I am afraid Trumpenings calculations are unlikely to arise in real savings to the UK Treasury unless a lot of Asian and Caribbean pensioners are deported. As presumably many of these are now naturalised British citizens, this seems most unlikely to occur.

I am also somewhat sceptical that a trade deal with the US will deliver much benefit to the UK. Trump has said he wants an America First policy which hardly portends gifts to the UK. Besides, the UK’s strengths are in services, which are often difficult to supply to markets with markedly different time zones. Manufacturing, I am afraid, is never going to come back as a large scale employer.

Equating a single market with a free-trade area ignores non-tariff barriers which nowadays are often more important than tariff barriers.

London had added a million people in the last 10 years and is at bursting point on the transport systems. I hope we lose lots of bankers and the population goes down so london can be more livable. Life is not all about making money strangely enough.

Spot on. The thing that won Brexit was the establishment threatening it would harm The City. They are so out of touch, they thought it would scare people. Quite the opposite!

Germans look after their people and keep the banks in control. Sadly on foreign soil (Greece) they don’t do this, so I’m not convinced the EU is on the same side as labourers. The key difference between the UK and German establishments though is the Germans won’t let the banks rape their own nationals. The UK establishment see British workers as sub-human and are very happy for all banks to farm them.

I’d also add that as a result of banks farming the locals via land prices banking is *not* break-even. The cost to ordinary people is huge.

Regarding trade deals – what would the UK trade? It’s all “services” which is basically money laundering then bankers take the proceeds and exchange fiat with plebs for being waited on hand and foot. Nothing is produced. What will we trade?

Paris, Berlin and London … are like Highlander. Only one can be left standing. Sorry Rome ;-(

It seems bizarre that so many decision makers in the UK don’t seem to realise that when you opt out of a trade pact based (at least notionally) on mutually beneficial trade, then immediately all your ‘partners’ become competitors and mercantilists and will treat it as a zero-sum game. It is the job of French and Belgian and Irish and Dutch politicians to bring jobs and wealth to their country, not to be ‘nice’ to the UK government or people. With the Brexit vote every competent national, city and regional government in the EU will have been setting up committees and agencies with the specific task of grabbing as many jobs and industries as they can. If they didn’t do that, they are not doing their job. There is simply no incentive for them to do otherwise, especially when the UK government is in such a very weak negotiating position.

But worse than that, as demonstrated by Boris Johnsons idiotic comments about Italian Prosecco, the British government (and I think by extension, much of the establishment) doesn’t seem to realise just how weak their position is. It reminds me of Syriza when they came to power, convinced they had a far stronger hand than they did in reality. They were of course clobbered, as will the UK government be on the first day after the A.50 declaration is made.

Incidentally, writing from Dublin I can confirm that there is a constant stream of delegations from the UK looking at office space – I’ve no doubt the same is happening in Amsterdam, Paris, etc. Very few, if any, are signing lease contracts yet (so far as I’ve heard), but they all seem to be rapidly planning their exits if necessary. Its not just the finance industry – the construction industry in the UK in particular is very worried about being excluded from EU tendering contracts as if anything the legal nightmare of Brexit is even worse in Construction than in Finance as there are so many overlapping national and EU requirements.

I don’t think many decision makers voted for Brexit. I even suspect that for many, it did not even cross their mind that a disgruntled part of the population could actually lean that way.

Because they are special…

Trade could never leave the City

They are deluded.

Absolutely – the view of the Brexiters is that UK can ask for everything, because it is in the UK’s interest, and the foreigners should of course stop paying attention to thei foreging national interests and start treating the UK ones (or I’d say the English ones) as the only ones that matter.

Re Dublin – TBH, I doubt it. The headoffice may be located in Dublin, but the “stuff” (or “staff”) will be then located somewhere else.. My money there is on Amsterdam – it’s almost as if you were in an English speaking country, excellent transport links to just about anywhere in the world (I bet Schipol has more flights to the US than Dublin does, and many more to Asia – and I’m not even mentiioning the fast trains to Brusell, Paris, Berlin etc.).

The main problem with relocation IMO is that even getting 10k people a year relocated into a new location is non-trivial. Say both Dublin and Amsterdam have populaitons around 1m, about 1-.5-2m if you count “suburbs”. 20k immigrants means say 15k familiesies, so about 20k children. Let’s say there’s 100 schools in Dublin – so you get extra 200 pupils per school, and I can bet those immigrants are going to be much more selective with schools than to pop them into any that comes.

Same with hospitals, GPs etc. etc.

I’d say to Dublin etc. – be careful what you wish for..

I agree that Dublin won’t be the big winner. The main constraint is office space and accommodation, there just isn’t enough now and not enough will be constructed within the next 2-4 years. Dublin office rents and housing costs are rocketing at the moment due to a shortage of both. The damage caused by the crash is still a key issue here – banks just aren’t releasing sufficient money to the development market to create more supply. From what I’ve heard no major developers are anticipating that Brexit will substantially increase the demand for office space. A major part of their thinking seems to be that even if there was a demand, the construction industry at present simply could not meet it, so there would be no point in trying to entice very large one-off banks to move.

My understanding from various whispers I’ve heard is that it is very unlikely that any banks would opt for a relocation to Dublin for the reasons you suggest, but mostly because there just isn’t the office space available. However, as Dublin has a very large presence of many US and other banks for tax and other reasons, it would be comparatively easy for lots of banks, US ones in particular, to simply opt to beef up their Irish operations at the expense of their London ones. It would be more an incremental process than a full blown move. It all really depends on what they will be able to get away with in terms of passporting.

As for the other reasons, I wouldn’t underestimate the cultural attraction of Dublin for US and other workers. I know a few US finance and IT professionals in Dublin, and for many it was the relative similarities in language/schooling/law that made it an easy move. Good quality Irish private schools and universities are plentiful and generally significantly cheaper than the UK or US equivalents. And you’d be surprised at just how many daily flights here are from Dublin to the US (although not to Asia). Its 20 minutes from the city centre to Dublin airport by taxi, that’s a major consideration for many companies.

Interestingly enough, the UK has managed to stay in the Unitary Patent system and remain a part of the Eurpopean Patent Office. But those are more treaties and agreements rather than purely European institutions.

https://www.gov.uk/government/news/uk-signals-green-light-to-unified-patent-court-agreement

The powers that be may fail, but they are certainly trying to remain as European as possible after the Brexit vote.

It makes sense for the UK to maintain as many non-EU treaties as possible to minimise disruption, and there are many pre-existing bilateral arrangements which stayed in place when the UK joined the EU. As one example, there was a pre-existing agreement for the free flow of people to live and work between Ireland and the UK, on top of which are the arrangements under the Belfast Agreement.

The problem will come when these arrangements fall foul of their interrelationships with EU laws and agreements. An example would be the difficulties in maintaining an open border between northern Ireland and the republic for workers, while the Republic maintains its open borders with the EU. If Ireland becomes a staging post for migration (in either direction), it may come under pressure to choose. There are numerous grey areas which will open up, giving countless opportunities for confusion and legal nightmares.

Of course, one of the ironies of the anti European movement in the UK is that one of the things they hated the most was the European Court of Human Rights, which had nothing to do with the EU and is unaffected by Brexit.

Careful Yves, or you’ll get NC not only on a US blacklist but some UK one too.. Becasue who isn’t pro-brexit, is clearly a dupe of EU that wishes the UK only the worst. While you can’t be braided traitor in the UK, you may get on some other T-list..

More seriously, UK is toast short term. Unfortunately for the UK, the first few months post-Brexit the economy performed (which is no wonder, as it was primed to peform – and the low sterling may have helped in some areas). This made most pro-Brexiters thing all’s gonna be well, becasuse, you know, the experts got it wrong! (again).

Except that the warnings from the real experts weren’t about 2016, but for a) the EU negotiations b) the effects of their likely failure and/or hard Brexit. Which is not going to happen for at least another six months or so. That is, unless of course we get to see more -xits, like Holland (possible win there, but maybe just a stalemate), France (unlikely), Italy (EUR-xit? Yes, EU-exit? No)…

I think the big ‘unknown’ of Brexit is what happens with all the money of varying degrees of ‘hotness’ which has piled into the south-east, both into the City and especially into property. If the Chinese, Russians, Greeks, etc decide its safer to cash out for now, then there would be very serious consequences as it would lead to a major property crash with obvious consequences for the domestic banking sector and sterling. But I think its equally possible that they may decide to hang tight for the long term, or even see a dropping sterling as an opportunity for more investments.

Agree with this, and with comment like it below. The City will just turn to more dirty and dictator cash, and Parliament will lower standards accordingly/as dictated. I once had a Nigerian cabby tell me “every dictator in the world keeps his money here,” which wasn’t true at all. But it was my first view into how The City operated.

Will be interested to see whether there are sentimental or other inducements to Trump & Whiteco. to throw these guys any bones.

The secret is they let people was dirty money but *only* through land. Land price ramping is the strategy.

>to see Brexit boosters, the few that wander into Naked Capitalism and the ones who are well represented in Fleet Street, act as if the UK somehow has the upper hand.

I hope you aren’t talking to me. I don’t consider myself a one-issue person that “wanders in”. That said:

1) “Booster” is not a good characterization. It’s the thing that has to happen, not that it will be good for anybody. It’s a tumor removal, except both sides are pestilences on humanity.

2) It needs to happen so that there are no more Greeces.

3) It will be worse for Britain than the rest of the EU. But the entire course the EU is taking is right towards the suck, so making Britain (the 2nd largest economy) take more than it’s otherwise share of the future suck will lower the EU level of suck. But be very sure of the suck.

4) Re #3, think before posting here gleeful notices in the future about any particular Britain suck unless the EU is excreting gold bricks. I doubt that will be the case.

5) There will be plenty of money for “The City”… it will be even dirtier than the current money flowing thru there, though. Hard as that is to believe. As you said, “The UK has a very lax regime (by global standards)”. This is unfortunately a strength Germany will not offer. The EU is not the world.

6) If the EU doesn’t straighten up it’s ship, it’s going to disintegrate… and therefore the people that leave first (um, Britain) will actually have the lowest level of suck. Not predicting this, though.

Also, just for laughs, despite (or maybe because of) #1 I’m still pretty darn sure it isn’t gonna happen. The type of money that’s going to expect to come into The City will scare even those particular bankers

My question… is it really the pro-Brexiters who are over-optimistic or the anti-Brexiters now in a position to negotiate the exit?

Perhaps very slightly (though not very) off-topic, but still on UK matters, I attended the Leveson Lecture given by Vince Cable (Cabinet Minister 2010-2015) last week.

The money quote of the evening IMO was when he defined the heart of the UK’s problem – ‘the unwillingness of UK politicians to stand up to the press barons’.

Cable was of course the Minister who did the most to block Rupert Murdoch’s bid for 100% ownership of Sky six years ago which would have further tightened Murdoch’s hold on the UK’s media – and thereby the UK political system. Now Murdoch is back for this, presumably reckoning the UK government is now too weak to stand up to him.

I cannot recall which Brexiteer it was, but one of them said quite recently that the Brexit campaign was like a fight between men and boys. The boys were Cameron and Osborne, the men Murdoch and Dacre (the Daily Mail editor).

Europe has destroyed or seriously damaged the careers of three successive Tory Prime Ministers – Thatcher, Major and Cameron. May is probably, rightly, worried she will be the next. Although 51.9% voted to Leave the EU there is no majority for any one direction of departure. For now May can keep everyone hoping she will head the way they want but as soon as she shows her intention, the knives will be out.

The brinksmanship isn’t even close to beginning.

#1 What are the chances that the city decides it isn’t part of the UK? They already take that view in quite a few very important ways. The city tries to remain inside the EU while the UK leaves. It wouldn’t look all that different from the way things are now. For instance- “english law” in the above post, with respect to clearing and derivatives is city law. Doubt that? How did the LIBOR scandal turn out?

#2 What about cash? I’d imagine that the city has a very sizable hoard of EUR currency. Actual bills, most of which are laundering proceeds. Couldn’t that back some sort of offshore haven in the city? Isn’t that how EU members have always treated it? Their home away from home?

IMO, this is the city trying to separate itself from the UK in perception. In fact, they already are separate. The city tries very hard to pretend it’s “english” or UK, or british, or whatever the queen is calling it these days. They are not. It’s a label of convenience that can change with whatever the city decides. Who decides? The city of london corportation. They sit above both the UK and EU in banking matters. They ARE the bank.

the city stays, that’s my bet on how this plays out, whatever “brexit” does. EU clearing or GBP clearing? Which is worth more, assuming that the GBP, and the queen herself even wants to try to yank GBP clearing in this instance. It’d be a lot easier on the city’s bottom line to ditch GBP, if it had to.

Who feeds the city? Will there be an airlift? Where is the water system actually housed? Power? Will they resort to beaming power to London? Who are these ethnic Londoners ready to fight for their city state? Will the Queen stay?

Oh sure, they can pay for it, but capital can just move. Brussels, Rome, Venice, and on and on will all stand ready to replace London which derives it’s power from vestiges from the old empire. London wouldn’t be the first city to try to be called “the city.” Istanbul literally means “to the city.” As in, Constantinople was so important you didn’t even need to specify what city. This is why certain elements will panic. London is nothing special. It can be forgotten just like that.

I don’t follow this at all. I’m wondering if China isn’t the reason Brexit succeeded. That it is more important for the UK to have a free hand dealing with China than to remain in the EU. The UK has imported lots of Chinese steel and they gave them the contract to build the Hinkley (?) nuclear power station. I read 2 or so years ago that the City of London didn’t quit the derivatives market but instead moved it all to Hong Kong. And shortly thereafter the demonstrations in Hong Kong began so maybe the UK was trying to achieve more banking freedom there. I’d like to know what the relationship is between the UK and China currently and if staying in the EU was harming that relationship. They (UK) seemed to be trying to have cake and eat too when Cameron was arguing about certain (banking?) concessions from the EU and lost. And it seems that Brexit was actually the result of that impasse. Clearly the EU is protecting the euro against London’s business practices – and that would be interesting to hear about too.

Brexit succeeded because New Labour and Tories are unresponsive. Whatever game Cameron had in mind are irrelevant. This was a rebuke to the political establishment. It’s like Trump. Once he became the enemy of Jeb he went from a “none of the above” placeholder to a presumptive nominee.

Tony Blair was the final straw, and if Scottish independence had not become such a big deal (largely a result of New Labour being seen as an enemy), I suspect the numbers would have been worse for Remain.

China, Putin, whatever Muslim country annoys us at the moment, etc don’t really matter. Governments who say, “I’m smarter than you and am telling you not to believe your lying eyes and worship me,” ultimately fail if they don’t produce results. There were two main actors: the Tories and New Labour. Both are unpopular, and both supported remain relying on fear to win votes. Hillary and friends are simply Ozymandias. Or as Tolkien described the decline of Minas Tirith wasn’t caused by orcs or goblins but when old men worried more about their family history and not the lives of their sons. Nothing changes. Statues of bad kings get ripped down. Pensioners in Northern England don’t care about free hands with the Chinese of what kinds of legs they can use. They care about football scores and the rent. Blair sent their kids to bleed in a far away land then told them to vote remain while he pocketed millions over lies. The rest is white noise.

I largely agree with you . I am a Brit. The failure of the Remainers was the same failure as the Clinton gang ; they thought they had their perception management well honed and that would succeed. But we’re all done with that now . We all live in our own little bubbles and that’s the basis of the world view we hold now, not what some stooge in Washington or Westminster tells us. But look where are they now Cameron and Osborne . They are on the Washington lecture gravy train at $75,000 and upwards and Obama will no doubt be readying himself for January with some lucrative book deal, consultancy etc etc . None of us are fooled anymore . That’s their problem and they don’t know how to deal with it because they don’t have a model for it and they don’t have a clue how to construct one because it would mean owning up and that is just not an option.

I am completely baffled about why Brits believe they can leave the EU and still retain all the benefits. I envision that Brexit will eventually turn into something like the US-Canada relationship.

The EU governments would be doing a disservice to their own citizens if they did not take reasonable measures to ensure that activities like Euro-clearing shift back to EU financial and business centers (Paris and Frankfurt come to mind for this particular activity). If they put the same rules in place that allow for London to do the same type of clearing as the US, London would still retain a bunch of business but probably not the lion’s share. London will simply need to compete without having the financial passport and freedom of personnel movement that they enjoy now.

For my mind, bearing in mind how incompetent we are as a species in prediction, I would expect UK to become the leading smuggler into the eurozone using Irish intermediaries.

I am thinking mainly of physical goods but we might also see the City’s army of commission-only salesmen marching through Europe collecting deposits perhaps with UK residency and/or passports.

All UK trucks on European service will be “sold” into Dutch or Belgian ownership and Northern Ireland will suddenly become rich and prosperous.

That’s a silver lining to set against the banking hit, eh?

The EU Referendum legislation of 2015 called for a government research report to be produced and published in Parliament ahead of the actual referendum. This report called “Alternatives to membership:

possible models for the United Kingdom outside the European Union” reached the following conclusion:-

“The UK Government believes that no existing model outside the EU comes close to providing the same balance of advantages and influence that we get from the UK’s current status inside the EU.”

The majority of current Tory and Labour MP’s including the new prime-minister have either not read the report or promptly decide to forget it. The government’s cabinet is now going round in circles trying to reinvent the wheel in order to produce a “bespoke” plan that will cause no economic damage to the UK. The research report clearly tells them this isn’t possible. Parliament has descended into a state of utter farce with only the Lib/Dem Party, SNP and Green parties willing to pay any attention to the research report!

https://www.gov.uk/government/uploads/system/uploads/attachment_data/file/504604/Alternatives_to_membership_-_possible_models_for_the_UK_outside_the_EU.pdf

In any discussion of Brexit, there’s a need to draw a clear line between trade in goods and capital flows between Britain and the EU and other trading partners from the United States to India and Brazil.

For example, see this:

Here is where Brexit could have a beneficial effect on the average British standard of living, since EU trade rules for goods are not always beneficial to British manufacturers and importers (examples: the whopping ~50% EU tariff on Chinese solar panels, high tariffs for trade with India, etc.). In addition, if capital flows into and out of London are restricted (anti-neoliberalism), this lowers property prices in London since much of the price increase is due to foreign wealth seeking secure investments for their cash, much of it from shady sources (tax shelters as in the Panama Papers, drug cartel money, dictators looting their national banks, etc.).

That’s really the heart of the anti-neoliberalism argument: restrict capital flows to improve the health of nation-state economies and prevent economic manipulation by capital flight mechanisms. This is also why so many “free trade deals” of the past should be reclassifed as “free capital flow deals.”