By Wolf Richter, a San Francisco based executive, entrepreneur, start up specialist, and author, with extensive international work experience. Originally published at Wolf Street

And transactions in the apartment sector plunge.

After seven dizzying boom years, commercial real estate prices peaked in December 2016 and have since turned south. These values are collateral for nearly $4 trillion in loans, a good chunk from smaller banks. When the last bubble imploded after September 2007, prices plunged nearly 40%. The Fed has been pointing at the risks the new CRE price bubble poses for the banks. Among the sub-sectors, prices of apartment buildings, according to Green Street’s Property Price Index, were down 3% in May year-over-year.

And transaction volume of apartment buildings has plunged. Real Capital Analytics put the “story for the apartment sector” this way:

Activity in this sector, which was the largest and most liquid investment market for most of 2015 and 2016, declined in May and was lower than activity in the office sector. For the year to date, transaction volume for apartments is down 25% year-over-year.

There is another side to this equation – the most important: rents. Because they pay for the whole construct, including the loans.

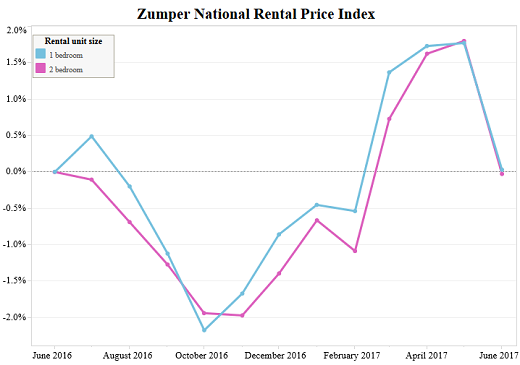

According to Zumper’s National Rent Report for June, rents in multifamily apartment buildings (single-family houses for rent are not included) spiraled into a surprising counter-seasonal drop in June.

“Summer is peak rental season, meaning it’s usually a difficult and expensive time to look for a new apartment,” said Zumper co-founder Taylor Glass-Moore. “However, renters this year are in luck, as median rents are dropping for both one and two bedrooms nationally.”

The chart below shows the monthly percentage change in median asking rents since June 2016. Note the seasonal surge in early spring – and then the sudden drop in June. That’s when the median asking rent, instead of rising, dropped 1.7% for one-bedroom apartments (blue line, $1,149) and 1.8% for two-bedroom apartments (red line, $1,367) — both where they’d been in June 2016.

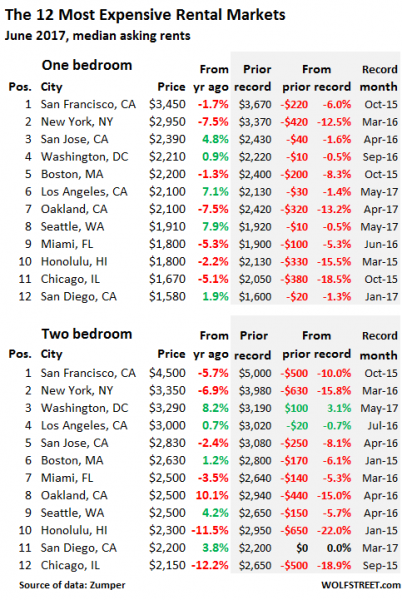

Rents fall in the most expensive markets

In San Francisco, the median asking rent for a one-bedroom apartment dropped 1.7% in June from a year ago to $3,450 and is down 6.0% from the peak in October 2015. For a two-bedroom, the median asking rent dropped 5.7% year-over-year to $4,500 and is down 10% from the peak in October 2015.

The last period of year-over-year declines in San Francisco ended in April 2010. This time, there is no Financial Crisis. There is however a “Housing Crisis,” where the middle class can no longer afford to move into a modest apartment. This has consequences. And the exodus has started.

In New York City, the median asking rent for a one-bedroom dropped 7.5% year-over-year to $2,950 and is down 12.5% from the peak in March 2016. For two-bedrooms, it dropped 6.9% and is down 15.8% from the peak.

In San Jose, median asking rent for a one-bedroom rose 4.8% year-over-year to $2,390 but is down 1.6% from the peak in April 2016. For a two-bedroom, it fell 2.4% year-over-year to $2,830 and is down 8.1% from the peak.

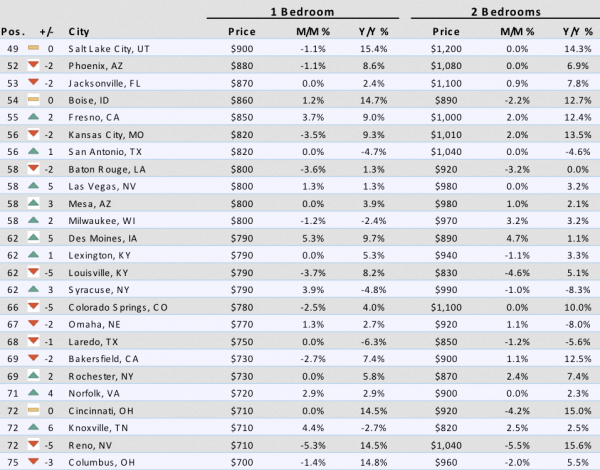

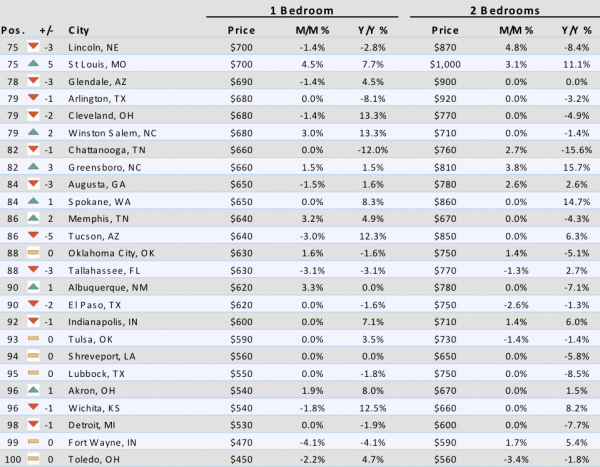

This table of the 12 most expensive large rental markets in the US shows median asking rents, their year-over-year changes, and (in the shaded areas) the prior record and the change since then:

Note the double-digit plunges from the peak in New York City, Oakland, Honolulu, and Chicago.

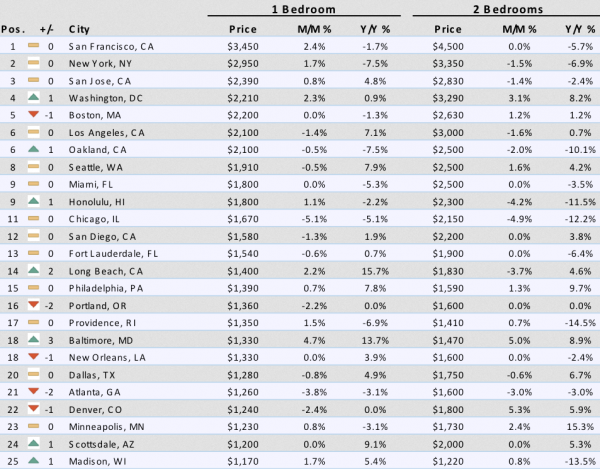

Asking rents do not include incentives, such as “1-month-free.” In San Francisco, a historic construction boom is flooding the rental market with high-end apartments and condos. But employment in May dropped to where it had been in July 2016, and the labor force dropped to where it had been in March 2016. Landlords are trying to fill their units, and incentives – a trick to keep asking rents high and make the market look better – have become common.

What gives? In some “mid-tier” rental markets, asking rents are soaring in the double digits, and in most other areas they’re rising by smaller amounts, though there are now some other markets where rents are heading down sharply, including Chattanooga, TN, where the median asking rent for a 1-BR dropped 12.0% and for a 2-BR 15.6%.

Here are some of the mid-tier markets with the large year-over-year rent increases:

- Nashville, TN (+15.0% and +12.9%);

- Sacramento, CA (+15.2% and +15.7%)

- Charlotte, NC (+15.3% and +11.2%)

- Houston, TX (+15.3% and +14.4%)

- Durham, NC (+15.5% and +12.0%)

Few workers receive those kind of pay increases. So these surging asking rents pressure consumers and cause them to cut back in other areas. And for the national numbers, the plunging rents in Honolulu and the soaring rents in Sacramento, and all the ups and downs everywhere else get neatly averaged out to 0% rent growth year-over-year. And that hasn’t happened since rents started soaring in the Fed-inspired asset-bubble euphoria that followed the Financial Crisis.

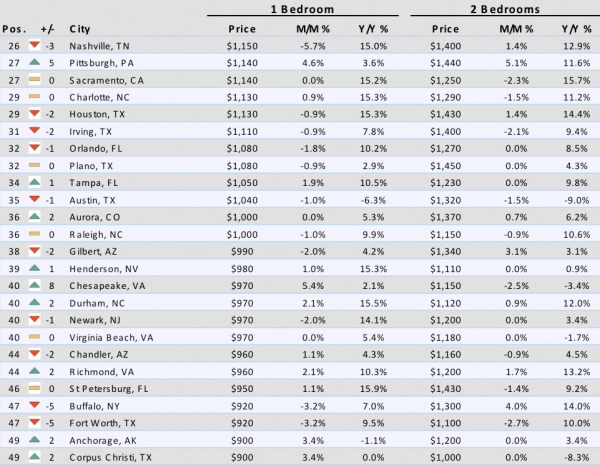

Below is Zumper’s complete list of the top 100 most expensive rental markets and price movements. Check out your city (click on image to enlarge).

Commercial and residential real estate price bubbles can choke the economy, the consequences of which are now visible in San Francisco. Read… San Francisco Bay Area Sheds Jobs and Workers

To be San Francisco’s Cassandra for the day, the landlords and real estate interests have been carrying out a greed driven heart transplant (funded by insane VC and their unicorn progeny) while forgetting the need for a healthy replacement organ. Perhaps some road kill will be propinquitous for the “surgeons”.

Nice word, duck1, and nice metaphor.

I don’t know about the other cities, but in NYC and SF, there has been a ton of new apartments built in the last couple of years, which has led to the price fall in both markets. Pretty odd Wolf does not mention that.

Wolf does mention “In San Francisco, a historic construction boom is flooding the rental market…”

Huge amount of rental supply has come online in downtown Brooklyn in the form of high rises and there’s several more projects coming. I’m in one. It’s pretty much all dual income couples without kids. There has been a lot of turnover as people finish up their first year in the building and balk at paying the “gross rent” without the months free they got at move in. Admittedly the quality of life and convenience of these buildings is great, but the rents are unsustainable if you plan to have children.

Anecdotal but the “animal spirits” I felt in NYC around 2014-2016 with the millennial wave here are gone. Manhattan is definitely a stagnant tourist playground. But many people have left and plan to leave.

Personally I have no interest in making the massive infrastructure spending needed here, as well as the pension liabilities that will be faced by NYC, NJ, et al, my problem by buying property and dropping anchor here. Property taxes and income taxes are already ridiculous, it’s higher than “socialist” countries where you actually see benefit!

I look around at the professionals I know (early thirties crowd) in a lot of sectors, as well as regular people and I don’t see prosperity. A lot of highly educated people out of work or slow at work and maybe holding on due to a spouse. There’s really a quiet stagnation in the US that the media doesn’t cover because The Stock Market.

What’s the vacancy rate like in those areas?

I have heard NIMBYism is partly to blame in the SF Bay Area, but not as sure about the situation in NYC.

Boston has been filled with cranes building rentals and condos that last few years, and they are still going up. It’s all been “luxury housing” for rents of 3000-4000 for a one-bedroom. It hasn’t taken a genius to see the crash coming…

Twenty years ago I looked up at the towers rising in Manhattan and prayed for the day the rich scum and their dirty money vaults in the sky would leave and make room for the people who work in NY to live.

Upper Broadway was plastered with flyers begging to pay $1000 to share an apartment with five other rent-croppers.

Now I walk around Chicago and wonder where the money is coming from to pay all these rents.

Between housing, health/insurance, energy and crapification, 9 of 10 people in the Richest Country The World Has Ever Known don’t have two nickels to rub together.

Now I walk around Chicago and wonder where the money is coming from to pay all these rents.

And mortgages.. Reasonably desirable condo prices have skyrocketed in recent years

In Seattle, rents have been going up DAILY.

My friend’s daughter was looking for a studio. She looked on a Friday at a place for 1800. She went back to get it on Monday, it had gone up from 1800 to 1950.

It still is insane here.

Lots of long-term Seattle residents moving away. Can no longer afford it.

Truly amazing to see Madison, outpost in the middle of nowhere (I can’t even get family to visit!), ringing in at #25, behind only Chicago, Denver and Mpls in all of flyover.

…probably related to UofW, Madison.

I like Madison and surrounding areas. Great bike riding territory. And my coffee bean supplier is there! http://www.burmancoffee.com

In Charlotte part of the reason rents might be going up is because almost all of the new units going on the market are decidedly upscale. This isn’t to say there isn’t a shortage of housing affordable to regular people there, I’ve heard people complaining about it.

There have been several new complexes built downtown, right near everything, listing well above that average. I also noticed a new set of units that went up near UNCC. I haven’t been inside but from the outside they look far nicer than anything that was there when I attended in the early 00’s.

Dont’t I wish – south SF Bay, just got our annual ren-jacking notice to the tune of +7%. Please can we get on with the next global fin-crisis, pretty please? 2008-9 was the last time rents in my area dropped.

I am sorry guys but you are missing the real reason here. Santa Clara has been one of the worst offenders of wanting only office/commercial space built because they could get tax dollars for it and offer no services (schools, parks etc….). It will hurt them in the long run or there will be condo conversions…