By Wolf Richter, a San Francisco based executive, entrepreneur, start up specialist, and author, with extensive international work experience. Cross posted from Testosterone Pit.

When Blackstone’s global head of private equity, Joseph Baratta, said Thursday night that “we” were “in the middle of an epic credit bubble,” the likes of which he hadn’t seen in his career, he knew whereof he spoke.

Junk bond issuance hit an all-time record of $47.6 billion in September, edging out the prior record, set in September last year, of $46.8 billion, according to S&P Capital IQ/LCD. Year to date, issuance amounted to $255 billion, blowing away last year’s volume for this period of $243 billion. The year 2012, already in a bubble, set an all-time record with $346 billion. This year, if the Fed keeps the money flowing and forgets about that taper business, junk bond issuance will beat that record handily.

Junk-bond funds got clobbered in July and August as retail investors briefly opened their eyes and realized what they had on their hands and fled, and they went looking for yield elsewhere, but there was still no yield in reasonable places, and so they held their noses and picked up these reeking junk-bond funds again. Cash inflow doubled over the last week to $3.1 billion, the most in ten weeks.

These retail investors were fired up by the Fed’s refusal to taper even a little bit, giving rise to the hope that it might actually never taper, that this is truly QE Infinity, Wall Street’s wet dream come true – on the theory that the Fed is mortally afraid that any taper would blow over the sky-high financial-markets house of cards it has constructed over the last five years. And the retail cash returned to these junk-bond funds and just about refilled the hole that had been dug during the summer.

“The cost of a high-yield bond on an absolute coupon basis is as low as it’s ever been,” explained Baratta, king of Blackstone’s $53 billion in private equity assets. Even the riskiest companies are selling the riskiest bonds at low yields. The September frenzy hit the upper end too and set a new record: companies sold $145.7 billion in investment-grade bonds in the US. And Baratta complained that valuations “relative to the growth prospects are out of whack right now.”

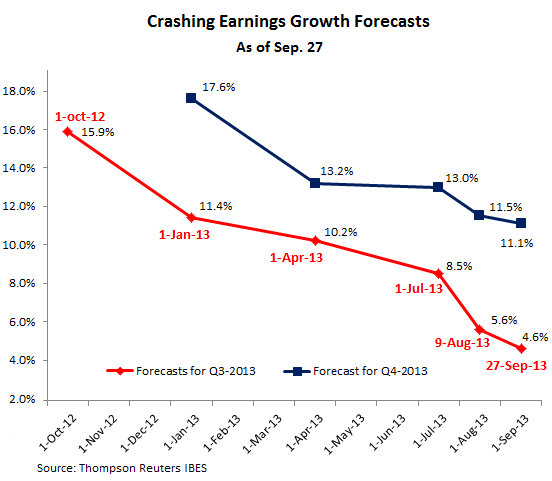

These “growth prospects” look grim, with corporate revenues barely keeping up with inflation, and with earnings growth, despite all-out financial engineering, getting decimated. On October 1 last year, earnings estimates for the third quarter 2013 still saw a growth of 15.9%. As of Friday, estimated earnings growth had plunged to 4.6%, dropping 20 basis points per week in August and 10 basis points per week in September. And they may still be too optimistic.

Meanwhile, earnings growth estimates for the fourth quarter have barely budged since August and remain at the deliriously lofty level of 11.1%, pulled up largely by financials, whose earnings growth is still pegged at a breath-taking 25.7%, based on the assumption that the Fed will continue to feed them.

But financials are having some, let’s say, issues. The five biggest banks alone face a $1 billion cut in earnings from just the past month, based on a big decline in fixed-income trading revenues – with our special friend, JPMorgan, eating more than half of it. There had been “hopes of a final trading flurry in the last few weeks of the quarter,” the FT observed, but those hopes have now been squashed.

Then there is the death of the mortgage refi bubble that has been hammering banks, with number one mortgage lender Wells Fargo suffering the most. Four banks have so far announced 7,000 layoffs in their mortgage divisions. JPMorgan confessed that it would lose money in its mortgage business in the second half. On top of that, JPMorgan is contemplating $11 billion in legal settlements for its various mortgage scams. And earnings at financials are still expected to grow 25.7% in the fourth quarter?

“Out of whack” is what Baratta called this phenomenon of sky-high valuations in relationship to grim growth prospects.

Earnings estimates have been slow in coming down. And the stock market, supposedly forward looking and focused on corporate revenues and earnings, has been completely blind to them. It follows the mantra that fundamentals no longer matter. All that matters is the Fed. A shift that has become the Fed’s most glorious accomplishment. And the Fed continues to feed Wall Street with $85 billion a month.

Yet in this glorious environment where there is no gravity for stocks and even junk bonds, the smart money is selling hand over fist, unloading whatever they can, however they can. Record junk bond issuance is just one aspect. Another aspect: IPOs. They have gone haywire.

There were 23 IPOs in May, 20 in June, 17 in July (Independence Day put a damper on it), 19 in August, and 21 in September. But last week alone, there were 12 IPOs – more than two per day! Generally, IPOs are scheduled apart to avoid overloading the market. But now the smart money is scrambling to issue paper while it still can and stuff it into the portfolios of retail investors at current “out of whack” valuations, stocks and bonds alike, before the Fed turns off its crazy money spigot, and before investors will finally open their eyes to the grim earnings reality.

Why would anyone buy this crap? No, not the clothes in J.C. Penny’s stores – which practically no one is buying – but the shares it sold on Friday. It desperately needed to raise capital because it’s bleeding cash and won’t be around much longer without lots of new cash to bleed. So it did. At a horrendous expense, overnight, to existing stockholders, and at a steep loss for the new ones.

It looks like one of the consequences of QE has been to drive investors into increasingly high-risk investments in quest of yield. I don’t see how this can end well.

Our current era seems to resemble the 1890 to 1914 era in many ways, poised as it was on the precipice of three decades of world-wide war and depression. When the rentier’s quest for yield blows up in their faces, the quest for scapegoats will begin.

As Jacques Barzun asks in From Dawn to Decadence,

Right. And it is still just as terrifying to know that history dictates, proves, that we are all totally nuts.

The market is forward looking in pricing positive or negative delusions.

I regularly look at page 21 of this report:

http://research.stlouisfed.org/publications/net/

The market has a hard time noticing drops in earnings. It usually takes a few quarters of dropping corporate profits to GDP before the market really reacts.

Right now, the ratio is still at an all-time high so we probably still have a few more quarters of optimistic delusions… but the debt market is usually faster on the trigger.

Functionally, the Fed believes that the only cure for a burst bubble is a bigger bubble — so this comes as no suprise. They appear to be wilfully blind that, in an era of plutocratic concentration of wealth, the old supply-side nostrums don’t work.

The economic model is broken, and until we have a large redistribution of wealth in America, it will stay broken. The bi-partisan focus on ‘growth’ is a red herring, a distraction, so that we don’t have a conversation about the real problem.

But they don’t beleave in bubbles. Any more than they beleave in evolution, global warming, or that the poor can only afford to take weekend trips to the Bahamas.

…”before the Fed turns off its crazy money spigot”

“if the Fed keeps the money flowing and forgets about that taper business”

“And the Fed continues to feed Wall Street with $85 billion a month.”

I’m still confused about QE. In a recent podcast with Stephanie Kelton and Warren Mosler (at neweconomicperspectives.org), Mosler says, IIRC “..but QE doesn’t flood the market with money.” He describes QE as (correct me if I’m wrong) just shifting assets from the banks’ savings account at the Fed, to their checking account at the Fed (although these accounts are called Treasuries and Reserves, they amount to savings/checking accounts.)

In the Randy Wray podcast (also at newecon), he says if QE ended, there would be a brief turmoil in the markets, and then investors would realize it didn’t really make any difference.

Mosler also says that far from increasing the money supply, QE actually *removes* money from the economy, by turning interest-bearing assets into non-interest-bearing assets. And just because they’re more liquid, doesn’t mean people will run out and spend them into the economy. (One question I have on this aspect of it: what mechanism lets the Fed convert other parties’ bonds to reserves, is it voluntary or involuntary for those bond-holders?)

I’m still looking for a really lucid source that describes in detail what’s going on with QE. Mosler is great but I can’t find an article by him drilling down into some of the details that are still unclear to me.

But posts like this throw me off, given Mosler’s seeming authority and expertise. Is Wolf Richter just speaking in some shorthand, or does he not know what he’s talking about wrt QE?

For example:

The Fed decides to buys MBS… Pimco might be the seller… then Pimco ends up with cash which permits it to buy something else… government bonds, newer MBS, high yield, etc? So part of this money ends up in the economy and another part moves around across pension plans.

With low velocity, I would say that a lot of this money is just flowing up into the large DB plans.

Right, but because that MBS that once belonged to Pimco now belongs to the Fed, that cash flows attached to the MBS that would have gone to Pimco go to the Fed instead. So over time, about as much money is drained out of the private sector to the Fed as was injected into the private sector by the Fed’s purchase.

Not really because the new security that replaces the MBS has coupons also. Furthermore, if those MBS were backed by delinquent mortgages, no money would have been flowing anyway. Also, because the pension plans got propped up, pension benefit cheques are still being sent to retirees.

However, one thing is for sure, money is getting parked…

instead of having dollars move hand to hand, government must generate more dollars of debt to generate GDP.

But the bottom line is that capitalism, not just our brand of gangster capitalism, is dead in the water. Capitalism relies on skimming from somewhere – excessive growth; trashing the environment; screwing labor, etc. Nothing is going to revive it now. We are “in crisis” because the old economy is useless and we will be here for a long time, years, maybe decades. So what’s a Fed Head to do? Just keep the money circulating as much as possible. Life support. It is, however, a life support system that left out all but the very rich. So it will not save them either. Poetic justice. And Congress? Forget it.

The situation resembles that editorial cartoon back in the late 1920s showing an endless belt with money flowing from Germany to France as reparations, from France to the US as repayment of war debts, then from the US back to Germany as loans.

Something in it for everybody (snicker)!

“I’m still confused about QE.”

You’re not alone.

I’ve read articles by people explaining in incomprehensible (to me) detail, either why it’s great, or why it’s terrible.

and none of them seem to be able to write an explanation without using words and acronyms that I suspect many people don’t understand.

They’re talking to each other I suppose.

my simple question is, who is getting the credits, the money, and what are they using it for?

Where’s it ending up? Is it going into the stock market?

is there a simple, layman’s explanation for this? without any insider jargon?

“The Fed Winged It”

QE is good if it props up confidence and stops the world from imploding (which it did) but is bad if it generates a drop in confidence by squeezing out industry (which it is increasingly doing).

Go look at the balance sheets of the large consumer discretionary stocks over the last 1-2 years, compare it to the stock prices and tell me that their activity inspires confidence in future economic growth.

DIY QE education via “Quantitative Easing Explained” with 5.6 million views since 11/2010!

http://www.youtube.com/watch?v=PTUY16CkS-k

And “Quantitative Easity Revisited”

http://www.youtube.com/watch?v=oGIvw7T0GPI

I wonder if NC readers find anything false in these.

thanks.

“I’m still confused about QE. In a recent podcast with Stephanie Kelton and Warren Mosler (at neweconomicperspectives.org), Mosler says, IIRC “..but QE doesn’t flood the market with money.” He describes QE as (correct me if I’m wrong) just shifting assets from the banks’ savings account at the Fed, to their checking account at the Fed (although these accounts are called Treasuries and Reserves, they amount to savings/checking accounts.)”

Ha ha! That’s a good one. The guy probably even believes it too.

Creating money is actually quite easy. *Poof* I just created a million Dubies. Want to see me do it again? *Poof*, another million Dubies. But the trick is getting some one to take my Dubies in trade for goods and services. In fact, my Dubies can’t even be called a currency until they are accepted as a medium of exchange. I haven’t actually made any Dubies, until I spend them into existence.

But there is another quirk here. If I was to accept a Dubie in exchange for something, as I was the originator of the Dubie, then the Dubie poofs into the same nothingness from whence it came. And this would only make sense, if I can create Dubis at will, than by definition a Dubie must have zero value to me. So every Dubie I take back, regardless of what I do with it later, effectively removes it from the economy.

Thus the amount of currency in circulation becomes a balance equation; if I spend more Dubies than I accept in trade, then the supply of Dubies is growing in the broader economy.

For the good old US of A, the one who poof’s US dollars into existence isn’t the US Treasury as you might think, but the Federal Reserve. This is why the government has this national debt because they have to schlep it like the rest of us.

So when the Fed “buys” any thing; from toilet paper for the office to trillions in mortgage backed securities, it is buying it with dollars that were poofed into existence. Regardless of the mumbo-jumbo they try to peddle about over-all balance sheets.

That gives you the fed’s side of the story. But with Quantitative Easing, there is the other side of the store that is told by the too-big-too-fail-banks.

The Fed’s theory about “the liquidity crises” is that the banks had a ton of assets that had temporally been devalued in price, thanks to the “great recession”. (Snic- oh you just got to love that spin.) But once the recovery takes hold, and the economy is always in recovery, than all of those mortgage backed securities will snap back in value, and even start turning a profit again.

So to tide things over, the Federal Reserve basically buys bank-generated assets, such as mortgage backed securities, and holds them for later. When things recover, the Fed will start selling the assets back to the bank. So they aren’t running those printing presses to cause the next Weimar Hyperinflation… oh no this is only temporary. See how clever they are?

Of course, now the 2B2F banks have an incentive to create worthless paper assets, knowing full well the Fed will buy them – no questions asked. And the fed doesn’t risk any thing because it’s the one that created to dollars in the first place. Indeed, they seem to have a preference for the junk as they are the only ones who will buy it. The Federal Reserve has basically become the consumer of last resort. The banks then have all that brand new free cash to play with which they can used to go gambling in the great global casino called the stock market. Or better yet, they can use those new dollars to create even MORE worthless assets with which to sell to the fed.

That is basically what is happening. The rest of the mumbo-jumbo you hear is just gibberish to try and obfuscate and conceal that this is actually happening, or more likely in an effort to puff themselves up and make themselves look… well…competent. All though I suspect they set there self delusionary image a lot higher than that. It’s good to have goals I suppose.

So where is the hyper-inflation you may be asking? Well, it turns out that you don’t create hyper-inflation by simply flooding the market with a currency you just printed. Why this is… is complicated. It’s also some what off topic.

But there is another explanation. As I said before, a currency has to be spent into existence. But the fed isn’t actually spending it, but rather simply making transfers in exchange for fiscal assets that are as equally made up. The 2b2fb take their new cash and “invest” them into other paper assets, which are also fabricated from out of thin air, and which value expands only because other 2b2fb are taking their new Fed cash and trying to buy the same paper assets.

Because the banks are basically creating assets to be sold to the fed, the 2b2fb have basically become a defacto extension of the fed. And like the fed, every dollar the 2b2fb take in – effectively disappears from the economy, regardless of what their balance sheet shows or how they chose to invest it in the stock market or other speculative bubbles.

Despite all the talk of Taper, the reality is that the fed CAN’T stop quantitative easing or the whole thing will simply implodes. But nor is all of the new fed money contributing to the economy because its all going to making more money through financing.

“Mosler also says that far from increasing the money supply, QE actually *removes* money from the economy, by turning interest-bearing assets into non-interest-bearing assets. And just because they’re more liquid, doesn’t mean people will run out and spend them into the economy. (One question I have on this aspect of it: what mechanism lets the Fed convert other parties’ bonds to reserves, is it voluntary or involuntary for those bond-holders?)”

Well Mosler is not entirely wrong, but not for the reason he states. (FYI: Interest baring assets do not add currency to the economy.) Remember that balance sheet equation? If the fed spends more money than it takes in, then it is expanding the money supply. But if the 2b2fb have become extensions of the Federal Reserve because they in effect create money out of thin air, then they also have the consequence of destroying the money that they take onto their balance sheets. It then becomes a question of weather the 2b2fbs are spending more money then they are collecting.

As for the last part of your question… I have…. no clue.

I propose a doobie-based exchange economy, as doobies are always in HIGH in high demand. It’s a growth market!

wom wom

Any better ideas?

“Despite all the talk of Taper, the reality is that the fed CAN’T stop quantitative easing or the whole thing will simply implodes.”

Of course, that’s the best reason for stopping it. Do it now, or do it later, with later being much worse.

The debt situation is worse now than it was in 2008. So if the Fed did not let stuff default then, why would it start now?

IMO, the Fed taper will depend on the ROW crumbling first.

And the stock market, supposedly forward looking and focused on corporate revenues and earnings, has been completely blind to them. It follows the mantra that fundamentals no longer matter. All that matters is the Fed. A shift that has become the Fed’s most glorious accomplishment. And the Fed continues to feed Wall Street with $85 billion a month.

Since 2008, Obama’s policies and the Fed’s policies have succeeded in reinflating the financial industry at the cost of an enormous amount of debt. The status quo has been preserved, but the real economy has been cannibalized and not restored. There have been no reforms, ensuring a repeat of the 2008 meltdown at an even greater scale. Wall St. is more out-of-control than ever.

Debt will allow you to ignore the fundamentals and put off the reckoning, but only for so long. That time is running out, and the rats are cashing in and jumping ship:

But now the smart money is scrambling to issue paper … before the Fed turns off its crazy money spigot

This will all end in tears.

Something about rumor control a la Jim Rickards and any next event requiring an IMF SDR thingy… ouch.

Many seem to think that QE was for the elite only. But it has also been for the benefit of the top 10-15%. Those with a pension.

90% of DBs are something like 30% underfunded. Without QE, I can imagine how many write-offs they would have had to do. How even more underfunded plans would have been.

Then, some propose having the government print, print, print without issuing debt… makes one wonder what these underfunded plans would buy! More corporate bonds based on easy printing? If we chose to go this route, chances are all plans would have to go pay-as-you-go. That would mean HUGE upheaval in the markets. The people would hate the elite even more… revolutions often start when the top 10-15% get angry but these QEs have been neutering them.

The benefit of QE to pension funds depends on the asset mix. Equities have recovered, but fixed income yields have evaporated. So the Fed is forcing pension funds into a riskier asset mix (equities, alternative investments) as opposed to traditional I-grade corporates and treasuries.

I suggest QE is merely kicking the can wrt to pension funds, because what QE has done is to accelerate a decade or more of equity gains into the last couple of years. The hope was that the economy would attain “escape velocity” and justify the multiples and historically high profit margins.

As Ben Inker at GMO has written, this hope is justified only if the majority of American willingly embrace serfdom.

Yup. But they still got another good 4-5 years of bond gains and bailouts and QE propped up equities. It has probably given most DB pensioner n extra 5-10 years of benefits.

With no bailouts and QE, there would have been write-offs in bonds and equities would not have moved up as much. DB plans would have had to cut.

The reality is the leaders do not want to be the ones telling the top 10-15% that they are broke. They will do whatever it takes to just let it happen through what appears like market forces. That’s what is great with being able to blame a central bank, it’s impersonal.

Also, they probably intuitively know that the real troble will come when those DBs go bust.

Yes, good points. I pretty much agree.

Credit bubbles are marked by the use of a ton of leverage in the corporate sector, usually in the form of a wave of mega-LBOs. In the late 1990s and in 2005-2006, there was a new giant LBO announcement splashed across the front page of the Wall Street Journal practically every other day. That was a tell-tale sign of a credit bubble, a sign that was followed by a collapse of the credit markets in 2001-2002 and in 2008-2009. The absence of mega-LBOs in the current market suggests we are not in a credit bubble.

But I can see why this guy Baratta is complaining. In a “normal” environment, he would take a company private at a low multiple to EBITDA, use cost-cutting and fast economic growth to grow EBITDA, and then sell the company back to the public at a higher multiple. Boo hoo, multiples aren’t low enough to ensure he will double his money at every one else’s expense. Too bad.

Someone else eating is lunch. Boo-hoo!

However, when these guys complain, take notice.

I like the idea of there being a simple answer to QE or the world financial system. Let’s face it, economics must be simple or the buffoons we elect wouldn’t be able to understand it.

In principle QE sounds like it matters where you stack your money, almost as if moving it around the vault has some kind of ‘astrological effect’ on the real economy. Anyone who believes this should send their life savings to ACOPONZI (Cayman Offshore Secure Holdings) Inc before Jupiter next blinks. Send with complete power of attorney – we don’t want regulatory red tape getting in the way of profits …

In ACOPONZI I’d no doubt start by lying to you – triple your money in months and such. QE started with a lie – it was to boost loans to the real economy and so on. I’m ex-cop and saw hundreds of scams as ‘simple’ as QE. A good one to look at now is the rip-off of US municipals – http://www.rollingstone.com/politics/news/the-scam-wall-street-learned-from-the-mafia-20120620

I generally found juries immune to fraudsters and their lawyers and this holds in the US municipals case. I think we need to ‘go cop’ to see that QE is really just a simple scam. As in the case Tabbi reports, we the public are the losers and a small few have been facilitated in looting. We need to boil it down to Cui Bono.

The banking system clearly could not be supported by different astrological positioning of money. In the Carrolo trial wiretaps clearly demonstrate the simple scam.

I guess QE somehow facilitates drawing fresh money in the Ponzi and the hiding of losses in an 888 account. The defence is that this is for the good of us all because otherwise the sky will fall. What we need to understand this is not the espoused theory of QE but the money trail and transaction transcripts of its theory-in-practice.

Our municipalities had plenty of well-qualified and well-paid lawyers and accountants, but were ripped off by a simple scam. The Fed and BoE have lots of well-qualified people too. QE will turn out to be a simple scam. We don’t need complex explanations, but do need evidence of the transactions it has allowed. Anyone really want to bet on who is holding the debt parcel?

Re earnings growth: Kalecki, bitchez!!1!