A lawsuit filed against Deutsche Bank by two former senior wealth management employees demonstrates a basic problem: even rich people find it difficult to get people to manage their money who won’t take advantage of them. Here, the former employees allege that Deutshce Bank repeatedly pressed account managers to violate their fiduciary duties and stuff discretionary accounts with risky products like start-up hedge funds, even when the customer was clear it wanted only low-risk products.

We’ll discuss lawsuit in some detail for it illustrates a both perverse and troubling trend, that the idea of “fiduciary duty” is becoming a dead letter in the US. Many types of financial relationship, and this was one, impose a fiduciary duty on the service provider. Under the law, a fiduciary duty is the highest standard of care; the professional is supposed to put his client’s interest before his own. Here’s one definition: An individual in whom another has placed the utmost trust and confidence to manage and protect property or money.

Now the increasing difficulties that the wealthy have in hiring honest help may seem a remote concern to Naked Capitalism readers. But this issue exposes a fundamental flaw of the entire neoliberal project: that markets are an efficient and fair way of allocating resources, so the more use of market mechanisms to address social issues, like how to provide for retirement or supply health care, the better. But if the rich, who should be hugely attractive customers with plenty of bargaining power, are abused despite having taken proper precautions, how can the rest of us expect to do any better?

Younger readers, who’ve grown up with predatory capitalism, may think that the notion that fiduciary duty was ever taken seriously is a hoary old myth. Let me give some examples that show how much the world has changed. When I started out in business, financial firms were far more solicitous about client interests even when they were not fiduciaries. For instance, standard fee agreements in mergers and acquisitions indemnify the banker for his actions under the agreement except for cases of bad faith and gross negligence. And M&A professionals are the pit bulls of finance: tell them to get a deal done, and they won’t let go. Yet back in the stone ages of the early 1980s, when Goldman was still a respected institution, I was the junior team member on one client account, a very lucrative, very loyal, and not terribly sophisticated Fortune 100 company. It was hungry to do a medium sized acquisition that on paper met its strategic targets very well. The merger & acquisition department members were tearing their hair because it was a terrible deal: grossly overpriced and the financial statements had red flags on top of that. They felt they had to (and they did) talk the client out of the deal without looking like they were dissing the client’s judgment. The fees they might earn weren’t worth the potential damage to the relationship. Mind you, this was considered to be obvious commercial good sense back then. It had nothing to do with virtue or legal duties.

There are numerous instances where a professional has a fiduciary duty relative to his customer. The most stringent are when the agent is given a great deal of latitude in handling assets. Think, say, of wealthy real estate magnate who sets up a trust to manage his estate on behalf of his schizophrenic son (the building in which I live is in a trust like that), or the classic widow or orphan, who inherits some property and that serves as their source of livelihood and needs to be managed conservatively. Another type is someone who is too busy to manage his assets or believes a professional has more expertise and will do a better job; think of entrepreneurs who prefer to focus on running their business and hire a specialist to manage their retirement accounts.

It’s becoming increasingly apparent that even the rich can’t protect themselves. We’ve mentioned the case of Len Blavatnik, now number 39 on Forbes’ international wealth ranking (Full disclosure: Blavatnik was a client of mine when he was much less rich than he is now). Blavatnik had about $1 billion in cash across all of his operating companies, and thought it could be managed better. His staff went through a disciplined process of selecting a money manager and chose JP Morgan. They wanted only to beat Treasuries by 15 basis points, which before ZIRP was not terribly ambitious. Their agreement with JP Morgan stressed the need for safety and liquidity, and also restricted how much JP Morgan could put in various buckets, like real estate related assets versus loans.

The crisis started and in summer 2007 JP Morgan started using Blavatnik as a stuffee and dumped lots of drecky short-term paper into his account. He lost $100 million on a $1 billion cash account. He sued and recovered roughly half.

Consider: JP Morgan decided to trash its relationship with its second largest private client in North America, one who not only has lots of assets to manage, but regularly buys and sells companies, meaning he generates lots of deal fees and financing income. And if this is the sort of behavior that financial firms engage in at the top of the food chain, imagine what the rest of us can expect.

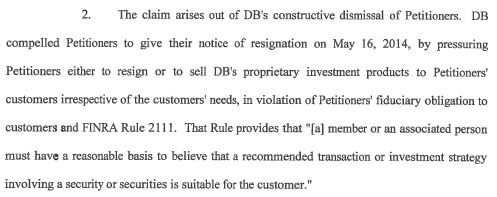

Now to the Deutsche Bank case. Benjamin Pace and Larry Weissman, both former members of Deutsche Bank’s wealth management unit, are suing to have the bank’s non-solicitation policy deemed unenforceable. The plaintiffs were both long-standing Deutsche Bank employees. Pace had been Deutsche’s Chief Investment Officer for wealth management products in the Americas for a decade. Weissman was head of Portfolio Consulting and was Pace’s direct report. I’ve embedded their short and readable filing at the end of the post. This is the guts of their claim:

Both men managed the Discretionary Portfolio Management group, which solicited and managed funds on behalf of high and ultra high net worth individuals. In the overwhelming majority of cases, the clients give Deutsche discretionary authority, meaning they can buy and sell investments without conferring with the customer. That degree of discretion is what produces the fiduciary duty.

The investors were told that Deutsche had an “open architecture” platform, which meant that account manager could choose the products that were the best customer fit, rather than best for Deutsche Bank. But the group was integrated with other asset management business into a new division a few years back, and was increasingly pressured to sell in-house products that were inappropriate for the Portfolio Management (PM) accounts. The filing stresses that many of the PM customers either did not want alternative assets at all or only wanted a limited portion allocated to them, yet Pace and Weissman were pushed to make significant buys of these risky strategies irrespective of suitability or the clearly stated objectives of the account owner.

Some of the dodgy products that the suit alleges Pace and Weissman were pressured to put into client accounts included:

A seed hedge fund. Note that fund managers often incubate lots of funds, and the ones that turn out to have good records are then marketed more broadly. Not only were customers exposed to losses from a potentially losing manager, but even if the fund merely had mediocre performance and was wound up, investors would eat the expenses of the failed fund as well as the cost of liquidating current investments to buy into the fund and then re-establish positions when they exited. Even worse, this particular fund had not even gone through the normal “New Product Approval Process” and internal compliance had not signed off on offering it to PM customers.

A private equity fund by Japan’s Softbank. The PMs were told to sell it not because it was any good but because Anshu Jain, Deutsche’s Co-CEO, was good buddies with the head of Softbank.

Another “seed” fund, this for European equities.

A proprietary private equity fund (Secondary Opportunities Private Equity Fund III) where Pace says he was hectored often for not doing enough to fund it.

Adding various proprietary products to Deutsche model portfolios, which would have led to them being sold into accounts, even though the products did not fit allocation requirements and inclusion of one, a Japanese fund, would have generated adverse tax outcomes.

The suit also describes a series of organizational changes that had taken place and were underway which are depicted as intended to pressure the PM staff to act more like brokers than fiduciaries.

The US seems to be doing a wonderful job of creating not just failed states but failed markets. In wealth management, the big risk used to be too much sleepiness, that overly-risk averse account managers sat in wood-paneled offices and were better at running errands for rich customers than managing their money. But in those days, they knew their limits and stayed with simple products. And truth be told, the most important rule of money management is not to lose principal, so at least they kept their eye on the biggest target.

The Brave New World of modern portfolio theory was supposed to produce a more scientific approach, but in fact, it underestimates market risk in several ways, thus leading customers to take on too much in the way of risky products. It also allows salesmen to bamboozle customers with their supposedly superior knowledge and intimidating jargon. Even so, the industry didn’t have to wind with widespread looting particularly since Pace’s and Weissman’s strenuous resistance of pressure to stuff their accounts shows that even a lot of well-paid Wall Street professionals want to do right by their customers even when their organizations don’t.

Too much of the finance business has become a classic lemon market. And if George Akerlof is right, the end result is that as bad drives out good, more and more customers steer clear of those markets altogether. Financiers are confident that they are invaluable, but we’ve had successful economies with far smaller banking and investment industries. So perversely, if regulation doesn’t reverse financial services industry hypertrophy, the fraud and grifting eventually will.

Benjamin Pace and Larry Weissman v. Deutsche Bank 05-28-2014

The TBTF I’m personally aquatinted with is winding down its Trust division (this process is rather drawn out as you can’t just dismantle a Trust and even transferring it to another Trustee is convoluted and potentially incurs legal risks to the party trying to offload its legacy responsibility; nevertheless, the Trust division is effectively closed to new business and is under a standing order to wind itself down).

Why ? Because the TBTF cannot ensure that culturally, managerially or ethically it is fit to operate with a fiduciary duty. It knows that, eventually, someone somewhere will not be able to fulfil its responsibilities as a Trustee. It’s not a question of pricing power or profitability (both of which are actually quite healthy). It recognises that it has lost (forever?) the capability.

Yes, it’s small comfort to us little people (and actually, you don’t need to necessarily have megabuck assets, theses days a £5M to 10M trust fund might only generate a smidge above average income if it has to support a minor from “cradle to grave”) that scamming is an equal opportunity crime.

I was going to write it in comment to the PE screwing its investors – there it’s a question how much LPs really care, because again, they don’t play with their own money.

Fiducary duties are something that precious few investor advisers/managers put in the first (or any top) place.

With rich, I’d say caveat emptor, but with the rest, I long believe that a) investment advisers should be banned (financial advisors, i.e. someone who helps you to do your budget, find the best mortgage or a saving account are ok.. ) as it’s akin to card reasing. b) the only active management investment schemes available to the wider public (MiFID’s retail investors) should be where the scheme’s managers 1) have at least 25% of gross wealth in 2) are not allowed to roll fees into the fund pre-tax 3) have a lock-down period on taking the money out if they retire

In other words, they would be out there not to make money for (or rather, from you), but are out there to make money for themselves, and for a share are willing to take you along.

The problem is that if all the fiduciary duties were respected, there would be millions of people quitting and not being able to find another job… I think armbrit explained it as crapification yesterday

I got out of my industry because of what I perceived as major conflicts of interest that got me in arguments a little to often for my own sanity. But I was living way below my means and could afford to protest, most of those around me would not be able to quit because of their huge financial obligations.

When you’ve got a 1B portfolio and you expect to make more than inflation or gross GDP, you are contributing to the growth in inequality… unless you are only investing in businesses that increase production and jobs and don’t somehow try to cheat or game the system.

However, most of the rich today are looking for a free lunch… you reap what you sow.

When the rich get a good dose of their medicine, maybe we’ll start to see some change.

One can only hope. Some posit (I really don’t know) that the main reason that Bernie Madoff got busted is not that he ripped off middle class people, but that he ripped off very very rich people. Plus he made a good early scapegoat.

I won’t hold my breath waiting for improvements. The wealthy usually manage to find ways to take care of themselves without having to follow any rules or laws. Time will tell.

I agree about Madoff. Just today, in a comment to the article A Warm Welcome to Our New Private Equity Readers, I posted this link showing that some very rich companies and individuals were robbed by Madoff:

http://en.wikipedia.org/wiki/Madoff_investment_scandal#Largest_stake-holders

The Snake has begun eating its own tail and is working its way up.

Yves has noted how fiercely the brokerage industry has fought the “fiduciary” designation. I would wager that 99% of customers assume their broker has a fiduciary duty to them when, in fact, they do not.

My very Right Wing friend, who is a very good person, truly believes that companies would not do the things they do (ie. major banks laundering billions in drug and terrorism money, Frackers poisoning water supplies) because of the reputational risk alone. He also believes that those who rise to the top are no different than the population at large in terms of criminal proclivities.

I used to believe a lot of this myself. Then, I observed Reality.

Sociopaths Rule us.

One thing I noticed throughout the years is that most people can not spot a sociopath… and that is sooo frustrating as they fall prey to these charismatic creatures.

I think you’re spot on here. My Libertarian friends cannot seem to contemplate that a business (or individual) would knowingly screw over another party or business because ‘The Market’ would punish them. ie., no need for those antiquated rules that limit rapacious behavior like the Glass-Steagal Act. The sociopathic behavior appears to be nothing more than a race to the bottom in the financial services industry. In fact, this very point was addressed right here at NC about 4 years ago.

http://www.nakedcapitalism.com/2010/04/citigroups-chuck-prince-confirms-that-risky-behavior-drives-out-prudent-when-risk-is-rewarded.html

“My very Right Wing friend, who is a very good person, truly believes that companies would not do the things they do ”

Thats funny, it used to be the right who called the left naive, and actually, I think they still do.

But they believe in the goodness of other people just as much or more than the left does, apparently. I guess its just as long as those people are white and have money, theyre not supposed to do crime?

He is white and married to a black woman.They attended a Tea Party event together. Many who were there were good people who feel, just like many here at NC, that SOMEthing is very much wrong with America. Of course, they just see the evil Govt. does and seem blind to evil done by Corporations.

I believe many on the Right are well-intentioned people being exploited by cynical (and worse) leadership. Just like many on the Left.

I think there is a fundamental difference in how these groups view the World.

It might be helpful to stop assuming all on the Right are stupid bigots. I know plenty of “Liberal” bigots.

I don’t propose any solutions, but recognizing that any New System is likely to end up with sociopaths at the top might be a start. I assume that if Occupy makes inroads as the Crash resumes, it too will come to be led by a power-hungry manipulator, with a fashionable Brooklynesque beard.

Agree. Bigots to the right of me, bigots to the left, but not all on either “side” are bigots or stupid, but most are authoritarians blindly following whatever is the creed du jour. My family is very rightwing and religious. They are not stupid at all, highly educated, reasonably sophisticated, well traveled and mostly not bigoted. Being super-duper religious, they’ve mostly been brainwashed by their churches (a long story). But most of my so-called “leftwing” pals aren’t much better in terms of discernment. Those on the “left” are mostly still Obomabots (STILL!) bowing and groveling at the fabulousness of Barry O and outright refusing to acknowledge reality.

Sometimes very frightening to witness. Since the dreaded horrid “D” Team is putatively in charge now, I actually have more reasonable conversations with my rightwing friends and family. They seem – at this time – more clear that something is truly rotten in the world, and they are more ready to accept that the difference between “D” and “R” is irrelevant. And that we’re really looking at a massive swindle by the 1s v. the 99s. And they finally seem willing to acknowledge that their prior slavish devotion to ensuring that their 1% Overlords getting everything they want is NOT going to end up with the Overlords treating them any better than the lowliest of poor people.

It’s a tough slog. Certain things seem so evident to me and some of my other pals, but brother it’s a long road to getting the majority of citizens to adhere to common sense and view brutish brutal reality for what it is: we’re run by a bunch of sociopathic criminals (to which the Mafia can only aspire in terms of venality) who care only about themselves, screw everyone else. I do mean: everyone.

The broker does have some fiduciary duties. Not for advice, but as a custodian of assets. They’re required to actually hold the assets which your statements show.

Be aware: brokers have violated this rule before, and simply lied to clients about what was in their accounts. They will probably do so again.

This is good. Now maybe we will have some sort of pushback, as those with money and power are screwed by the financial industry. I have read that the changes brought about in the 30s during the depression happened not because the lower classes rose up, but, the monied classes lost all patience with the bankers, and had enough influence to reform things. We can only hope. Lord knows most of us have no power to fix the mess.

Like Bismark, that Flaming Liberal, Roosevelt reformed things enough to prevent a full-fledged Revolution. It is said that Roosevelt saved the Rich from themselves. ObamaBush were too ignorant and bought off to do the same.

This is what’s been driving me nuts for the last two decades.

Earl Grey in the 1820s and 1830s gave some really blunt speeches, where he told the English nobility that they *had* to reform the system enough that the new industrial classes would feel some desire to maintain the system; and if they didn’t, what happened in France (revolution, Napoleon, etc.) would happen to them. Simple self-interest demanded reform.

We seem to have a bunch of elites who don’t understand this. It’s frightening.

Reminds us when Sen Sanders was questioning a former Goldman Sachs manager on selling that “s***y deal” (Timber Wolf) to his clients. https://www.youtube.com/watch?v=whlzFWwVv98

Or when Sen Sanders was questioning CEO Blankfein on betting against their clients. https://www.youtube.com/watch?gl=BE&v=oOpFbjHcxF0

Why would rich folks continue to trust and invest on Wall Street after all that has been learned? Scaring customers away seems to be least the criminals running Wall Street are concerned with. The drive for quarterly results take precedence over conflict of interest — even with wealthy clients.

Note to rich people: Invest your money locally, in and around the neighborhood you live in.

One “fix” to this problem is the (re-)creation of local stock exchanges and bond markets.

http://online.wsj.com/news/articles/SB10001424052702304563104576357680647926882

http://www.frbsf.org/community-development/publications/community-development-investment-review/2009/august/local-stock-exchanges-national-stimulus/

Hubris and Teflon.

The system has served them well… what’s wrong with it… the whiners are just losers…

They think they are part of the boys’ club and that no one would ever lie to THEM…

To be more specific: Teflon Man Syndrome

John, it was Senator Levin, not Senator Sanders, doing the questioning while he and Senator Coburn were investigating the frauds perpetrated by the banks. Senator Levin is a member of the Senate Permanent Subcommittee on Investigations who brought forward the most important report on all the fraud committed by banks when they securitized their subprime mortgages, an action which led directly to the financial crisis in 2008.

http://www.levin.senate.gov/newsroom/press/release/us-senate-investigations-subcommittee-releases-levin-coburn-report-on-the-financial-crisis

My same Right Wing friend sincerely believes that was all due to CRA. Can you kindly provide link to single best refutation to that horribly wrong perception?

……all due to CRA….

I can’t suggest a link, but a question: What does the CRA require and if the CRA did cause the Great Financial Crisis, why did it take 30 years to happen? (CRA was passed in 1977).

If he (or she) REALLY believes that CRA caused the GFC (and is just not just regurgitating propaganda) , there’s nothing left to do but smile, smile, smile.

This by Barry Ritholtz is very good:

http://www.ritholtz.com/blog/2011/11/examining-the-big-lie-how-the-facts-of-the-economic-crisis-stack-up/

Thank you very much.

John, I was going to make a similar comment. It’s not like there aren’t a million good local projects out there that could use capital. And it’s not like big capitalism hasn’t crashed and burned and found itself without an honest investment. Two problems, one good solution.

Obviously, this is further evidence of a breakdown of morality and propriety at the deepest level.

We see government officials obviously lying to the public, and they no longer feel any shame nor need to apologize. Newspapers print articles that are obviously false – like there is a terrible shortage of American scientists and engineers – and no matter the evidence, they keep printing it because that’s what they’ve been paid to do. The government decides not to enforce certain laws, or to make others up out of whole cloth constitution be damned. It’s no longer about the rules, but about power and what you can get away with.

We are moving to the point where it is not going to be enough to be rich – you will have to be connected to the ruling oligarchy. Then if you are ripped off you can just call your friends and they will claw the money back – the rules will no longer matter, your making a profit will no longer matter, your friends will just shovel money into your accounts. But if you are not connected, then you can be jailed, your assets confiscated etc. on any pretext and you will have no standing to resist, just like the rest of us proles.

This is the inevitable consequence of the neoliberal lie that ‘markets’ can automatically regulate anything, including truth and justice. So we have billionaires telling economics departments who they can hire as faculty – that’s obviously going to make the field of economics better, right? And they are telling newspapers what stories they can and cannot run – clearly going to get us closer to the truth, right? And telling politicians what laws should or should not be enforced – obviously there will be more justice if justice goes to the highest bidder. What can go wrong?

“We are moving to the point where it is not going to be enough to be rich – you will have to be connected to the ruling oligarchy. Then if you are ripped off you can just call your friends and they will claw the money back – the rules will no longer matter, your making a profit will no longer matter, your friends will just shovel money into your accounts. But if you are not connected, then you can be jailed, your assets confiscated etc. on any pretext and you will have no standing to resist, just like the rest of us proles.”

I expect that this phase of gangster capitalism that is now emerging will eventually devolve into straight-up warlordism once the hyper-financialized capitalists have devoured themselves in their insatiable greed. Will there be any resources left to loot on this already ravaged planet?

We can look to Orwell, Huxley and others to help us imagine dystopian futures. Yet Gregory of Tours depiction of life in late 6th century Italy may turn out to be closer to the mark:

“What is there to please us in this life? On every side we see grief, on every side we hear groans. Cities are destroyed, forts overthrown, fields depopulated, the lands reduced to a wilderness. No inhabitant remains in the fields, and scarcely any dweller in the cities; and yet these tiny remnants of the human race are still afflicted every day without respite. And the lashes of heavenly justice do not end because their faults are not corrected even under the lash. Some we see carried into captivity, other mutilated, others killed. What then is there to please us in this life, my brothers? If we still delight in such a world, it must be wounds we love, not joys. We see what will be left of Rome herself, who for a while seemed mistress of the world; bruised again and again by many great sorrows, by desertion of her citizens, by oppression by her enemies, and by repeated destructions, so that we may see in her what the prophet says against the city of Samaria [Ezekiel 24] …Where is now the senate? Where now the people? …And we few who have remained are still daily oppressed by the sword and innumerable tribulations… For because the senate is missing and the people lost, and because even among those who remain sorrows and groans daily increase, Rome. Now deserted, burns.”

(Bishop Gregory of Tours, Homilies on Ezekiel, II.6.22)

Eventually? The shift to warlordism usually happens *very* quickly once nobody trusts the legal system any more.

About ten years ago my retirement fund Board of Directors dropped “the prudent man” rule for an updated version as a guide to their fiduciary duties and responsibilities. After reading the new fiduciary rule it was clear that the board members now bore no responsibility for the failings of their policies or investment strategies. Based on a reasonable reading of the new rule, the only way they could be held accountable was if they were found asleep during an official board meeting. Otherwise, there was really no legal accountability for their bungling or short-sightedness.

Good luck with protesting any of this nonsense. And I couldn’t run for a position on this cozy sinecure since I lived out of state. Dog catchers, I kid you not, are eligible to serve on this board.

Since I’m agnostic, praying is out. I can only hope that I croak before these knuckleheads (who ignored warnings about the dangers of derivatives ten years ago) start with the…”It wasn’t my fault. Who knew?”

It is nice to think that when the rich no longer trust banks, they will then insist on changes to the banks so that trust will return. I am not holding my breath waiting.

It scares me to think that J.H.Kunstler and the Archdruid are right — that the real reason for this is that we are actually poor, not rich. Perhaps back in the day the financial industry could keep a measure of honesty in sharing the profits because there were real profits to be shared.

It scares me to think that ZIRP might be an accurate reflection of the wealth-generating potential of the North American economy — that real enterprises can’t pay more than a pittance of a percent.

It scares me to reflect (rereading George Cooper’s The Origin of Financial Crises) how easy it is for economists to conflate

– 1 – high demand

– 2 – dearth of supply.

Market Delusion. Higher prices can’t bring out goods that really aren’t there.

The scenario isn’t new (Liar’s Poker: “Haf you any more great ideas up your sleef?”), but in the setting — what do you do when you’ve steered you client away from the bad M&A deals and find there are no deals left? What good is a reputation for honesty if you can’t monetize it?

Naw. There’s wealth being generated constantly in the solar photovoltaics industry. It’s not the only one.

The trouble is that our financial institutions are currently heavily leaning on sectors which are not generating wealth.

“But this issue exposes a fundamental flaw of the entire neo-liberal project: that markets are an efficient and fair way of allocating resources, so the more use of market mechanisms to address social issues, like how to provide for retirement or supply health care, the better.”

Yves, you don’t really think these people actually believe this, do you? Those who occupy the upper echelons of any socioeconomic system are there because they have adopted that method that allows them the most efficient pursuit of something for nothing, i.e., fraud, stealing, lying, etc.

If ANYBODY understands the nature of completely manipulated markets, it’s those who are doing the manipulating!! They could care less what the current intellectual non-sense espouses one way or another.

There are many who see it and many more who are blind to it. It’s amazing how deluded you can be when life treats you well.

Good point impermanence. The markets have been this way – dysfunctional – since they sputtered out after Vietnam. And maybe for fear of socialism the US refused to create markets that work. Or maybe it was malice aforethought. It is now easy to see, looking back, that that was a huge mistake. Only markets that are designed to be rational will be rational. We really dropped the ball on “the market.”

I look at NC articles like this one, with this, “But this issue exposes a fundamental flaw of the entire neoliberal project: that markets are an efficient and fair way of allocating resources, so the more use of market mechanisms to address social issues, like how to provide for retirement or supply health care, the better,” and then go on to read the one right next door: http://www.nakedcapitalism.com/2014/05/occ-as-case-study-of-how-regulators-choose-to-fail.html regarding the way by which purported government regulation of the market also seems to be teh suck, and it leads me to wonder just what our gentle host proposes as a solution, other than the standard, “Get more honester [sic] people doing the regulating!” which, to my libertarian way of watching the world, just never, ever, quite seems to happen.

I’m open to discussion on the matter… ;-)

This isn’t a contradiction. Neoliberals don’t like regulators. Regulators are not well paid and don’t get any respect thanks to the concerted effort to move the country to the right. As recently as the 1980s, a lot of the agencies that have been hamstrung, like the SEC and the FDA, were effective and respected. Look, even during the crisis, Sheila Bair did a good job at the FDIC.

The neoliberal project has poisoned the regulatory well. You can’t look at the current state of regulations independent of neoliberalism.

The first simple question to ask someone who claims to give financial advice is to ask who pays you and on what basis? If its other than you in a fee for service basis, Then there is at least a potential conflict of interest. The recent crisis repeats the lesson of the past to trust no one on financial advice. (Consider how many government units got taken to the cleaners by the banks). If you don’t know who pays the advisor, then assume he cares more about how/how much she or he is paid than your welfare. I have become convinced that paranoia in matters financial makes a lot of sense. Of course the first lesson learn what the average returns are, and use this knowledge to detect things that are to good to be true.

“Even Rich People Can’t Escape Being Screwed”

Pathetic. What’s wrong with you people?