We are continuing our discussion of some of the things that the public can discern now that we’ve called to their attention that 12 super-secret private equity limited partnership agreements were unwittingly made public (see here for more of our recent coverage).

We are continuing our discussion of some of the things that the public can discern now that we’ve called to their attention that 12 super-secret private equity limited partnership agreements were unwittingly made public (see here for more of our recent coverage).

We started by what is not in them. That’s because a senior official SEC has stated, forcefully, that these contracts do a lousy job of protecting investors because they are vague or even silent on critical points. Now that we can look at these limited partnership agreements, there are so many of these lapses that rather than try to cover all of them in one post, we’re addressing them bit by bit. We’ll deal with two important omissions today: the lack of independent valuations and reconciliations of various types of distributions to investors.

Independent valuation. In other institutional investments, such as hedge funds, the fund manager is required to provide a periodic valuation of fund assets that is verified by an independent expert. Not providing that valuation on a timely basis or having a misvaluation is seen as a huge deal by investors in other strategies. For instance, one hedge fund manager we know had an operational problem with their otherwise successful fund that led them to send out their monthly net asset value late, which is a huge red flag, and then shortly after that, restate the valuation showing that the earlier report had been about $1 million too high. That sequence created such alarm that it led quite a few investors to redeem as soon as possible, eventually precipitating the death of the fund (other more understanding investors were forced to cut their holdings as their positions came to exceed more than 10% of the remaining fund balance, which their policies would not permit).

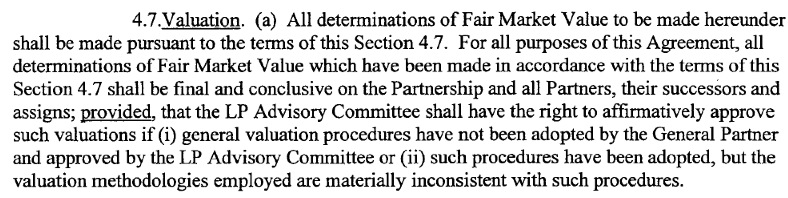

By contrast, it has long been accepted as perfectly acceptable in private equity to turn over the valuation process to the general partner with only laughably weak checks in place. Here is representative language from one of the private equity limited partnership agreements, that of Platinum Equity Capital Partners III (click to enlarge; the omitted intervening section discusses the valuation of marketable securities):

Now this might not seem all that bad until you ponder it a bit. First, for any other type of investment, the default is for investors to get independent valuations as a matter of course. Here, only those investors who sit on the advisory committee are in a position to require this to happen, on an exception basis, and they have to arm-wrestle with the general partner before that can take place. And, critically, the GP gets to appoint the LP investors that will sit in judgment of their valuations (“5.4. LP Advisory Committee. (a) The General Partner shall select an advisory committee…”). You can be certain that the general partner will makes sure that enough pliant or clueless limited partners are designated for this role so as to assure that they never get pushback on this or any other important supervisory matters.

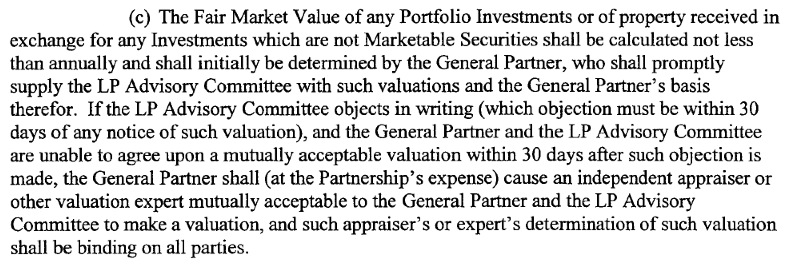

Second, if the limited partners nevertheless decide they really do want an independent valuation, the cost comes out of the fund. Since the general partners typically only represent 1% to 3% of fund assets, that means the limited partners bear those costs almost entirely.

A third issue to bear in mind is that the limited partners are afraid of getting in the bad graces of the general partners. Remember, they believe they need to be in private equity. They do not want to develop a reputation for being difficult or demanding. That might lead them to not being “invited” to invest in other funds. Recall that subservience to the pet wishes of general partners is so deeply inculcated that public pension funds as a matter of course refuse to disclose information that is clearly required to be disclosed under state FOIA laws (see here and here for examples).

And remember, misvaluation is a real issue. A recent paper by Tim Jenkinson, Miguel Sousa, and Rudiger Stucke of Oxford found that private equity funds typically inflate the value of their funds during fundraising periods to make their performance look better than it is, then take the air out of the marks over time. In addition, industry industry insiders report misvaluations late in the life of funds. Remember, the good deals get sold quickly; the ones that are mediocre to dogs tend to linger. The general partners can usually offer plausible-sounding reasons to liquidate the last deals in their portfolio at less than what they were carried at in the most recent valuation. This seldom gets much notice because the commonly used but problematic measure of returns, IRR, tends not to change much even when the last assets fetch less than anticipated.

General partners will no doubt defend this practice, arguing that valuation of private companies is more art than science (true) and that getting an independent valuation is costly. If the funds were to do it once a year, a specialist like Houlihan Lokey might charge $30,000 a company. If you are talking a portfolio of 12 to 20 companies, that adds up.

But the “oh that costs too much” should never serve as an excuse for cutting corners in investing. If if really is too costly to have proper protections for investors in place and make attractive returns, the logical conclusion is investors should stay away from that strategy.

And finally, even if it’s reasonable not to insist on an annual independent valuation of assets for cost reasons, wouldn’t such an exercise every three years or so be a valuable means of keeping the marks anchored to reality?

Explanation of Distributions and Management Fee Offsets. Even though banks process huge volumes of transactions at a very high level of accuracy, most customers still look at their bank and credit card statements each month to make sure they recognize the charges and checks as authorized.

Revealingly, the limited partnership agreements stipulate that when an investor is getting a capital call (a request to send some of the committed funds to the general partners) that they be told what it is for in the capital call notice, meaning whether and to what extent the funds are being used to make portfolio investments versus pay management fees versus reimburse partnership expenses versus fund reserves.

However, when you read the language on distributions, as in what the limited partners get when the general partners, it’s so complicated that it usually represents a separate article of the limited partnership agreement. Similarly the limited partners also get rebates of transaction fees and monitoring fees charged to the portfolio companies as stipulated in the limited partnership agreement (typically 80%, up to the amount of management fees paid). But there is no language in the agreement requiring that these payments be reconciled or otherwise explained in any detail.

Another astonishing omission regarding the fee rebates is the lack of limited partner audit rights.* They are standard practice in business contracts like licensing agreements. If mere commercial counterparties have determined that audit rights are a good way to make sure their business partner won’t be tempted to play fast and loose, why are fiduciaries, which are held to a higher standard of duty, so lax?

These omissions make it hard for limited partners to find obvious signs of catching obvious short-changing or other suspicious signs, like peculiarly consistent charges for fees that are activity-based (as in if suspiciously level periodic charges are combined with various one-off rebated fees in a single payment, it would be impossible to parse them out). But as important, they also set up an excuse for the general partners if they ever manage to get caught. The general partners can piously claim it was all a mistake, unless an insider is willing and able to provide evidence that the skimming was deliberate. If you read the indemnification sections in these contracts, the limited partners have provided very broad indemnification to the general partners, with the big outs typically being for bad faith, gross negligence, and willful misconduct. It might be possible to establish “gross negligence” without proof from someone close to the general partners with sufficiently detailed information. It’s well-night impossible without that.

Bear in mind that these kinds of practices that could never stand the light of day. They were some of the key reasons why general partners insisted on keeping their limited partnership agreements secret for so long. And we’ve only started exposing the dirty linen.

____

* The limited partners do have the right, typically on giving five or ten days’ notice, to review the books and records of the partnership, meaning the fund. But that does not include the records of the portfolio companies, which typically pay most or all of the fees at issue, nor does it include the records of the general partner or general partner affiliates who would, as is the case with KKR Capstone, be the beneficiary of fees that the limited partners look to have a legal basis to have rebated to them.

Great post. Sadly, the lack of defensible valuation procedures is a feature, not a bug, of PE investing. As someone said in the comments of your PE post yesterday, the practice of GPs “smoothing” (fibbing about) valuations gives LPs the benefit of the excess return of small cap equities, but with much lower volatility than those stocks actually exhibit in the public market.

Yeah, I misspoke … shoulda claimed ‘small-cap excess returns with bond-like volatility.’ ;-)

‘Fair Market Value shall be calculated not less than annually’ is what I choke on. Talk about illiquidity!

If one seriously wants to approximate monthly market values of PE holdings (and I sure as hell would), a proxy portfolio of similar-sized publicly-traded companies in the same industries would serve the purpose quite well.

In reality, since IPOs come to a grinding halt during bear markets, using a proxy portfolio of public companies is generous. Refloating debt-laden privately-held companies during periods of depressed equity valuations yields pennies on the dollar, if it can be done at all.

Unfortunately, this is going to be a huge issue a few years down the road, when Bubble III pops with an almighty bang, and Business Week once again proclaims the ‘death of equities’ (or more accurately, their clueless owners, leaping from ledges). JUMP!

I’ve had a peak at investment valuation from inside the PE world, and I can tell you that some of it makes Gabriel Garcia Marquez read like a road sign — I mean, the PE documents were magical without the realism. And yes, they tend to lose all tether to our solar system around fundraising time. The ‘big boys’ on the investment side, however, do tend to see through it all; they know how the game is played.

I have to say, reading about private equity makes hedge funds seem like John Bogle.

And I’m really incredulous as to how so-called sophisticated investors buy into these scams!

My own pet theory is that it’s tribe identification: people will gladly pay dearly for luxury brands that allow them to communicate status. For example, I think the key to hedge fund success, ironically, was the SEC rule barring “unsophisticated” investors in investing in them. No other luxury brand has a govt mandate to keep the riff-raff out. Otherwise hedge funds would have been subject to the same prole drift as fashion brands inevitably are. And once luxury brands lose their status, everyone inevitably sees that except for price they’re no different than the Walmart brand stuff being made in the same Chinese factory.

PE has one upped that: you have to get an “invitation”. since you can only get into PE by being invited, everyone slobbers over each other to get a coveted invitation. The fact that once in the party you’re the pig being roasted doesn’t matter if it allows you to boast to your inferiors that you got in the latest Cereberus fund while people of lesser net worth didn’t “qualify” and have to send their checks to Fidelity like the rest of the hoi polloi.

The SEC rule barring “unsophisticated” investors in investing in them. No other luxury brand has a govt mandate to keep the riff-raff out.

Exactly. Finding out what ‘accredited investor’ means is one of those taps on the shoulder you get when your bank account first hits seven figures.

+1 for ‘prole drift.’ Don’t we miss ol’ Paul Fussell.

This is actually better language then the LPAs that I have seen. Language such as “Final valuation shall be in any case determined by the GP and binding on all parties” is common.

Yes, I thought I’d be generous. The KKR doc has language along those lines, but I didn’t want to be accused of being unfair to the industry by citing the imperial language the biggest funds employ. I probably should have used the KKR text too, but there’s a tradeoff in these posts in how to present the material so that the finance pros (who have much more tolerance for detail) see how this looks form a public interest/common sense standpoint, versus keeping the posts accessible to laypeople.

But the point is the more limited partner friendly language is a sham, since the advisory committee is guaranteed never to buck the GP.

Great reporting. If this were fiction, instead of real with serious financial consequences for pension funds and individuals, I’d compare the PE business model to Max Bialystock’s in the Mel Brooks’ comedy “The Producers”, where the “little old ladies” getting fleeced here are the Limited Partners and pension funds. But there’s nothing funny about this PE business.

I got cleverly scammed by a famously successful hedge fund operator who held something like half his fund in legended energy company stocks. When the listed stocks went up, he raised the valuation of the legended stocks, and took 20% incentives. When some of the listed stock went down beyond easy recovery, he shuttered the fund, and kept all the incentive payments. He then distributed the recoveries from the listed stock, and then declared deep haircuts for the legended stocks. Later he took haircuts again. So far he has never distributed proceeds from sales of the legended shares, but has still kept the incentive payments from their highest valuations. What a racket!