By Wolf Richter, a San Francisco based executive, entrepreneur, start up specialist, and author, with extensive international work experience. Originally published at Wolf Street.

In real estate, particularly in housing, national averages elegantly paper over the gritty details on the ground in specific metro areas and neighborhoods. When a new trend starts in some locations, it’s neutered by data from other locations. Blips and squiggles are averaged out of the picture. But by the time changes consistently show up in national averages, they’ve taken on serious weight on the ground. And now the “smart money” – smart because it has access to the Fed’s free moolah – is abandoning the housing market.

Wall Street money entered the housing market gingerly in 2010 and 2011, then piled helter-skelter into select metro areas over the next two years, grabbing vacant single-family homes out of foreclosure with the goal of first renting them out, then selling to yield-desperate investors and unsuspecting mutual-fund holders their latest toxic concoction: rent-backed structured securities that are even worse than the mortgage-backed structured securities that helped take down the financial system only a few years ago.

It worked. Each wave of buying ratcheted up prices via the multiplier effect, not only in the neighborhood but beyond. It created instant and juicy paper gains on all prior purchases. In this way, the same companies, now mega-landlords, were able to push up the value of their own holdings with new waves of purchases. It was a wonderful game while it lasted. And it was funded with nearly free money the Fed graciously made available to the largest players. Housing Bubble 2 came into full bloom.

But these billions of dollars being pumped into the housing market had the effect of pushing prices out of reach for many potential homeowners who’d actually live in these homes. And first-time buyers, the bedrock of the housing market? Well, forget it. Their share of purchases dropped to 33%, the lowest since 1987.

These inflated prices had another effect: the buy-to-rent business model collapsed. Rents were rising, but people are strung out, and so rents couldn’t rise fast enough to keep up with soaring home prices. At some point, depending on the dynamics of the metro area, the buy-to-rent equation stopped working. And now institutional investors have massively thrown in the towel:

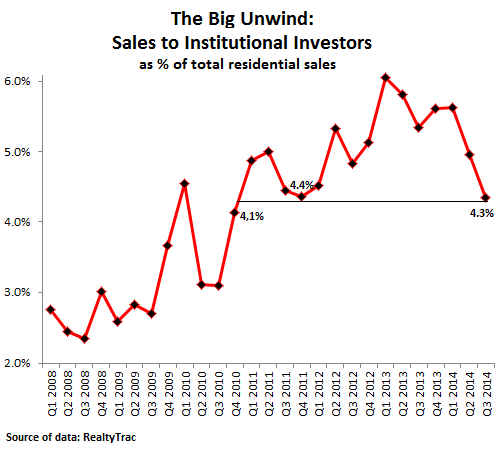

Sales to institutional investors in the third quarter plunged to 4.3% of all sales, RealtyTrac reported. It was the lowest level since Q4 2010. The big unwind.

This is how the “smart money,” coddled by the Fed and encouraged to do just these sorts of things, has reacted to the recent home prices that it so strenuously inflated: It bailed out.

This chart shows that the peak of institutional frenzy occurred in Q1 of 2013. After that, institutional investors – defined by RealtyTrac as entities that purchase at least 10 properties per year – started having second thoughts about the new price levels in some of the hottest markets. But other markets hadn’t caught up, and investors shifted their focus to them. The national averages initially covered up much of the drama on the ground.

Institutional investors are still active, but much less so on a national basis, and they “continue to gravitate toward markets where lower-end inventory is still available,” said RealtyTrac VP Daren Blomquist. And when they’ve pushed this lower-end inventory out of reach for the strung-out American middle class, they’ll throw in the towel there too.

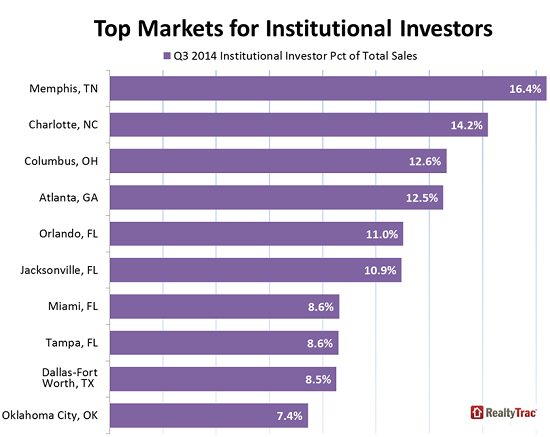

While the hottest markets for institutional investors in the early stages of Housing Bubble 2 used to be Las Vegas and Phoenix, the money guns are now trained on markets that they originally neglected. These are the latest hotspots:

While Memphis was number one in the third quarter, its institutional investor share of 16.4% was actually down from 20.3% a year ago. But some metro areas had year-over-year increases, including most notably Miami from 6.3% to 8.6%, Tampa from 7.5% to 8.6%, and Knoxville from 4.5% to 7.0%. These ups and downs by metro area indicate how the “smart money” comes and goes in waves, focusing on specific markets to ratchet up prices that will provide them with instant paper gains. And not much later, they’ll collect a pile of cash from the securitization of rents.

They did exactly what the Fed in its genius wanted them to do. In the process, they turned homes into an asset class for Wall Street firms and further deflated the American Dream of homeownership [The American Dream Going Bust – in One Chart].

But now what eventually had to happen has started to happen: as investors bailed out of the housing market due to prices that are too high for their business models, and as potential first-time buyers can’t get in due to those prices, sales have swooned for over a year. Initially, prices were still skyrocketing, but earlier this year, price increases started dissipating. And now, prices of new homes have turned south as Housing Bubble 2 pops in its full glory. Read… New Home Prices Plunge the Worst EVER (in One Ugly Chart)

It’ll be interesting to see whether Dan Gilbert’s campaign to resuscitate downtown Detroit – though I do think his self-interest embraces his good intentions – eventually results in nasty unintended consequences.

I define “bail out” as “sell” not “buying less than before”

What Richter describes though is that wave of cash investment ‘moving on’. Small wonder the projected IPOs can be postponed – acquisitions in Charlotte or Orlando lend time, and aggregate national reportage of house prices lend cover.

While I think I do get the general drift of the criticism of mechanics, it seems to me the way it is being framed in the article is a little disingenuous. Would the author prefer the institutional money continues to bid the prices even higher and “not move on” ? Is the very act of moving on and consequent price softness not implicitly part of the market clearing mechanism ?

Further to what I wrote ( I inadvertently seem to have hit “post”);

I think the entire dynamic of the powers that be (fed ?? ) encouraging the institutional money to chase the depressed housing market was to provide some floor and may be some means of allowing the shadow inventory to at some stage find an economic exit.

That this optics seems to have currently at least partially worked is clear. Also clear is that if someone was willing to position themselves astutely to go along for the ride they were rewarded and good for them.

The more pertinent issue I think is, what is the process to pick the winners to whom the gusher of liquidity was provided and what was the criterion for the selection.

I think the bigger question is why was some sort of a warrant or option mechanism was not extracted from in return for bail out funds from the institutions so at least it would seem the tax-payer also overtly participated in the “revival” (TM). The alternate scenario of course would have been to let the cratering of all markets (RE, Stocks et al )continue – which somehow does not seem likely given all pensions funds would vaporized, the muni bonds would have been in larger trouble, all current financial transmission edifice would have been rendered and importantly recognized as moribund.

In short unless there was explicit willingness to revisit all forms social contracts and conventions and look for a different paradigm there is no way any body politic anywhere at anytime in history could have done different. Yes the mechanics maybe quibbled over (and in many situations this is important ) but in the end the substance of the reaction could not have been different.

How and why it came to be that things came to such a juncture is a bigger and perhaps a more philosophical question. The reaction of the triage team after a fact is being criticized ( I have also often contributed my tu pence worth) but on reflection could it have been different given what is the state of play ?

Richter’s interest in the progression is to show how it proceeds and how it escapes notice. If you’re going to question him, it would be better to speak to his actual argument.

Phyllis and I look at older homes with a half acre or better in the South. So far, prices are still in delusional territory. The beginning of a downturn is showing. Prices are being dropped in ten percent increments regularly now. Usually, one drop and then the property is delisted. Six months later, the property goes back up for sale, but now, for the previous low. Before, re-listings would occur with the previous opening price in place. The dreaded online auctions are beginning to show regular events of no bids offered at the starting prices. The larger online auction sites we’ve looked at are generally associated with one or another of the large “crooked” banks or institutions. They haven’t yet admitted to themselves that the glory days are past. They will often re-list at the original asking price and then sit around wondering why they didn’t get any offers the second time. We’re keeping our powder dry and have agreed that a 50% drop in price from the original asking price is the baseline for our retirement home hunt. Depending on your tolerance for the boonies, you can now find decent homes built in the first half of the twentieth century of 2500 square feet and better for under 100 grand. In near move in shape too.

All this suggests that there is an opportunity for a civic renewal movement coming up. When these “rental securitizations” start going t—s up, organizations with some deep pockets can probably buy large chunks of rehabable single family dwellings out of bankruptcy at literally pennies on the dollar. Set up a “sweat equity” rent to own program aimed at the poor and lower middle classes and you have the seeds of a renaissance of the society. This would be something a Soros style plutocrat would be able to pull off. Perhaps even regional governments could adapt some of that “business incentive” programming they love so much to supply future customers for all those entrepreneurs they claim to adore.

We’re looking as well(as is my daughter who wants to buy in the next year or two). I’ve noticed that prices have started to drop too and have noticed the exact trend of listing and delisting that you have remarked upon. I do think that prices need to drop more though because the reality is that there is an opportunity cost to home ownership that is rarely discussed but definitely an issue. You lose mobility when you choose to buy. It takes years to build up equity to the point where moving doesn’t end up costing you unless you happen to be in the latest and greatest hot market when you decide to move. And unfortunately the reality of today’s job market is that you can no longer rely on your employer to employ you for the 30 years that you’ll own that mortgage.

If we buy it’ll be a 15 year with a heavy cash contribution so that we don’t have anything other than taxes due in our retirement years. It’ll also be to save on the lot rental

I hadn’t thought about the mobility issue. We are nearing true retirement ages. So, a house out of the way is possible for us. Someone who might have to move for work would be well advised to consider the ‘rentability’ of their chosen dwelling for future circumstances. I’ve seen private rent to own agreements go either way; to the promised land or to the infernal regions.

One aspect of the social costs of the new short term employment model is just such a disincentive to home ownership. That’s one big reason why we expect house prices to drop significantly over time. The price will have to become comparable to the reward.

Good luck with your and your daughters searches. Have patience, nothing, especially delusional economic systems, lasts forever.

. I think you’re wise to be patient on the sidelines because it’s catch a falling knife time.People tend t confuse a house as an investment rather than a depreciating durable good.

Have you considered Savannah?

You might laugh at me but, after the Katrina disaster, (we stayed in our old house near the mouth of the Pearl River and ended up in our attic,) we are a bit leery of coastal communities. I hear that Savannah is very nice though.

Investment or durable good, a house is distinct from a home, I agree.

Jack Kerouac’s first book, “The Town and the City,” is very good on that subject.

thanks for the background.

I’m looking in the Fresno, Oroville, and Lakeport areas. Seems housing were going very fast, and being bought by flippers, but that has now stopped. I see a lot of deja vu houses too.

We’ve been seeing the ‘deja vu’ houses too. We’re wondering if there might not be a large raft of houses bought for flipping, that never sold, coming down the ways. When this second housing bubble pops, a large number of small time entrepreneur ‘flippers’ are going to be impoverished. I’ve had it explained to me that; “There isn’t any other simple investment that promises such a large return around.” I’m waiting for Patagonian Beefsteak Mines to go up on the exchange any day now.

Coinciding with the end of QE. When new homes got clocked in September the biggest home builders announced they would no longer build homes for the middle class but would now turn to luxury housing. There were a few stories on how cities were the hottest new markets with high-rise condo complexes that only high-rollers could afford, etc. So, as Nomi Prins told us here yesterday, even tho’ all that money primed the pump-n-dump, nobody bothered to change their business model. It just gets more and more insane.

Maybe the Smart Money can go to China, Hong Kong or Moscow (or maybe not there, nor HK if you are prone to double murders).

The best bet, though, is to mess up Spain or other South European countries.

Already messing.

http://www.reuters.com/article/2014/10/24/us-spain-housing-specialreport-idUSKCN0ID0GP20141024

Ugh, I’m 40 and have been waiting to buy a home after taking a bath on a condo I held for a decade. I missed the buying Opportunity after the 2010-2011 drop in prices and now would like to buy a home but don’t want to buy at what could be the height of the market. Looking to buy on train line in suburban chicago with good schools but given the high taxes, would hate to see a drop in prices just after finally “planting my flag” so to speak.

Any advice is welcome, would like to buy next summer.

1. You don’t make money when you sell, you make it when you buy.

2. Timing the market is a sucker’s game.

3. Avoid Hubzu.com and auction.com (They are not legitimate auctions. As in, you are bidding against the auction site itself until the reserve price is met. Lots more evildoings involved.)

4. Walk around the neighbourhood and get the ‘feel’ of the place. (You’ll be living next to these people for years.)

5. Get your own real estate agent to deal for you. (We learned the hard way not to trust the sellers agent.)

6. Make absolutely certain of the ‘chain of title.’ (We have walked away from great deals over this, and there is a lot of this about. [You’re in the right place to learn about this subject, no two ways about it.])

7. Get everyone in the family involved. (You would be surprised how astute small children are about a neighbourhood and the people in it. The little ones haven’t been socialized into neurosis quite yet.)

I just looked at a home that turned out to be a Hubzu house.

What a scam, a fee of 10K to participate in the “auction” and a 500$ fee. Uh, no thanks.

thx for your platitudes.

Oh, so, as I’ve hunted for homes, I’ve noticed in desirable suburban & chicago neighborhoods inventory has been very very low and a strong majority of avail listings are from Berkshire Hathaway. (i.e. Great Northern Chicago hoods, Desirable Western & Southwestern suburbs) I tend to defer to their acumen on economic trends and wonder if the rash of Berkshire listings reflect a saavy investor dumping this asset class prior to the bubble popping or appearance of coincidence brought on by the sheer size of Berkshire’s investment (that any divestiture floods the market overwhelming other listings).

Welcome any comments or other anecdotal indicia

The homes bought by investors are generally not in “desirable neighborhoods”. $200,000 is the maximum price they buy.

Get to know the police people in the area you are investigating. (The cops on the beat, not the bureaucrats.) They will know exactly what a neighbourhood is like, and what way it is trending. An area “in transition” as the boffins call it, can be moving in either direction.

Low inventory can also be a sign that smaller investors and owners are afraid of dropping prices and are “waiting the market out.” Reslez as above is right; timing the market is for investors, ur, suckers, um, I meant gamblers, oh well, you get the point.

Yves,

Guess I’m slightly off topic but within the theme of cooling housing market. However, institutional investors refraining from additional buying of bubble valued 200K homes isn’t bailing out of a position, they are simply opting not to add to their position.

They are looking for an exit, just not necessarily in the form of selling homes individually. We’ve had a couple of PE firms IPO their rental businesses but the taper tantrum killed that. Next we had 8 or so rental securitizations. Now we have Blackstone planning to IPO its rental business next year.

Thx Yves,

So, PE is moving its hot potato, then when next holder of that biz seems profitability of rental book dropping(for reasons outlined on NC, i.e. costs of mgmt), at some point the underlying home will be listed to pay off redemptions(assuming int rates rise. Inventory comes back on the market. Thoughts?

I’m a real estate appraiser (Washington) and I’m seeing prices in this area going up only because there’s few remaining foreclosures or short sales. I’m thinking this could be speculation driving prices up, and, like in 2006, I’m seeing a lot of new offers for business loans to my business. Never had those before. Right before this it was automobile credit offers flooding the mailbox. It’s saying to me that loans are drying up and lenders are getting desperate again to make new loans. FHFA Watts is telling realtors that he’s going to try to ease restrictions on loans and increase demand. Smells like he wants to create a bubble again to me. IMHO Caveat emptor

Real estate is every and always local. If job conditions are good in your area, or people are moving in (retirees?) that could make it deviate substantially from national patterns.

Here in Memphis, we have been going through school system re-organizations. Simply put, white school districts were created in the suburban towns to the east of the city of Memphis. Memphis and the unincorporated areas of the county(Shelby) became a 90% minority school system. The city of Memphis is 65% black. Most the white population is in East Memphis, some in Midtown, and some in condos Downtown along the Mississippi River. There are 2 or 3 public elementary schools middle class whites will send their children too and 1 high school (mostly if they get into the optional program). Rich whites send their kids to protestant private schools. Middle Class whites go to cheaper Catholic schools.

Historically, Memphis has had a 20% poverty rate. The 80’s through 90’s it crept up to low 20’s. 2000’s it was 24ish. Since 2008, it has gone up to 27%. The city itself teeters on insolvency. Every year is a budget crisis and next year’s will be worse. The tax base is property taxes, sales taxes, and fees. We aren’t allowed to have a payroll tax although most of the people in surrounding suburbs work in the city of Memphis. (That is changing though) Middle class white families are moving into the new white municipal school districts. Up until recently too understand real estate in Memphis, it is all about where new houses are being built for whites and where whites just left. With the rise in poverty, collapsing tax base, and chaos/decline of school system, working and middle class blacks are leaving the city as well. Since they can’t move east because property values have risen too much, many are moving south to Desoto County Mississippi. In the 90’s and early 2000’s whites were the largest demographic moving there. The last 10 years it has been blacks. With the outflow of blacks from Memphis into Desoto County, the school system in Desoto County is laying the groundwork to redraw school district boundaries, so there will be separate black and white schools. This is the South.

The city of Memphis is getting more and more polarized. It always has been by race, but the decline in the middle class bodes ill for the future.

http://polardonkey.blogspot.com/2013/09/take-drive-around-county-judge-mays.html#links

A quick note on economic decline and Memphis. There is a large market for custom rims in Memphis. A few weeks ago, State Farm stumbled onto a new trend. There was a car accident. State Farm covered most of the damage except the rented rims. State Farm had never heard of rims being rented before. I am asking around to see where and how much rented rims cost.

So neo-liberalism has created a market in extracting rent from tire rims. These guys don’t sleep, do they?

Are rent-backed securities really a new thing? Isn’t that what REITs have been doing for decades?