Greece and its lenders appear to be on an inexorable path to a Greek default unless Greece capitulates in the next few days. In a move meant to tell Greece that the onus was on them to offer more concessions, the IMF negotiating team left for Washington, as other senior European officials, such as Bundesbank chief Jens Weidmann and European Council president Donald Tusk issued warnings.

The gap between the two sides on the structural reform hot topics of pension and labor market reforms has seemed for some time too large to possibly be surmounted. Moreover, even though the creditors have clearly rejected debt renegotiation as part of the bailout, making it clear that they planned to address that only after a reform package was settled, Greece has continued to try to get it on the table, including it in its 47 page document submitted a week ago Monday, as well as providing a memo along with its response to the five-page document provided by the creditors last week.

This week, the media reported that European commission president Jean-Claude Juncker and Eurogroup chief Jeroen Dijsselbloem made an additional offer the week prior that Tsipras rejected, that of extending the bailout till March 2016 if the Greek government agreed now to certain structural reforms (press accounts varied as to how much Greece would have o concede to get the additional time; it was also not clear if this was a trial balloon or formally authorized).

Recall that after Tsipras received the creditor offer and met with Juncker and Dijsselbloem on Wednesday, he’s said he’d send a response by Thursday that would serve as a basis for another meeting to continue negotiations with Juncker on Friday. Tsipras instead cancelled the Friday meeting (and in keeping did not send a document) and went to Athens to give a speech to Parliament on Friday evening, in which he rejected the creditor offer with considerable vehemence.

I looked at both the Greek and creditor proposals last week and am embedding them below. The press did not discuss them much beyond flagging key points where the two sides remained at odds, for instance, on the remaining gap on the level of primary surplus and on the still large difference on pensions and labor market reforms; one of the more detailed accounts, at Bruegel, noted: “Pension reform: remains a red line for both sides….Labour market reforms: are probably the most red among the red lines at the moment.”

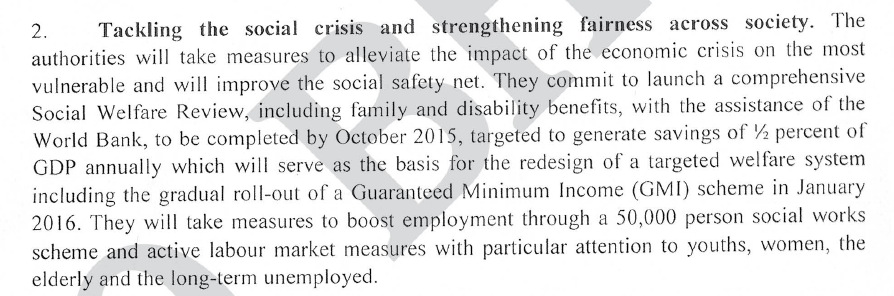

Consider this item on the first page of the creditor missive. It’s item 2, which one would think means the creditors wanted to make it prominent:

The creditors are proposing a social safety net and a minimum guaranteed income program, plus the hiring of 50,000 people for social works. Now a lot of pixels have been spilled on the Greece/creditor negotiations, far too many for me to stay on top of them all. Nevertheless I don’t recall seeing anyone take note of this section.

There’s no corresponding item in the Greek proposals, nothing even close. The Greek proposal, on pages 13-18, discusses “social security issues”. That’s what the media and the creditors have been calling pensions. The difference in nomenclature reflects how pensions have come to serve as an umbrella safety net in Greece. While other European economies have other forms of social welfare, like unemployment insurance, in Greece, pensions are the mainstay of social support. As the Economist pointed out in 2010 on Greek pensions:

Finally, as in many Mediterranean countries, all social spending was skewed towards pensions, essentially for vote-winning purposes. Things like unemployment benefits are pretty miserly in Greece, the real money has always gone to pensions, which have been used as a “substitute” for other welfare policies.

Now in fact there are enough underage people on pensions in Greece to make Germans see red. As reader IsabelPS pointed out, quoting Greek Reporter:

On Greek pensions, from December 2014 and the previous Labor Minister:

“In the public sector, 7.91% of pensioners retire between the ages of 26 and 50, 23.64% between 51 and 55, and 43.53% between 56 and 61. In IKA, 4.44% of pensioners retire between the ages of 26 and 50, 12.83% retire between 51 and 55, and 58.61% retire between 56 and 61. Meanwhile, in the so-called healthy funds, 91.6% of people retire before the national retirement age limit,” Vroutsis said.

So the seemingly high Greek pensions are due in part to an aged population, in part due to the fact that some of the spending on people under normal retirement age might fall under disability or unemployment insurance in countries with a more robust set of programs.

With that understanding, read the creditor offer that we flagged again:

I paarse the long second sentence, the one that begins, “They commit to launch a comprehensive Social Welfare Review” as saying: “You will get savings from current programs like family and disability benefits to round up 1/2% of GDP to fund a targeted welfare program that will include a Guaranteed Minimum Income scheme.” So far that does not sound all that interesting, since it is taking an bunch of current programs and using them to fund a bigger, simpler, and hopefully more equitable program. Not terrible, but it seems hardly important enough to feature in a short, high level document.

But this bit suggests there could be more to it: “which will serve as the basis for a redesign”. That seems to leave the door open for it to be funded more generously. Now mind you, the creditors have taken the view on part of the pension negotiations that Greece could preserve some of the benefits if they found a way to fund them. And regardless of what you make of that sentence, the social works program to hire 50,000 is above and beyond that.

Now this is all seems moot now, but was this a creditor attempt to find a path out of the Greece/lender impasse on pensions? As we’ve stressed, the pensions issue is such a hot button politically in creditor countries, due to the perception that they are generous. That means it’s impossible to get the needed Parliamentary approvals to unless they are reduced, particularly given what were seen as early retirement abuses. Were the creditors trying to give Syriza a channel for telling voters that the cuts in pensions would be offset by spending in new programs?

As we’ve said, the bigger problem was that the ruling coalition conceded on a key point early, that of maintaining primary surpluses, which are tantamount to austerity and agreeing to the painful target of 3.5% of GDP starting in 2018. Thus having conceded the point, they need to make the numbers at least appear to work. So even if that language was means as a channel to provide for programs to make up for what was lost on the pension side, Greece would still need to find a way to fund it within the stringent primary surplus targets.

A colleague with close contacts on the Greek side confirms that it’s worth questioning whether this idea was explored. But we seem to be well past that point, with both sides locked into a lose-lose strategy. But Greece is just about certain to suffer much more serious damage.

creditor-May-2015-proposal

creditor May 2015 proposal

Greede-May-reform-proposal

Greede May reform proposal

Αυτά είναι παραμύθια των συστημικών παπαγάλων. Η ηλικία συνταξιοδότησης στην Ελλάδα βρίσκεται στον ευρωπαϊκό μ.ο. Οι μόνοι που συνταξιοδοτούνται κάτω των 50 ετών είναι οι ένστολοι. Τα επίσημα στοιχεία τού υπουργείου λένε ότι κάτω των 50 ετών οι συνταξιούχοι γήρατος είναι 18,5 χιλ.

A Greek reader can translate this better.

But it essential says.

These are tales of systemic parrots. The retirement age in Greece is the European average of The only people who retire under 50 are uniformed. The official data of the Ministry say that less than 50 years of old-age pensioners is 18.5 thousand.

I would believe the Greek commenter in the article more than the article than Vroutsis the previous Labor Minister who was a member of the protectorate and lied to make excuses to push austerity measures.

Meanwhile, in the so-called healthy funds, 91.6% of people retire before the national retirement age limit,” Vroutsis said.

I cant believe that article is even been used. This is laughable.

Link? You’ve provided a quote with no source. This is a random assertion without any backup whatsoever.

The New York Times says that average age of retirees was 61:

As a consequence of decades of bargains struck between strong unions and weak governments, Greece has promised early retirement to about 700,000 employees, or 14 percent of its work force, giving it an average retirement age of 61, one of the lowest in Europe.

http://www.nytimes.com/2010/03/12/business/global/12pension.html

You need to have a LOT of retirees under 65 to drive the average retirement age down that low.

And the same report was in etkathimerini, and indicated the report was made to Parliament:

http://www.ekathimerini.com/4dcgi/_w_articles_wsite2_1_03/12/2014_545132

I have replied but it didn’t go through.

The quote is from a commenter at the bottom in the article you posted. If he is wrong his wrong and then I am wrong. But I don’t trust anything someone like Vroutsis would say. Or any of those papers.

This is from the OECD if you haven’t seen it. You will understand it better than me. Is what Vroutsis says the same as what the OECD says?

http://www.oecd.org/pensions/public-pensions/OECDPensionsAtAGlance2013.pdf

Greece is at about page 262.

But none of this explains that Greeks contribute a lot of there wages to pensions percentage wise. Have many axillary pensions to contribute to. And still work after retirement or are supported by family. The pension in Greece is used by many to support the whole family and many families supplement their family members pensions with their wages. There is no such thing as a luxurious or better pension in Greece. Despite what is written anywhere. People in Greece don’t retire and that’s it. They have to do something to earn money or they don’t eat don’t get medicines and don’t pay rent and utilities. The pension is not enough compared to the cost of living.

“If the commenter is wrong, then I am wrong.” May I suggest that the next time you dump material into NC’s comment thread, you make some minimal effort to determine whether it is true or false? Similarly, if you don’t trust Vroutis, you might make some effort to share with readers why you don’t, so they can filter information for themselves. Finally, in regards to “Is what Vroutis says the same as what the OECD says?” Don’t assign work to Yves. She has enough to do. You do the work, and you share the results.

Per Lambert’s remark, our Policies clearly state that giving assignments is a major no-no. And other sites have similar policies.

But isn’t this precisely the point of this post? That “the institutions” are suggesting that it would be more efficient and fair, across the Greek society, if pensions were to take the role they are supposed to have, to support people past their working age, instead of standing in place of a global social safety net?

They may have been suggesting that. It looks that way but you’d need to discuss further (or suggest clarification of the language) since part of it is ambiguous. If so, that indicates some appreciation of why Greek pensions are so high as a % of GDP.

I can’t argue about the no. of pensioners and their age (I would want a lot of hyper detailed numbers) but from my informal knowledge of Greece (from a lot of ppl who work, have worked, there) I bet if you add up on the one hand ‘Pensions’ and on the other ‘all other social spending’ – which, in a country like Switz. includes:

… unemployment, partial unemployment, paid furloughs, paid unworked hours; disability benefits, which can include paying a family member to take care of the other (typically, X paid a small but sufficient in the situation salary to care for Y who has Alzheimers), disability aid (paid medical aid for ‘handicapping conditions’ which can include dentistry and plastic surgery, paid aid to assuage, such as taxi rides and computers for the blind), gvmt. contributions to health insurance (those who can’t pay are helped), scholarships for poor students, a stipend for adults who ‘re-train’ or ‘up their working skills’ (typically, a computer course, a new language, for free), and on and on, to end with social aid (3% of the pop. is on social aid, the end of the road thing, of some kind), which pays to keep poor families alive.

—> You would find ‘all other social aid’ in Greece to be extremely low as compared to ‘pensions’ in any other European country (incl. Spain and Portugal.)

Now comparing Switz. with Greece is perhaps ridiculous, but my point is that the ‘aid’ in Greece is churned through ‘pensions’ and that this is an outcome not only of political structure, clientelism or whatever, but of the society.

Family solidarity is high; most/many small biz, and they account for a large part of G. production, are familial; re-distribution is informal, in a family scheme; submission of the ‘young’ to the elders is considered ‘normal’; it is usual, also, for the elders to be obligated to take care of others and to be considered ‘wiser’ and so on. The unit that makes the decisions is more often familial / larger circuit, family ties to others, etc. So churning social aid into pensions makes sense of a kind.

In contrast to Switzerland, where aid is targetted to the individual (fixing his teeth, paying his studies, so that he can become an entrepreneur, a bus-driver, or a good watchmaker), built on a Protestant ethic of individualism, personal hard work and achievement. (I have exagerated the cultural traits for the sake of making my point.)

I can only agree with that. Replacing a social security system that is exclusively based upon pensions shared within families by a more individualist approach as seen in Northern European countries would be a huge undertaking and an open heart surgery.

If a society wants to take this direction at all, for it’s certain to undermine solidarity, government can take a few small steps now and then, and balance out the side-effects. But it will still remain a major project for at least a whole decade and certainly not the type of project that would help reconstruct the Greek economy on a short term.

Interesting point.

I remember reading that Southern European countries tend to have a social security skewed towards pensioners, for voting reasons (they are the most consistent voting group). (Actually, I don’t remember if it was “Southern European countries” or “Southern European young democracies” which is not quite, quite the same). What I do know is that in all studies that I have seen about the effects of the crisis in Portugal, older people seemed to have been better protected from increased poverty: the group whose poverty or risk of poverty increased more was children and young people. And that in spite of all anedoctal (in the sense of not statistical) reports of older parents pensions supporting the brunt of the unemployment, loss of home, etc, of their children and grandchildren.

Also, I suppose that in Greece, like in Portugal, there is a backlog of pensions for which there was no contribution, as the system is fairly young. But I don’t know if that matters for this argument.

I’m sure your sources are correct Yves, but consider this. Pension “reform” now as a prerequisite to obtaining current debt financing. Social welfare “redesign” maybe later, after some study in concert with the World Bank. And the significant concession you point to is some ambiguity about whether the money available for social welfare under this new proposal, if it ever got approved, might somehow be more money than the amount by which pensions are being cut now?

Is that seriously your argument? Because it sounds exactly like the sort of bait and switch B.S. (medicare cuts now to be replaced by some kind of vague and inadequate Trade Adjustment Assistance in the future) by which Obama and Pelosi are trying to get the TPP approved.

All that the creditors would have to do is insist on a 1 for 1 exchange between pension “reform” and any increase in social security spending, i.e. that such spending be “paid for”.

Given the inability of the parties to agree on the primary surplus, haggling about this detail is spitting in the wind. And no, “close to agreement” on primary surplus figures for 2015, when they’re talking about billions of Euros is not “close.” The level of blather might not be as high, because primary surplus figures are such abstractions to the public, while pensions have been cast in lurid colors, but if you’ve been in any kind of settlement negotiations involving big money, you really can’t just split the difference, because small percentages of difference amount to a large amount of money.

I am afraid you are operating from incorrect premises.

We’ve said for years that austerity does not work and that Germany is following contradictory policies that are guaranteed to break the Eurozone if they do not relent.

But the Greeks are dealing with parties who have vastly more power than they do. Greece continues to act as if this is a negotiation between equals, or at least between parties with a less stark power imbalance.

My posture, from the very outset of the negotiations, has been to analyze the negotiation dynamics. That is both to help anticipate whether a deal will get done and what it would look like, and also as an object lesson for students of power.

Thus while Syriza’s stated goals are estimable and clearly more sensible than those of the creditors, they’ve given undue weight to their belief in the merits of their case in how they’ve approached this situation.

it will start to be a negotiation between equals the very day Greece defaults.

No, Greece is immediately in an even worse position. It loses access to much, perhaps all of its trade finance. Exporters to Greece will make only small shipments and demand immediate or even advance payment. The reduction in imports and uncertainty over when they will appear will be another economic blow.

Greece already is expected to run out of dough by the end of the month and will need to pay pensioners and employees in scrip. That will hurt the already lousy economy. Worries about being in Greece when if/when it imposes capital controls will scare tourists away during the peak season (which BTW is also critical for tax collections). All of the above puts more strain on the already barely functioning hospital system and further reduces pharmaceutical imports.

By contrast, a default in the Eurozone will cause some market upset, but a default is not a Grexit.

Greece will go into the creditor sweatbox. I doubt the current government lasts as much as six months.

I don’t think you’ve properly analyzed Greece’s trade balance, because everything you wrote in this comment is nonsense.

I’m not giving you an assignment. I’m just saying I have analyzed this and you’re wrong. You should stop talking about things which you haven’t researched.

With all due respect, it is you who appears not to have looked at any data. Tourism is a large part of the Greek export mix. Greece’s primary surplus before Syriza came in was due to the pickup in VAT receipts in summer months and the month before and after due to tourist spending. Greece ran either at close to breakeven on budget or a deficit the rest of the year.

Two of Greece’s other large export sectors are agricultural goods and refined petroleum products. Greece does not have oil fields. It imports and refines oil, then re-exports it. That means the loss of trade finance and tightening of payments terms by suppliers would interfere with production here.

Pharmaceuticals are an example of imports which may not be as large in dollar terms but are essential. In one of the past Greek crises (I forget whether 2010 or 2012), a special program was set up by the creditors to make sure that insulin supplies continued to come to Greece. There was a high risk they’d not come in in adequate volumes (meaning diabetics would die) and the Greek government succeeded in making enough noise about it to get the creditors to deal with the issue. But notice that there are pharmaceuticals where loss of supply has such a clear-cut risk of death (think inhalers for people with chronic pulmonary problems or anti-stroke medications) where interruption of supply over time would almost certainly lead to more deaths.

— There is no such thing as “the creditor sweatbox”. This is merely an insane fiction of your own devising.

— Tourists routinely flock to countries which have recently devalued their currencies, as will happen with a Grexit.

— Greece’s imports are not important to its economy, with the unfortunate exception of gasoline (which deserves its own analysis). The constant trade deficit will evaporate, but that’s probably a good thing.

— Greece is a major exporter of locally-produced agricultural goods, and exports will promptly be boosted.

It is not of my own invention. Another writer has independently come to a similar forecast:

Read more at http://www.project-syndicate.org/commentary/syriza-eu-default-negotiation-by-anatole-kaletsky-2015-05#BXiEzTZXOqt6eeBy.99

http://www.project-syndicate.org/commentary/syriza-eu-default-negotiation-by-anatole-kaletsky-2015-05

…and then what?

Everything will be fine as soon as Syriza leaves the government?

Yves, you convinced me back in January that you were right about the dire consequences of default for the Greeks. It will be hell and the rest of the Austerity-mongers among the EU Group will make sure they suffer as much as possible for discourager les autres.

My point all along has been to remind people why we are here with a Syriza government in the first place – because PASOK and New Democracy along with all other “accomodationist parties” lost almost all political support. It is simply impossible to force starvation down their throats without imposing an open military dictatorship and ruling by executive decree – what I have been calling the “Heinrich Bruning” model – since we all know what happened after the Bruning government collapsed.

The things you point to as a possible “opportunity” for agreement are not real because the creditors would simply insist, as they always have, on a 1 for 1 exchange between any expansion of social security payments and pension cuts.

EU spokesmen re-iterated that yesterday in saying that if the Greeks objected to the proposed “structural reforms” they would have to identify other “savings” of equal value – i.e. no stimulus would be permitted. And a stimulus is exactly what you have been arguing was the “opportunity” that was missed.

As for the governmnt collapsing, the Greek people will continue to lose confidence in Syriza for their failure to obtain relief from crushing poverty, but the fact remains that NO OTHER PARTY has any credility as a potential governing entity.

That is why I have emphasized the example of 1930’s Germany. The attempt to cobble together a “coalition” government to ram more austerity down the throats of the Greeks will default either to Nazism, Communism or an outright South-American style military dictatorship. There are no alternatives. Anybody young enough or with any kind of transportable skills will flee and Greek refugees will swarm over Europe like North African ones do today.

It is worth remembering that from Syriza’s side 3 indivisible interlinked parts are on the table: 1 -the memorandum 2 negotiation, 2 – debt restructure and 3 – investment for growth.

http://www.informationclearinghouse.info/article42110.htm

Varoufakis interview, Tagespiel

Agreed that that was what they wanted but Greece signed a memo with the Eurogroup in February agreeing to negotiate structural reforms separately (as in first) to get the “bailout” money, the 7.2 billion euros at issue. So they conceded on that plan months ago yet curiously making statements as if it were operative.

I haven’t seen a first comment on a post be so off-point for a long time, and unfortunately that set the tone for much of the thread, as first comments often do.

The question this article raises is stated clearly in the headline. Let me repeat it:

Based on the documentation — not “article” provided — the answer looks to be Yes. We’ve got, for pity’s sake, the creditors putting a “guaranteed annual income” (!) on the table; see the screen dump.

1) This is amazing enough, and even more amazing, the media missed it entirely (so you read it here first at Naked Capitalism).

2) To me, an offer like that is an invitation to continue negotiation. (I say that to avoid the whole discourse about the evilness of the troika, power imbalances, and all that, which true as they are, are not germane to the question of negotiation, and certainly Syriza has been telling the Greek people negotiation has been going, so who am I to disagree?) And yet Tsipras flew home and gave his speech. Did he read the memo? Did he read it and not think it was worth discussing? Did he read it and not respond as a matter of strategy? Who knows?)

To me, I’m just gobsmacked that the words “guaranteed annual income” and the words “50,000 person social work scheme” appeared in an offer from the creditors. And call me crazy, but it seems to me that consideration might have been given to making the question posed in the headline, as well as the substance of the documents reproduced and attached, the focus of discussion, rather than off-point unsourced random comments given a halo of authenticity through the use of the Greek alphabet. Just saying.

NOTE It could be “offer” is the wrong word, but I’m not a negotation maven.

It’s definitely news that this was proposed. The real question is who’s proposing it and is it a proposal with serious backing (the creditors are not unified).

…by the way, the existence of the proposal shows that *some* of the creditors realize that they are holding no cards at all.

Greece has all the cards. I don’t think most of Greece realizes this.

— The one thing which is impossible is Greece remaining in the same currency with Germany. As all reputable trade economists including Krugman have said, this cannot happen without recurring direct transfers from Germany to Greece, which have been rejected not only by the German government but also by the German electorate (so the government’s hands are tied, and so are those of future governments). This doesn’t give Germany any cards; no freedom of action there. Germany actually should want to finance Greece’s purchase of German exports… but Germany’s populace is happy to destroy its own export markets, so it won’t happen.

— As a result, the Greek people’s desire to stay in the euro is impossible. So nobody holds any cards with respect to this. Grexit is *guaranteed*.

When you realize that we’re merely looking at the timing of Grexit and the terms of Grexit, you realize that Greece holds all the cards and the creditors have nothing, nothing, nothing. I suspect some of the creditors are starting to notice. A sensible reaction would be to try to make offers which will avoid a total Greek rejection of the EU, rather than offers which will solidify hostilities for a generation…

On a short term, it’s exactly as you describe it.

On a medium term that could change. Politically, Germany has become the European powerhouse only because of the liberal-conservative and Blairite governments all over Europe backing the German position to seek patronage.

The tide might however slowly turn with:

– Podemos in Spain teaming up with the PSOE (general elections in December 2015)

– The Portuguese Socialists gaining traction and slowly turning their backs against austerity (general elections in October 2015)

– Hollande’s opportunist PS in France losing out against Front National and more nationalist Republicans

– National conservatives in non-Euro heavyweight Poland and other Eastern European countries further gaining traction and turning towards the U.S.

– Britain threatening to break away from the E.U.

– plus SNP, Sinn Fein, AKEL, HDP

– did I miss something?

Unsure what Renzi stabilizing his power in Italy could mean, but Central and Southern Italy would need more development funds. Also unsure about the increasing rifts within the German coalition, with the NSA spying scandal and TTIP looming and the Social Democrats being unhappy with the electoral consequences of their current junior role.

Then the economic crisis in Ukraine will require large-scale financial solidarity to avoid a full-scale humanitarian catastrophe over there.

Finally, the U.S. won’t accept the Eurozone ejecting Greece without finally taking Turkey in, which for the notorious German taxpayers would be an even larger hit.

In the end this all could mean that the German Austerity rule has peaked and will steadily decline in the coming months, even without another full-scale outbreak of the financial crisis. If that should happen, the building of a new, vastly more solidary Europe (and Eurozone), becomes possible.

For the Greek government, every month gained in the negotiations is a month won, except for the economic fallout which Greece however seems ready to bear.

You’re right. Yves (bless all her works) keeps talking about how Spain and Portugal are particularly hostile to Greece’s attempts to avoid austerity but that’s, at best, a half truth. It’s the governments of those countries that are hostile, not the Spaniards or Portuguese who actually have to live under austerity.

I guess it hasn’t registered to Yves that even with further reforms that Greece is going to default. Rather than make brain dead proposals to the EU, wouldn’t Greece be better off accepting that it cannot pay its debts, defaulting and focusing on putting itself back on economically sound footing (part of which would involve pension, labor and other reforms as well as ensuring that the government is only able to spend money that it actually has in government receipts?

Nothing brain dead there.

Watch the first battle in the European struggle against austerity. This is simply not a one-off negotiation about a Greek turn-around. While an “honorable compromise” is what the Greek public would prefer, a possible default is absolutely backed by Syriza’s mandate to push the conflict with the creditors further without giving in. Being thrown out of the Euro might be a consequence, but will recoil on the creditors. The Greek government has fully done its homework and can cope with all that.

Now that Schäuble has been sidelined, it’s up to the rest of the Eurozone.

Still can’t see the negotiations as being locked into a lose-lose strategy.

Contrary to public perception, the Greek government has done quite a good job under the most adverse circumstances. And only those of you who live in Europe, and particularly in Germany, will know what a massive propaganda war the pro-austerity governments have waged against the Greek government. Still the latter has succeeded in slowly but stubbornly pushing its arguments into public perception. And while a majority might still disagree with them, the seeds for a widescale change of thinking have been sown.

Increasingly raising its leverage in the negotiations, the Greek government has managed to elicit at least some retreats by the creditors’ side with more to come at a later point. Whatever the two sides will agree upon, won’t ever be final – with Varoufakis et al. on board, there agreement’s exegesis will remain creative. And if the creditors complain about the text being bent all to much, the next round of negotiations will follow.

The Greek public doesn’t want its government to give in. Even more, it gave Syriza mandate to launch a vanguard attack on the status quo, aiming at a mid-term change of the European political course rather than a mere short-term improvement of the Greek situation. And as far as I can see, Syriza has embarked on that challenge and sticks to it.

So unless defeated on a full scale, the struggle will continue until it has been finally won. That’s why the creditors’ waged a loud war on the Greek government rather than agreeing on a decent (and silent) compromise.

In the medium term, Syriza’s chances remain high, as with anti-austerity movements consolidating all over Europe, it will find more and more allies against neoliberalism – mainly left-wing, but to a certain amount also from the populist and christian-conservative right. In a few years we will see that Schäuble is “over”.

What has Greece has done to deliver on its campaign promises? There are plenty of things they’ve they said they’d do, like go after the oligarchs, help alleviate the humanitarian crisis, and fix the tax system. Suicides are up, the economy is worse, unemployment is up. There are things that Syriza can be doing to address these issues that don’t take money. The reports I’ve read say that Syriza has done perilously little in the way of the business of governing, of delivering services to the people. Only a few ministers are involved in the negotiations, so that isn’t an excuse for not getting around to addressing pressing issues within their budget constraints. Golden Dawn was actually feeding people. What is Syriza doing on the ground? See this from Ed Conway six days ago:

https://medium.com/@edconwaysky/tales-from-the-greek-crisis-92f39bad6626

And from a June 3 report:

https://medium.com/@edconwaysky/athens-five-minutes-to-midnight-28509196c403

Syriza’s support has dropped to below where it was at the time of the elections. The latest polls shows a majority of Greeks now favor making a deal with the creditors: “About 54.8% is fearful of a default and about 50.2% believe that the Greek government should accept the agreement proposal of the creditors.”

http://www.thetoc.gr/eng/news/article/new-poll-majority-of-greeks-want-a-deal-with-the-creditors

It’s easy to urge on the Greeks when you aren’t bearing the cost. And if you think the picture above is ugly, it gets an order of magnitude worse upon a default or Grexit. The public has been led to think the government might win when the creditors are demanding large concessions. What happens when they find the cost of defiance was vastly higher when they were led to believe? Tsipras’ poll ratings are falling as Greeks are starting to realize what the downside looks like from their already desperate situation.

I’m not urging on the Greeks. I’m paying all my respect to the Greek public which has already found out that the cost of defiance is much higher than it thought it to be, yet keeps backing the government on pushing for a mid-term yet full scale victory against the creditors (see the May 2015 Public Issue Political Barometer). And remember the Greek government didn’t have any propaganda apparatus at its will, but had to cope with broad opposition and obstruction from most Greek media.

As for the domestic issues, the government has taken quite some meaningful steps in all areas. While their own government apparatus remained slow, cumbersome and big time aligned with the old PASOK and ND parties; parliament, the cabinet, government taskforces and parliamentary committees are nonstop at work:

The new government has gone after the first few oligarchs and corrupt ex-politicians. They have helped alleviating the humanitarian crisis, giving poor debtors a break and reconnecting them to the electricity grid. They have created a more supportive atmosphere towards the various citizen’s action groups and food banks, and are currently providing the homeless with mobile sanitary equipment and basic medical services. They also fought some battles with the large-time fascist police apparatus ending their often brutal law-and-order course.

Furthermore, they went on to tackle the humanitarian crisis on the islands where much more Syrian refugees have debarked than ever, bringing tens of thousands in to the mainland and providing them with food and shelter.

At the same time, government has revisited the large scale privatization plans and sorted out what to follow, what to modify, and what to abandon. They investigated the war reparation claims. Yesterday, they successfully reestablished the ERT state broadcasting service (paid by a monthly 3€ levy). They have also rehired the 500 laid-off cleaning ladies and delegated them to more meaningful workplaces. All of these are symbolically incredibly important steps. And while the situation on the street has only gradually improved, finally hope has returned, so I would be very surprised if suicide rates wouldn’t drop sharply in 2015.

From what I can see, these are quite impressive achievements for a five months government period without any money to spend.

What they mostly haven’t done yet is the more expensive economic measures, including social security and pensions. But note, this area is exactly what is heavily disputed in the “negotiations”. Any measures taken before crunchtime would reduce their leverage in the “negotiations” or would go too far alienating the creditors. So obviously this large policy area is bound to remain on hold for now.

Also, all fiscal decisions were taken in regard to raising money now in order to pay back some debts, basically to buy time for the “negotiations”, the chicken game with the creditors.

Certainly, it didn’t stop the economy from further declining, but in the end that isn’t possible without big time expansionary measures.

So even if those comments you cited may be right in that roadworks remain abandoned and pensions have not been “reformed” (or axed), this isn’t very enlightening about the country’s situation and the new government’s track record. Syriza has done whatever it could while wrestling with the creditors, and has been quite successful in sounding the bell for the era to come.

Thanks for your perspective / insight, Pancho. And thanks for putting it in English (for us mono-linguists). My guess is english is probably a 3rd or 4th language for you; you’ve done a remarkably good job of writing clearly. Wish I could understand German or Greek and get a better feel for the events transpiring in Europe. (Getting accurate accounts of events in the english media can be a challenge.)

“The new government has gone after the first few oligarchs.” Link, please.

Here.

Taken from this article by a Syrizia supporter that is probably one of the only English language attempts at writing a positive “what has Syrizia done for us?” summery. It does have a few sourced claims like:

http://tvxs.gr/news/ellada/peripoy-85000-megalokatathetes-sti-lista-nikoloydi

http://www.euro2day.gr/ftcom_gr/article-ft-gr/1292904/o-syriza-kanei-to-tampoy-ton-oligarhon-oikonomi.html

https://eydapftaneipia.wordpress.com/2015/04/10/%CE%BD%CE%B9%CE%BA%CE%BF%CE%BB%CE%BF%CF%85%CE%B4%CE%B7%CF%83-%CE%BA%CE%B1%CE%BD%CE%B1%CE%BC%CE%B5-%CF%84%CE%B6%CE%B1%CE%BA-%CF%80%CE%BF%CF%84-%CF%83%CF%84%CE%B7-%CF%86%CE%BF%CF%81%CE%BF/

Sorry, they’re all in Greek, but Yves has told us she has many Greek informants who can translate the gist.

The three links concern:

1) legal actions initiated against oligarch-owned media (nearly all are oligarch-owned)

2) the enormously complex and time-consuming process of identifying individuals with 200,000 euros or more deposited abroad which have not been declared

3) initial recovery on the first 5,000 individuals so identified (3 billion euros), with another 24,000 under current investigation

Awesome. We like evidence (though if one wishes to be really obsessive, one checks provenance, hard to for a non-native speaker). On “initial recovery” (point 3), does that really mean swelling Greek coffers by €3 billion in cash? Interesting if true, also awesome. Or is it a projection of future collections?

From the article on recovery of assets from foreign bank deposits:

Έστειλα 5.000 υποθέσεις φοροδιαφυγής στα δικαστήρια, από τις οποίες το κράτος θα πρέπει να ανακτήσει 3 δισ. ευρώ ενώ βρίσκονται σε αναμονή άλλες 24.000.

I’ve forwarded 5,000 cases of tax invasion to the courts, from which the (Greek) state must (i.e. is anticipated/logically expects) to recover 3 billion euros; another 24,000 such cases are currently awaiting (adjudication).

Quote from Panagiotis Nikoloudis, newly-appointed Minister of Transparency and Anti-Corruption.

More on his background

http://greece.greekreporter.com/2015/02/18/greek-minister-of-transparency-vows-to-fight-corruption/

(this one’s in English!)

Glad to have some actual information from Greece. Thanks!

Very informative comment; I had no idea things were already that bad. In a way, it helps to explain Greek intransigentness over pensions- if your Society appears to be collapsing around your ears the impulse is to hang on for dear life to anything that is “guaranteed” .

My guess is that support for the current Greek government will vanish instantaneously the first time the pension checks are either late or short.

How close are they to that ?

“It’s easy to urge on the Greeks when you aren’t bearing the cost.” That’s just it, the costs will come here. They already are for some, the lowest on the totem pole probably have a similar existence to the overall Greek population. When i read your comments yves, i think you still believe this is all salvageable. Why would we want to salvage the current system? It appears to me the system is cannibalistic, and instead of feeding on the rest of the world as we have for the past 50 so years, the only source of energy left is within our own borders. That is what i see when i look at our governments actions the last 15 or 20 years.

“What is happening in Greece is clearly about more than just money. How can they blithely give Ukraine a pass and a free lunch, and Greece the Iron Heel? “

You seem to think that my describing that Greece is certain to lose is pumping for them to lose.

Do you also think that doctors that tell a patient that he has Stage 4 cancer (5 year survival odds under 20%) is out to see him die? You are confusing analysis with advocacy.

Lose? What do you mean, lose? Lose *what*? You can’t lose something which is already lost….

I don’t think you understand the situation properly.

Grexit is guaranteed by the laws of trade economics. “Making a deal with the creditors” just means more austerity, more suffering, and a swift backlash and Grexit at the next elections.

Have you not figured this out yet? It’s simply a question of how long the extend-and-pretend is going to go on. The longer it goes on, the worse the situation for Greece is. “Rip the bandaid off” is the best option, although it has to be “sold” politically.

The only way in which Grexit could be avoided is a complete policy reversal on the part of Germany, and I don’t see a scenario where that happens.

Maybe Syriza hasn’t properly noticed the risk of Golden Dawn on the horizon.

Remember, *Grexit is guaranteed*. Germany has guaranteed it. This was set up long ago when Germany set up the Eurozone “golden handcuffs” and guaranteed when they recommitted to the “golden handcuffs”. (The golden handcuffs are a disaster for Germany as well, as they destroy its export markets, but they don’t seem to realize this. This is why I don’t consider this to be any power in the hands of Germany; they have shot themselves in the foot, and that isn’t power.)

There is therefore zero cost to “defiance”.

There is, however, a large and real cost to extend-and-pretend, pretending that Greece and Germany can stay in the same currency union without fiscal transfers. If Syriza keeps up extend-and-pretend too long, then Golden Dawn or someone else wins.

“Making a deal with the creditors” accomplishes nothing, it just means that at the next election an even more radical party is elected to remove Greece from the Eurozone.

I wonder why Ed Conway is being bruited here as an expert.

He seems unaware that the Creditors made negotiations conditional on Greece not undertaking any “unilateral” legislation, i.e. enacting national laws in the national parliament. Syriza has done so anyway, first of all the humanitarian aid supported unanimously by all parties. Other decisions have been made through adjusting existing policies.

Ed Conway is on the ground and has also spent a lot of time in countries under financial stress similar to what Greece is facing. He thus has relevant reporting experience. Moreover, he is also ex the Telegraph which is Euro-skeptic, as in much more inclined to criticize the Eurocrats than most of the business (see his former colleague at the Telegraph, Ambrose Evans-Pritchard, as another example).

Hoping this is not a forbidden link around here –

Europe Gives Greece 24 Hours To Comply; Germany Draws Up Capital Control Plans 06/11/2015

http://www.zerohedge.com/news/2015-06-11/europe-gives-greece-24-hours-comply-germany-draws-capital-control-plans

Reuters citing Bild: “It said a debt haircut for Greece was also being discussed, adding that government officials were in close contact with the European Central Bank on that.”

Wasn’t *that* a creditor red-line?

Oh good. Another “deadline.” I’m seriously thinking of collecting them and pasting them in my scrapbook. (Only I don’t have a scrapbook :-( )

I’ll say it again: if Greece holds firm they will get their (worthless) bailout. It won’t be called that though. The Eumenides will come up with a handy euphemism, so their capitulation won’t be obvious. But no one will be fooled, sorry guys.

Europe has a lot to lose, Greece has nothing to lose (because either way they are screwed). Do the math.

Wow. It looks like the Germans may actually agree to major fiscal transfers to Greece. I really didn’t see a plausible scenario where that would happen.

This is indeed the basic fact: “Europe has a lot to lose, Greece has nothing to lose (because either way they are screwed). ” Negotiation theory tells you who holds the cards in that situation.

Indeed, the unthinkable might happen.

Just watched conservative hardliner Wolfgang Bosbach and “social democratic” EP president Martin Schulz on Germany’s notorious No. 1 talkshow “Günther Jauch”.

After repeating his notorious “I’m fed up with the Greek government”, Greece’s faux friend Schulz backed Tsipras against his party’s left-wing only to reaffirm he would (and will) do anything to keep Greece in the Eurozone.

And Bosbach said he expects a majority in the Bundestag to approve handing out the Second Memorandum’s last tranche even without substantial commitments from the Greek side. He just added, he personally wouldn’t just vote with “No” but would also seek personal consequences. (Might he be leaving Merkel’s CDU party to finally join the right-wing nationalist AfD party? We have a saying in Germany that one shouldn’t stop a traveler…)

So all the lamenting and swearing at the Greek government intransigence might be a clear sign that an intermediate agreement will be struck this week. And that it won’t include all too much prerequisites beyond what the Greek side offered in their last proposal. Halleluja!

Without meaningful debt relief, Greece is never going to make it as a functioning member of the Eurozone.

I don’t claim to be any kind of expert like Yves on these negotiations but I’ve never read or heard of the Troika making a single concession on debt reduction.

I guess what I’m trying to say is that a concession on pensions alone, even if true, doesn’t really move the needle much. Greece is toast without acknowledgement by the creditors that they’ve thrown good money after bad and like any creditor in a distressed scenario, they’re going to have to take a haircut.

“…Greece is toast without acknowledgement by the creditors that they’ve thrown good money after bad…”. Almost all of these so-called loans are laundered through Greece and given to creditor banks, not into the Greek economy.

Right, we passed the “charade” stage a long time ago. Any further bailouts serve mainly to transfer money from the left hand to the right hand of the creditors.

Of course it is. And equally “of course,” the fact that all the debt is a result of German banks dumping their Big Shitpile of bad debt onto European countries in 2010, a fact that has conveniently gone into the memory hole, from where Syriza has not retrieved it, despite all the fulminating against neoliberalism.

And recognize that many of the banks (German D-Bank) have received funds from the US Federal Reserve (Trillion$). So the risky private loans these banks made are now your (public) responsibility. The banking system is now nothing more than a legalized skimming operation.

From Greek Reporter today:

AFAICT, from the beginning Syriza has sought a comprehensive agreement that ends austerity and the bailout farce. The focus on structural reforms was forced by the Troika. Creditors naturally want to talk about how a borrower will pay instead of why the debt needs to be reduced/restructured.

Troika-friendly media depicit Greece’s noncooperation as incompetence instead of a negotiating ploy in response to the Troika’s intransigence. The media’s mischaracterization has led to loads of cognitive dissonance as Syriza holds firm in their defiance. Those who accept the media spin can’t imagine why the Greeks haven’t already cut a deal.

=

=

=

H O P

You can read the agreement the Greek government signed with Eurogroup in February. It clearly states they have to submit reforms in order to get bailout funds. Debt negotiations were never part of that deal.

You can read the text of that agreement and our analysis here:

http://www.nakedcapitalism.com/2015/02/benchmarking-greeceeurogroup-bailout-memo-process.html

Trying to retrade an agreement you have made is dealing in bad faith. It’s toxic to negotiations.

Yves, you would be right if these were ordinary negotiations. But again, they aren’t.

Watch the first E.U. government using its electoral power in order to change Europe to the better, rather than pampering its electorate in order to stay in power. Watch the first steps of an ongoing struggle against the neoliberal agenda that won’t be settled until the full defeat of one or the other side.

Jackrabbit is completely right in that the Greek government’s seemingly awkward negotiating strategy doesn’t mean they were inexperienced or incompetent or whatever. There has been quite some debate on whether Hans-Werner Sinn from German think tank IFO got the Eurozone’s TARGET mechanism right or not. But what he got right in hailing (or warning against) “Varoufakis’s Great Game” is that almost every step taken by Tsipras and Varoufakis makes a lot of sense in prolonging the “negotiations” in a war of attritition that would slowly push the Schäuble gang together with its ugly propaganda war into the abyss.

Only imagine an agreement would have been made at the climax of the Austerians’ propaganda war. It would have been a major defeat for the anti-Austerity movement. Two months later, it isn’t anymore.

Don’t you (other guys) always think of the economy only. Coming from all spectres of neo- and postmarxian paradigms, Syriza have mastered Gramsci, Poulantzas, Laclau & Mouffe, and game theory. And they’re successfully making use of it.

So when it comes to breaking a hegemony, it’s not all about economy: rather it’s the psychology, stupid! ;-)

My disagreements with this comment can be best expressed in the form of a table:

If any voters take Pancho seriously, no left wing government is ever going to be elected in Europe, ever again, and for the record, I think that’s bad. I think the Greek government has a duty of care to its people, and (as a corollary) that needs to enter into the negotiating strategy; if capitulation is the best deal for the Greek people, do it, and live to fight another day. Pancho doesn’t. Pancho believes that the Greek people are there to be used for higher and better purposes — different purposes, I grant, from the purposes that neo-liberals think are higher and better, but there to be used, they are. Wrong, wrong, wrong, wrong, wrong.

I agree with you, Lambert, and this is why the difficult moment for Tsipras, Varoufakis, Lapavitsas et al. is now: they need to make calls on the relative suffering and decide…

Capitulating is not the best deal: it leads to further suffering and shifts the moment of the stand up further away, and to a weaker Greek population.

Finding the right negotiation mix is a difficult call. But it is obvious by now that extend and pretend, which means accepting the fake reforms and fake forecast figures, and pushing the ball forward in exchange to money to be paid back instantly, is no longer it…

Lambert, you’re grossly mischaracterizing my comment. As I said in another comment here, it would be perfectly understandable if the Syriza government had gone for just a quick, slight relief from the creditors’ imposts, and otherwise carried on.

Read again what I wrote there:

My point is that Syriza simply wasn’t elected to do the same reforms in just a little bit better way. A remarkable majority of the electorate still wants the government to stay strong and stick to its red lines.

What you’re basically assuming is that the Greek people can’t be represented well by this government as the economy keeps turning down. But then you’re assuming the Greek electorate was all about the economy, as would be the case in our “armchair” societies.

But in fact, Greek people never considered the Greek economy to be “their economy”. Over all the years, they have learned that all economic wealth would go to the banks and oligarchs and all the debt would end up being payed by themselves.

Therefore a great many of them simply don’t prioritize a fast economic turnaround. What they do care about is a government that really makes a difference in staying strong against the

oppressorscreditors, and that doesn’t give in earlier than absolutely necessary.They don’t just want what you call “the best deal” for the Greek economy. Rather they don’t want to capitulate upon the creditors’ demands which they (correctly) consider illogical, unjust and cynical. And it’s certainly not upon us to call their tenacious approach nonsense or brush it aside the way you did.

Pancho, thanks. Your last 4 paragraphs are dead on the mark and well put.

And you can see my response to your comment. As for gross mischaracterization, I’ll just quote you again:

Please show me where Syriza explained that to the Greek people, and where they bought into it. I don’t think you can. You can’t both praise the Greek government (in my reading, that’s exactly what the whole “watch the” paragraph does) for not “pampering” the voters and say “Sure” the Greek goverment has a duty of care and, while we’re at it, claim that I’m “deciding” for the Greek people, while in fact Syriza doing the deciding, and without the informed consent of the voters, I claim, as well. That’s “wrong.”

Adding… General polls on support won’t do it. Show me backing for that not “pampering” as part of a larger struggle against neo-liberalism.

I’m also a bit puzzled as to what “EU government” means. The European Parliament has limited power and is not a party to these negotiations. The Eurogroup is the finance ministers of individual nations in the Eurozone. I must confess to not having a full grasp of the procedural issues, but for decisions of importance, it requires approval of ALL members, making it very hard to effect change. The ECB is one of the real powers in this drama and has managed to be much lower profile than the IMF, but is the real enforcer here (as in it can withdraw ELA support, and that threat lead Ireland, Cyprus, and Greece in 2012 to capitulate). Central bank independence (as in fealty to bankers) is sadly widely seen as necessary and desirable, so I don’t see the ECB becoming more accountable to citizens.

I don’t believe Pancho meant the government OF the EU (as a whole), but rather the (first) government IN the EU — i.e., the Syriza government in Greece (i.e., the first government to do such and so). The trouble with prepositions! (I work as a translator, so I’m used to seeing the misunderstandings that a small difference in such matters can make.)

On another point, I must honestly say that I find the tone of many of these exchanges in the comment threads on this website to be quite offputting. There’s a great deal that I find valuable in this website, especially given my highly limited grasp of the crucial technicalities involved. And I’ll bet a lot other people also find this site valuable for this reason. But given the nasty cuts that many commenters seem to want to administer to other commenters here, I find myself wondering if I’m wasting my time and needessly raising my blood pressure to dangerous levels. And if many others respond as I do on this point, that would be a shame, since there’s a great deal about matters of prime importance (for the left in particular) to be found on this site (including in the comment threads). So, for the sake of maximizing the reach of your admirable educative efforts, could all of those persons on this site (among both writers and commenters) who have a habit of lunging for the jugular — could you calm down a bit, thereby making it easier for those of us who want to follow figure out what’s going on to concentrate on the “sakfråga” (that’s Swedish for the real issue, the substantive matter at hand). Make it all a little easier and more pleasant, please! For those of us who are unschooled in these matters, it’s hard enough as it is to understand the details and technicalities involved.

For what it’s worth, Lambert, you don’t understand politics *at all*. And you are wrong, wrong, wrong, wrong, wrong, wrong.

That is not an argument, and it is a personal attack, pure ad hominem, and a violation of our Policies.

Thanks for sharing. I had no idea it was OK for governments to use their people as guinea pigs without their informed consent, but now I understand. Good to know.

The Greeks would have to enter into new negotiations in January of 2016 to completely abandon the surplus figures they agreed to, simply because the economy will contract further between now and then, even if they capitulated and reached an agreement now. Perhaps the negotiating atmosphere would be better, but probably the EU would insist that Greece stick to the deal they made, just as they have since 2010.

Thanks for the response. It seems that Syriza never got anywhere with their negotiation posture. Giving up on debt relief that early was fatal.

Still that doesn’t absolve the Troika from their miscalculations. They thought Greece would recover enough to handle the debt load by now or at least muddle through like Portugal, and they thought by taking an absolute hard line they’d get Tsipras to fold. It appears that they were wrong on both counts.

I’d consider Merkel and the IMF both to be acting in bad faith here. Their position is intractable – the losses made by creditors have to be recognized now, no matter how incompetent or devious they think Syriza is. Being closer to the Greek people Syriza has the greater responsibility to lead and act in their interest, but I think Merkel and the IMF deserve what they get if in fact this goes pear shaped on them.

Personally, I think the only people with a handle on the situation are the Left Platform in Syriza (too time-pressed to find the link in Jacobin; I will on request), probably because they have old-line leftie contacts who know a war when they see one. But although they can veto what Tsipras does, they aren’t running the show because they don’t have the votes. And it’s not clear they have an answer either.

Lambert Strether: … I think the only people with a handle on the situation are the Left Platform in Syriza

——————

But the Left Platform openly calls for default and a program of low budget surpluses (still “austerity”!), freezing cuts to wages and pensions, debt restructuring, and a new plan for public investment–all of which, while not guaranteeing it, certainly makes Grexit an extreme likelihood–precisely the outcome which we are repeatedly told in these pages will be an utter disaster for Greece.

I said I thought they had “a handle on the situation,” meaning I think they have always been more clear about the power relations. I didn’t say I liked their proposals. On Grexit, we’ve taken our cues from Yanis, who argues it’s a disaster because of the loss of EU agricultural subsidies (and perhaps for other reasons that don’t come to mind). The Greek people aren’t in favor of it either.

They not only have a handle on the situation, their proposals are actually *correct*. Bluntly speaking. They need some more political finesse…

No, they aren’t. Greece needs deficit spending. Unfortunately, they can’t get that with the Euro. Also unfortunately, not only is the cost of regaining sovereignty in their own country extraordinarily high, Syriza has not, to my knowledge, prepared the country for it, and it’s not even clear they have the operational capacity to achieve it.

So the moment of tragic recognition, that there are no good options, has yet to come.

Here’s Lapavitsas’ latest (Jacobin)

https://www.jacobinmag.com/

Actually, there’s something very strange about Syriza’s blocs. The ruling block (Tsipras, Varoufakis etc.) are not in fact the party’s true (inner) power bloc, which is most prominently represented by Lapavitsas given his professional status.

Maybe. Link is to Jacobin mag only. Is this new?

Published yesterday.

Here’s the full link

https://www.jacobinmag.com/2015/06/syriza-troika-lapavitsas-austerity-tsipras/

Costas Lapavitsas at the “party’s true (inner) power bloc”? How did you come to that conclusion?

He is a well respected academic figure, and as Greece’s most vocal proponent of a negotiated Grexit, he succeeded in attracting quite some attention. But apart from being an MP on Syriza’s ticket, he’s about as much in Syriza’s core circle as Yanis is.

The Left Platform’s heavyweights are Lafazanis, Stratoulis and Chountis, with parlamentary speaker Zoi Konstantopoulou representing the hardliners within Tsipras’ majority faction.

Indeed this is true. I was specifically referring, however, to his professional status as an economist within the left bloc.

Maybe it’s time to consider Left Platform/Group 58 as part of Syriza’s strategy.

Not take things so literally. This is a life & death matter for Greece….all stops are out.

why?

Apologies if this link appears elsewhere on the site. I couldn’t find it, and it seems relevant to all current discussions about the Greek crisis providing a nice potted history of the stages since 2010 and a somewhat, to my mind, whimsical rationale for the IMF to get out and bring the true culprits to heel.

I’m firmly, now, of the opinion that default is inevitable, and most likely, in the long run, desirable and morally justified. But then I’m not Greek nor do I have to live there, so it’s easy for me to say.

http://www.theautomaticearth.com/2015/06/how-the-imf-can-save-greece-and-itself/?utm_source=feedburner&utm_medium=email&utm_campaign=Feed%3A+theautomaticearth%2FOCyb+%28The+Automatic+Earth+3.0%29

I can only drop in for a few seconds, because Water Cooler, but let me make two points:

1) On a quick scan, nobody has anything to say about the thesis expressed in the headline. Therefore, I assume everybody agrees with it.

2) Unlike left — I won’t say armchair, so let me just say — theoreticians (folk or academic) the Greek government owes a duty of care to its people.

So yes, it damn well is a negotiation, and not least because the ruling faction in Syriza presented it to the Greek people as just that. People on the left would do well to consider how this discourse sounds outside their particular bubble, because to me, and I would bet to most voters, it sounds a lot like “These guys would throw me and my family under the bus to prove a theoretical point about the evils of neoliberalism.” And if that is the case that Tsipras is making — short term pain for long term gain to escape neoliberal hegemony — then why isn’t he making it? The simplest explanation I can find is that he doesn’t believe it; the fact that Tsipras supports a primary surplus is an obvious supporting fact here.

This one sentence from a Bloomberg story puts things in an interesting, although unintentional perspective:

“A poll this week shows 50.2 percent of Greeks want the government to accept the creditors’ proposals to prevent the country’s bankruptcy. Only 37.4 percent want Tsipras to keep up his resistance.”

37.4% — isn’t that pretty much the percentage of the vote that elected Syriza in the first place?

http://www.bloomberg.com/news/articles/2015-06-11/tusk-says-greece-must-bow-to-reality-as-time-for-gambling-over

> the Greek government owes a duty of care to its people.

Sure it does, but its not us to decide what’s considered the right kind of care by those who are really affected by the situation. While we’re only seeing the economic collapse, possibly the humanitarian catastrophe, we’re missing the collective humiliation by the Troika and the pro-Memorandum forces.

If in May, after everybody had the chance to perfectly understand the consequences, 43% of the electorate say the government should “definitely not retreat”, with additional 15% saying it should “rather not retreat,” this makes it perfectly clear that a public majority still wants the government to stay strong. There’s probably no more politically interested (and literate) public than the Greeks, and as far as I can see (and hear from my friends) they fully understand that this is another type of insurrection against a humiliating serfdom they are not willing to take anymore.

Sure we’re not entitled to encourage them playing the European vanguard, but we should understand that a large share of the Greek public is seeking moral (and finally outright) victory rather than a halfway acceptable compromise. Saturated and leaning back into our *armchairs*, we’re just no more used to that kind of determination.

Two more short points:

– RE the headline: Yes, that seems to be yet another nice concession the Greek side obtained. The creditors seem to go creative, maybe in covering their eventual surrender on many (if not most) issues without losing their face.

– in the Eurozone, without an own currency, primary surplus isn’t a question of faith, but of necessity, if a poor country doesn’t want to be susceptible to blackmail. So if Tsipras says: No more deficits, he basically means: never again a Troika. The Europe-wide struggle against the no-deficit-paradigm is yet to wage – in fact it would be the next phase of the struggle against austerity – but not before Greece has a few more allies in European governments.

^ for this and much more data, again see the Public Issue Political Barometer (13-19 May 2015)

Thanks for the link.

How do your Greek friends think this should be resolved?

Should the Troika chop a few zeros off the debt and everybody just move on?

Do your Greek friends see the debt as legitimate, i.e. should be repaid?

Do your Greek friends think the humanitarian problems will go away if the debt is reduced?

Thanks.

As far as I can see, only few people see the public debt accumulated since 2010 as being just or legitimate. While some are ready to give in and accept it, others refuse bowing down. At the same time, a majority can live with kicking the can further in order to renegotiate the debt at a later point.

Most of them however understand that it won’t be easier to negotiate once a deal has been struck. Just like the government, they understand that the price of a default won’t ever be as low as it is today. Right now, people feel like they already lost so much that they simply don’t dare even losing a bit more now, if that allows them (and the country) to start afresh. So at least currently, a default won’t severely harm the government’s domestic reputation.

Regarding the humanitarian problems, these will improve either way.

If an agreement can be reached with the lenders, they will be solved in a more “Global North way”. If on the other hand Greece ends up being thrown out of the Euro, the problems will be solved more along the lines of an “Emerging Nations way”, i.e. replacing unaffordable import technology by lower, but domestic technology, combined with a laxer handling of foreign patent issues, and a slightly more labor-intense, solidarity-based approach. Institutions for that are in place, plans in the drawers and can be rolled out within a short time.

So Greece is well prepared, and in either scenario the majority of low and middle class people definitely won’t suffer more than they already do – possibly in terms of GDP per capita, but certainly not in terms of quality of living.

Now most people fear isolation and therefore prefer the Eurozone, but if the alternative is an Eastern Mediterranean economic zone within the BRICS framework approach, they will not just be fine with that, but will see it as a fascinating and promising new perspective for Greece and the whole region.

Both Tsipras and Kotzias have gone at great lengths to make this scenario possible, see for example the meeting with the presidents of Cyprus and Egypt. Certainly, the meeting with al-Sisi hasn’t been exactly popular. And neither would be meetings with the Israeli government or even the Syrian regime. But with a slightly lowered profile they could happen soon.

The new Northern Cypriot president opens yet another axis of cooperation, and the waiting AKEL in the South would be even warmer embraced. And the vastly strengthened HDP, Greece now even has a strong and warmly embraced ally in both Turkey and Rojava.

So the alternatives are there, and in the end, it’s the creditors’ decision whether they want Greece to remain in the Eurozone (and act accordingly) or whether they let Greece go. Indeed the result of excellent work by the new government, and as well a comfortable position for Tsipras to negotiate a good compromise.

Thank you very much for the detailed response.

“If on the other hand Greece ends up being thrown out of the Euro, the problems will be solved more along the lines of an “Emerging Nations way”, i.e. replacing unaffordable import technology by lower, but domestic technology, combined with a laxer handling of foreign patent issues, and a slightly more labor-intense, solidarity-based approach. Institutions for that are in place, plans in the drawers and can be rolled out within a short time.”

I have heard this case made elsewhere, and I would like to believe that a “solidarity-based approach” would work, based on emergent Greek networks. I’m not seeing any evidence of it. Do you have any evidence? Organizations to point to? Efforts? It’s one thing to fight a gold mine or occupy a square. It’s another thing to run an entire economy. People come and make pronouncements all the time, but “words are wind,” as they say on Game of Thrones. And presumably a solution to how Greece purchases oil is in the drawer as well.

NOTE Adding, this would mesh nicely with a Jobs Guarantee, but only if Greece is sovereign in its own currency, that is, if it leaves the Euro, not merely defaults.

Thank-you, Pancho, for all your contributions.

Thanks for that. Assuming the polling is accurate, always a big if, and not largely out-of-date, it looks clear that the Greek government’s main red-lines are their public’s read-lines.

A question like “Some argue the government should retreat and compromise….” Well, it’s hard to argue for retreat, particularly in a strongly nationalistic country. In the US, that question would surely skew toward “no retreat.”

Here’s more analysis from the same source. Headline: “Yes to negotiation, no to retreat, no to elections.” Making it — to bring this back to the point of the post — all the more remarkable that indeed that Tsipras (as all the commenters by their silence agree) missed a huge opportunity to negotiate.

“[A]ll the commenters by their silence agree”? Are you quite sure you want to say this? Are you being literal, or instead perhaps a bit hyperbolic? Is this a theory of implied consent you’re working with here? Sounds a bit too Hobbesian for me to swallow all that readily (if you mean it literally, that is).

Yes, this is hyperbole, but there are very engaged commenters on the thread, who (at the time of writing) had not engaged this salient issue.

More on the polling (and speaking to Pancho’s point on the Greek populace having been fully informed) from Bill Mitchell, who the Greeks should really call if in case of Grexit:

It’s that incommensurability that makes me question whether Greeks do indeed “fully understand,” through no fault of their own, but because Syriza hasn’t made the case.

Mitchell goes on to make policy recommendations which Grexit advocates should read.

Lambert Strether: …Bill Mitchell, who the Greeks should really call if in case of Grexit…

————–

Btw, Lapavitsas doesn’t seem too impressed with MMT:

“So-called modern monetary theory, this kind of neo-chartalism, is weak monetary theory; it has very little to offer to the understanding of the eurozone and modern capitalism generally.”

https://www.jacobinmag.com/2015/03/lapavitsas-varoufakis-grexit-syriza/

Well, maybe that’s why you’re getting poor policies from the Left Platform, eh? (Even if Costas isn’t in it.) The Jobs Guarantee would mesh quite neatly not only with the networks Pancho alludes to, but with the employment needs of the Greek people. The Jobs Guarantee (a policy advocated by many MMTers) also puts baseline wages and working conditions under democratic control. So I think MMTers, at least, have quite a bit to say about modern capitalism. (I don’t hear anybody advocating for collective ownership of the means of production, although I may have missed it, so I assume everybody, including Syriza, is operating in a capitalist framework, at least in the “short term”).

Lambert Strether: Well, maybe that’s why you’re getting poor policies from the Left Platform, eh?

——————–

I’m not so sure that the poverty of the Left Platform program has been sufficiently established. What I’d really like to see is a detailed, point by point rebuttal to Lapavitsas’ arguments, rather than simply brief references to Varoufakis’ opposed views.

Bill Mitchell doesn’t see the fact that Lapavitsas is not an ‘MMTer’ as being that significant. The heterodox camp is a broad camp.

As Pancho has pointed out Syriza has incorporated a blend of neo and postmarxian thought. My shorthand for all this heterodox thought is that they want to take practical steps to improve the lot of labor against the strong neoliberal forces that have been in place more recently.

There are various ways of getting there but they want to put people to work at good wages and have good social safety nets and improve inequality.

Totally agree with you here. That’s why Levy scholar Rania Antonopoulos was appointed Alternate Minister for Combatting Unemployment. Her nationwide Job Guarantee plans will be rolled out as soon as the government got clearance (and enough liquidity).

Note that Costas Lapavitsas is an outsider even within the Left Platform, kind of a lonely wolf without all too much traction within Syriza. Unrepetantly advocating a Grexit, he certainly played an important role in dismissing all those horror scenarios ranked around a Grexit, as well as in warning against all too much optimism regarding the Eurozone’s flexibility.

His point on MMT isn’t completely mute either. MMT indeed doesn’t offer all to much relevant policy to Eurozone governments without currency sovereignty. AFAIK, MMT scholars have admitted that weakness before (does someone find a source saying so?).

So MMT-based policies within the Eurozone will depend on carving out more concessions from the rest of the Eurozone unless European policymakers can be convinced of fully embracing MMT.

Now while euro-pessimist Lapavitsas doesn’t see that ever happen, across the ocean, Bernie might make a difference though if he keeps empowering deficit owls like Steph Kelton. So time will tell.

“[C]urrency sovereignty” is absolutely a prerequisite for MMT because the State needs discretion over deficit spending, which Greece does not have. I am more in “In case of Grexit, break glass” mode, here. So we will see how Antonopoulos’ program goes. The left platform commitment to deficit targets, however, is absolutely harmful and destructive. We struggle with that here. (Sanders can’t really “empower” Kelton, because she can’t write legislation or regulations. However, it’s a good thing that she is in the position she is in, and it may yield benefits down the road in terms of combating elite zombie ideas.)

True, but that’s been almost half a year ago. Since then, two thirds of the (mostly oligarch-run) Greek media (including the conservative Kathimerini and the liberal To Vima, to name two papers with an English language edition) has been ceaselessly pushing all the risks and consequences of a Grexit into the Greek public. Until reestablishing the ERT network and besides the Avgi newspaper, the Syriza government barely had a mouthpiece in mainstream media at all. So at least since February, the Greek public has been made perfectly aware of the whole range of possible consequences.

Still, most of them didn’t change their minds and keep supporting an uncomprimising negotiation stance.

Lately, even the possibly most respected pro-business liberal journalist and talkmaster Nikos Chatzinikolaou, who initially didn’t support the Syriza government, has approached the government’s course harshly dismissing the creditors’ last proposals:

So, no. People clearly still don’t want the government to bow down. In the contrary, more and more of them are convinced that the creditors’ proposals would lock the country (and themselves) into a deadly downwards spiral.