By Lambert Strether of Corrente.

Most coverage of ObamaCare lately has focused solely on increased enrollment numbers; as we know, this is a deceptive metric, and is probably due, at least in part, to an economy no longer in the depths of depresssion. However, the mere fact of enrollment tells us nothing — any more than a ticket to a movie means the movie ends happily — and so in this post I want to focus on “narrow networks,” since it seems a common-sense notion that your doctor (whether you could “keep” them, or not) and your hospital are key determinants in your quality of care, especially if you require a specialist, and narrow networks limit both, as Modern HealthCare describes:

Narrow-network plans have grown in popularity, particularly on the Affordable Care Act’s insurance exchanges, because their cheaper premiums appeal to price-sensitive consumers. About 70% of plans sold on the exchanges in 2014 featured a limited network, and their premiums were up to 17% cheaper than plans with broader networks, according to a study by consulting firm McKinsey & Co.

But there is significant consumer and provider dissatisfaction with how many of these plans are organized, including concern about inadequate access and information. Critics say insurers have made many missteps in building adequate networks and maintaining accurate, up-to-date provider directories. In some rural areas, there are too few in-network providers, forcing plan members to travel long distances to see one. Some patients find out that a hospital or doctor was out-of-network only after they receive a shockingly high bill. So far, federal and state regulations on narrow networks are vague and inconsistent, experts say.

Naked Capitalism readers, of course, have been warned about narrow networks starting in 2013: See here, here, and here, for starters. Modern Health confirms our warnings:

Anecdotally, narrow-network plans have led to surprise out-of-network bills for consumers. Hospitals often contract out for emergency physicians, radiologists, anesthesiologists and other hospital-based specialists. While a hospital may be in a patient’s plan network, some of its doctors may not be—and patients may face bills based on out-of-network rates.

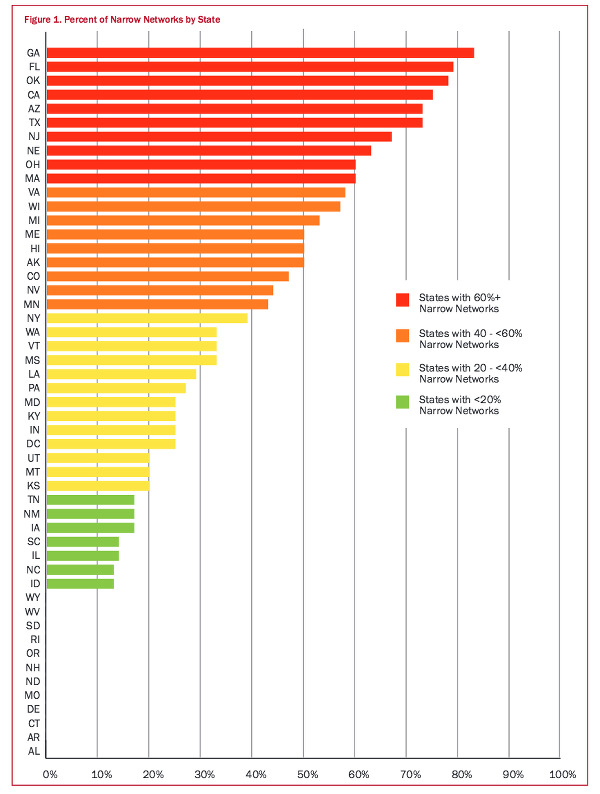

Of course, anecdotes are all we have, since oddlly, or not, the Obama administration never studied the matter. Now, however, we have a new study that at least gives us an idea of how prevalent narrow networks are. From the University of Pennsylvania’s Leonard Davis Institute of Heatlh Economics, we haveDan Polsky and Jan Weiner’s study, “Variation in Narrow Networks on the ACA Marketplaces” (PDF). And we see that narrow networks dominate many states, although we also see great variation between states. From Table I of that study:

Or in prose:

The 83 percent of Georgia plans having narrow networks surpassed that of all other states, according to University of Pennsylvania researchers.

Georgia’s narrow network rate was followed by Florida’s 79 percent; Oklahoma, with 78 percent; California, with 75 percent; and Arizona and Texas, each with 73 percent.

Narrow networks were on the increase before the ACA was enacted, but they have become more prevalent under the health reform law.

However, we see not only variation between states, but variation within states. For example, North Carolina:

Taken as a whole, only 13 percent of ACA plans offered on the federal exchange qualify as narrow networks. However a closer look shows that those plans are concentrated in in and around the Triangle, according to the report, done by Dan Polsky and Janet Weiner, Janet Weiner of University of Pennsylvania’s Leonard Davis Institute of Health Economics (LDI).

So how narrow are they? The San Francisco Business Times:

The average Obamacare health plan’s provider network includes 34 percent fewer health care providers than the typical commercial plan, according to an analysis by Avalere, a Washington, D.C.-based health care consultancy.

Such exchange plan networks include 42 percent fewer oncologists and cardiologists, 32 percent fewer mental health experts and primary care doctors, and 24 percent fewer hospitals, Avalere said Wednesday.

Now, to be fair, there are studies that provide proxies for delivery of health care services that can be used to support a claim that narrow networks do not impact the delivery of health care. Health Affairs:

We found that the common belief that Marketplace plans have narrower networks than their commercial counterparts appears empirically valid. However, there does not appear to be a substantive difference in geographic access as measured by the percentage of people residing in at least one hospital market area. More surprisingly, depending on the measure of hospital quality employed, the Marketplace plans have networks with comparable or even higher average quality than the networks of their commercial counterparts.

However, averages mislead; as we know. For example, averages will conceal the fact that one Tennessee citizen dropped their care because their hospitial was an hour’s drive away, even if another was satisfied. Averages conceal the fact that narrow networks discriminate against poor people with cancer. And averages conceal the fact that narrow networks create “medical homelessness” if citizens can’t find primary care doctors. Worse, implicit in the very idea of applying an averaging methodology in this case is the value judgment that big variations in citizen access to potentially life-saving health care aren’t in the least problematic; that a civilized society treats the health of its people as a crapshoot, albeit a highly profitable one (at least for a very few).

But wait! You say. All these problems happen because the citizen didn’t pay the tax on their time invest sufficient hours in due diligence to find out whether the plan they are mandated to sign up for has a narrow network or not. Unfortunately, ObamaCare affirmatively conceals this information. Polsky and Weiner:

Within the current marketplaces, it is difficult for a consumer to assess network size, even as a broad concept. As a result, the trade-off between network size and premiums is not at all transparent. It is even hard to gauge which providers are in the network as this typically would involve checking the provider directories at the issuer’s website for a particular provider for a particular plan. These provider directories are notoriously out-of-date.

Cindy Zeldin of the consumer group Georgians for a Healthy Future describes the effect on the consumer citizen:

“Right now, provider networks are a bit of a black box for consumers, preventing them from choosing the plan that best meets their needs and potentially limiting access to care,’’ she said.”

Zeldin said it’s true that some consumers are willing to make the tradeoff of a lower premium for a smaller network. But that’s not the whole story, she added.”

“Others need a broader network to meet their health needs,’’ she said. “And everyone deserves the tools and information to make that choice and to know that they can access services for all covered benefits.”

(Of course, under the simple rules of neo-liberalism, nobody “deserves” anything except for what they get. What’s wrong with you, Cindy?) Now, to be fair, the ObamaCare directories may improved in the coming year (that is, seven years after ObamaCare’s enabling legislation was passed). Polsky and Weiner once more:

New federal rules for 2016 will require plans to publish up-to-date, accurate, and complete provider directories, including information on which providers are accepting new patients, the provider’s location[1], contact information, specialty, medical group, and institutional affiliations.

Assuming this happens, which given ObamaCare’s clusterf*ck-littered history is a big assumption, the consumer’s citizen’s fundamental problems with narrow networks are not solved by this minor fix. First, the issue is not providing information on any one plan, but on comparing plans, which the fix does not support; that is, ObamaCare’s affirmative concealment of key information continues. Second, the fix goes meta in a particularly neo-liberal way: It assumes that providing information about services (in the argot, “transparency”) is equivalent to actually providing services. I mean, what do I do when I use ObamaCare’s spandy new directories, plural, and discover that the specialist I need is 500 miles away? Move? Finally, the fix makes a second classically neo-liberal assumption about consumers citizens: That acquiring and aggregating and making sense of information is frictionless and cost-free (as it is indeed for the top 10% who wrote this monstrosity and are busy using their expertise to cash in on it; they have lawyers and accountants and personal assistants and staff). In fact, that assumption is utterly untrue; we can see how hard it is to do research on the ObamaCare website from this post in 2013, where Dromaius researched for specialists. Now imagine somebody not middle-class, not technically inclined, and poor trying to do the same from a public library terminal. So we see this that ObamaCare’s tax on time is especially onerous for the poor and the already sick, those who (assuming the program to have been designed in good faith) ObamaCare was designed to help.

So why is this so hard? Why is it hard to aggregate data across health insurance plans and present it to consumers citizens so that they can make informed decisions about their health care choices, even given the rotten circumstances Big Health has placed them in? Well, as it turns out, the reason is quite similar to the reason Greece couldn’t escape the Euro: The health insurance industry has a concrete material basis in information technology, that technology wasn’t designed or built with that function in mind, and it’s difficult/risky/expensive/not in their interest for its owners to change it[2]. Here’s what Polsky and Weiner had to do to get the data for their statistical study[3]:

From the 2014 list of all 1065 unique silver plans (and 6690 unique plan / rating area combinations) sold in the marketplaces for all 50 states plus DC as provided by HIX Compare, we identified 394 unique provider networks offered by 267 different issuers. We used the publicly available provider directories on the issuer websites of individual marketplace-based networks and plans to gather all providers in specified networks, including data on provider characteristics such as specialty, name, gender, and geographic location. These data were collected in the fall of 2014.

The provider lists from which these data were gathered were not uniform in their formats and coding. Thus we created a multi-stage cleaning process to integrate all lists into a list with unified formats for names, addresses, and specialties (see our first Brief for more details). We used national provider datasets to confirm unique physicians and to identify physicians in the rating area who did not participate in any plan.

We excluded non-matching records, physician locations outside of a plan’s rating area, and issuers and networks without complete data. Our analysis dataset consisted of 450,232 physicians participating in plans issued by 267 carriers across 355 networks where we were successful in gathering information on all physicians. Table 1 lists the number of issuers and networks in each state’s marketplace and the number of networks that we were able to collect for our analysis. Overall, our data sample includes 90% of all silver plan networks in the 2014 exchanges.

Building ObamaCare directories, plural, won’t be an easy project because it involves the same systems and data issues. And it’s also a back-end project: It doesn’t involve the shiny, public relations-friendly website on the front end; it involves accessing multiple databases, gnarly data formats, and plenty of data conversion; all tasks that the administration has already shown it is simply not competent to perform. I mean, they still haven’t fixed the existing back end. For example, the ObamaCare back end is still failing to validate applicants for eligibility, and that’s its basic function:

[T]he government is unable to verify eligibility for insurance or subsidies. The Government Accountability Office recently announced it was able to successfully enroll 11 out of 12 fictitious applicants, (some with invalid or nonexistent social security numbers and others noncitizens claiming lawful presence in the U.S.) on the federal exchange in 2014 despite the fact that the GAO did not provide any supporting documentation requested by the exchange for some applicants and provided fabricated documents for others.

All 11 fictitious applicants who enrolled in 2014 were automatically re-enrolled under a Centers for Medicare and Medicaid Services policy that automatically re-enrolls policy holders for 2015. The outside document-processing contractor does not check for fraud beyond flagging obvious document alterations.

A just released report from the Department of Health and Human Services inspector general confirms that the federal exchanges internal controls were not effective in ensuring that applicants were eligible for enrollment in qualified health plans and for receipt of subsidies – other than identifying applicants incarceration status, the exchange had trouble validating applicants’ citizenship status, social security numbers, income and family size and lacked reliable procedures for resolving inconsistencies between information applicants submitted and information in the federal data services hub.

So, while from a humanitarian standpoint I suppose I should be happy that ObamaCare will sign you up as long as you aren’t in jail, from a systems perspective, at the back end where the eligibility verification takes place, ObamaCare is the same clusterf*ck as it has been from the beginning. (The GAO report has dropped like a stone, out of the news flow, so the other defining characteristic of ObamaCare — nobody is ever held accountable for any failure, no matter how gross — holds good as well.)

In other words, don’t assume those directories will work, because the administration seems not to have the operational capacity to build them. As a consequence, don’t assume that the network you join isn’t narrow, even if — after doing your many hours of research — you concluded it is not and signed up for it.

What are we to make of this? First, that ObamaCare’s relentless creation of second-class citizens continues; the quality of health care you get is the luck of the draw. ObamaCare, being at its heart a bailout of the insurance industry, was not designed to change that, and hasn’t.

But there are wider implications. Maggie Thatcher, bless her heart, came up with the neo-liberal trump card: “There Is No Alternative,” which we often abbreviate as TINA. In the case of the Greek drachma, as we showed in remorseless and excruciating technical detail from people who actually build and maintain such systems, there was indeed “no alternative” to the Euro-based payments system available in a realistic time-frame. The concrete material basis in information technology did not permit it. That the Greek outcome was tragic makes it no less real.[4]

In the case of the health care system in the United States, however, there is an alternative, for which the concrete material basis already exists in the form of information technology: Medicare; a simple, rugged, proven, and popular program already used by millions. Here, however, we see a second tragic outcome: There seems to be no alternative because corrupt politicians from the legacy parties — for example, Hillary Clinton — carefully airbrush the real, existing alternative away.

Notes

[1] To best serve the consumer citizen, this information would have to be updated in near real-time, since people will be using it to make decisions in real time, and not merely during the “enrollment period.”

[2] Which makes sense; a cartel doesn’t tend to make it easy to compare products between cartel members; its simpler just to fix prices anyhow. Nor does any health insurer have any particular incentive to “transparency,” given that they profit by denying care.

[3] The Polsky and Weiner study is static, mind you, a snapshot in time taken for academic purposes, which is very different from keeping an ObamaCare directory “up to date” so that consumers citizens can make decisions in real time. Their project scope is sufficient to create a sample from which generalizations can be made. The project scope of any ObamaCare directory is the entire country, all plans, and all providers; 100%, not 90%, and in near-real time.

[4] Indeed, if we cast Tsipras as the hero, we might even regard the moment where he rejects Varoufakis’s hare-brained scheme as the moment of tragic recognition.

Appendix

Why the state-to-state variation? We don’t know, but Polsky and Weiner suggest:

But what causes one state to have more narrow networks than other states? This is a question for future research. While we cannot answer that question, we do find a strong correlation between states that offer HMO plans and states that have more narrow networks. … Here we see that states with a high prevalence (60% or more) of narrow networks are dominated by HMOs, whereas states that have the lowest prevalence (20% or less) are dominated by PPOs.

HMOs were resoundingly rejected by (most) consumers citizens in the 90s, when Big Health first tried them. ObamaCare is doubling down on HMOs by rebranding them as Accountable Care Organizations (ACOs), and giving them another shot. So it seems likely that narrow networks will only increase in number and extent.

Readers, comments are open because I’d like to hear of your experiences on this issue!

“Within the current marketplaces, it is difficult for a consumer to assess network size, even as a broad concept.”

This is way too diplomatic. In fact, the labeling of some plans on the exchanges steps right up to the line of consumer fraud. The names are highly suggestive of being affiliated with major medical centers when in fact they are not. We have an adult child currently shopping on the Washington state exchange. It took us some time to figure out that, for a plan called BridgeSpan Exchange Silver+ UW Medicine, despite its name, the UW Medical Center (arguably the leading medical center in the state) is out of network. There is an entity called Northwest Hospital & Med Ctr Dba UW Medicine Northwest which is in-network, but the main UW Medical Center and associated practices are not.

Under the best conditions, it would be very difficult for a harried consumer to pick a plan based on the network. Fighting against insurance industry marketing, it’s almost impossible.

Not sure where this fits in the overall picture but a little anecdotal information:

– There’s a lot of buying and selling of hospitals going on in California.

– My wife, a teacher, was offerred the no extra cost option of Mexican Insurance. We live 10-15 miles from Mexicali, B.C. a city of close to a million. The people who use it say it’s pretty nice. Main problem is long wait times for crossing back to the U.S..

– Every time we use my wife’s insurance, thankfully not often, the company calls to make sure we don’t have other insurance. Yesterday she was told that the insurance of the person whose birthdate falls earliest in the year will be used first. So if I buy myself a cheap insurance, with a high deductible and copay, that one would be billed first. Hmmmmm…

Your average Democrat lives in health insurance Happyville and has zero experience with Obamacare (i.e., the “exchanges”/expanded Medicaid). That’s an important little fact, seems to me.

Maybe “folks” (“consumers”?) should start sending their unexpected bills to the White House or to Nancy Pelosi’s office. Or maybe to Jonathan Gruber. Seriously. And ask them to pay up, please. Mind, you may want to actually pay the bills yourself in order to avoid certain consequences, but for god’s sake, let’s at least send them a copy and a nice note.

Anyone?

Just be sure to but “signature requested,” “return receipt” requested when you send along the bill. And while you’re at it, use the address change form for your account on the Exchange so you aren’t troubled with further dunning. Maybe use the local office in the district so the zips make sense?

Of course, I would never advocate this….

Excellent idea re the use of signature/return receipt! Applicable to all manner of similar situations.

In my limited experience with the powerful, one of the things they despise the most is for upstart peasants to call them out on their hypocrisy and their bull$#it. Doing so won’t get you what you want, but it will make them gun shy, which is itself a victory of sorts.

Part of the reason that I did not beggar myself in order to submit to the ACA mandate was that when I first starting looking for insurance not one could tell me if my doctor or the nearest hospital to me was in network. I determined that they were not by checking with each. Although last year I spent little time on it, just determining that the plan I was most likely able to afford was not in network meant once again checking with those entities and once again finding that no, they were not in network. And mind you I use the word afford with greater irony and far less cynicism then those that titled this flaming piece of excrement.

It is shocking to find that once again one of the basic things that enables the Swiss system to work was jettisoned by the insurance lobbyist most involved in crafting this law. There should, of course, have been distinct requirements as to information regarding networks, minimum size of networks, and yes exceptions to the need to be in network. Certainly if you want the law to work in making sure that your citizenry is adequately provided with health care and not just inadequately insured, these would have been among the things you would have insisted upon when crafting an American version of the supposedly market based Swiss system. But just as the Swiss system is not truly market based (what with its price controls and strict regulations of those markets), ours is only market based if your market is about shooting the consumer like fish in a barrel as the protections are all on the side of protecting the suppliers rights not to supply the service.

I recently did some health insurance investigation for a friend who needs to reduce insurance costs. Since I’ve lived in the area all my life, and I grew up in a family capable of obtaining quality medical care, it’s possible for me to quickly scan a plan and its participating hospitals and doctors to know whether the plan is worthwhile. Here’s what I found:

–The plans with the most well-known names (i.e., Blue Cross) were the most expensive, had a fine selection of hospitals but a poor selection of the best physicians.

–There are ways to save money if you don’t need subsidies, but not if you need mental health care. (My friend has a child who takes medication for attention deficit disorder, so that option was out.)

–If you’re over 50 years old, you’re screwed, regardless of the plan. This is one area where the health industry continues to discriminate.

–Illinois’s s-chip program is one of the best deals anywhere: great hospitals, great physicians, extremely low costs for medication, doctor’s visits, etc. Families earning up to $94,000, if I remember correctly (it may be $92,000, but it’s still fairly high) are eligible to enroll their children in s-chip. I suspect a lot of families don’t look at this option because they think it’s Medicaid, and that they don’t qualify, or they think there is some sort of social stigma attached to using the program.

–Some of the best physicians no longer remain with one medical group or hospital. So if you think you’re basing your selection on access to a particular physician, you may be surprised that the physician you wanted is no longer affiliated with x, but now works for y.

I think it would be very difficult for less savvy or less educated people to understand the options available to them and the true costs. Each person or family is different, and if you have special needs–whether that means medication, physical location or whatever–the decision making process becomes quite complex. I think it’s only going to be more restrictive as these health insurers merge.

Have your friend get their child’s ADHD meds from a neurologist instead of a mental health doc. Then it is covered under medical. It’s what we do and have for years. Our son continues on the meds and is now in college. This works well and you get actual medical care and evaluation not just some shrink pill pusher.

Thanks! Great suggestion.

“Medicare; a simple, rugged, proven, and popular program already used by millions”

Agreed. I would add that expanding the Veterans Affairs to be a UK NHS For All system is a 2nd alternative.

Perhaps “Da Troopz” would be for it, if said expansion boosted the VA’s economies of scale to add additional capacity in hospitals/physicians/etc, thus increasing the service level of the existing military members. Also if it were merely a “VA Public Option”, it could charge say 130% of actuarial cost to the Option patients, and using the leftover revenue to the VA’s “capital budget” to maintain/expand the capacity.

I know this would go against the official politician propaganda that Military Lives Matter The Most [1] and Regular Murican Lives Don’t Matter and Deserve No Social Insurance Whatsoever, “So Go Die Quickly” (c) Alan Grayson. So it would be a propaganda/messaging struggle to overcome this if this policy were to be legislated.

What do yall think about a VA/NHS For All alternative?

[1] I understand that the VA Benefit might be the only actual case where We Love The Troopz TM is actually demonstrated by the Federal politicians & BigMedia, whereas in many other cases the powerful screw over the military/ex-military, such as not treating ex-military that have demonstrated PTSD

Agreed on the VA. As far as IT goes, we’ve got the concrete material basis for single payer in not one, but two systems.

And yet TINA. It’s undiscussable. Are these people insane? Wait, don’t answer that.

The VA works for me because I have almost no need for medical care. I get a checkup once or twice a year, and an inexpensive blood pressure medication.

In recent months, I have noticed that the RNs who work with my primary physician no longer answer their phones. I can contact them through secure email, with a day or two’s delay. I also noticed a decrease in hours at the clinic that I go to.

You can’t prove anything by a sample of one, but I have a feeling from my experience and from unspoken attitude of the clinic staff that they are under a lot of pressure to provide services with reduced hours and budget.

The plural of anecdote is data.

More antidotal info. My bestie has worked for years as a PA in the Lebanon PA VA hospital. The understaffing is horrendous the VA has no money to fully staff its facilities. Ditto supplies and equipment. She is a do gooder type and only works there because she says someone has to do what they can for these patients though the overwork and stress is taking its toll. They often rail at her because they have to wait 3 months to get an appointment to have a growing lump checked out…

If we go to a VA or Medicare system, which I am enthusiastically all for, we will HAVE to fund and staff it to the hilt. Otherwise we will continue to screw over the least able to access care.

And I just do ‘t see the average selfish American shelling out more in the dreaded ‘taxes’ to let their trash collector or lawn guy or house cleaner access the same care as they do. And the idiots we sent to Washington will never have the balls to pass it over their constituents’ objections. Sad. And depressing.

All I can say is, thank God we can afford a good plan, and were able to find (through professional contacts) an insurance agent who knew how to navigate the Blue Cross website — as opposed to healthcare.gov. Cost of said plan, for a couple in mid 50s/ early 60s is not all that much less than our monthly mortgage… and is likely almost to equal that mortgage payment in 2016 when insurance premia increase. Furthermore, when we parsed the other plans available (is a “silver” plan really worthy of the name of a precious metal?) it was clear that all the doctors we wanted to see, only belonged to the network associated with the “gold” plan we have. We found out that in our state, most doctors belong to the Blue Cross PPO (associated only with gold plans) and don’t bother belonging to any others.

Again, this is a huge burden for us, but we shudder to think of those less fortunate and less educated than we are.

I recently needed a root canal with no endodontist (doctor who does the root canal) in my network. I found an out-of-network endodontist who did the root canal— on the wrong tooth, and charged me $1,000 for the privilege. Because he had no relationship with the diagnosing dentist he chose not to speak with his office before doing the root canal. Now I need a root canal on the tooth that originally needed it but my insurance coverage for the year has been used up. A new dental insurance company input an incorrect date of birth in their database. Despite correcting this the only endodontist in my area aside from the one who did the wrong tooth says that the dental insurance company (Cigna) is refusing coverage because of the incorrect birth date. I made the point that they aren’t refusing my premiums because of the incorrect DoB, only coverage. Did I mention that my health insurance premiums have tripled in two years in anticipation of the Obamacare ‘Cadillac tax?’

Lambert/others,

what is your overall opinion on the ACA, relative to pre-ACA status quo? For Actual Real Murican people (as opposed to health insurers, corrupt pols like 0bama, etc), is

1 ACA a net improvement for the health & financial worth of USian people

2 ACA is a net worsening for the health & financial worth of USian people

3 ACA’s net effect is unclear & TBD

If that Harvard Public Health study (Lambert cited in an article) were valid, the ACA reduces 60K yearly USian deaths due to not being able to afford healthcare, down to 30K USian deaths per year. Alternatively stated, the DC pols are in bipartisan agreement that the cartel profits of the Health Insurers is more important than USian lives. 0bama/Hellary with the ACA prefer to murder ~10X the USians annually that were murdered once in the Sep 11 Terist attack, whereas Jeb!/B0ner/ReThugz are more savage & prefer to massacre the equivalent of ~20X Sep 11s of USians annually. “Both Sides Do It”, in refusing to enact Medicare For All. But hey look over there at the relatively small time Boogey Men Du Jours like ISIS, who murder a handful of USians.

The ACA presumably is actually helping those with serious preexisting conditions, that refused to sell any “affordable” (by extortionist Exceptional TM Murican standards) or even flat refused at any price to sell any insurance to in the pre-ACA years.

OTOH, it seems a much larger number of USians in the Millions is facing the time tax, & ripoffs, that Lambert documents, in the ACA status quo. Are these money & time ripoffs even worse or less worse than the pre-ACA situation?

What is the status of life expectancy, health stats, obesity rate, cancer/heart disease/etc rates, US bankruptcies, medical bankruptices, median adult USian net worth, and has the ACA had any positive or negative effect on these stats?

I’d have to select #3, it is unclear to me if the ACA is a net benefit or net albatross. I’d love to read your opinion about this topic.

These are all good questions and I don’t think the answer exists. Furthermore, we don’t know the future.

In the short term, I’m guessing that ObamaCare, crapified as it is, has improved some people’s health care and saved some lives; a program that big could hardly fail to do so, no matter how poorly designed and implemented, and rentier-infested (and ObamaCare is all that). This is unexceptional, and I’ve said it all along. However, for any given individual — you, for example, or me — it’s still a crapshoot. To me, that’s just immoral.

In the medium to long-term, I think ObamaCare is very dangerous, because it sets the precedent for salivating neo-liberals that citizens can be forced into a market, and that paves the way for every government program to be a market. For example — speculating freely, I admit — I envisage a “Retirement Marketplace,” with “Social Security” as “the public option.”* I’d expect Social Security to collapse under such a program, and I would expect quality of life for elders, and life expectancy, to drop under such a program. And under all such programs. All features, of course, and not bugs.

* The website landing page might have a beautiful white ice floe on it, with pale blue accents. That blue the Democrats picked for their trade dress would be perfect. It’s so peaceful and reassuring.

It’s a very dangerous precedent to force people to buy a private for profit product period, even irregardless if it spreads to social security, medicare etc.. Conservatives were ultimately right on this (and many did object to this being forced to buy a product).

As for the long run I see positives of the ACA and negatives of the ACA as two lines graphed heading in opposite directions (and it’s not positives that is increasing). I can’t say when or if they will cross. Regardless of whether the contagion spreads to Social Security etc., even just the Cadillac tax which we know will hit will hurt some, even just the mergers of insurance companies (noone could deny at this point like big banks they are becoming too big to fail) has a lot of potential to hurt people, increasing the penalties if it is enacted will hurt some (and is there any limit to how much they can be increased – the ability to penalty is the ability to destroy), etc.. But it becomes hard to win an argument about the long run versus lives saved now.

NPR piece on Native Americans being nudged towards the ACA marketplaces.

Because

inadequate Indian Health Services budgetmarkets.the ACA takes the worst of of a NHS type program with the overhead of the previous private insurance racket, and institutionalizes it. More people may be “covered”, but less “care” is going on because costs have doubled, and bankruptcies and associated stress-related illnesses and deaths I’m sure aren’t being counted.

The ACA was designed to destroy the productive class, nothing more.

For my two cents: absolutely atrocious. We had the public will and the *ahem* Democratic numbers in Congress and the Presidency to pass some variation of universal healthcare.

The whole point of PPACA was to find a way for the political class to not pass universal healthcare without imploding the Democratic party. PPACA has set back American healthcare a decade at minimum, probably closer to two decades. And it has quite successfully created an overhang of ‘leftist’ leaning folks who now are reputationally and financially trapped into continuing to support PPACA indefinitely even if they may privately desire universal healthcare.

I would point out that I am talking in aggregate at a policy level. There are of course many individual winners, which is part of why PPACA was written with such complexity. It needed to have at least some clear winners so some of the results would be positive even if the aggregate is negative.

I choose door #2, socialism for insurance companies. Probably, in my opinion, it’s going to get worse before it gets better

I have always felt that if you are going to ‘improve’ some facet of the American life, you should use the best in the world as the example. In education that would have meant going to Finland, but except for teachers there wasn’t enough profit in it for people who have little interest in making sure that every child in American is educated. And so we get tests, vilification of those who know education best and are on the front lines of it and a destruction of their part of the industry as a job choice.

When we decided to address our expensive and wholly inadequate health care system did we look to the programs that provided the most health care efficiently and most affordably? No. Did we look to the universal system that had the best results and most respected by its ‘customers’? No. We took the most expensive and least effective version of universal health care to be found and stripped most of the controls that allowed it to be universal, somewhat effective and even remotely affordable from it. That the people who did this belonged to the party that was once the bastion of unions and the working class but now were more concerned with the profits of two of the biggest rentier industries in the country pretty much tells you how little thought was put to actually making sure those workers got healthcare at all, even less as to how they would struggle to pay those mandated premiums.

Frankly the continued claims by the President that this would eliminate medical bankruptcy in this country were galling. Why it would do it nationally when it hadn’t even reduced them by a significant amount in Massachusetts was beyond me, but then I’m just told I don’t understand the economics of it, How a program designed to rip almost 8% of a person’s income before taxes merely for a physical exam, demand thousands of out of pocket expenditures, massive co-pays, and with a significant portion of common drugs full price as they are not covered at all, lets not consider balanced billing, with the knowledge that the deductible and the premiums will NEVER go away year after year is affordable for an illness of any lengthy duration is of course beyond me. And as a supporter of Single Payer, I’m told I want unicorns and sparkle ponies. Somehow I think pot kettle black applies here.

Do we really know? No. But nothing I have seen, observed, nor the data indicates that this can be considered anything but number two – a net loss. Especially when the cadillac tax begins crapifying the employer provider insurance at an even greater rate then the greed of the insurance companies was doing it. Please do not forget that that coverage was supposedly part of the workers’ compensation – and now will cover less at a greater expense and the worker must put more of their cash income to make up the difference without getting a raise that will make up for that huge increase in their cost of living. And that group will grow every year. Nope – net loss.

It’s a minor point, signifying almost nothing, but during WWII there were regulations forbidding unions from asking for an increase in salary. I believe this is true from past reading, but I can’t provide a link.

These regulations did not prevent unions for asking for new fringe benefits, or an increase in those benefits, so instead of increased wages workers got company paid medical care. And so it goes.

They should have gone for more vacation time then (most of the rest of the world’s unions did and they have it now) or a reduced work week, at least we might still have it (or not). But raises will be inflated away in time and monetary benefits stolen I guess. But asking for more leisure time in WWII was probably also forbidden. How convenient war is … for the elite mostly.

It is still fun how right we were and how wrong every establishment Democratic politician and pundit was. PPACA was such a disaster we’re still talking about things we don’t know 7 years after the 2008 election. Our healthcare system remains the most wasteful and least universal in the entire industrialized world. Exactly as we said would be the case.

***

Slightly bigger picture, I find the Greek drachma and Medicare comparison very interesting. Medicare is no more capable right now of providing universal healthcare than Greece is of introducing its own currency. Both are things that would be phased in over time. Medicare needs all sorts of tweaks, from simple legislative things (like the age eligibility) to fundamental changes (like negotiating volume discounts with drug dealers, breaking up monopolistic hospital franchises, and deciding what exactly Medicare would pay for and how). Just to give a nonrandom example, how many existing relationships does Medicare have with abortion providers? Even Medicaid only covers abortion in the case of rape/incest or life of the mother.

The issue of immediate concern is what else to do. The focus of whether Grexit can or can’t be done is TINA in action. That’s what Firestone and others have continued to miss for years now in asserting knowledge of sovereign money as an answer when ignorance isn’t the problem. The issue isn’t the debt ceiling or the Greek currency unit or whatever other technical barriers are thrown out. It doesn’t matter whether Greece uses the euro, the dollar, the pound, the lira, the ruble, the renminbi, or a new drachma.

The issue is much more fundamental. What principles do we value as a society, and how do we elect leaders that will act based upon them? Medicare needs reform, Greeks need to decide whether to tax their oligarchs and bail out their banks or not, and high value platinum coins are irrelevant to a government that already spends every dollar it wants to.

These things are all related because they all get at the same core element of problem solving: you have to identify and understand the problem before you can design effective solutions. Otherwise you end up with solutions in search of a problem, like PPACA and Grexit and deficit spending.

Whocouldanode. The health insurance system, exactly like the payment system, is a power relation.

The power relation apparently now includes Native Americans among the uninformed and vulnerable as Indian Health Services morphs into Obamacare. Will the collateral loans of estate recovery be included in those Medicaid policies as well?

Under the Hyde Amendment, federal funds cannot be used to provide abortion services. Unless the Hyde Amendment were to be overturned, abortions would not be covered.

More generally, there currently are thousands of women of reproductive age on Medicare: those on SSI/SSDI. My sources tell me it is a huge pain in the neck for them to even get birth control prescriptions covered (despite that medication being used for many reasons beside contraception). So suddenly having millions of their age cohort on Medicare with the requirement that the Pill be covered (as is required under the ACA) would probably make at least that issue easier for them.

you will see people leaving america due to obamacare (actually, mandatory health sector extortion ).

To where? Inquiring minds want to know!

“Price sensitive consumers”? What a mealy-mouthed way of saying “people who can’t afford a better plan.” They make it sound like people are shopping for tvs or cars, instead of insurance that may determine whether they receive life-saving (or pain reducing, or quality of life-determining, or disability-avoiding) medical care.

And if that isn’t everything that’s wrong with the commodification of health care in a nutshell.