Yves here. This article is a sad vignette of how severely central bankers and many economic commentators, in this case one at Westpac, are locked into destructive orthodox thinking. The ECB’s unconventional monetary policy experiment has been an abject failure. And the reason should be obvious: businesses don’t borrow to expand just because money has gone on sale. They borrow to expand if they see an opportunity and if the cost of funding does not constrain the growth plan. The parties most likely to borrow just because money is cheap are the last ones you want to do that: financial speculators, since the cost of money is one of their biggest costs and zombie businesses, since they will borrow if they can to keep an otherwise failed venture going.

Notice also that Westpac, presumably following the ECB, views more consumer demand for credit as a good thing. Since more and more economic studies have found that borrowing by households is economically unproductive beyond a modest level, policymakers need to get over the wrongheaded idea that they should promote growth in consumer credit.

It is also bizarre to see what central bankers have rationalized or ignored in order to persist in increasingly counterproductive monetary experiments. For instance, super low interest rates drain demand by reducing incomes of savers and retirees. Yet the monetary authorities told themselves that pensioners would choose to spend their capital to maintain their lifestyles. That’s not what has happened. They’ve cut spending and even tried increasing saving to make up for lost returns. For the most part, the ones who have eaten into their nest eggs had no choice. Similarly, super low interest rates signal a lack of official confidence about the economy, and unprecedented monetary experiments are very disconcerting to many businessmen. If the officialdom is signaling deflationary risk, the rational response is to save, since goods and services will be cheaper later.

By David Llewellyn-Smith, founding publisher and former editor-in-chief of The Diplomat magazine, now the Asia Pacific’s leading geo-politics website. Originally posted at MacroBusiness

From Westpac’s Elliot Clarke

A key purpose behind the ECB’s alternative easing programs has been to materially improve credit provision and conditions in the Euro Area economy. Exhibiting a lagged relationship with the business cycle and further hampered by the health of European banks, success on this front has been slow and limited.

As referenced in their most recent policy statement, “loan dynamics followed the path of gradual recovery observed since the beginning of 2014”. However, that has only left annual growth in loans to non-financial corporates and households at 1.9%yr and 1.8%yr respectively at September 2016.

These are hardly strong outcomes and, of late, there has been a clear lack of momentum, meaning further material gains are unlikely for the forseeable future. Indeed, from the detail of the ECB’s own bank lending survey, there is evidence to suggest credit growth is set to slow.

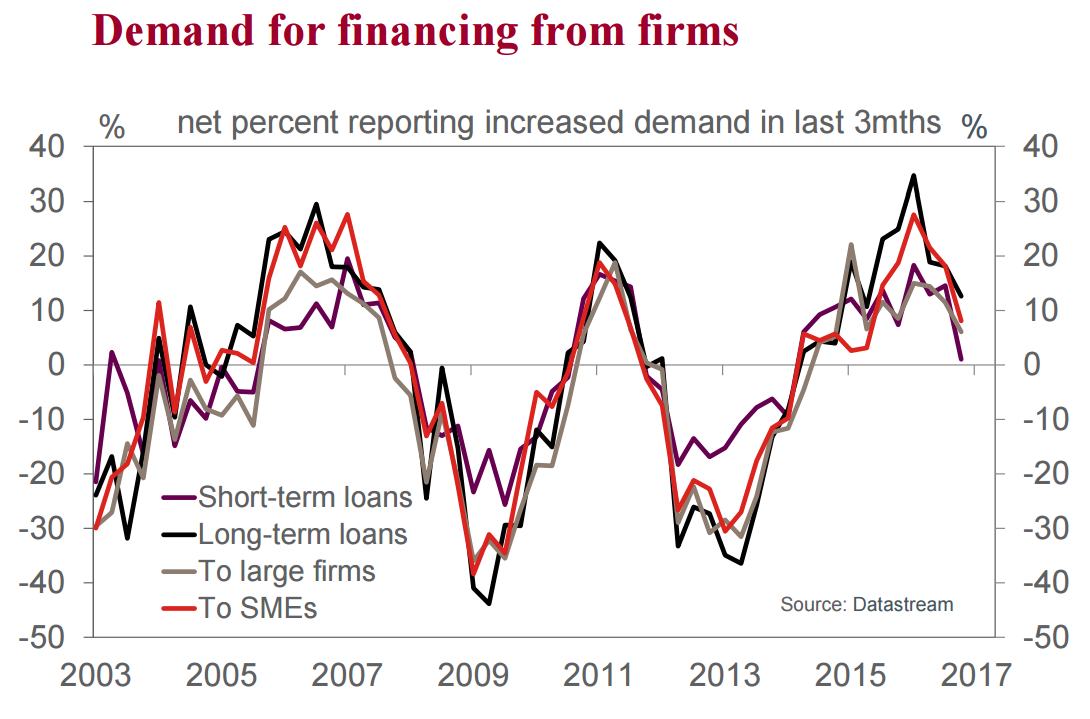

Starting with non-financial corporates, the ECB survey reports that there is a clear downtrend in current credit demand, with the net per cent of respondents reporting increased demand for credit from firms having peaked in the first quarter of 2016 and consistently declined ever since.

Expectations of future growth in non-financial corporate loan demand is also in a clear downtrend. Importantly, the peak in the expected series came in mid-2015 (six months ahead of the actual series’ peak) and has endured. It should be noted though that the expected series peaked at a high level and is still consistent with positive credit growth – so we are not anticipating an outright contraction in new lending.

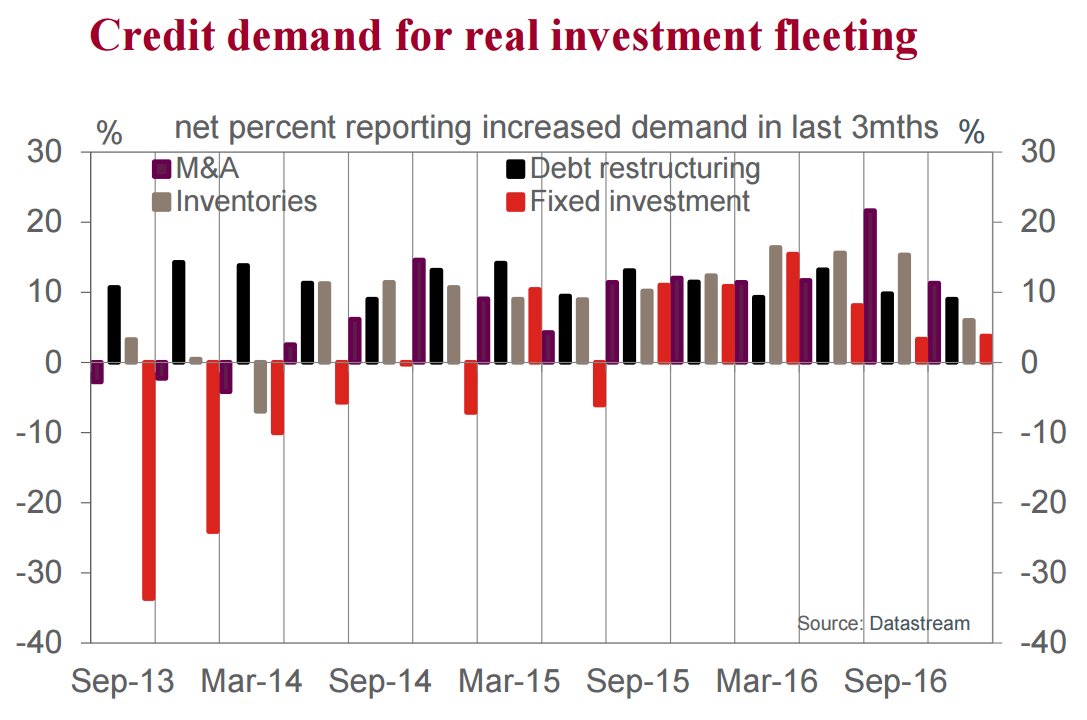

The purpose for new loans for corporates also remains unhelpful to the growth outlook for the real economy. Having improved from mid-2015 to early 2016, the six months to October saw demand for credit to fund fixed asset investment abate.

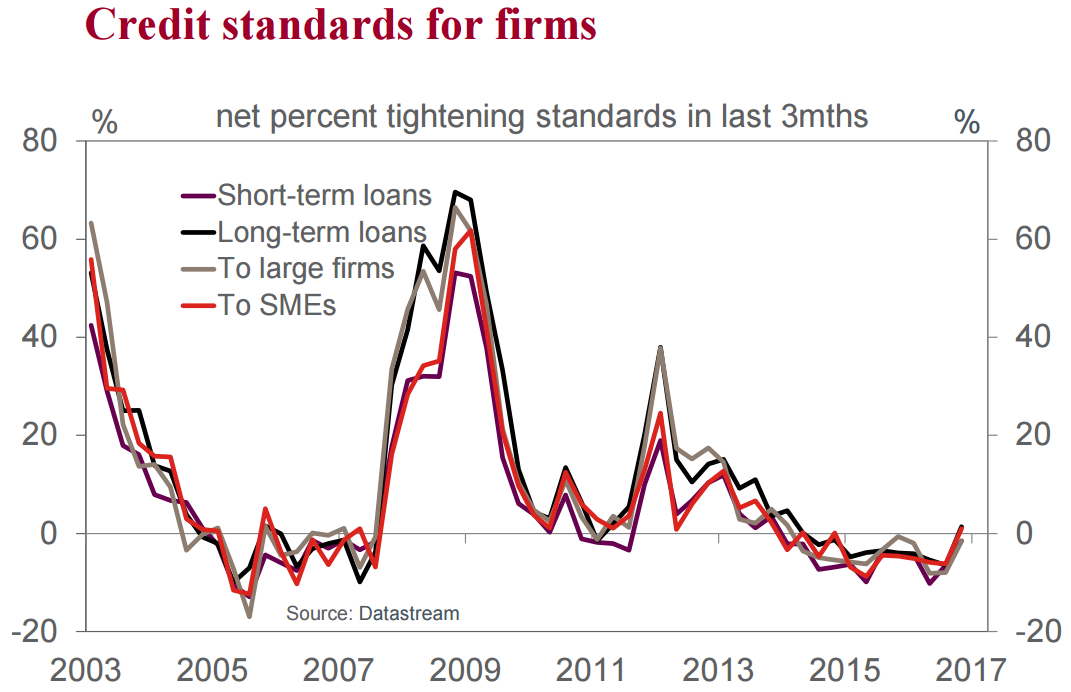

Ergo, after a prolonged contraction to mid-2015, it seems a recovery in real investment has failed to launch. This is partly attributable to a lack of confidence in the outlook. But it has also come as a result of loan conditions for firms remaining tight. The ECB’s survey suggests conditions have only improved incrementally since mid-2014.

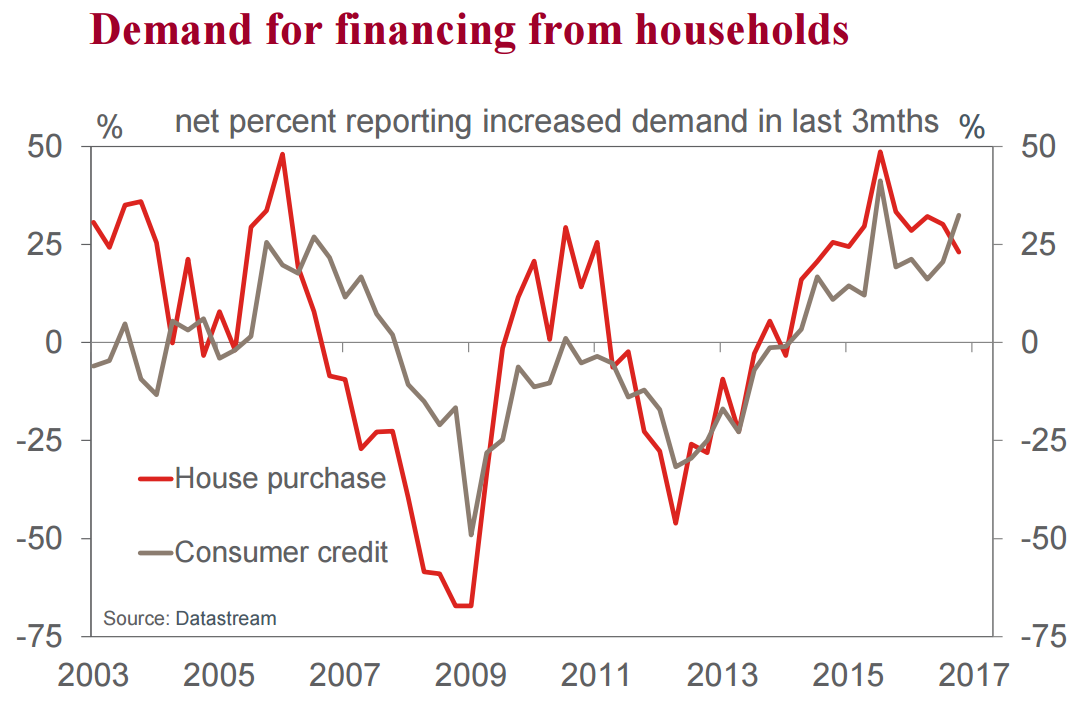

The above results imply only limited support to job creation and therefore to household incomes. It is unsurprising then that growth in credit to households also looks to be peaking at a fairly modest pace relative to history.

As for non-financial corporates, households in the Euro Area are clearly benefitting from lower interest rates. Yet the overall credit conditions they are currently experiencing are little changed from a year ago, or indeed late-2013. Note that since end-2013, the average percentage of banks reporting an easing in standards for mortgages and consumer credit has been 2% and 3% respectively. In the three years prior, an average of 14% and 6% of respondents reported tighter conditions each quarter.

The above analysis does not, of itself, justify the ECB continuing its asset purchases well beyond March 2017 – there are many market and political points that also need to be considered. But it does suggest that credit provision in the Euro Area is not yet self sustaining. Without the ECB’s support, the Euro Area’s economy; banks; and financial markets will be left in a fragile state, susceptible to any and all economic or financial shocks.

Add the political strife building across the Continent that is threatening further eurozone fracturing with the Italian referendum in December, Netherlands election in March, French election April-May, German election in September then Italy six months later and there is no way that the ECB can allow economic weakness and/or peripheral funding stress to creep back in.

Can we assume, then, that the PM sector is a good bet right now?

Disturbed Voter

Only gamblers bet. Precious metals hold up only on the very long term … longer than you have left to live. The end of the Roman Empire was good for gold, because a lot of it moved from Roman to Germanic pockets (and to the Huns while they were a threat). But “Roman Lives Matter” was a short lived Twitter storm. Like Secretary Mellon proposed under Hoover … “liquidate everything” was the policy.

Jim Haygood

Gold’s near-zero correlation to stocks is not a gamble. It’s a structural feature that’s useful in portfolio construction, given that too many asset classes ARE correlated to stocks.

While on its own gold could be called a speculation, in a portfolio context it is not. Red line in this chart is gold’s one-year rolling correlation to the S&P 500 index:

Gold measured in Euros has been in a bull market for quite some time now, and if they continue to print, PMs don’t seem like much of a gamble.

Robert NYC

Since 1971, the dollar has lost about 97% of its value versus Gold, around 85% of value versus the Swiss franc and approximately 75% of value versus the yen. The tells you about all you need to know about America’s problems with inequality and stagnant incomes. A bad monetary system produces a bad economic system, and that erodes the foundations of a society.

Tinky

Yes, you can. And ignore those who claim, nonsensically, that it will take many years, let alone decades (lol!) for a significant rise in value to occur.

Pepe Aguglia

Fed tightening cycle is a headwind for PMs. Not saying it is the overriding factor but it’s something to keep in mind in terms of timing entry points.

Lord Koos

Yeah, that coming-someday .25% rate increase will be a huge headwind.

BecauseTradition

Gold’s current price is surely based on, to a significant extent:

1) the obvious, on-going failures of the current fiat and credit system.

2) the hope that we’ll return to a gold standard – as if that’s the only conceivable alternative to the current system.

And imagine the environmental damage (e.g. to the Amazon jungle) if we did return to a gold standard as people, especially the poor, rush to mine money?

Still, if one knew when to get off the bus then even “Cabbage Patch Dolls” were a good “investment.”

EndOfTheWorld

A full blown gold standard may not be the only possible alternative, but gold is likely to be at least PART OF whatever alternative system (e.g. special drawing rights). Right?

Sound of the Suburbs

Central Banks using monetary policy to control economies is just a bad idea.

Compared to the FED and ECB, the BoE is doing well but that isn’t saying much.

Many years ago when Alan Greenspan first proposed using monetary policy to control economies, the critics said this was far too broad a brush.

After the dot.com crash Alan Greenspan loosened monetary policy to get the economy going again. The broad brush effect stoked a housing boom.

When he tightened interest rates, to cool down the economy, the broad brush effect burst the housing bubble. The teaser rate mortgages unfortunately introduced enough of a delay so that cause and effect were too far apart to see the consequences of interest rate rises as they were occurring. The end result 2008.

With the Euro-zone, the Germans were the first ones to go bubble crazy over the dot.com boom and their version of the NASDAQ collapsed by 97% in the bust.

To help Germany, the ECB lowered interest rates and blew bubbles in the Club-Med nations that burst when the Euro-zone crisis hit.

The low interest rates didn’t actually encourage the German’s to borrow as they had just had their fingers burnt with the dot.com bust and they were busy repairing their balance sheets.

The recessionary atmosphere in Germany allowed them to press ahead with labour reform.

The Club-Med nations and Ireland couldn’t resist the low interest rates and started borrowing heavily. This new debt created new money which increased the money supply.

With more money around wages rose and labour quietly became more uncompetitive, un-noticed in the boom of low interest rates, mass borrowing and mass money creation.

From 55 mins. – Explanation of ECB action to help Germany

The broad brush of monetary policy being applied to the divergent economies of Euro-zone was a disaster waiting to happen. It was never going to work and its problems have already manifested themselves in the housing bubbles of Greece, Spain, Holland and Ireland when trying to help Germany with low interest rates.

Holland desperately tries to keep its housing bubble inflated and avoid the fate of Ireland, Spain and Greece.

The broad brush of monetary policy also divided the Euro-zone’s labour market, making German labour more competitive and Club-Med nations labour less competitive.

The Euro-zone is suffering from problems caused by the dot.com crash and broad brush Central Bank monetary policy, these problems only manifested themselves much later after the next big crash in 2008.

Trying to solve these problems now, 16 years later, is proving very difficult indeed, especially using the broad brush of monetary policy that failed so miserably all those years ago.

The targeted solutions that were used in the past seem far more sensible than the broad brush of monetary policy and the evidence is becoming over-whelming for even the most hardened ideologue.

Keep throwing more money at it Mario, we have no idea how to fix the Euro.

Targeted solutions are best, but we don’t have one.

RBHoughton

So every government in Europe and North America is playing Nero?

Surely someone somewhere can save the economy. What does Stiglitz and Ha Jun Chang have to say?

Paul Morphy

At some point interest rates will have to rise. With more and more debt being having been accumulated the effect of rising interest rates will be felt more sharply and more quickly than the last time.

The accumulation of indebtedness makes it more necessary for central banks to keep interest rates lower for longer.

Sure central banks can try to keep interest rates at super low levels. But the real question is for how long more can central banks do this? Super low interest rates are bad for savers. Super low interest rates make it harder for insolvent retail banks to make profits/reduce losses.

Central banks and their bankers have backed themselves in to a corner from which it is hard to see an exit.

jsn

The only way out for central banks is to allocate losses somewhere.

Having already lain waste to the working class and the lower tiers of the managerial class, expect “innovative”, “disruptive” and “transformative” new grifts to move the looting up the class ladder.

So long as the PTB can get away with looting the weak to protect the plutocracy, they will. As we’ve seen with CETA, TPP, Greece and Cypress, no amount of popular will expressed through legitimate means will stand in their way.

Lord Koos

I guess that leaves only illegitimate means then?

RMO

How many savers are there really? Just curious because of the stats showing what a huge percentage of the U.S. population wouldn’t be able to come up with a fairly small sum of money for an unexpected expense.

Heaven forbid that the EU and many of the other western economies actually try something like stimulus spending and programs to get money into the hands of people who will actually spend it on real goods and services. It shows how screwed up things are when a policy that has worked extremely well in practice has been tossed down the memory hole.

Sound of the Suburbs

It’s been eight years since 2008 and the global economy hasn’t recovered.

He gives graphs of bank reserves and shows the ridiculous surplus the BoE, BoJ, FED and ECB have created.

It’s not working because people aren’t borrowing.

The QE money just stays in the financial system and doesn’t enter the real economy this is why inflation figures are so low around the world.

These excesses in bank reserves are going into financial speculation, blowing bubbles and leading us into the next crash.

Fiscal policy is the answer.

Perhaps we should all listen to the man Ben Bernanke listened to, Richard Koo:

(Video link above, to understand it you need to understand money BoE link below.)

He explains the mistake Christina Romer made analysing data from the Great Depression leading Central Banks to think they could get us over 2008 with monetary policy.

In the first 12 mins.

At 54 mins. you can see the IMF projection for Greek recovery with austerity and see the horrifying reality.

When the US was panicking about the fiscal cliff it was because Ben Bernanke had read Richard Koo’s book and knew cutting Government spending would drive the US economy into recession.

The secret is in how money works, which is why hardly any economists understand either the problem or the solution.

Money and debt are opposite sides of the same coin.

If there is no debt there is no money.

Money is created by loans and destroyed by repayments of those loans.

After the system has been flooded with lots of debt with a nice housing boom, the bust gets everyone paying down debt and not borrowing.

This makes the money supply contract making it harder to pay down the debt.

When the repayments are larger than the new debt being taken on, the money supply starts contracting.

This is what needs to be analysed, is the aggregate debt within the banking system growing or shrinking?

The money supply follows this exactly.

The Government needs to step in as the borrower of last resort to keep the money supply stable, otherwise you head into a deflationary spiral.

Austerity is the worst thing you can do in a balance sheet recession.

The Club-Med nations aren’t going to get any better with austerity, cutting Government spending and borrowing just accelerates the contraction of the money supply.

Robert NYC

Unfortunately after you create this mountain debt there is no way out of it short of some type of monetary catastrophe. Deflation is the natural course of events in such a scenario but utterly unacceptable to the rich and powerful since it will wipe out so much wealth. Much of that wealth is bogus of course since it resulted from all the debt/money creation and is therefor just the other side of the debt. The authorities have succeeded in staving off a collapse for the time being but this can’t go on for ever and it’s not going to miraculously correct itself.

This is a major period of monetary history with far reaching and profound consequences. Nobody knows what comes next but it is unlikely to be pleasant.

Jim Haygood

A more compassionate term for the eurozone would be CLE — Countries Living with Eurosclerosis.

No cure is known. But palliative measures can keep patients comfortable during their prolonged sunset.

Carey

What if… the PTB do in fact know *exactly* what they’re doing? This thinking does

require a different frame. Their policies seem to be working quite well for some.

Synoia

Look at austerity, and consider the major looser in the war of austerity, demand suppression, is China, manufacturer to the world, and challenger for the position of “world leader.”

Then reflect on who is winning and who is losing.

A similar analyst in the MENA (Middle East North Africa) results in a different view of the world (The Russians are very vulnerable to Muslim discontent, as happened in Chechnya). Who benefits from the chaos?

Hint: It is probably a county where there is an insignificant Muslim population, and large barriers to hordes of refugees arriving on the country’s border.

Temporarily Sane

Ah yes, the savage Muslim hordes who bring down entire nation states with worrying frequency. Remind me again how many governments the great Muslim empire has overthrown or critically destabilized since WW2? What, with their dysfunctional banking practices currently creating oligarchies in the west and history of fighting or fueling covert, overt and proxy wars around the world in the name of “regime change” that have killed millions….why that must be a long list indeed.

Don’t forget the crippling economic sanctions these animals placed on Iraq that killed ~ 500k children and the sanctions still in place against Syria preventing food and medicine from reaching civilians. Someone needs to come up with a solution to sort these barbarians out once and for all!

It is instructive to see how the fear and uncertainty that thrives in hard economic times combined with the rhetoric of paranoid or conniving public figures and celebrities has resulted in many westerners casually embracing bigotry and even hate without much, if any, self-reflection.

They are so busy scaring themselves with delusional fantasies that conveniently “explain” all the problems of the world and heaps them upon the shoulders of that big glop of shapeless evil known as “the Muslims”…that they don’t notice the actual culprits looting, pundering and killing right in front of them.

There is an ancient Chinese saying that goes: “The person who does not know of what s/he speaks needs to STFU” Or maybe that was Wittgenstein. Anyway, the message is clear enough.

As for your “countries” that benefit from the current geopolitical order…if you mean the US, Canada or Australia, think again. How is the average non-billionaire faring in these places? Healthy and vibrant middle-class, good wages, stable economy and a bright future, right?

I leave you to ponder the practical wisdom contained in this succinct gem of a quote:

“Better to keep your mouth shut and let people think you are a fool than to open it and remove all doubt.”

– Dan Quayle

DarkMatters

OK, at the risk of removing all doubt, an attempt at clarification:

“Savage Muslim Hordes”, aka Saudi-financed Wahabbism, vetoed by violence social progress in Afghanistan (from the late ’70’s on); destabilized eastern Africa; then migrated to former Yugoslavia to exacerbate ethnic tensions and aid in national disintegration there; then toppled Qaddafi and destroyed an arguably prosperous society in Libya; exported from that country jihad to Mali and arms to Syria, which country their brethren were already trying to destabilize and take over. And then we have Yemen.

I agree with your assessment that western financial oligarchies did produce and support much of the preceding chaos. They provided military and diplomatic support, and their agents wrecked Iraq pretty much on their own. But we shouldn’t ignore the role of the middle-eastern financial oligarchy either. Currently, occasional evidence of their briberies reported in western governments raises the issue as to exactly which agenda is being promoted in this sinister collaboration.

Chauncey Gardiner

Bingo!… Based on the ECB, BOJ and Fed monetary policies over the past three decades, I think we should be looking at all Western central banks through a different lens than their legislative mandates. The long-term decline in the velocity of M2 money is the tell of massive policy failure (or success, depending on your view regarding concentration of wealth).

It has become clear that their suppression of interest rates to negative real levels by pushing bond prices ever upward through their unrelenting bond purchases primarily benefit legacy bondholders, the stock market indexes, highly debt-leveraged financial entities, and large speculators.

50 years from now (assuming humanity survives the reign of the US neocons), I expect this era will be known as “The Age of the Central Bankers”; just as the late 13th Century in feudal Germany and the late 1800’s in the U.S. both became known as “The Age of the Robber Barons”, and for similar reasons.

RBHoughton

Agreed. Central Banks belong to a system that no longer works – abandon them.

We need a means of exchange that is based in reality not the silly policies of “independent” banksters.

Les Swift

My suspicion has long been that the plan is not some endless propping up of the system, but rather keeping it going while structural changes are made. On the financial front, that involves downsizing the operations of the institutions, and dealing with bad assets through a combination of letting them mature and writing them down. On the political front, it involves replacing elected representative government with technocratic governance, as we see fairly openly in Europe, and in a more disguised form, in the U.S. That is, the West is shifting to a political system deemed more suited to enforcing austerity when the music stops. The extend-and-pretend, money-pumping schemes help accomplish this overall goal.

Each financial crisis seems to result in an increase of technocratic power. This has been visible in Europe, where each national crisis results in further concession by national governments to the supranational powers. It is also visible in the “global solutions to global problems” approach to coordinated international regulation in the post-2008 period.

Synoia

Each financial crisis seems to result in an increase of technocratic power.

Rule by banker, wedded to their dogma of “more debt is good for you,” and guided by their Priests (Economists), all worshiping at the altar of Greed.

It is a cult.

BecauseTradition

If the definition of “citizen” includes being able to deal directly with her/his nation’s fiat then depository institutions are citizens and we, the general public are not.*

So I reckon the US has about 6,000 citizens in total.

*Unless one includes the ability to deal with unsafe, inconvenient, perhaps soon to be abolished physical fiat, a.k.a. “cash”.

Plenue

I’m always in awe of economists and their complete inability to grasp the most basic of concepts. So much about being a professional economist seems to be about learning to turn off parts of your brain. Businesses aren’t expanding because they have no reason to do so. If anything they’re shrinking. Why? Because nobody has any money! And what money they do have they’re using to pay down debts, not go out an buy fancy bullshit.

Here’s another simple, and related, concept 99% of economists don’t understand: “Debts that can’t be repaid, won’t be.” If the only way for people to get more money is to go further into debt, it’s an endless spiral down. How does it end? Probably with a lot of economists heads of pikes.

John Bougearel

Missing from this commentary is draghi’s rationale for these asset purchases to reach the near 2% inflation target yet after 18 months the EU inflation rate is stuck at .4% there is no evidence that asset purchases stimulate any uptick in inflation The disconnect between the ECB’s QE policies and the inflation rate is glaring so methinks the near 2% inflation raterationale is being used as cover for these highly flawed asset purchases by the ECB

I neglected to make the VERY important point that QE is NOT “printing”. It does not increase the money supply. It is an asset swap. ECB buys bonds. Investors get cash but they want to hold securities, so they go buy new securities. It does not create new cash system wide. Deficit spending would do that.

BecauseTradition

I neglected to make the VERY important point that QE is NOT “printing”. It does not increase the money supply. It is an asset swap. ECB buys bonds. Investors get cash but they want to hold securities, so they go buy new securities. It does not create new cash system wide. Yves Smith [bold added]

That depends, doesn’t it? If the asset seller is a bank, for example, then only bank reserves increase and those aren’t part of the money supply since the public is not allowed accounts at the central bank. But if the asset seller is a non-bank member of the private sector then bank deposits (liabilities) increase too and those are part of the money supply. Yes, those deposits can be used to buy new securities but that just moves the deposits around without decreasing the money supply – unless the new securities are bought from a bank; which, come to think of it, they probably often are.

Deficit spending would do that. Yves Smith

Yes, since that increases both bank reserves (not part of the money supply) and bank deposits (part of the money supply).

Btw, it appears that QE is just a way to give the rich more money by allowing them to act as middlemen between bond sellers and the central bank. For shame!

Robert NYC

QE is printing and all claims to contrary have been thoroughly refuted. The Bank of England and others have done multiple studies on this and QE asset purchases do in fact inflate both the base money and M1 money supply. It is easy to prove this point by setting up three simple t-account to see the transmission mechanism. The money that is created does not make it way to the broader public though and this is a problem. It is also why helicopter money will make its appearance at some point because that way they can distribute the money more broadly.

The more important point is that the monetary system is a disaster due to incompetent management of the system. All money is debt, an esoteric point that few people understand including most economists. The secret to running a healthy fiat based monetary system is to limit the rate of credit expansion to the growth of the real economy. It’s basically that simple and the authorities utterly failed in this regard by allowing credit to expand at rate well in excess of real economic growth. Excess credit creation brings consumption forward, leads to speculation and asset price inflation leaving behind a mountain of debt and the associated financial claims on the real economy. It is quite literally a recipe of destroying an economy and the underling society. And voila look where we are!

BecauseTradition

The secret to running a healthy fiat based monetary system is to limit the rate of credit expansion to the growth of the real economy. Robert NYC

But deficit spending can drive real economic growth too and without increasing private debt*.

So how about this? Let creditors create all the new deposits/liabilities they dare but let’s make sure those liabilities are genuine liabilities and not largely a sham wrt to the general population as they are today.** In other words, let’s give honest accounting a chance?

*Ideally the “debt” of the monetary sovereign should always grow but:

1) It need not and should not pay positive interest to avoid welfare proportional to wealth.

2) The rate of growth should not cause excessive price inflation.

**This will be 100% evident if physical fiat is abolished since then a member of the general public will be literally unable to use his/her nation’s fiat AT ALL!

BecauseTradition

It is also why helicopter money will make its appearance at some point because that way they can distribute the money more broadly.

Yes, and please note that the proper abolition of government provided deposit insurance should require the distribution of huge amounts of new fiat to provide the new reserves needed for the transfer of at least some currently insured deposits to inherently risk-free accounts at the central bank itself or equivalent.*

*e.g. A Postal Checking Service that was forbidden by law from lending.

BecauseTradition

All money is debt,

If Equity is debt then I agree but it isn’t so I don’t. ;)

an esoteric point that few people understand including most economists.

Basic accounting should be a REQUIRED course in economics.

Robert NYC

Why do you keep repeating this nonsense? There are multiple studies showing the QE does increase the money supply. Here is just one.

And if you don’t want to believe the Bank of England’s technical staff, I suggest you sit down and draw a few T-acconts and trace it through for yourself. You seem to labor under the mistaken impression that when a central bank buys bonds from a constituent bank that is the end of the story. It’s not. The banks then move to restore the earnings from those lost securities by buying bonds from the public sector. They do this by creating new deposits from nothing and the money supply increases as simple as that. Investors then buy bonds to replace those that were sold which forces up assets prices. As for the new deposits, they stay in the banking system and slosh around in the repo markets.

And if you still don’t understand this just go the FRED data base and plot QE versus M1. I would embed the chart here but you can’t display gifs in these text boxes. With all due respect you really need to study up on the monetary system because it is clear you don’t have a proper understanding of how it works.

Can we assume, then, that the PM sector is a good bet right now?

Only gamblers bet. Precious metals hold up only on the very long term … longer than you have left to live. The end of the Roman Empire was good for gold, because a lot of it moved from Roman to Germanic pockets (and to the Huns while they were a threat). But “Roman Lives Matter” was a short lived Twitter storm. Like Secretary Mellon proposed under Hoover … “liquidate everything” was the policy.

Gold’s near-zero correlation to stocks is not a gamble. It’s a structural feature that’s useful in portfolio construction, given that too many asset classes ARE correlated to stocks.

While on its own gold could be called a speculation, in a portfolio context it is not. Red line in this chart is gold’s one-year rolling correlation to the S&P 500 index:

Gold measured in Euros has been in a bull market for quite some time now, and if they continue to print, PMs don’t seem like much of a gamble.

Since 1971, the dollar has lost about 97% of its value versus Gold, around 85% of value versus the Swiss franc and approximately 75% of value versus the yen. The tells you about all you need to know about America’s problems with inequality and stagnant incomes. A bad monetary system produces a bad economic system, and that erodes the foundations of a society.

Yes, you can. And ignore those who claim, nonsensically, that it will take many years, let alone decades (lol!) for a significant rise in value to occur.

Fed tightening cycle is a headwind for PMs. Not saying it is the overriding factor but it’s something to keep in mind in terms of timing entry points.

Yeah, that coming-someday .25% rate increase will be a huge headwind.

Gold’s current price is surely based on, to a significant extent:

1) the obvious, on-going failures of the current fiat and credit system.

2) the hope that we’ll return to a gold standard – as if that’s the only conceivable alternative to the current system.

And imagine the environmental damage (e.g. to the Amazon jungle) if we did return to a gold standard as people, especially the poor, rush to mine money?

Still, if one knew when to get off the bus then even “Cabbage Patch Dolls” were a good “investment.”

A full blown gold standard may not be the only possible alternative, but gold is likely to be at least PART OF whatever alternative system (e.g. special drawing rights). Right?

Central Banks using monetary policy to control economies is just a bad idea.

Compared to the FED and ECB, the BoE is doing well but that isn’t saying much.

Many years ago when Alan Greenspan first proposed using monetary policy to control economies, the critics said this was far too broad a brush.

After the dot.com crash Alan Greenspan loosened monetary policy to get the economy going again. The broad brush effect stoked a housing boom.

When he tightened interest rates, to cool down the economy, the broad brush effect burst the housing bubble. The teaser rate mortgages unfortunately introduced enough of a delay so that cause and effect were too far apart to see the consequences of interest rate rises as they were occurring. The end result 2008.

With the Euro-zone, the Germans were the first ones to go bubble crazy over the dot.com boom and their version of the NASDAQ collapsed by 97% in the bust.

To help Germany, the ECB lowered interest rates and blew bubbles in the Club-Med nations that burst when the Euro-zone crisis hit.

The low interest rates didn’t actually encourage the German’s to borrow as they had just had their fingers burnt with the dot.com bust and they were busy repairing their balance sheets.

The recessionary atmosphere in Germany allowed them to press ahead with labour reform.

The Club-Med nations and Ireland couldn’t resist the low interest rates and started borrowing heavily. This new debt created new money which increased the money supply.

With more money around wages rose and labour quietly became more uncompetitive, un-noticed in the boom of low interest rates, mass borrowing and mass money creation.

Richard Koo goes into the details:

https://www.youtube.com/watch?v=8YTyJzmiHGk

From 55 mins. – Explanation of ECB action to help Germany

The broad brush of monetary policy being applied to the divergent economies of Euro-zone was a disaster waiting to happen. It was never going to work and its problems have already manifested themselves in the housing bubbles of Greece, Spain, Holland and Ireland when trying to help Germany with low interest rates.

Holland desperately tries to keep its housing bubble inflated and avoid the fate of Ireland, Spain and Greece.

The broad brush of monetary policy also divided the Euro-zone’s labour market, making German labour more competitive and Club-Med nations labour less competitive.

The Euro-zone is suffering from problems caused by the dot.com crash and broad brush Central Bank monetary policy, these problems only manifested themselves much later after the next big crash in 2008.

Trying to solve these problems now, 16 years later, is proving very difficult indeed, especially using the broad brush of monetary policy that failed so miserably all those years ago.

The targeted solutions that were used in the past seem far more sensible than the broad brush of monetary policy and the evidence is becoming over-whelming for even the most hardened ideologue.

Keep throwing more money at it Mario, we have no idea how to fix the Euro.

Targeted solutions are best, but we don’t have one.

So every government in Europe and North America is playing Nero?

Surely someone somewhere can save the economy. What does Stiglitz and Ha Jun Chang have to say?

At some point interest rates will have to rise. With more and more debt being having been accumulated the effect of rising interest rates will be felt more sharply and more quickly than the last time.

The accumulation of indebtedness makes it more necessary for central banks to keep interest rates lower for longer.

Sure central banks can try to keep interest rates at super low levels. But the real question is for how long more can central banks do this? Super low interest rates are bad for savers. Super low interest rates make it harder for insolvent retail banks to make profits/reduce losses.

Central banks and their bankers have backed themselves in to a corner from which it is hard to see an exit.

The only way out for central banks is to allocate losses somewhere.

Having already lain waste to the working class and the lower tiers of the managerial class, expect “innovative”, “disruptive” and “transformative” new grifts to move the looting up the class ladder.

So long as the PTB can get away with looting the weak to protect the plutocracy, they will. As we’ve seen with CETA, TPP, Greece and Cypress, no amount of popular will expressed through legitimate means will stand in their way.

I guess that leaves only illegitimate means then?

How many savers are there really? Just curious because of the stats showing what a huge percentage of the U.S. population wouldn’t be able to come up with a fairly small sum of money for an unexpected expense.

Heaven forbid that the EU and many of the other western economies actually try something like stimulus spending and programs to get money into the hands of people who will actually spend it on real goods and services. It shows how screwed up things are when a policy that has worked extremely well in practice has been tossed down the memory hole.

It’s been eight years since 2008 and the global economy hasn’t recovered.

Central bank monetary policy is not the answer.

All explained by Richard Koo:

https://www.youtube.com/watch?v=8YTyJzmiHGk

He gives graphs of bank reserves and shows the ridiculous surplus the BoE, BoJ, FED and ECB have created.

It’s not working because people aren’t borrowing.

The QE money just stays in the financial system and doesn’t enter the real economy this is why inflation figures are so low around the world.

These excesses in bank reserves are going into financial speculation, blowing bubbles and leading us into the next crash.

Fiscal policy is the answer.

Perhaps we should all listen to the man Ben Bernanke listened to, Richard Koo:

(Video link above, to understand it you need to understand money BoE link below.)

He explains the mistake Christina Romer made analysing data from the Great Depression leading Central Banks to think they could get us over 2008 with monetary policy.

In the first 12 mins.

At 54 mins. you can see the IMF projection for Greek recovery with austerity and see the horrifying reality.

When the US was panicking about the fiscal cliff it was because Ben Bernanke had read Richard Koo’s book and knew cutting Government spending would drive the US economy into recession.

The secret is in how money works, which is why hardly any economists understand either the problem or the solution.

Money and debt are opposite sides of the same coin.

If there is no debt there is no money.

Money is created by loans and destroyed by repayments of those loans.

From the BoE:

http://www.bankofengland.co.uk/publications/Documents/quarterlybulletin/2014/qb14q1prereleasemoneycreation.pdf

After the system has been flooded with lots of debt with a nice housing boom, the bust gets everyone paying down debt and not borrowing.

This makes the money supply contract making it harder to pay down the debt.

When the repayments are larger than the new debt being taken on, the money supply starts contracting.

This is what needs to be analysed, is the aggregate debt within the banking system growing or shrinking?

The money supply follows this exactly.

The Government needs to step in as the borrower of last resort to keep the money supply stable, otherwise you head into a deflationary spiral.

Austerity is the worst thing you can do in a balance sheet recession.

The Club-Med nations aren’t going to get any better with austerity, cutting Government spending and borrowing just accelerates the contraction of the money supply.

Unfortunately after you create this mountain debt there is no way out of it short of some type of monetary catastrophe. Deflation is the natural course of events in such a scenario but utterly unacceptable to the rich and powerful since it will wipe out so much wealth. Much of that wealth is bogus of course since it resulted from all the debt/money creation and is therefor just the other side of the debt. The authorities have succeeded in staving off a collapse for the time being but this can’t go on for ever and it’s not going to miraculously correct itself.

This is a major period of monetary history with far reaching and profound consequences. Nobody knows what comes next but it is unlikely to be pleasant.

A more compassionate term for the eurozone would be CLE — Countries Living with Eurosclerosis.

No cure is known. But palliative measures can keep patients comfortable during their prolonged sunset.

What if… the PTB do in fact know *exactly* what they’re doing? This thinking does

require a different frame. Their policies seem to be working quite well for some.

Look at austerity, and consider the major looser in the war of austerity, demand suppression, is China, manufacturer to the world, and challenger for the position of “world leader.”

Then reflect on who is winning and who is losing.

A similar analyst in the MENA (Middle East North Africa) results in a different view of the world (The Russians are very vulnerable to Muslim discontent, as happened in Chechnya). Who benefits from the chaos?

Hint: It is probably a county where there is an insignificant Muslim population, and large barriers to hordes of refugees arriving on the country’s border.

Ah yes, the savage Muslim hordes who bring down entire nation states with worrying frequency. Remind me again how many governments the great Muslim empire has overthrown or critically destabilized since WW2? What, with their dysfunctional banking practices currently creating oligarchies in the west and history of fighting or fueling covert, overt and proxy wars around the world in the name of “regime change” that have killed millions….why that must be a long list indeed.

Don’t forget the crippling economic sanctions these animals placed on Iraq that killed ~ 500k children and the sanctions still in place against Syria preventing food and medicine from reaching civilians. Someone needs to come up with a solution to sort these barbarians out once and for all!

It is instructive to see how the fear and uncertainty that thrives in hard economic times combined with the rhetoric of paranoid or conniving public figures and celebrities has resulted in many westerners casually embracing bigotry and even hate without much, if any, self-reflection.

They are so busy scaring themselves with delusional fantasies that conveniently “explain” all the problems of the world and heaps them upon the shoulders of that big glop of shapeless evil known as “the Muslims”…that they don’t notice the actual culprits looting, pundering and killing right in front of them.

There is an ancient Chinese saying that goes: “The person who does not know of what s/he speaks needs to STFU” Or maybe that was Wittgenstein. Anyway, the message is clear enough.

As for your “countries” that benefit from the current geopolitical order…if you mean the US, Canada or Australia, think again. How is the average non-billionaire faring in these places? Healthy and vibrant middle-class, good wages, stable economy and a bright future, right?

I leave you to ponder the practical wisdom contained in this succinct gem of a quote:

“Better to keep your mouth shut and let people think you are a fool than to open it and remove all doubt.”

– Dan Quayle

OK, at the risk of removing all doubt, an attempt at clarification:

“Savage Muslim Hordes”, aka Saudi-financed Wahabbism, vetoed by violence social progress in Afghanistan (from the late ’70’s on); destabilized eastern Africa; then migrated to former Yugoslavia to exacerbate ethnic tensions and aid in national disintegration there; then toppled Qaddafi and destroyed an arguably prosperous society in Libya; exported from that country jihad to Mali and arms to Syria, which country their brethren were already trying to destabilize and take over. And then we have Yemen.

I agree with your assessment that western financial oligarchies did produce and support much of the preceding chaos. They provided military and diplomatic support, and their agents wrecked Iraq pretty much on their own. But we shouldn’t ignore the role of the middle-eastern financial oligarchy either. Currently, occasional evidence of their briberies reported in western governments raises the issue as to exactly which agenda is being promoted in this sinister collaboration.

Bingo!… Based on the ECB, BOJ and Fed monetary policies over the past three decades, I think we should be looking at all Western central banks through a different lens than their legislative mandates. The long-term decline in the velocity of M2 money is the tell of massive policy failure (or success, depending on your view regarding concentration of wealth).

It has become clear that their suppression of interest rates to negative real levels by pushing bond prices ever upward through their unrelenting bond purchases primarily benefit legacy bondholders, the stock market indexes, highly debt-leveraged financial entities, and large speculators.

50 years from now (assuming humanity survives the reign of the US neocons), I expect this era will be known as “The Age of the Central Bankers”; just as the late 13th Century in feudal Germany and the late 1800’s in the U.S. both became known as “The Age of the Robber Barons”, and for similar reasons.

Agreed. Central Banks belong to a system that no longer works – abandon them.

We need a means of exchange that is based in reality not the silly policies of “independent” banksters.

My suspicion has long been that the plan is not some endless propping up of the system, but rather keeping it going while structural changes are made. On the financial front, that involves downsizing the operations of the institutions, and dealing with bad assets through a combination of letting them mature and writing them down. On the political front, it involves replacing elected representative government with technocratic governance, as we see fairly openly in Europe, and in a more disguised form, in the U.S. That is, the West is shifting to a political system deemed more suited to enforcing austerity when the music stops. The extend-and-pretend, money-pumping schemes help accomplish this overall goal.

Each financial crisis seems to result in an increase of technocratic power. This has been visible in Europe, where each national crisis results in further concession by national governments to the supranational powers. It is also visible in the “global solutions to global problems” approach to coordinated international regulation in the post-2008 period.

Rule by banker, wedded to their dogma of “more debt is good for you,” and guided by their Priests (Economists), all worshiping at the altar of Greed.

It is a cult.

If the definition of “citizen” includes being able to deal directly with her/his nation’s fiat then depository institutions are citizens and we, the general public are not.*

So I reckon the US has about 6,000 citizens in total.

*Unless one includes the ability to deal with unsafe, inconvenient, perhaps soon to be abolished physical fiat, a.k.a. “cash”.

I’m always in awe of economists and their complete inability to grasp the most basic of concepts. So much about being a professional economist seems to be about learning to turn off parts of your brain. Businesses aren’t expanding because they have no reason to do so. If anything they’re shrinking. Why? Because nobody has any money! And what money they do have they’re using to pay down debts, not go out an buy fancy bullshit.

Here’s another simple, and related, concept 99% of economists don’t understand: “Debts that can’t be repaid, won’t be.” If the only way for people to get more money is to go further into debt, it’s an endless spiral down. How does it end? Probably with a lot of economists heads of pikes.

Missing from this commentary is draghi’s rationale for these asset purchases to reach the near 2% inflation target yet after 18 months the EU inflation rate is stuck at .4% there is no evidence that asset purchases stimulate any uptick in inflation The disconnect between the ECB’s QE policies and the inflation rate is glaring so methinks the near 2% inflation raterationale is being used as cover for these highly flawed asset purchases by the ECB

I neglected to make the VERY important point that QE is NOT “printing”. It does not increase the money supply. It is an asset swap. ECB buys bonds. Investors get cash but they want to hold securities, so they go buy new securities. It does not create new cash system wide. Deficit spending would do that.

I neglected to make the VERY important point that QE is NOT “printing”. It does not increase the money supply. It is an asset swap. ECB buys bonds. Investors get cash but they want to hold securities, so they go buy new securities. It does not create new cash system wide. Yves Smith [bold added]

That depends, doesn’t it? If the asset seller is a bank, for example, then only bank reserves increase and those aren’t part of the money supply since the public is not allowed accounts at the central bank. But if the asset seller is a non-bank member of the private sector then bank deposits (liabilities) increase too and those are part of the money supply. Yes, those deposits can be used to buy new securities but that just moves the deposits around without decreasing the money supply – unless the new securities are bought from a bank; which, come to think of it, they probably often are.

Deficit spending would do that. Yves Smith

Yes, since that increases both bank reserves (not part of the money supply) and bank deposits (part of the money supply).

Btw, it appears that QE is just a way to give the rich more money by allowing them to act as middlemen between bond sellers and the central bank. For shame!

QE is printing and all claims to contrary have been thoroughly refuted. The Bank of England and others have done multiple studies on this and QE asset purchases do in fact inflate both the base money and M1 money supply. It is easy to prove this point by setting up three simple t-account to see the transmission mechanism. The money that is created does not make it way to the broader public though and this is a problem. It is also why helicopter money will make its appearance at some point because that way they can distribute the money more broadly.

The more important point is that the monetary system is a disaster due to incompetent management of the system. All money is debt, an esoteric point that few people understand including most economists. The secret to running a healthy fiat based monetary system is to limit the rate of credit expansion to the growth of the real economy. It’s basically that simple and the authorities utterly failed in this regard by allowing credit to expand at rate well in excess of real economic growth. Excess credit creation brings consumption forward, leads to speculation and asset price inflation leaving behind a mountain of debt and the associated financial claims on the real economy. It is quite literally a recipe of destroying an economy and the underling society. And voila look where we are!

The secret to running a healthy fiat based monetary system is to limit the rate of credit expansion to the growth of the real economy. Robert NYC

But deficit spending can drive real economic growth too and without increasing private debt*.

So how about this? Let creditors create all the new deposits/liabilities they dare but let’s make sure those liabilities are genuine liabilities and not largely a sham wrt to the general population as they are today.** In other words, let’s give honest accounting a chance?

*Ideally the “debt” of the monetary sovereign should always grow but:

1) It need not and should not pay positive interest to avoid welfare proportional to wealth.

2) The rate of growth should not cause excessive price inflation.

**This will be 100% evident if physical fiat is abolished since then a member of the general public will be literally unable to use his/her nation’s fiat AT ALL!

It is also why helicopter money will make its appearance at some point because that way they can distribute the money more broadly.

Yes, and please note that the proper abolition of government provided deposit insurance should require the distribution of huge amounts of new fiat to provide the new reserves needed for the transfer of at least some currently insured deposits to inherently risk-free accounts at the central bank itself or equivalent.*

*e.g. A Postal Checking Service that was forbidden by law from lending.

All money is debt,

If Equity is debt then I agree but it isn’t so I don’t. ;)

an esoteric point that few people understand including most economists.

Basic accounting should be a REQUIRED course in economics.

Why do you keep repeating this nonsense? There are multiple studies showing the QE does increase the money supply. Here is just one.

http://www.bankofengland.co.uk/publications/Documents/quarterlybulletin/qb120402.pdf

And if you don’t want to believe the Bank of England’s technical staff, I suggest you sit down and draw a few T-acconts and trace it through for yourself. You seem to labor under the mistaken impression that when a central bank buys bonds from a constituent bank that is the end of the story. It’s not. The banks then move to restore the earnings from those lost securities by buying bonds from the public sector. They do this by creating new deposits from nothing and the money supply increases as simple as that. Investors then buy bonds to replace those that were sold which forces up assets prices. As for the new deposits, they stay in the banking system and slosh around in the repo markets.

And if you still don’t understand this just go the FRED data base and plot QE versus M1. I would embed the chart here but you can’t display gifs in these text boxes. With all due respect you really need to study up on the monetary system because it is clear you don’t have a proper understanding of how it works.