Yves here. When I lived in Sydney, in a very nice but not the most tony part of town (Potts Point), housing prices already seemed nuts. I benefitted from the dollar being super strong, but in purchasing power party terms, $A1=$1. A $300 cart of groceries in both countries would be pretty similar. Rentals in Sydney were not terrible due to lots of people owing investment properties and wanting income to cover the carrying cost (that’s how firmly speculation was already built into psychology: renting units at a loss was pervasive). I thought the purchase price of my apartment was high relative to incomes. It was too close (in local purchasing power terms) to New York City prices when mortgage interest was not deductible like here. As you can see prices in Australia have only continued to accelerate since then. Some of it is clearly due to the liberalization of immigration and investment by Chinese.

By Wolf Richter, a San Francisco based executive, entrepreneur, start up specialist, and author, with extensive international work experience. Originally published at Wolf Street

“The authorities should prepare contingency plans.” The big four banks are too exposed to mortgages. Even if the banks don’t topple, the economy will get hit hard.

In its latest report on Australia, the OECD focuses to a disturbing extend on housing, household debt, what the current housing downturn might do to the otherwise healthy economy, and what the risks are that this housing downturn will lead to a financial crisis for the big four Australian banks, an eventuality that it says “authorities” should make “contingency plans” for.

The big four banks are huge in relation to the Australian stock market and the overall economy: Their combined market capitalization, at A$341 billion, even after today’s sell-off following the OECD report – accounts for 26% of Australia’s total stock market capitalization.

How they dominate the stock market showed up on Monday after the release of the report:

- Common Wealth Bank of Australia (CBA): -2.98%

- Westpac (WBC): -3.38%

- Australia and New Zealand Banking Group (ANZ): -4.09%

- National Australia Bank (NAB): -2.54%

The overall ASX stock index on Monday dropped 2.27%.

These big four are heavily owned by Australian pension funds, retail investors, and the like and form a big part of the retirement nest egg of the nation. So a banking crisis that involves the Big Four matters on all fronts – and the OECD report even pointed out that a collapse in the share prices of the Big Four would itself impact the overall economy negatively.

The report (PDF) starts by explaining just how strong the economy is in Australia:

With 27 years of positive economic growth, Australia has demonstrated a remarkable capacity to sustain steady increases in material living standards and absorb economic shocks.

The labor market has been equally resilient, with rising employment and labor-force participation. Life is good, with high levels of well-being, including health, and education.

It expects “continued robust growth of around 3%” in the near future. And the OECD’s “resilience indicators” suggest “that there is no emerging downturn at present.”

But then there’s the housing bubble, household debt, and the banks that have funded this bubble and that households owe this debt to.

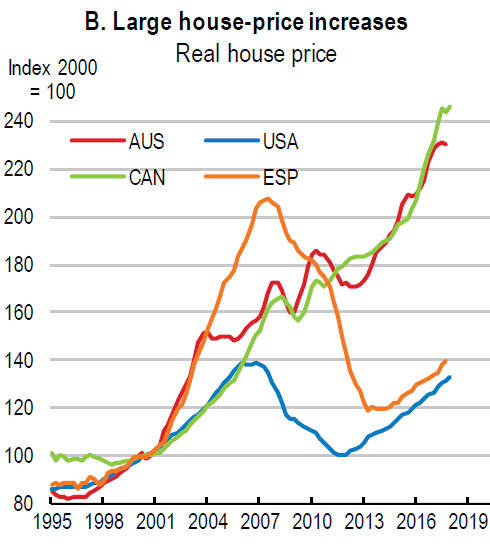

The charts below are from the report. The first chart compares inflation-adjusted house prices of the two most magnificent housing bubbles, Australia (red) and Canada (green), Spain (ESP), and the US. The index measures changes in price levels, adjusted for inflation. Clearly, Australia and Canada are in a world of their own, but Spain, whose bubble collapsed disastrously and led to numerous bank resolutions and bailouts, got close:

The Australian and Canadian two-decade long housing bubbles make the old US Housing Bubble 1 look practically infantile. However, with the US housing market being so much larger, and with US banks and financial products such as mortgage-backed securities being so interwoven in the financial world, the US housing bust that morphed into the US Financial Crisis became the Global Financial Crisis.

This is not going to happen with Australia and Canada: If they get into a financial crisis, they’re not big enough to drag the entire world into it.

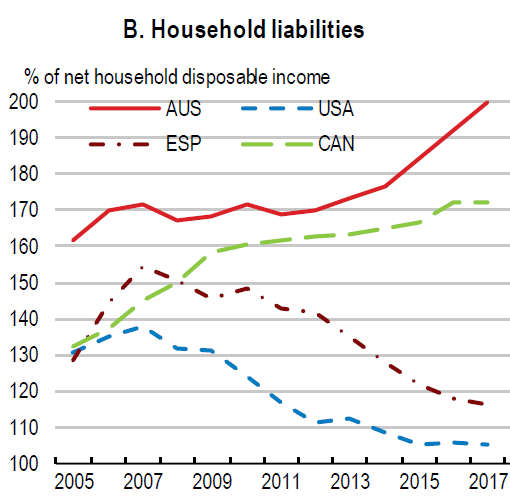

Australia’s household indebtedness, mostly tied to mortgages, and mostly owed to the above big four banks, reached 200% of net household disposable income, the highest ratio in the world. Even Canadian households can’t keep up with that. And US households, after the Financial Crisis, just fell of the mortgage wagon:

All this household debt has been incurred by households and provided by the banks on the assumption that the housing bubble would continue to inflate forever. But late last year, home prices began falling in Australia’s two largest housing markets – with prices in the Sydney metro down 9% and prices in Melbourne down 6%by last month. That was never part of the plan.

The OECD’s chart below depicts house prices in the big five capital cities. House prices in Perth (dotted line) have been in decline since 2014 due to the mining bust:

The ongoing sell-off in Sydney and Melbourne is “a welcome cooling of house prices,” the report says, which also lists some factors that contribute to it:

- “Prudential measures taken by the Australian authorities” to halt the “deterioration in lending standards.” This includes limits on interest-only loans, and many other measures.

- “A sizable pick up in new housing supply” – with new construction now flooding both markets at a record pace.

- “A fall off globally in the appetite for housing as an asset class,” which may, without naming names, refer to the sudden loss of appetite for Australian housing among Chinese investors.

- “Domestic rule changes and alterations to state-level taxes that may have deterred some foreign buyers.”

But the price declines haven’t done anything yet to fix the situation. The OECD warns that “though house prices have eased recently, they remain high in level terms (they have more than doubled in Sydney and Melbourne since 2005).”

And this housing downturn is happening even as Australia’s central bank (RBA) has kept interest rates at a record low 1.5%, which stimulated the housing market until it didn’t.

First, the report holds out hope: “The current trajectory would suggest a soft landing, but some risk of a hard landing remains.” But then it takes that hope away: “Past OECD work has found soft landings are rare.”

So How Will It Impact the Banks?

The Australian “authorities” are in denial, the OECD seems to say ever so politely in between the lines: “Direct risk to the financial sector from mortgage defaults, triggered for instance by a hard landing in house prices or interest rates hikes, is viewed as limited by the authorities (for instance, see, RBA, 2018).”

More denials from the “authorities” that encouraged this housing bubble to form in the first place:

- “A particular feature of the housing loan market is that it comprises mainly variable rate mortgages. This makes household loan repayments more sensitive to movements in interest rates….” But that’s not considered to be an issue.

- And: “Risk of financial stress from the large numbers of mortgages with interest-only phases that are due to transition to principal-plus-interest repayment is also not considered substantial.”

Nevertheless, here’s what authorities should do, after they get through with their denials (emphasis added):

“The authorities should prepare contingency plans for a severe collapse in the housing market. These should include the possibility of a crisis situation in one or more financial institutions.” The contingency plans should include “a loss-absorbing regime (including bail-in provisions) in the case of financial-institution insolvency.”

Despite the big four banks passing the stress tests, “the possibility of financial-institution crisis should not be discounted entirely.”

So when this “financial-institution crisis” happens, who should pay? The OECD explains:

Insured account holders will be fine: “For account holders there is a deposit insurance scheme, the Financial Claims Scheme, which provides protection up to a limit of A$250,000 per account holder at each bank.”

But bank shares – that A$341 billion in current market cap – senior debt, and uninsured deposits may be bailed in:

“As regards the institutions, a crisis would put recently passed crisis-resolution legislation under test. Unlike in the United States or European Union, the legislation does not include explicit bail-in provisions on senior debt or deposits owed by financial institutions. This gives flexibility to adjust resolution plans to the specific characteristics of the crisis.”

“On the other hand, the absence of explicit bail-in provisions could slow down the speed of resolution and risk encouraging financial institutions to gamble for resuscitation. APRA has indicated that it will start a consultation on its loss-absorbing capacity framework in late 2018;”

“Loss-absorbing and recapitalization capacity should consist of a financial entity’s equity (shareholders) as well as debt instruments (certain bondholders and uninsured depositors) on which losses can credibly be imposed in a resolution.

Even if the Banks Don’t Topple…

The report warns that “substantial impact of a hard landing in house prices on the wider economy may occur through other channels”: “If house prices collapse, consumer spending could suffer, via negative impact on wealth, including from exposure to bank shares, which would encourage deleveraging. Together with reduced housing-related expenditures, this would put pressure on the whole economy.”

“A large drop off in house prices could cut household consumption, prompt collapse in the construction sector, increase mortgage defaults, and freeze bank lending to business.”

In its own OECD bold, it says: “Financial supervisors and bank regulators should be prepared in the event of a hard landing in the housing market.”

And the RBA should hike its policy rates to remove the stimulus under the housing market: “In the absence of negative shocks, policy rates should start to rise soon. Monetary conditions remain very accommodative, with the risk of imbalances accumulating further if the low-interest rate environment persists. In the absence of a downturn, a gradual tightening should start as inflation edges up and wage growth gains momentum.”

So “a start to policy-rate normalization is now firmly on the horizon.” And “Though there are risks” to this “gradual tightening” envisioned by the OECD, “it could potentially bring welcome unwinding of the tensions and imbalances that have accumulated from the low-interest environment, notably housing-related issues.”

Which should have been done years ago before “the tensions and imbalances” got so big that they threaten to trigger the next financial crisis.

The house price declines in Sydney and Melbourne aren’t exactly slow motion anymore. Read… Update on the Housing Bust in Sydney & Melbourne, Australia

Cough … Glen Stevens …..

I’d be curious to lean what the average equity requirement per home (if any) is in Oz? Certainly , the banks take a hit, but the homeowner real estate investor also gets singed fingers. The losses are only realized in this ‘toxic’ partnership when a sale occurs. So, a work-out, between bank and owner is a possibility– at least there is a single note-holder with whom an ‘owner’/ borrower can meet. Lowered values acknowledged, note terms renegotiated, but an owner/borrower with skin in the game remains the prime motivator. The properties are less likely to fall into disrepair and decay, ditto the neighborhoods, and arguable the broader local community. The asset stays on the books, it keeps performing, at the lowered basis— partnership in the bruising.

US style securitized mortgage lending makes no room for a workout. The invisible hand turns palm down and squishes the show like a bug.

Maybe banks and shareholders get hurt– that’s part of investing– but the impacts on society— keeping those losses local, and not socializing them into the collective ‘we’ — it just doesn’t seem as dire as our ‘exceptional’ system. I guess we won’t know— that was a post-WW2 reality with local banking doing the work. The NWO in Amerika is a Hank Paulson Goldman-style Financial Giant figurehead riffling through a legal tablet at a podium, in abject panic begging for help, TBTF.

Thank you Jefemt. 20% deposit is required, below that would be required to take out mortgage insurance, which protects the bank, not you, in case of difficulties.

The bubble was always going to burst. The banking royal commission accelerated it as we learned the extent to which loans were approved with no real check on incomes and expenses. In my case, no check about the deposit (mostly from inheritance rather than savings). With valuations now going south, the banks risks are rising, whether they default depends on cash flow. Not enough people are going under. Yet.

Generally, banks will foreclose. But if that becomes a rout, perhaps they’ll look for win win solutions.

Not there yet and RBA still has some room for more rate cuts

Maybe Steve Keen will finally be redeemed and can come down off the mountain.

https://www.news.com.au/finance/economist-steve-keen-loses-housing-bet-against-rory-robertson/news-story/93ed4546692bf96793651c0cbcf0d8bb

“For fun, if Australian house prices ever fall by 40 per cent from any peak in my lifetime, I will follow in Dr Keen’s footsteps,” Mr Robertson said.

Might be time for Mr. Robertson to get in shape.

I’ve been following the Aussie housing bubble, but only on the margins, as i’m more interested in the NZ housing bubble.

Aussie banks dominate the financial milieu in NZ, and EnZed seems a year behind the times in their bubble compared to the Lucky Country.

The stories i’m reading in the NZ press are eerily similar to what you would have read here in 2008-ish. Lots of boosterism, the market is fundamentally strong, oh look over there, prices have gone up in Whanganui-see the market’s holding up, kind of bullshit.

I tried to impress on a few friends in Auckland how big of a bust it’ll be, but they’ve never seen such an animal and they did nothing, not that you really could, as the housing bubble in NZ was a completely kettle of fish to the one here, in that even in the white heat of ours, there were always places where you could buy a home cheap enough somewhere, but from what I saw in NZ, the entire country was in it’s grip.

There’s still areas of poverty and lack of opportunity in NZ where there’s cheap houses, useful to point out when needed to provide guidance to uppity millennial aspirants.

But yes there have also been growing numbers of basically low value towns seeing massive spikes in land values as the contagion spreads from main centres via the dual pressures of longer commuting junior corporates and low end investors going further afield to find things in their price range to rent out.

The NZ market is teetering though, because of lending pressure, a stagnant economy, and insurance.

It’s been very interesting to see the continued effects of the Christchurch quake on the insurance market. We’re now seeing many gentrification hubs dropping in price because the introduction of regional insurance risk premiums has had enormous consequences(premiums were previously all national averages which sunk a couple insurers in the chch eq). Notably the insurers are taking the opportunity to price in not just natural disasters that the areas might be prone to but also sea level rise. This has meant attractive seaside commuter suburbs like Petone which are already a high risk of liquifaction damage in earthquakes are also being recognised as likely to wear the worst of storm surges and erosion.

Not looking good for the Australian economy but has been long in the making. A bit of background. After a series of amalgamations we now have four big banks and a coupla smaller ones. I doubt that they will be amalgamated any further as neither the government nor the public have any appetite for fewer more powerful banks. At the moment we have not had a recession over a quarter of a century – since the early 90s. That was also when interest rates reached 17% which was a shocker. This means that a whole generation has grown up with little idea of what bad times look like. We dodged a bullet during 2007-2008 only because China was still buying our rocks and because the government of the day did not decide to go the route of austerity but went by way of public spending instead. We will probably be without those tools next time around.

Others may disagree but there is like a mania in Australia with real estate and everybody wanted to believe that real estate prices will always go up. Sound familiar? This same mentality has also encouraged people to go into debt rather than to save for stuff. Well now there is going to be the devil to pay and him out to lunch. Yves is right about the prices going through the roof. We sold our house in outer Sydney back in the early 90s for about $93,000 but now when I checked it is listed at $790,000. Yes it has been rebuilt since but not $700,000 worth. I suspect that NC will be featuring more articles on this story in the coming year. The only good thing is that houses will be eventually more reasonably priced over time as last I heard, they were triple what they should be listed at. What effect this will have on politics I have no idea.

Don’t forget the 9B the fed wired the RBA, but then again we had our own Greenspan-esque mea culpa with Henry wrt the share holder value meme of late, along with the revolving door and ideological capture of regulatory agencies.

Not to mention the whole thing is just basically a huge control fraud based on the model out of Orange county L.A. which went walkabout.

Yet then again the whole FIRE sector economic template was imported as best practices and after Keatings recession, we had to have, most assets were sold to international anglophone investors for a steal. On that point its quite interesting to see the whole China thingy long after the horses have bolted and the previous owners sell for a nice mark up to the Chinese nouveau riche, but its all about the Chinese take over … chortle …

Only thing else is the observation that most that were hippie-punching occupy or its supporters as commie socialists are now saying the same things, with the exception, most are trying to figure out the best way to short it all for a quick buck e.g. cheering on a collapse – with some very moralistic overtones – about the need for sundry RE investors to burn for their wants and the proceeds from shorting it will enable them to enjoy the fire sale prices after the collapse. Reminiscent of the whole Boomers stole all the wealth meme, so lets burn it down and then the new blood will get it right, its just so DEVO ….

I can imagine that the situation in Australia is very similar to what we have here in Canada.

I will be blunt. I think that there is going to be a pop in the housing bubble. Both Australia and Canada have too Liberal immigration policies and too much Chinese investments, while the real wages for citizens cannot possibly be rising anywhere near the level required to make this happen. Ian Welsh has recommended really high property taxes for foreign investment and I think that is a smart move at this point.

Both nations seem to be trying to tighten their lending standards.

https://globalnews.ca/news/4097215/canada-new-mortgage-rules-stress-test-2018/

In Canada, it is leading to a skyrocketing rent rate because people who want to buy need more income. That is the root of the problem. Real wages are falling behind the cost of housing. Vacancy rates in rentals are down as well.

The big issue is, when is this whole house of cards going to fall and what will be the impact?

In the USA, most people if they have assets, tend to be house rich and cash poor.

The bigger effect would be a colossal loss of confidence, as for the majority of those with investments, it’s the bright shining light in their portfolio.

I’ve mentioned this before, but name one commonly held consumer item that goes up in value aside from used houses? (and yeah, I get it, a lot of the value is in that sacred 4,000 sq foot lot that is pretty damned special)

You buy a new car, and it starts losing value them moment you drive it away from the dealership-until it plummets to near nadir, or made in China merchandise that loses value even quicker.

Lot sizes have been declining here for years, Wuk.

Prior to the 90s, much of the new land in Australia was subdivided into blocks of around 800 to 1000 m2, roughly 8000 to 10000 ft2?? Today, the blocks are around 400 m2 and the houses tend to occupy the whole block now, with perhaps a bit for a pool or some plastic grass.

The shame of it here is that a good shade tree or 2 at the bottom of your garden can really lower temperatures. (I have a huge ficus). Can barely plant a palm tree in the new blocks these days.

What’s it like your way?

When we lived in L.A., the gambit was to squeeze new homes onto small lots, and they’d have a 15 foot deep by 40 foot wide backyard, where you’d ‘entertain’.

Old school lots in parts of L.A. were huge, and i’m taking Arcadia and environs (it became one of the go-to places for Chinese money, and some wags called it “Arcasia”, ha!) that had 8,000 sq ft lots, many of which have either had giant new homes replacing the old torn down one, or they’d squeeze a few homes onto the lot.

Here in the Sierra foothills, property isn’t worth hardly anything, as it’s all nature acres, dotted by an oak savanna.

Nobody would dare cut down the trees to put in homes, so we’re all pretty much living surrounded by them, which is nice.

A home with 600 acres sold for $1.2 million a few years back, if it was in L.A. it’d be worth a huge bundle.

Near us a housing estate has been built in the pat decade or so. The houses cover most of the block with a bit left over for a lawn – of sorts. The crazy thing is that for the prices that they went for, for only a few kilometers more you could have bought acreage and with cheaper council rates consequently. The old traditional quarter-acre house block seems but a memory now.

There is a major difference between the US and Australian housing markets which people should keep in mind.

That difference is, that unlike in the US, it’s very difficult to actually default on a mortgage (technically a home loan) in Australia. You can’t do “jinglemail” and simply send the keys to the bank if you find your house underwater.

In Australia, when a bank lends you $500k (for example), that’s a loan secured by the property. And the whole amount has to be paid back.

– if the property declines in value to $300k, you still need to pay back $500k to the bank.

– if the property burns to the ground, you still need to pay $500k back to the bank.

– if aliens decide to take the property back to Alpha Centuri, guess what, the bank will still want its $500k.

What this means, in practise, is that loans in Australia for property aren’t just secured by the property itself, but by the entire personal assets of the creditor. This means that it’s only in the extreme cases of default – where the property is underwater, the owner has no other assets that can be sold (either through bankruptcy proceedings or before), and insufficient income to cover the repayments that the banks can actually lose money on the loans.

So when property prices dip in Australia, owners generally just bunker down. They cut down every other expense to make their mortgage payments. They use their savings to cover low rents on investment properties. They don’t sell unless they absolutely, positively have to.

So while property prices are going down – and this is indeed a very good thing – there need to be other things that happen to really turn it into a systematic crisis. I would be truly worried if the house price drops were coupled with significant rises in unemployment, because that could really start to increase the number of defaults. Alternatively, a massive drop in immigration to Australia would could also lead to demand drying up, but that doesn’t seem to be on the cards.

There would have to be something that happens that could really push the default rate up. But for the last couple of years the more marginal stuff has been stamped on – dodgy mortgages, interest-only mortgages. It’s not as though the entire boom has been financed by 105% mortgages – most investors have significant equity, and can absorb a big fall in prices, even if they don’t like it one bit.

The Australian property market is over-priced, obscene and filled with perverse incentives. But I don’t think it can cause too much damage to Australia as a whole, and a soft-landing is indeed likely. And I speak as someone who hates the Australian property market so much that I emigrated to get away from it.

“most investors have significant equity, and can absorb a big fall in prices, even if they don’t like it one bit.”

Concur and would add the scenario reminds me of the early 90s economic transients moving from Calif to Colorado et al – SDY – Melb to say Brisbane or peripheral locations to get lower cost out flows and set up shop … rinse and repeat.

Reminiscent of those that have spent years shorting AUD based on wonky money theory and then blame all and sundry for the opposite outcome, not the bad info in their heads.

Great point Atarxite, Australian banks have what’s known as full recourse, meaning your debt stays with you regardless of your financial situation.

Also heading into negative equity territory will have very significant consequences for borrowers and their families that did not do their due diligence, jumped on the FOMO bandwagon, and bought into (pun intended) the typically post 2000-Australian property speculation dogma. This is the direct result of obscene tax incentives and government policy, political influence, lobbying, and propaganda which has successfully engineered this sad situation. This mindset has effectively sold out a generation of Australians and transformed the archetypal notion of home ownership from a home that you reside in to raise a family to a speculative asset class. I won’t even mention negative gearing.

I’m looking to emigrate also after jumping around 3 states contracting for work. Someone else can clean up this mess.

In the article, I noticed the pungent phrase “bail-in,” as one of the central bank options for dealing with an asset price collapse to “bail out” the FIRE players. I wonder if that lines up with the “full recourse” element to Oz property law you mention, so that banks that run into trouble playing the run-up in prices can then seize deposits of mope customers to refill their capital reserves? That would be a nice precedent present for the neoliberal looters to have established for them. I’m sure Wells Fargo and BoA and the rest would be pleased to follow suit…

not big enough to cause global contagion?

Wasnt there something about if a Monarch farts in Sydney, sushi smells in Tokyo?