Another skeleton has fallen out of Apollo’s closet, implicating not just the firm but also the SEC, as well as Apollo’s fixer, um, law firm Paul Weiss. And this embarrassment, picked up by the Financial Times, comes when the firm is already in hot water over the firm’s co-founder Leon Black’s dodgy-looking relationship with serial child rapist Jeffrey Epstein. Black paid over $50 million in fees to Epstein, an implausibly high figure, for financial advice after Epstein’s criminal conviction in 2008.1

Even though the immediate conduct, that of a former partner charging hundreds of thousands of dollars of personal expenses to investors, looks penny-ante, Federal Judge Kevin Castel blasted Apollo in what was a SEC civil suit against the miscreant former partner, Mohammed “Ali” Rashid despite Apollo not being a party to the litigation.

As we’ll explain, the SEC comes off looking as if it was played by Apollo. However, since a lot of people find they’ve been outfoxed by Leon Black and his merry band, being snookered by Apollo per se isn’t a big a badge of dishonor as what actually happened. The agency has repeatedly made clear that it held the touching belief that the widespread investor fleecing in private equity that it unearthed in 2014 and 2015 were just mistakes by otherwise upstanding firms. Once they were made aware that their behavior wasn’t proper, of course they would shape up. In other words, the agency is constitutionally incapable of believing that anyone other that rogue employees and bucket shops engage in deliberate misconduct.

Apollo had previously settled with the SEC over having charged Rashid’s expenses to investors, along with two bigger-ticket abuses. That settlement totaled $52 million in fines and disgorgements; we’ve embedded it at the end of this post. You can see it skipped over the unseemly details of Rashid’s grift.2 But thanks to Judge Castel, we now know more. From the Financial Times:

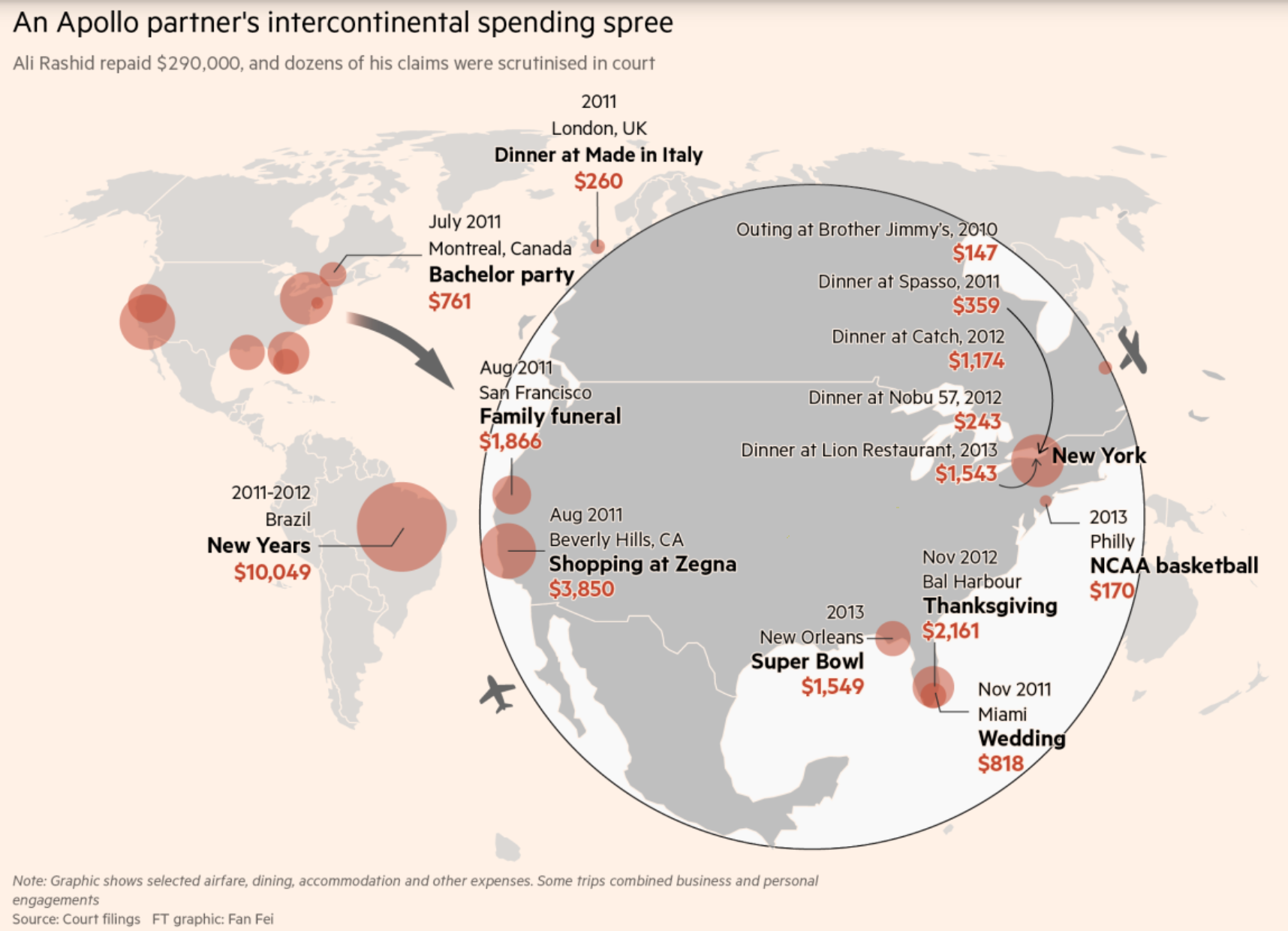

Judge Castel made clear he didn’t buy the garbage barge that Apollo had sold to the SEC when the agency settled charges with Apollo over having billed Rashid’s bogus charges, like the $10,049 New Years’ trip to Brazil or another jaunt reported in the New York Post, flying to Paris with a girlfriend, to investors.

It is clear that the SEC believed Apollo when Apollo depicted Rashid as having gotten investors in Apollo’s funds to pick up some of his high living. From the SEC’s order (emphasis ours):

29. From at least January 2010 through June 2013, a former Apollo senior partner (“Partner”) improperly charged personal items and services (collectively, “personal expenses”) to Apollo-advised funds and the funds’ portfolio companies.

The agency also came cringe-makingly close to fawning over Apollo’s cooperation. Again from the order:

47. In determining to accept Apollo’s Offer, the Commission considered remedial acts taken by Apollo and cooperation afforded the Commission staff. Apollo initiated several reviews of the former Partner’s expenses and voluntarily reported the improperly charged personal expenses to the Commission staff.

48. Throughout the staff’s investigation, Apollo voluntarily and promptly provided documents and information to the staff. Apollo met with the staff on multiple occasions and provided detailed factual summaries of relevant information. Apollo was extremely prompt and responsive in addressing staff inquiries.

In fact, Judge Castel found that Rashid had no knowledge of Apollo’s practices (as in what Apollo did with his expense claims) and that Rashid had been told that “the firm” (meaning Apollo as opposed to the portfolio companies almost entirely owned by investors) would pay for it. From the Financial Times:

The judge also heaped blame on Apollo for directing private equity funds it managed for outside investors, who include many of America’s biggest public pension funds, “to pay the entirety” of the bogus expenses. “While Rashid lied on his expense reports and was recklessly indifferent about the source of his reimbursements,” Judge Castel wrote, “significant responsibility lies with Apollo…

Mixing business and personal travel was the norm at Apollo, according to Mr Rashid, who testified to being told: “travel, don’t sit around, go find new deals”. He added that founder Leon Black and other top Apollo executives including Marc Rowan, Josh Harris and Scott Kleinman “[would say] in passing, things like, you know, ‘the firm will cover that’, or ‘the firm will pay for this’ or, you know, ‘just bill it to the firm’”….

Yet unbeknown to Mr Rashid and many of his colleagues, Apollo often was not paying the bills, but passing them to outside investors.

“It appears that private-equity funds were billed regardless of the nature of the expense, in contradiction to the limited partnership agreements that governed the funds”, wrote Judge Castel, who found the practice so alarming that he mused in court that “maybe there should be more defendants in this case”…

“Apollo, and not Rashid, put in place a policy of invoicing expenses to funds that . . . seemingly should have been borne by Apollo’s own management companies,” Judge Castel concluded.

A former private equity executive says that Rashid not influencing where his expenses are charged is standard. At his old firm, even though he worked with portfolio companies as well as on fundraising (meaning some but not all of his out-of-pocket expenses should have been allocated to portfolio companies), he was never asked nor informed about how much was invoiced to particular portfolio companies or the firm.

As a result, this bit is an eye-opener:

He [Judge Castel] wrote in his opinion that even current Apollo chief financial officer Martin Kelly and his predecessor Eugene Donnelly wrongly believed that Apollo was covering some of the charges.

The CFOs claim they thought Apollo was picking up some of Rashid’s charges? This posture is the beancounter’s version of “I’m the CEO and I know nothing about what goes on here.”

The only way these statements could be truthful is if the expense allocations to funds are done at a comparatively low organizational level, by design, to give the top brass a semi-credible “Those operations are handled at a much lower level and I don’t review the details.”

The Financial Times also fingers Paul Weiss, the law firm Apollo hired to investigate expense abuses at Apollo in August 2012. Note that it is hard to view Paul Weiss as arms-length; it regularly represents Apollo on its deals and therefore has powerful incentives not to upset the apple cart. It should therefore come as no surprise that Paul Weiss is also conducting an “independent” investigation into Leon Black’s relationship with Jeffrey Epstein. From the pink paper:

The ruling from Judge Castel comes eight years after Apollo retained law firm Paul, Weiss to review its expenses systems. The firm…found that of 300 top Apollo employees, only Mr Rashid’s expense submissions “warranted more in-depth review”.

The investigation identified about $20,000 of personal expenses incurred by executives other than Mr Rashid that needed to be repaid, but found no widespread misconduct. In fact, in a presentation prepared for the SEC and later filed in court, Paul, Weiss concluded that Apollo had picked up the tab for more than $370,000 of expenses that should instead have been borne by funds it managed for outside investors.

The findings of the investigation by Paul, Weiss now stand alongside those of a federal judge who ruled that “policies and procedures within Apollo contributed heavily to any act of fraud that was effected on investors in the Apollo funds”.

So Judge Castel has called out Paul Weiss’ whitewash. If you look at the order below, you can see Rashid’s assistant had questioned his expenses in 2010, which led to a review of six months of charges by an “expense manager,” a confession, reimbursement of some charges, and a reprimand. In early 2012, Apollo again got a whiff that Rashid might be pushing the envelope, and ordered another 6 month review, which led to another round of reimbursement and dressing-down. This part of the SEC’s order, in addition to the content of the Paul Weiss review, which was presented in this case, probably heightened the judge’s ire:

In August 2012, Apollo, on its own initiative, engaged outside counsel, which then engaged an independent audit firm, to conduct a firm-wide review of expense allocations. As part of this review, Apollo requested that the independent audit firm review the Partner’s reimbursement practices.

Bear in mind that the examination wasn’t as broad as “expense systems” but “expense allocations”. One has to wonder why Apollo saddle up Paul Weiss on this issue, while it was also conducting what was essentially a parallel audit of Rashid’s expenses, since as we know, whether an employee expense was reimbursed is entirely separate from how it was allocated. Was it because Apollo anticipated that the SEC would conduct an examination as part of its new Dodd Frank supervisory powers, and having a pet law firm Good Housekeeping seal would keep the SEC from nosing about on its own?

Read this section of the SEC order closely:

In June 2013, the independent auditor singled out the Partner’s expense reports for further review, which entailed an in-depth examination of the Partner’s expenses as well as the Partner’s emails and calendar entries.

We’re not disputing that Rashid’s expenses merited an in-depth examination. But remember that going on a business trip and then having personal meetings, or even using the business travel to get you to the starting point for a vacation, is perfectly kosher as long as you pay for the personal part yourself. It would also be perfectly permissible even to have an intent to vacation somewhere and arrange bona-fide meetings to get you to the vacation spot. The Financial Times describes how Rashid stepped over that line, that he pretended to have business reasons for expenses that were entirely personal:

Emails between the pair seemed to lay out the former Apollo executive’s method for defraying personal expenses. When his wife, who worked at another private equity firm, noted the rising price of plane tickets for a planned family trip to Dallas in 2010, Mr Rashid advised: “visit your port[folio] co[mpany] on the same trip.”

The court found that Mr Rashid employed a similar technique, “deliberately us[ing] the happenstance of [two business associates] presence in New Orleans at or about the time of the Super Bowl as a false justification for seeking reimbursement” for yet more personal travel.

So let’s go back to the probe of Rashid’s expenses. The auditor “singled out” his for checks against his e-mails and calendar to verify that they were business-related. But how could you be sure for anyone else who traveled or entertained without other members of the firm present unless you also reviewed them against his calendar and e-mails? In other words, it’s hard to take the claim that Rashid was the only abuser unless Paul Weiss had also randomly chosen other expense claims and subjected them to a similar verification process.

Put it another way: Paul Weiss would be far from the first “independent reviewer” to come up with grotesquely client-flattering outcomes. Admittedly, it would be hard to outdo Promontory Group. From a 2015 post:

The good news is that the New York Department of Financial Services (DFS) is still taking a hard line on bank misconduct despite the departure of its former Superintendent, Benjamin Lawsky.

The bad news is that in reporting on an investigation by DFS into one of the banking industry’s top regulatory fixers, Promontory Group, the New York Times curiously fails to discuss the eye-popping conduct at issue.

The case that led to the Promontory probe was the one that brought Lawsky to international attention, namely, his order against Standard Chartered for over $250 billion of money laundering on behalf of Iran, Myanmar, and other equally savory players….

Here is the priceless part, and where Promontory comes in. Standard Chartered asserted it had only $14 million of transactions out of compliance. This was despite the fact that the procedures for “repairing” as in doctoring, bank wires were commemorated in Standard Chartered operating manuals. How did Standard Chartered justify its claim of such inconsequential law-breaking? Promotory was the source of that very convenient estimate.

In case you managed to miss it, $250 billion is over four orders of magnitude larger than the $14 million that Promontory, whose claim to fame is that it is chock full of ex regulators, said was not kosher. And yes, Standard Chartered in its settlement with New York and other regulators, agreed that it had engaged in $250 billion of illegal transactions and that the Promontory estimate was wrong, and paid a total of $667 million to the DFS and other regulators.

Sadly, Paul Weiss partners won’t break a sweat over Judge Castel’s rebuke. Unlike private equity abuses of limited partners, Federal regulators actually care about money-laundering abuses and were embarrassed when Lawsky ran rings around them. There’s no threat of a competent regulator with clout taking this matter any further. But the flip side is that more and more Apollo investors have decided to make no new commitments until the Jeffrey Epstein controversy has been resolved. Having the integrity of the firm’s favorite fixer challenged by a judge isn’t going to reassure them.

___

00 SEC-Apollo 2016 OrderBlack claims he was buying investment and tax advice. This is an insult to intelligence. First, someone at Black’s level could easily hire the very best tax attorneys in the world, and similarly any financiers who had know-how that Black might value. Second, the fees Black paid to Epstein are astonishingly rich…. Third, Black admits much of what Epstein supposedly did for him couldn’t be relied upon…

Fourth, private equity barons are notorious skinflints; the idea that Black would pay so much for an uncredentialed individual with minimal relevant expertise and virtually no other clients strains credulity..

While it’s possible the two men shared recreational interests, Black would be certain to be aware of the risk of being extorted by Epstein. Black came out of Drexel and Drexel attempted to entrap its clients with sex. Connie Bruck’s The Predators’ Ball described the famed annual bash for Drexel’s raiders. One part was when the heavy hitters were brought to a room full of enticingly beautiful women. Bruck recounts how, almost comically, none of the men took the bait: they huddled with their drinks well away from the sirens.

So another possibility was that Black was indeed paying for illicit services, but of the financial, not the sexual, type. To give an unrealistically simple-minded example, what if these “fees” were just a way to create tax deductions, and only a fraction of the nominal fees were intended to be compensation to Epstein? This scenario would at least be logical from a hard-nosed business perspective; the other vague explanations that Black has offered don’t make much sense.

This sounds like a case of more financial chickens coming home to roost. If Obama had cracked down on Wall Street when he got in back in 2008, a lot of firms like Apollo would have tightened up their ship so not to fall foul of any crackdowns. But that never happened. The SEC remains to this day a compliant organization whose members hope to get jobs with the firms that they supposedly supervise. Certainly Rashid was playing fast and loose with his expenses and was probably hoping that all these trips and “expenses” would be lost in Apollo’s $180 million operating expenses. But this case still dogs Apollo after all these years due to the fact that Apollo made it possible.

I did find something of interest. It states that after examining 300 top Apollo employees, that only Rashid came under more scrutiny. Now it could be that Rashid was the bunny selected to get the chop but there may be more than that at work and may talk about the atmosphere at Apollo. The present chairman and CEO of Apollo is Leon Black and as this post mentions, Black came out of Drexler where he sought to entrap the heavy hitters with “honey-pots”.

Now it may be just me but when I heard that story, if I worked with Apollo with Black as my boss, I would be very wary about putting myself in such a position or playing fast and loose with any expenses. I would do nothing which was not authorized that would let a boss like Black have more leverage than he could normally have in my working life. That Epstein connection would just confirm it. The risk is too big so I do wonder why Rashid felt like he could go for broke here.

Even if these expenses had been allocated to Apollo they would still have been deducted for tax purposes and thus passed on in part to other taxpayers. Maybe a bigger scandal is the ability of the self-employed to deduct personal expenses which greatly limits the supposed progressivity of the tax code.

With most self-employed through an S-corp, their business income is also viewed as personal income as a sole proprietorship. This despite up to 70% of S-corps being registered on Wall Street.

However, a self-employed plumber is not in the same league as a multi-millionaire on Wall Street, despite both being classified as “sole proprietorships”.

Sole proprietorships are pass-through entities where all income is personal income. Losses can be deducted against all sources of personal income, IIRC. Please do note quote me on this.

Perhaps an exception could be made where using money from business to support another business, where both businesses are owned by one person… could be seen as an investment from one to the other. If losees are generated, the losses are only counted against the income of the originating corporation.

Perhaps limiting tax deductions from sole proprietorships to only that income generated by that specific business would do more to curb tax abuse than anything. If not done already. Such would curb the generation of paper losses through accounting gimmicks, as tax deductions.

The 2017 Republican tax scam had specific provisions for sole proprietorships, S corporations, lowering tax rates. Again, ip to 70% of these corporations are related Wall Street. Helping the plumber was incidental.

Perhaps S corporations should be limited to meaningful business activities that involving substantial work. With requirements being 181 days of substantial work – an employee in the office or on a work site, paying unemployment insurance, etc. With no comingling of business by a business owner, who just so happens to have registered multiple S corporations to one address.

That would clear out a lot of dross.

@D. Fuller

December 7, 2020 at 2:18 pm

——-

I’m an Enrolled Agent and Tax Accountant.

The IRS does not consider a Sole Proprietorship as a separate entity. Partnerships and S-Corps are separate entities, with income and losses passed through to the taxpayer’s personal tax return.

S-Corp income is not treated the same as Sole Proprietorship income. It’s reported on a different schedule on a personal tax return, and for some taxpayers, losses are limited if the S-Corp is considered to be a Passive Activity, with disallowed losses deferred to future years. This annual limit apples to all Passive Activity S-Corps, no matter how many a taxpayer owns. Sole Proprietorship losses are not limited.

If the taxpayer actively participates in the S-Corp’s business, then different limits, or no limits, apply to the losses.

The 2017 tax scam couldn’t reduce tax rates for Sole Proprietorships or S-Corps since they do not pay income taxes separately from the taxpayer. (Yes, there was a bit of reduction in personal tax rates, especially at the higher income levels, but the biggest reductions were for regular C-Corps.)

I also question your assertion that 70% of S-Corps are registered on Wall Street. S-Corps are registered at the state level. In addition, an S-Corp can have no more than 100 shareholders and only certain people or entities can be shareholders, not including another corporation. That rules out any publicly traded company.

Thank you for your reply and clarification. I had some doubt about my use of both terms.

You’re welcome.

I really like the formulation that Lambert(?) uses. Isnt it “however bad you think it is, its actually worse”? Or maybe thats Thom?

No, I’ve repeatedly quoted the famed short seller David Einhorn, “No matter how bad you think it is, it’s worse.”

Thank you

“As a result, this bit is an eye-opener:

He [Judge Castel] wrote in his opinion that even current Apollo chief financial officer Martin Kelly and his predecessor Eugene Donnelly wrongly believed that Apollo was covering some of the charges.

The CFOs claim they thought Apollo was picking up some of Rashid’s charges? This posture is the beancounter’s version of ‘I’m the CEO and I know nothing about what goes on here.'”

Martin Kelly was the Lehman Brothers controller when it blew up. His emails about Repo 105 having no substance etc. were quoted extensively in the Valukas Report.

This is what any good high-ranking Wall Streeter does: feign ignorance here, when that optimizes your outcome, virtue signal there if that’s the better way to survive, and so on. As pointed out, SEC and other regulatory/enforcement bodies, always led by Wall Street door-revolvers, always act as if it’s just a couple bad apples and never anything more systemic. And the band plays on.

“How did Standard Chartered justify its claim of such inconsequential law-breaking? Promotory was the source of that very convenient estimate.

In case you managed to miss it, $250 billion is over four orders of magnitude larger than the $14 million that Promontory, whose claim to fame is that it is chock full of ex regulators, said was not kosher. And yes, Standard Chartered in its settlement with New York and other regulators, agreed that it had engaged in $250 billion of illegal transactions and that the Promontory estimate was wrong, and paid a total of $667 million to the DFS and other regulators.”

Promontory is where Black Jesus’s SEC Commissioner Mary Schapiro went after leaving the SEC in 2012. Of course.

Schapiro also joine the boards of GE, CVS and the London Stock Exchange after leaving the SEC. Of course.

It’s in your face all the time, the robbing and the looting and the betrayal by those we are told to trust, over and over and over. Some of us bitch and moan about it here and there, and nothing changes. Can’t we do better?

It would seem that there’s a decent chance Black was being extorted by Epstein, no?

No, due to wanting to keep the focus of the post on the current offense, I did not cover material presented in earlier posts on Black and Epstein, specifically to Black having promoted Epstein’s tax and financial services to his partners at Apollo, and more important, the fact that Black and Epstein regularly had lunches and breakfasts. Since when is a victim on friendly terms with someone extorting them?

A top tax expert says a reason Black could have had for trying to get his partners to hire Epstein is to get them to use whatever schemes Black had gotten from Epstein. The IRS apparently gets cowed when a rich person can point to other people using the same questionable tax treatment that he has adopted.

Shades of “American business legend” Jack Welch of GE fame. Where Jack Welch led GE for two decades, with a golden contract that saw GE paying upwards of $150 million a year for Jack’s retirement, including his personal income taxes.

Welch rose up through the ranks of GE as a chemical engineer, with a long career. By 1981, Welch was CEO of GE. Then began the financialization of GE, with 40% of GE’s business being financial services. After Welch retired, GE faced accounting “corrections”. The value added by Jack Welch after the accounting gimmicks were accounted for, which included Jeffrey Immelt’s tenure – hand picked by Welch – are estimated at no more than $0.05 per share, probably closer to $0.02-$0.03. This despite growing GE’s business sales.

On a personal note, while sitting in a bar in Poland having a nice chat with a senior VP of a Polish company. The VP was stating how they were about to hire an American MBA as a VP at the Polish company when he asked my opinion. The reply was, “Check and see what happened to all the companies that that American had worked at.” That an American former VP was seeking employment at a Polish company at that time, was in of itself, suspicious.

The next night, the Polish executive informed that a ban on American hires had been instituted. The reason being that the American executive – an MBA – had worked at American companies, most or all of whom had gone bankrupt. With the American executive receiving very nice compensation from each of his former bankrupt employers.

American “business leaders” are more scam artist than business leaders, nowadays. IMHO, most don’t know how to run a company and generate profit. Too many American corporations are dependent on government & taxpayer subsidies to qualify as “Capitalists”. Such dependency is but one reason to invest in politicians – to keep their government & taxpayer subsidies flowing, as a guaranteed revenue stream funding their golden parachutes and stock options.

A small town plumber providing services is more the traditional Capitalist than any Wall Street banker or American CEO of a major corporation, ever will be in several lifetimes

The only way to save the system? Is to put it out of its misery and rebuild it from scratch. Apollo was caught by being too obvious. Much like Trump is despised by many even within his own party, not because he is so bad… Trump simply is too crass to disguise his grift that many others in politics and American business, practice.

I remember when Jack Welsh retired from GE – he sent out an e-mail to the entire company – I was in IT under GE Financial Assurance – Anyway, I had volunteered to get laid-off as I saw the imminent writing on the wall and felt others were in more need than me to bring home a paycheck. Mind you, I had the best boss ever – she was great and the people I worked with were the best people on the planet – IMHO.

The writing- on -the-wall was a meeting where a higher up was asking questions and one answer I gave was the repeal of Glass Stegall to a question about what law was repealed that gave GEFA a once in a lifetime opportunity to profit.

Back to that e-mail Jack sent out – I put together a letter about the ten things I would miss about working at GEFA – One was a dig about Jack’s contributions to SETI being so large was because if he did make contact with extraterestial intelligence – he would immediatley outsource.

Anyway, I accidently found an IT security hole by copying the address Jack used to send out his letter to everyone and pasted it to my send box – hit enter and went to lunch – by the time I got back, and my in box was stuffed with replies, my boss told me to duck out early because the head of IT was upset about his servers slowing down – I was wondering why so many folks were wishing me well on the way out – was just great

What’s extraordinary here isn’t that this Rashid clown kept getting away with billing personal expenses.

It’s that Apollo’s LP’s are so incurious about huge fees being extracted from them without being spelled-out in their agreements — and their willingness to facilitate tax evasion even though many of them are government organizations.

And none of it going to any productive purpose, other than enabling the Lolita Express.

Funny coincidence…Drexel’s party planner for the Predators Ball, who also recruited the women (prostitutes), was a guy named Don Engel, who go figure also shows up in Epstein’s Black Book in the special section at the end with Black, Dershowitz, Wexner, et al…

Black came from Drexel and as its head of investment banking would have been very aware of the escorts recruited for the parties. That is another reason why I deem him to be unlikely to have partied with Epstein. He’d be extremely aware of the downside.