Lambert here: Hard to be a 21st Century “arsenal of democracy” when you’ve outsourced your manufacturing base to China. But here we are.

By Maria Bas, Economist, CEPII, and Ana Fernandes, Lead Economist, Trade and International Integration Unit, Development Research Group, World Bank. Originally published at VoxEU.

The war in Ukraine has dramatically revealed the vulnerabilities of relying heavily on single foreign suppliers, following on from the COVID shock’s disruption of global value chains. This column presents evidence confirming the costly export shock for products with higher reliance on foreign inputs, and on China as the main input supplier, during the pandemic. In particular, the difficulties in producing remotely highlighted the vulnerability for products with a lower degree of complexity that rely on unskilled labour. Future resilience requires smart diversification and exploitation of working-from-home production.

Between January and June 2020, the volume of global trade retracted by 13%, with a sharp rebound from then onwards as the COVID-19 situation temporarily improved (World Bank 2020). Global shortages in face masks and medical equipment led many countries to ban their export (Evenett 2020), and a negative demand shock linked to heightened uncertainty account for some of the trade decrease. In a new paper (Bas et al. 2022), we provide evidence pointing to two main factors behind disruptions to trade caused by the COVID-19 shock: (i) the breakdown of production across the globe causing vulnerabilities in products that required inputs produced in specific countries; and (ii) restrictions to in-person production due to the pandemic creating vulnerability for products that are more difficult to produce remotely.

First, disruption to production due to the COVID-19 shock across the globe affected value chains. The sudden drop in the supply of products from China led to a debate about whether the increased exploitation of global comparative advantage, which had turned China into the world’s manufacturing powerhouse in the decade prior to COVID-19, had produced a dangerous foreign dependence on global production networks. China’s recently imposed lockdowns in the manufacturing hubs of Shenzhen and Dongguan are a reminder of the need to increase the resilience of supply chains. The Russia-Ukraine war has further illustrated that the resilience of foreign supply chains is a priority beyond the COVID-19 shock in need of serious attention going forward.

Second, the sudden onset of the COVID-19 shock in early 2020 resulted in substantial disruptions to economic activities as a large share of the global population was confined to home and a myriad of restrictions to reduce the spread of the virus were put in place (Baldwin 2020, Bénassy-Quéré et al. 2020). While high-skilled workers shifted to remote work and even experienced productivity gains (Barrero et al. 2021), less complex production relying mostly on unskilled workers was compromised.

What Is the Economic Magnitude of the Effect?

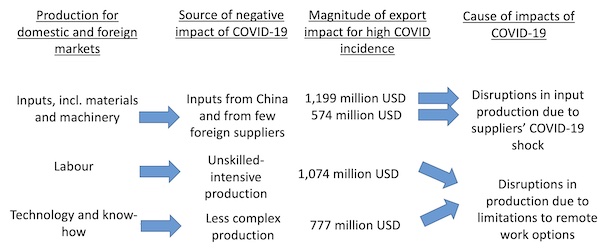

Our estimates, based on detailed product import data for the US, Japan and 28 EU countries in 2020, point to the substantial economic magnitude of the disruptions across three mechanisms caused by disruptions in input production and to in-person production. These are described in Figure 1.

Figure 1 The channels explaining the negative effect of COVID-19 on exports

Countries with higher COVID-19 incidence (captured by COVID deaths per capita) experience a 1.5 percentage-point larger decline in exports of more unskilled intensive products, corresponding to a decrease of US$1,074 million in median exports.1 A similar increase in COVID-19 incidence decreases exports of products with a higher reliance on inputs for which China is a dominant supplier by 1.69 percentage points, and exports of products with higher reliance on foreign inputs by 0.81 percentage points, corresponding to decreases in median exports of $1,199 million and $574 million, respectively. Finally, a similar increase in COVID-19 incidence leads to a decrease in exports of products with lower complexity by 1.09 percentage points which corresponds to a $777 million decrease in median exports.

Lessons for Future Crises

Where there is strong reliance on a small set of suppliers, efforts aimed at achieving smart diversification need to be a key priority for policy and industry. This requires having global production and supply arrangements that offer a portfolio of options away from concentration, particularly where there is very strong reliance on a small set of foreign suppliers. This does not at all mean decoupling from global value chains and the reliance on imported inputs, because that would not pay off and would come at a high price (Baldwin and Evenett 2020, Grossman et al. 2021, OECD 2022a). On the contrary, participation in global value chains actually reduced rather than increased vulnerability to domestic shocks during the pandemic as foreign sourcing was a beneficial diversification through trade when domestic production is disrupted (Eppinger et al. 2021, Espitia et al. 2020). Global value chains were pivotal for countries to get goods needed to vaccinate, protect and test during the COVID-19 pandemic (OECD 2022b).

As to resilience against future pandemics or conflicts that may restrain mobility and affect in-person production, further deployment of digital tools can help to effectively substitute in-person collaboration in production and also contribute to efficiency (Barrero et al. 2021). The automation of production can also reduce production vulnerabilities. However, this poses the risk of potential negative impacts on unskilled employment which can only be addressed through investments in worker upskilling and alternative models for revenue sharing in the economy (Guellec and Paunov 2017, Autor et al. 2020).

Authors’ note: The findings, interpretations, and conclusions expressed in this column are entirely those of the authors. They do not necessarily represent the views of the OECD, the International Bank of Reconstruction and Development/World Bank and its affiliated organisations, or those of the Executive Directors of the World Bank or the countries they represent. All errors are the authors’ responsibility.

References available at the original.

The Capitalists will sell us the rope with which we will hang them…uh, as there are no more rope manufacturers in the US, the reserve currency and international settelments financial structure will provide the wherewithal with which to purchase the rope…

Thank you for that comment – it brought a genuine smile to my face.

Ka-ching!

“Countries with higher COVID-19 incidence (captured by COVID deaths per capita) experience a 1.5 percentage-point larger decline in exports of more unskilled intensive products, corresponding to a decrease of US$1,074 million in median exports…”

In short, dead people don’t export. Why can’t it just be said?

That’s too in the face of what the consequences really are.

https://www.marketwatch.com/story/ups-stock-drops-to-6-month-low-after-earnings-beat-was-driven-by-higher-prices-while-volumes-dropped-11650992710?mod=mw_latestnews/

“Shares of United Parcel Service Inc. took a hit Tuesday, as the package delivery giant reported profit and revenue that beat expectations despite a “bumpy” macro environment, but only because higher prices masked a drop in delivery volumes….”

A little anecdote from today. Maintaining profit by raising prices is the only way to sustain quarterly profit numbers with a pandemic adding to illness (long term in significant enough numbers) and deaths of workers and consumers (no matter how the numbers ebb and flow, they keep adding up) – on top of most of the wealth continually flowing into fewer hands.

Lessons for Future Crises: Good news all around. With a little “smart diversification” we can keep globalization going while “reducing vulnerability to domestic shocks.” Automation also reduces vulnerability, although it might have negative impacts on unskilled employment but nothing a little “upskilling” — aka. education and training — and better revenue sharing — aka. ‘?’ — can’t fix. I am not sure how this helps unsnarl the ports or how it will handle a future of increasingly scarce pricey diesel, but I suppose more smart diversification and working-from-home should solve all the problems.