Yves here. This article from INET is far too triumphalist in tone about the prospects for the dollar but it is still worth considering some of its arguments. It also makes for an instructive contrast to the Ukraine-skeptic, anti-imperialist, and libertarian-oriented sites that see Russia and China and the other BRICs as soon to take the dollar down in a big way.

These commentators and analysts have done vastly a better job of calling the status of and prospects for Russia’s military campaign than the mainstream media. They have also not shied away from describing the considerable sanctions blowback to the West versus Russia’s economic resilience, with its economy so far performing better than Russian officials expected.

However, dethroning the dollar is another kettle of fish. This post outlines what it would arguably take for that to happen.

We’ve pointed out that to create a new reserve currency, the issuer would need to run sustained trade deficits to get its currency held widely abroad. Doing that is tantamount to exporting jobs. Pretty much no country want to do that even if they could; most countries pursue mercantilist policies so they can run trade surpluses (import jobs) or at worst, a trade balance. We’ve pointed out that as much as China would like to become the country that issues the reserve currency, it does not want the related burden of reducing employment. We doubt that Russia does either. And having some sort of SDR-type or other basket doesn’t solve that problem vis-a-vis the rest of the world.

A second requirement for being a reserve currency issuer is having financial instruments in that currency that your trading partners are willing to hold, since the balances for decent-sized trade counterparties will quickly exceed deposit guarantee amounts. The US dollar as deep and liquid capital markets, low cost trading for most instruments, extensive depositary arrangements, and a good regulatory regime (by world standards). Not only would it take China or Russia a long time to compete with the US on this front….they’d have to considerably financialize their economies to do so. Could they achieve that without incurring the same bad side effects as the US, such as a massive brain drain into banking and other rentier activities?

Having said that, Russia by dint of steadily rebuilding its real economy after the US sponsored and profited from the plutocratic looting of the 1990s, has not only achieved a decent standard of living for most citizens, but has built a military that is showing we squandered our opportunity as the sole superpower…and for a fraction of what ours cost.

In other words, it was a reasonable forecast that dollar hegemony would persist for at least another generation. It seems as if this is still a reasonable belief even with the shocker of the West stealing hundreds of billions of Russia’s foreign exchange reserves. Even though our contacts tell us of nervous billionaires moving their funds out of London banks to the Middle East, they aren’t moving them out of the dollar (if they were, you’d see big jumps in price of those currencies).

But the huge blind spot of this post is assuming that the world continues more or less as usual. There’s a shocking statement early on, to the effect that even if it’s true that the US has lost international power, it’s a mistake to assume some other state has gained it.

Huh? What about multipolarity don’t you understand? This is a shocking statement of American insularity. Russia beat us in Syria. Iran has won all of its last five wars (which the West does not acknowledge). By contrast, the US has lost all of its wars in the Middle East, unless you define nation breaking as victory. The fact that India, China, Saudi Arabia, and the Global South have all ignored America’s demands for support in the Ukraine conflict despite considerable arm-twisting speaks volumes (even backed up by threats to emissaries in the US along the lines of: “We know where your kids go to school in the US. We know where you have your bank accounts”.)

The shift from the pound sterling as reserve currency to the dollar came about due to the collapse of the gold standard in the Great War and the end of an era of globalization. Peter Temin argues, credibly, that the effort to restore the gold standard in the 1920s led to the Great Depression. A related argument is that no major economy has gone from being investment and export driven to being consumption-driven without undergoing a financial crisis. China’s financial crisis has been much predicted and has yet to come, but it may in the end be a big explosion coming after financial blow-ups in other markets.

Similarly, this post simply assumes that investors will continue to regard securities as solid stores of value. In the inflation of the 1970s, investors came to loathe stocks and bonds were trading at crappy values. High grade corporates like utilities had trouble selling bonds at less than 14% interest; I worked on deals with 15% coupons.

After the Great Depression, aversion to stocks and speculative instruments lasted for decades. It wasn’t until the 1950s that stocks came back to pre-Depression levels; even in the 1960s, stocks were seen as unsuitable for fiduciaries.

It’s not hard to imagine that the downside could be a lot worse than investors and the authorities are anticipating. As we discuss in a related post, the G7 has a loony-tunes idea that they can just say not to high Russian oil prices and still be able to buy oil from Russia. Now the EU might still be able to limp through this winter by not decommissioning nuclear reactors and using coal….but what if it can’t? What happens if there are widespread energy shortages on top of high food prices and food shortages? Businesses will reduce activity and even shutter. Tax revenues will fall. Lenders will default. The Eurobanks never recapitalized adequately after the financial crisis and the Italian banks and Deutshce Bank remain in poor health.

And mind you, winter cold and needed extra power for heat are not a one-shot deal. If the West keeps the sanctions on Russia (and right now, the idea of relenting seems impossible absent a lot of governments being voted out of office), even if Europe limps through winter 2022-2023, it will be weakened and will crawl into winter 2023-2024 in even worse shape.

And that’s not adding in that the Jackpot is coming….

By Photis Lysandrou and Anastasia Nesvetailova, Director, Macroeconomic and Development Policies, UNCTAD GDS. Originally published at the Institute for New Economic Thinking website

Since the collapse of communism in the early 1990s and the subsequent rise of the world economy as a single market-based operational totality, its monetary counterpart has been a unipolar currency system centered on the US dollar as the premier vehicle currency in the private sector, as well as the premier reserve currency in the official sector. The hegemony of the dollar has survived several global economic shocks, including that of the financial crisis of 2007-9. Whether the system can survive the seismic shocks stemming from Russia’s invasion of Ukraine in February 2022 is now under active debate.

Many prominent commentators argue that it will not, noting the ongoing attempts by Russia and her trading allies to circumvent the US-led imposed financial sanctions. Barry Eichengreen, for instance, observed that because of the Russian and other central banks’ increased diversification of their reserve holdings away from the dollar “we are seeing movement towards a more multipolar international monetary system.”[1] James Galbraith sees a dual currency system in the making, as Russia and her trading allies “carve out… a significant non-dollar, non-euro” rival financial system.[2] In a wider context of innovations in technology and finance, the IMF also noted the possibility of a scenario where “the greenback could be felled not by the dollar’s main rivals but by a group of alternative currencies,” including crypto and digital currencies.[3]

This is not the first time that a geopolitical crisis has prompted musings, at various levels of the academia and the commentariat, about the coming end of dollar hegemony. Invariably, they turned out to be wrong. Given the rather long history of failed forecasts, current predictions about the dollar’s future tend to be given with more caution and hedged with various caveats and qualifications. Indeed, to be fair to Barry Eichengreen, he is careful to emphasize that dollar dominance will not end soon, even while the Ukraine crisis may have accelerated the ‘stealth erosion’ of that dominance. A more general qualifying refrain is that a multipolar currency system, while not yet here, is nevertheless in the cards.

Is it, though? Can the ongoing attempts to establish a non-dollar alternative amount to a serious challenge to the hegemony of the dollar? The contrasting answers to this question reflect two alternative visions of capitalism. The declinist school of thought on the dollar supremacy stems, as Susan Strange noted some 30 years ago, from academic traditions that have historically overlooked the importance of the financial system in shaping the balance of power. It was a result of a methodological choice: at best, they have proxied it with currency regimes that serve international trade relations. As such, the declinist school of US power (and hence the dollar) originates in the productionist vision of capitalism, where trade reflects the structure of production, and where monetary regimes of individual states reflect the position of a country in international trade flows.

An alternative approach, known as the money view of capitalism,[4] or capitalism of futurity, places the tradability of debt[5] as the core institutional setting that defines political economy generally, and, more specifically, the force that anchors major decisions and developments in production, trade, and investment. From the latter perspective, we see no end to dollar supremacy, whether rapid or gradual. As Susan Strange wrote in her seminal critique of a realist school of international relations:

“the error of the declinist school of American scholars lies in assuming that if the US has lost power, some other state must have gained it… The facts suggest that this zero-sum idea is far too simple. The US government has lost power mainly to the market.”[6]

Today, we can add, the financial market. Focusing on the trade flows and currency reserve tactics of the central banks, the declinist perspective on the global role of the dollar overlooks the central force that underpins not only the hegemony of the dollar but lies behind global financialized capitalism in general. That force is the gravitational pull of the dollar-denominated securities markets.

2. The Gravitational Pull of the Dollar

“As recent crises make clear, up to now the dollar-based order has been supported mainly by instability elsewhere and the lack of a credible alternative or compelling reason to create one, or where such reasons are felt, the ability to do so… The system has been held up, in short, by confidence in itself, and not, so far as one can see, by much of anything else.”[7]

Galbraith is correct about the importance of the lack of alternatives to the dollar, yet the problem with his argument is his reading of the cause. He sees the confidence in the dollar as something highly fragile because it apparently lacks any material substance to back it. A lack that, presumably, comes down to the gap between the US share of world production on the one hand, and its share of world securities supplies, on the other.

Between 1986 and 2019, daily forex turnover had risen from about $0.4 trillion to $6.6 trillion.[8] During this period, the dollar’s share of this turnover has averaged about 44%.[9] In today’s terms, this percentage is roughly on a par with the US’s respective percentage contributions to the world’s equity stocks (40% of the $95 trillion outstanding in 2019) and to the world’s bond stocks (39% of the $106 trillion outstanding in 2019).[10] However, it is also far above the US’s percentage share of nominal world output (23% of the 2019 world GDP figure of $88 trillion). These numbers, taken in combination with the trend increase in the US trade deficits, underpin the widely held view, shared by Galbraith, that there will soon come a time when foreign investors will lose confidence in the dollar and thus abandon it due to mounting concerns about the US ability to meet its financial obligations in the face of its deteriorating macroeconomic fundamentals.

This scenario is realistic only if one assumes that there has been no structural change in the relationship between the financial sector and the macroeconomy. Yet, citing Strange again, the addition of credit has altered the balance of power in the world economy. But not in the way that Galbraith and others envisage it.

The expansion of financial markets, the explosion of debt and asset values, are typically associated with the phenomenon of financialization. Over the past few decades, financialization has evolved at an accelerated pace; the financial sector now completely dominates the real productive economic sector on which it rests. In 1980 the combined nominal value of the world’s equity and bond stocks stood at about $11 trillion, a figure on a par with that of nominal world GDP in that year. By 2020 the combined value of those securities stocks had grown over twenty-fold to $234 trillion, while world GDP had only registered an eight-fold increase to $84 trillion in that same period.[11] The growing scale disparity between the financial sector and the underlying real sector is what ultimately fuels narratives of an impending collapse, and the declinist school on the power of the dollar forms one of those narratives.

But financializaton is not a one-dimensional force. Its depth is just as important as an indicator of its historical significance, as is its speed of development because it reflects the structural role of finance in economic transformation. To be specific, the recent scale growth of the world’s equity and debt securities markets is an outcome of fundamental changes in both their supply and demand sides.

From a supply-side standpoint, this growth manifests the radical change in corporate and government dependence on financial security issuance. Previously that dependence may have been small, or, if large, always temporary (e.g., bond issuance to finance a large-scale project or to meet the costs of an emergency). Today, it has become both large and permanent, because of the new financial pressures on corporations and governments that are rising in tandem with the increasing size and complexity of modern economies. For increasing volumes of security issuance to be possible, there obviously must be investors with a correspondingly large enough demand capacity. Chief amongst those investors are the institutional asset managers, the pension and mutual funds, and insurance companies.

Once a small cottage industry catering to the wealthy, over the past four decades asset management has in many countries become a mass industry catering to the retirement and other welfare arrangements of large sections of the population. Along with this growth in asset management scale has come a corresponding growth in the need for investable assets – most notably, for equities and bonds. Although there are other types of assets that serve as stores of value for asset managers, the exigencies of their role as financial intermediaries mean that it is financial securities that necessarily comprise the majority proportion of their asset holdings. What sets these securities apart from other asset classes is their ability to combine a value storage capacity with a relatively high degree of liquidity. “In most countries, bonds and equities are the two main asset classes in which pension assets were invested at the end of 2018, accounting for more than half of all investments in 32 out of 36 OECD countries, and 39 out of 46 other reporting jurisdictions.”[12]

The new structural presence of the asset management sector has important implications for the financial system as a whole. The large absorption capacities of asset managers represent ample opportunities for corporate and government borrowers in having these investors on the buy side of the securities markets. However, at the same time, the industry is operating under new tight constraints regarding the disbursements of cash. As securities have no intrinsic value, their ability to serve as investables with a determinate value storage capacity depends entirely on the degree to which their prices are held firm and thus made tangible, a condition which, in turn, depends on the rate and regularity with which cash is returned.

Here lies the crucial significance of the transformation of asset management from a subsector of finance serving individuals, into an industry of wealth management populated by large institutional players. When households were the representative type of investor in the securities markets, borrowers had far more room for maneuver over cash disbursements. This was partly because households, as small investors, were less able to constrain security issuing organizations, but also because they had less motivation to do so, given that they themselves were under no obligation to invest any part of their savings in financial securities.

By contrast, institutional asset managers are always obliged to keep a substantial proportion of the portfolios that are marketed to the public in the form of liquid securities. It is this obligation that explains why these investors have been instrumental in the establishment of a whole new type of transparency and governance infrastructure in the financial markets that can help guarantee the regularity with which borrowers return cash.

In the final analysis, all understanding of what sustains the dollar’s supremacy in the contemporary era comes down to an insight into the remarkable transformation that securities have undergone in line with the new governance rules and constraints that are now binding on security issuers. Without these constraints, promises of returning cash are always in danger of remaining fictitious: promises filled with empty air. With the new regulatory and governance constraints, securities have been transformed from mere promissory notes into genuinely solid stores of value; from being particles without matter, they become particles filled with matter. What this means is that when all the securities of a country’s organizations are aggregated together, this aggregation endows that country’s financial markets with mass and a corresponding power of attraction for asset managers and other institutional investors: the greater the mass, the greater the power of attraction.

No facet of this power is greater than that exerted by the US securities markets.

Foreign investors currently have trust in the US and in its legal and governance infrastructure of tradability debt, or futurity. Far from there not being “much of anything else” underpinning this trust, there is, on the contrary, much of everything underpinning it. What the US offers, and what no other region can do at present, is a huge and varied abundance of securities (not only equities but also bonds, including corporate, financial, Treasury, agency, and municipal bonds) in which foreign investors can store large amounts of funds and across which they can also move these large amounts relatively easily according to any change in circumstances.

Given the need for dollars as a means of accessing the US securities markets, it follows that just as it is the sheer depth and liquidity of these markets that attracts foreign institutional investors in droves, this attraction serves, in turn, to further amplify the depth and liquidity of the market for dollars itself. This development helps to explain why the dollar remains the most widely used currency in the execution of various cross-currency transactions. For example, the dollar is the funding currency of choice in foreign exchange swap transactions that currently account for nearly a half of the $6.6 trillion daily forex turnover and that are mostly used by banks to hedge exchange rate risks and meet short-term liquidity needs. Similarly, the sheer depth and liquidity of the dollar market means that even when those institutional investors holding globally diversified portfolios transfer funds from one set of non-dollar securities to another non-dollar set of securities, they usually do so indirectly, via the dollar, to contain the costs of these fund transfers.

How will the financial sanctions currently imposed on Russia impact this situation? The answer is, hardly at all. Of course, these measures will see an increase in the amount of pairwise emerging market economy (EME) currency transactions. Yet to put this increase into perspective, there needs to be an estimate of the percentage share of the $6.6 trillion daily forex turnover that these transactions had prior to the Ukraine crisis. Even a cursory look at the figures makes it clear that this share was negligible.

In the first place, EME cross-currency transactions relate primarily to trades in goods and services, and these trades, taken in conjunction with all other real-sector-related currency transactions, account for no more than 8% of total daily forex turnover.[13] Once one strips out the real-sector-related transactions conducted between the advanced market economies (AMEs) themselves and those between the latter and the EMEs, it turns out that the remaining inter-EME currency transactions barely register as a meaningful percentage ratio.

The combined share of all EME currencies in daily forex turnover is just 13%. Even then, in most cases the counter currency was not another EME currency but an AME currency such as the euro, the yen, the Australian dollar but most notably the US dollar. China’s yuan, although the highest-ranked EME currency in 2019 at 8thplace in daily forex transactions, accounted for just 2% of these transactions and no less than 45% of these in turn had the dollar as the counter currency.

In sum, the Ukraine crisis will certainly lead to an increase in “non-dollar, non-euro” currency transactions, just as James Galbraith has argued. But the pre-crisis volume of these transactions was so vanishingly small as to invalidate any suggestion that this increase portends a multipolar currency system in the making.

3. An emergent multi-polar reserve currency system?

The same conclusion holds regarding predictions about the dollar’s primacy as a reserve currency. When Barry Eichengreen recently argued[14] that the Ukraine crisis will accelerate the movement towards a more multipolar international monetary system, his line of reasoning was as follows:

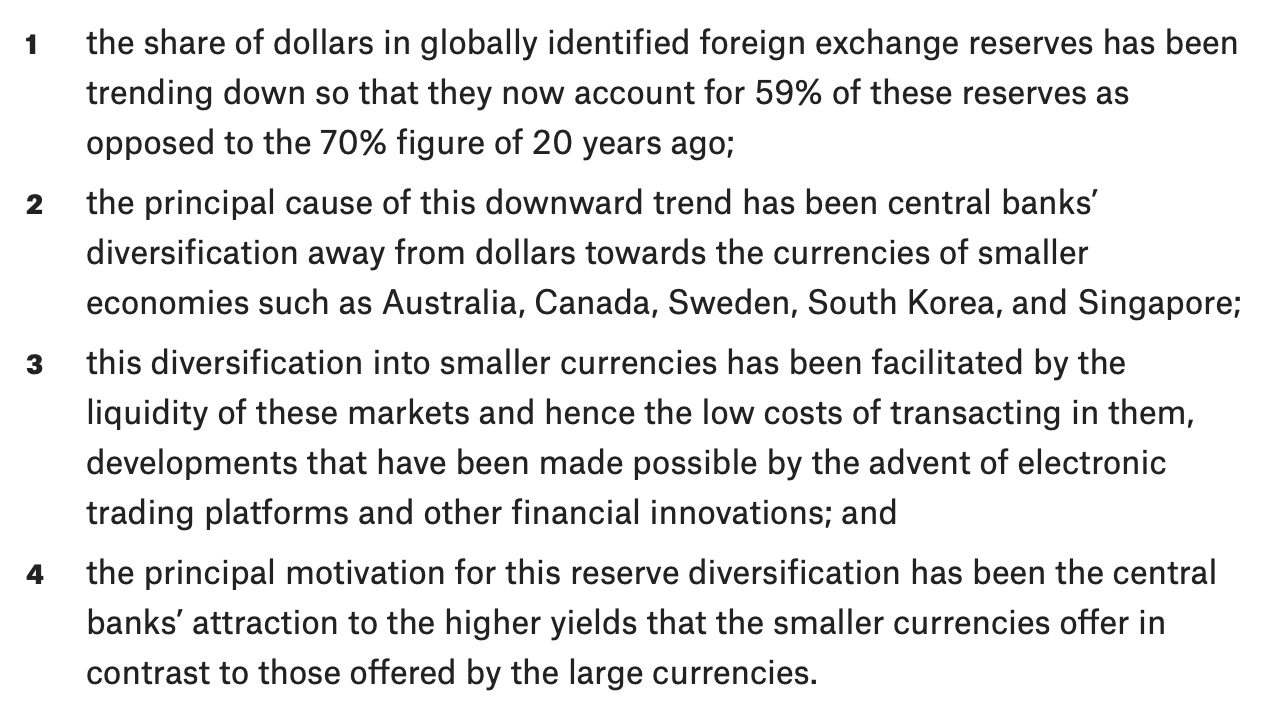

There is nothing wrong with this explanation as to why central banks are diversifying their reserve portfolios to include more smaller currencies. Nor is there anything wrong with the IMF’s observation that these reserve portfolios may now include alternative currencies such as cryptocurrencies and digital currencies. What is wrong is that these narratives are presented in entirely self-enclosed terms rather than in the broader context of what any increased diversification signifies for the overall composition of central bank reserve portfolios.

As with all institutionally managed asset portfolios, foreign exchange reserve portfolios are organized according to a core-satellite structure, where the core segment in this case typically comprises US treasuries and the satellite segments comprise the higher-yielding securities of other governments.

A key question, therefore, is whether dollar reserves in central bank allocations will fall far enough below 59% to warrant the claim about an emergent multipolar reserve system? The answer to this question, in turn, boils down to the question of whether the dollar core segment in reserve portfolios will shrink to a size comparable with the non-dollar satellite segments. The expectations are that it will not.

Recall that the reason why institutional asset managers must hold a significant, if not majority, proportion of their portfolios in the form of financial securities, is that these best combine liquidity with a value storage capacity. Now, while the huge growth of the stock of securities in recent years has provided these institutional investors with abundant supplies of safe and portable value containers, the flip side of this growth in financial value storage capacity is that it has also provided hedge funds and other speculative vehicles with massive financial firepower when targeting national currencies that are perceived to be vulnerable. As was pointed out in a Group of Ten report back in 1993:

“the growth in the size, integration and agility of international financial markets has greatly increased the scale of pressure that can be exerted against an exchange rate when market sentiment shifts.”[15]

The European currencies felt the scale of that pressure in the EMS crisis of the summer of 1992, while all the Asian currencies (bar the yen) felt the scale of that pressure in the summer of 1997. Indeed, it was largely because of the unnerving experiences of these crises that there was a subsequent sharp increase in central bank foreign exchange reserves. From barely $0.5 trillion in 1995, the total amount of allocated reserves held by central banks had risen to $5.4 trillion by 2010, an amount that was more than doubled again to $11.8 trillion by 2020.[16]

In 2020, the dollar’s share of allocated reserves was indeed 59% as compared with its share of 70% in 2000. However, to say that there was a “trend decline” in the dollar’s share over this twenty-year period is misleading because it gives the impression of a continuous, year-on-year decline. Rather, while there was an initial downward adjustment of the dollar’s share to about 60% that occurred in the first few years following the introduction of the euro, from 2005 to 2020 that 60% share then remained stable, as did the euro’s share of 20%, and as did the remaining 20% collective share of several other smaller currencies.[17] The fundamental reason why the dollar has continued to maintain this 60% share of foreign exchange reserves even as these continue to grow exponentially in absolute terms comes down to the large mass of US Treasuries.

In today’s era, when the world’s capital markets are deep and highly integrated and when cross-currency capital movements accordingly combine huge scale with high mobility, central banks that are concerned to minimize the impact of these movements on their domestic currencies need to have in reserve financial securities that: (i) have a large and safe value storage capacity, (ii) are available in abundance, and thus (iii) are highly liquid. No other financial securities, and no other financial instruments including crypto and digital currencies, can match US Treasuries as regards these criteria.

If any EME-based central banks needed any reminder of this crucial fact, the events of early March 2020, provided it. By that time, the covid-19 pandemic’s negative impact on the global economy became clear to the world’s institutional investors, and they quickly withdrew funds amounting to over $100 billion from the EMEs in the space of days. That withdrawal was catastrophic for many of these countries, but its impact would have been even more devastating had their central banks not quickly intervened in their domestic currency markets with huge sales of the US Treasuries kept in their reserves.

Central banks around the world may well add the higher-yielding securities of other smaller currencies to their reserve portfolios. But can we seriously believe that, at a time when the world’s financial markets continue to grow in scale and become ever more closely integrated, and the threats posed by sudden surges of cross-border portfolio investments grow accordingly, that these central banks will risk substantially shrinking their core holdings of US Treasuries in the search for higher returns? Of course not.

4. The Primacy of the Dollar as an International Currency

On April 1st, 2022, the Bank of International Settlements launched its 13th Triennial Central Bank Survey of Foreign Exchange Transactions and OTC Derivatives Markets, the full results of which are due to be published in November. In the two full years between the 2019 survey and the current one, the world economy suffered its biggest shock since the great depression of the 1930s with the outbreak of the covid pandemic. In 2020, nominal world GDP fell from its 2019 figure of $87.4 trillion to $84.9 trillion, while the world’s combined bond and equity stocks increased by more than 15% from $200.9 trillion in 2019 to $234.3 trillion, an increase principally driven by the steep increase in government bond issuance on the one hand, and the increase in security prices fueled by monetary policy easing, on the other.

The story in 2021 appeared somewhat better, as nominal world GDP rose above its pre-pandemic level to $94.9 trillion, but the world’s combined equity and bond stocks again rose substantially, to reach over $241 trillion.[18] In both these Covid-impacted years, the US share of the world’s supplies of equities and bonds remained stable at around 40%. Thus, going by the observation that forex turnover volume is overwhelmingly driven by financial sector interests as distinct from those of the real sector, we can safely predict that the dollar’s share of the new 2022 figure for daily forex turnover will remain around 44%, while, at the other end of the spectrum, the combined percentage shares of all the EME currencies will stay around 13%, with China’s yuan share at 2%. In other words, our prediction is that the Ukraine crisis that broke out just after the commencement of the latest BIS triennial survey of forex turnover will have had no discernible impact on the currency breakdown of that turnover.

As to the longer term, we also predict that there will be no serious challenge to dollar supremacy in the foreseeable future because there will be no other regional or national currency that will have a sufficient backing mass of equity and debt securities to enable it to mount such a challenge over that time span. To support this prediction, we need only invoke the experience of the euro.

When this currency was launched in 1999, it was widely assumed that, as the currency of the world’s largest single market and trading bloc, it would soon overtake the dollar as the world’s premier international vehicle currency. Chinn and Frankel, for example, argued that the dollar would relinquish that position by 2015 not only because ‘the euro now exists as a more serious potential rival than the mark or yen were’ but also because ‘the United States by now has a 25-year history of chronic current account deficits and the dollar has a 35-year history of trend depreciation.’[19]

This argument could not have been more wrong, because while the euro’s share of daily forex turnover hovered around an average of 19% between 2001 and 2010, it subsequently fell to an average of 16% between that year and 2019, the principal reason for this reverse movement being the eurozone’s failure to supply the world’s large institutional investors with sufficient amounts of euro-denominated securities in which to park their funds.

This insufficiency is even starker in the case of the world’s EMEs that today collectively account for about 20% of world equity stocks and about 15% of world bonds stocks.[20] Many EMEs have too small a domestic real economic base to support securities markets of any appreciable size. Those EMEs that do have large production bases nevertheless continue to have relatively small financial markets principally, if not exclusively, because of continuing weaknesses in their domestic legal and governance infrastructures.

China’s situation illustrates the point. Although China’s equity and bond markets are by far the largest of any EME, these are still small by comparison with those of the US, largely because its governance standards are currently of uneven quality, high in some sub-categories (e.g. law and order, crime prevention) and low in others (e.g. protection of minority shareholders). As for the period ahead, China, which is still a middle-income developing country, will find it difficult to move all its legal and governance institutions rapidly in the required direction.

5. Conclusion

Nothing that has been said above should be taken to mean that we favor a dollar-centered international monetary system. Far from it, for we believe that there are many sound reasons, ranging from the political to the economic, why a multipolar system is desirable.

Desire, however, is not enough. Nor is it enough to hope that the foundations of dollar supremacy are so fragile that it is only a question of time and of another shock or two to the world political and economic order for those foundations to come tumbling down. On the contrary, those foundations are strong, which means that any attempts to elevate rival currencies to a position where they can challenge dollar supremacy must start by recognizing the reason why its foundations do remain strong. That reason comes down to the hard stuff of the financial securities markets, their constituent solid matter. The chief purpose of this short contribution has been to explain the nature of that matter.

Notes

[1] Eichengreen, Barry, 2022, “Ukraine war accelerates the stealth erosion of dollar dominance”, Financial Times, 28 March 2022.

[2] Galbraith, James, 2022, “A multipolar financial world is here”, INET, 5 May; https://www.ineteconomics.org/perspectives/blog/the-dollar-system-in-a-multi-polar-world

[3] Arslanalp, Serkan, Eichengreen, Barry and Simpson-Bell, Chima, 2022, “Dollar Dominance and the Rise of Nontraditional Reserve Currencies”, IMF Blog, 1 June 2022, https://blogs.imf.org/2022/06/01/dollar-dominance-and-the-rise-of-nontraditional-reserve-currencies/

[4] Mehrling, Perry, 2010, The New Lombard Street, Princeton: Princeton University Press.

[5] Commons, John, 2017, Institutional Economics. Its Place in Political Economy, London, New York: Routledge.

[6] Strange, Susan, 1994, “Wake Up, Krasner! The World Has Changed”, Review of International Political Economy, 1:1.

[7] Galbraith, James, 2022, “A multipolar financial world is here”, INET, May 5th 2022.

[8] BIS, 2019a, 12th Triennial Central Bank Survey of Foreign Exchange Transactions and OTC Derivatives Markets, November.

[9] BIS calculates currency percentage shares out of 200%, to allow for the double counting of each currency pair. For simplicity, in what follows we halved the shares to give figures out of 100%.

[10] SIFMA, 2020, US Capital Markets Fact Book.

[11] SIFMA, 2021, US Capital Markets Fact Book.

[12] OECD, 2019, Pension Markets in Focus, p.29.

[13] BIS, 2019b, Quarterly Review, December.

[14] Eichengreen, Barry, 2022, “Ukraine war accelerates the stealth erosion of dollar dominance,” Financial Times, 28 March 2022.

[15] Group of Ten, 1993, p.33.

[16] IMF, 2017, Composition of Foreign Exchange Reserves, March. IMF, 2021, Composition of Foreign Exchange Reserves, March.

[17] UNCTAD, 2019, “Financing a Global Green New Deal”, Trade and Development Report.

[18] SIFMA, 2022, US Capital Markets Fact Book.

[19] Chinn, M. & Frankel, J. 2008, “Why the euro will rival the dollar”, International Finance, 11(1), p.51.

[20] UNCTAD, 2022, “Tapering in a Time of Conflict”, March. https://unctad.org/webflyer/ta…

See original post for references

Thank you, Yves. This is the kind of thing that sets NC apart for me. I generally get the dollar reserve currency issues from a geopolitical perspective but lack understanding of the financial perspective.

I wonder how settling accounts in national currencies affects this. That seems to be Russia’s preferred method of “attacking” the dollar. I also wonder about the proposed schemes for a new “reserve currency” based on a basket of currencies and commodities. Will this be an actual currency or more a method of determining the value of national currencies relative to each other for the sake of settlement?

Geopolitically then, I have to wonder if the US is miscalculating (again). There seems to be an assumption that the death of the global dollar requires being replaced by another currency, which requires the specifics addressed at the beginning of the post. But if that’s not the route of “attack” on the dollar is the defense of it still sound? I also wonder whether the real threat is an outside attack on it or the potential for a financial meltdown in the US? What happens if there’s a situation like 2008 but in the current context?

I’m not asking for answers to all these questions, they’re just the ones that come up in my head based on the new information (to me) in this post.

“Gas for roubles” was not about attacking the dollar (or euro or sterling). It was about having parties that had contracts for Russian gas make payments to Russian banks. Putin was explicit about that in his short statement before the detailed mechanism was worked out. If payments continued to go to Western banks, they could be stolen again as the Russian central bank reserves were. The “roubles” was a clever excuse since there are hardly any roubles circulating freely outside Russia for non-Russian banks to convert these payments to roubles.

Russian energy companies were already required to convert 80% of their foreign energy sales to roubles, so the impact of converting 100% made some but not a huge difference. The big reason the rouble has risen so much is the sanctions! Russian retailers are no longer buying many goods from the West (there has been ton more self than actual sanctioning here, Ikea and Starbucks et al pulled out on their own). They aren’t vacationing in Europe they way they once did. So the high commodities revenues and the big drop in imports = big rise in currency.

The big reason the rouble has risen so much is the sanctions!

I thought the value of the ruble increased because of demand.

It was brilliant to create a need for the ruble by demanding all purchases of Russian carbon be done in rubles, thereby creating a necessity for them.

It was a ju-jitsu move that mimicked the equation of the Petro-dollar regime, and is most likely going to be setting a future trend in currencies and their relationship to commodities.

> It was brilliant to create a need for the ruble by demanding all purchases of Russian carbon be done in rubles, thereby creating a necessity for them.

“Turning litter into money….” –Warren Mosler

Yes. I didn’t mean the gas for rubles part but the trading with friendly nations in their national currencies which seems to be a favored method of Russia going forward. I seem to recall that the oil trade with India would be completed in a mix of rubles and rupees. As I understand it, the dollar dominance is part the financial market aspect you detail and also that most international trade is completed in dollars. If international trade moves to settlement in the currencies of the trading partners, what effect does it have on dollar supremacy?

Where to begin as the Devil’s advocate?

1) why shouldn’t one of the BRICS decide to run a trade deficit? Why is a deficit equivalent to the export of jobs? Consider commodities. There are very few jobs in commodity mining by value produced. What if China bought a lot of Russian commodities and reoriented its economy to consumption, in a USA-KSA style arrangement. External claims on China would rise and, provided these were tradeable, so would the depth of the yuan as a reserve currency. Yes, by running a deficit, China would be exporting demand but if China keeps the terms of trade to importing low-labour inputs such as minerals, it will not be exporting jobs directly and, if it can sign agreements with its trade partners, it can control who benefits from the demand. If the world is dividing into blocs, China may have to take leadership of its bloc by opening its economy.

2) why should being a reserve currency require financialisation of the economy? It requires the issuance of government debt, which is otherwise known as the creation of safe assets for domestic investors and, if you open up, for foreign investors.

3) what ever happened to exchange rates? The dollar may be large and liquid pool of capital but is it quite so large and liquid at purchase parity exchange rates? And remember, sterling was worth $5 and now it is a quarter of that (and during the first US civil war, it spiked to $10 – how far will the value of the dollar collapse in the second US civil war…?). If the dollar’s deep pool of capital is twice as large as the US share of GDP, it only need to be cut in half, let alone a quarter, for the allocation weighting of other currencies to grow significantly.

4) what about gold? Yes, fiat currencies are cool and sexy, MMT is a description of actual monetary operations domestically etc. But there is a ready-made alternative to a reserve currency, if the BRICS willed it into being. And, provided China retained balanced trade, why shouldn’t China initially switch to a gold-exchange standard. You could view the progress of the dollar from gold standard to gold exchange standard to free float as the natural order of things rather than a historical contingency. Nation gets rich in specie by arming and feeding and financing the world (WW1); nation cashes its chips in for global dominance (WW2) and backs its fiat with specie; nation finances the world to buy its manufactures and rebuild itself (post-WW2); nation runs out of specie but its dominance as a financial power enables it to switch to fiat.

China has amassed fiat dollar claims in peace-time expansion but it could exchange them for gold or commodities then run a gold-exchange yuan until it can supplant the dollar as a fiat reserve currency. What if China went to KSA with its dollars and offered a military treaty and bulk bought all Saudi oil for the next twenty years? What would or could the US do? Sanction KSA so they cannot spend the dollars? How would it buy oil?

You don’t have to pick one, you could do a bit of everything. The dollar falls in purchasing power, China issues yuan debt to Russia to pay for commodity imports, China increases domestic consumption, China buys an alliance with KSA with its dollars while US shale oil and gas production drops and various petro-states nationalise their oil industries with the support of China. Suddenly the petro-yuan and the dollar are at equal weighting in global trade and the dollar is hanging on for historical reasons like inter-war sterling. All it takes is one wrong war to give it a final shove….

Running a trade deficit is exporting jobs. Rather than using your domestic demand to employ people at home, you are employing people abroad to satisfy that demand. That’s why countries ex the US attempt to pursue mercantilist policies.

You are effectively putting your fingers in your ears and yelling “nyah nyah nyah” on this topic.

Government debt is nowhere near sufficient to achieve reserve currency status. The example of the Eurozone’s failure to become an even minor alternative to the dollar should show that. You fail to appreciate the depths and complexity of investments available to dollar investors, from many traded commodities and securities indices, ETFs, derivatives, and the considerable infrastructure, both technology and regulatory, that the require. Many many studies have found that deep secondary trading markets are a drag on economies, they do not promote primary investment (in actual productive businesses) but those deep secondary markets are what is necessary to make investors happy about parking much dough in a foreign currency.

Gold does not make a currency attractive. There was rampant cheating under the old gold standard. Gold-backed currencies are also deflationary and that would be disastrous for an economy with high debt levels like China. If you want to trigger the long-overdue China financial crisis, that would be a great way to do it.

China is way less credible as a military partner than the US. The US is in the arms sales business. The US provides all the support and services, from our CIA goons in Ukraine to the Blackwater, now whatever successor entity they are using. Tell me the last war China won. The US can at least claim to have been successful in Desert Storm (not that I agree) and to have won the war but lost the peace in Iraq (not that I agree their either). It has scored some successes in the regime change business.

And why should China “issue debt” to pay Russia? That is nonsensical.

What do you mean war won?

China has achieved its political objectives in both the Korean War as well as in the short war with Vietnam. Shouldn’t these count as victories, ultimately?

All the while the US is loosing all the wars but still claiming to be the hegemon…

The Korean war was a stalemate in which all the sides achieved at least some of their strategic objectives without having a complete victory. The short conflict with Vietnam was an abject humiliation for the Chinese military. It indirectly led to them losing their foothold in SE Asia (Kampuchea) and they didn’t win a millimeter of Vietnamese soil (the Chinese maintain a historic claim on parts of northern Vietnam). It arguably led to the Vietnamese to choose in the long term closer ties with the west than with China. The only reason the Vietnamese don’t press this point is because China had nukes and they don’t.

The closest the Chinese have come to military successes in recent history is in crushing the Tibetans (basically, farmers on yaks) and in driving India out of parts of the Himalayan plateau. They’ve generally had the upper hand in most of the intermittent border flare-ups along the Aksai Chin, Ladakh, Sikkim and the border areas in Bhutan.

Not trying to be combative, but if my recollection of history is correct, the US/UN force in Korea was supposed to stop at the 38th parallel, but instead changed the goal to reunification. China warned they would not tolerate US on their border and attacked, pushing them back to essentially the 38th. This sounds like a win for China.

why should China “issue debt” to pay Russia?

The US has set the standard of exchanging debt coupons, US Treasuries, for commodities and manufactured products.

Why would the Chinese not copy this template?

I can not see why not.

That is not why the US sells Treasuries nor is it the reason that China holds Treasuries.

Asian countries have become eager to hold large foreign currency reserves to protect themselves from a currency crisis (ie they can use the FX reserve to defend the currency). The Asian financial crisis of 1997 scarred many countries. South Korea believes, probably correctly, that it was harmed more by the IMF program than the crisis proper (the 1997 crisis there is called “the IMF shock”).

There was even a time in the last decade when China was selling dollars out of its FX reserves for precisely that reason. The IMF even wrote papers saying China could hold out only for about a year plus and that might not be long enough.

Why does Russia have any reason to hold Chinese securities? Russia has been able to defend its currency in this crisis without reverting to foreign market operations. It’s enough of an autarky to be able to do that.

> Running a trade deficit is exporting jobs.

In other words, the United States, among the other things it is very good at, like pizza and shockingly over-priced and dysfunctional weaponry, is World Top Dog in keeping the working class down?

I do not agree that running a trade deficit will necessarily export jobs. If a country had a job guarantee like suggested by proponents of MMT, I would actually expext the country to run a deficit.

Sorry, your assertion is false and you have no evidence to back it up.

A trade deficit means a country is buying more goods abroad than it sells abroad. The net payments for foreign goods = US demand paying for foreign jobs.

A JobGuarantee would merely be a band-aid over that problem. It would need to create EXTRA jobs to make up for the jobs lost to the trade deficit.

Revenant — Where to begin as the Devil’s advocate?

I’m reading Revenant’s advocacy as possible actions specific nations would take in specific circumstances to mitigate or ameliorate specific adverse effects of dollar supremacy and nothing more beyond that. And I believe that increasingly is future of the dollar supremacy.

Yes this is what Michael Pettis has been saying for a while. The exorbitant privilege of the US dollar hegemony comes with an exorbitant burden that China, etc are simple unwilling to carry. Global investors want to hold US dollar assets despite everything and it takes a hell of a lot to change that.

The burden of having your enemies voluntarily paying for your military?

I like Michael Pettis, and he got some interesting points, but the he has statements lie the one above.

Great post. Thank you Yves. It has taught me a lot. Your comments are very sensible.

Hmm, I think this article is overestimating the importance of the financial logic of the current institutions in what is ultimately a political decision. What is at stake isn’t just which currencies are used within the institutions (where the dollar has systemic advantage), but the nature of the institutions themselves. If something like Keynes’ Bancor were established by treaty in a block of countries, the dollar would quickly lose relevance within that block. As the block grows to encompass more of the world, the dollar would inevitably decline.

Pray tell, why should a country in this bloc that wants to or structurally does run trade surpluses accept the Bancor feature that punishes running a surplus? For Russia, they are selling commodities that are in finite supply. They will hopefully further strengthen their manufacturing, services, and other value-added activities, but why should they accept the haircut that Bancor would effectively impose on them? My understanding that this wos one of the reasons that Bancor was rejected at Bretton Woods. Countries refused to accept the idea than running trade surpluses was bad and needed to be checked.

The discussion so far has focused on trade. Capital flight, debt service and investment or speculation are the key issues right now. The “debt bomb” will hit this summer and fall, as Global South countries cannot pay their foreign dollar debts if they must use their export revenues and foreign exchange reserves to pay higher prices for food and energy. Something has to give.

The emerging “anti-dollar” bloc can arrange currency swaps and create rancor credits (just as the IMF creates SDRs) to draw Global South countries into their orbits. But they will not create subsidies simply to let these countries pay their dollar debts. A choice will be forced, and major defaults (as occurred after Mexico’s announcement that it could not pay in 1982) will occur — in a highly polarized political environment.

Plus the microeconomic debt bomb caused by higher interest rates affecting derivatives, margin calls, etc, not to mention personal & small business bankruptcies, lower purchasing power, and so on. The one shot bail out tools used to paper over the 2007/8 collapse don’t exist today. What are the global macro implications of an impending U.S. financial collapse?

In short,

the lot.

CBs expanding balance sheets to the moon or as long as TBTFs are not directly involved actual bankrupcies and writedowns?

Because here I am guessing we might find some formerly hidden fault lines in the West. Particularly within the Eurozone.

The emerging “anti-dollar” bloc can arrange currency swaps and create rancor credits

In the elastic reality of the rule of law, as you illustrate, there is a myriad of mechanisms that could be initiated to keep the ball rolling in the present US Dollar/debt regime game.

Just like when the financial edifice was crumbling during the 2008 mortgage derivative crisis, and the FED churned out currency swaps around the world, along with its QE of buying worthless debt securities and hiding them on their balance sheet shelf, the next financial crisis will have the same clever mechanisms resurrected.

I would like to thank Mr. Hudson on his brilliant work illustrating this.

You have no idea what this takes operationally. Please don’t handwave.

The Fed swap lines had already been in existence for decades. And they were lending to mature, creditworthy borrowers. The banks in their countries that needed to get DOLLARS were also already on dollar payment systems.

Tell me how getting a RMB swap line solves a dollar payment crisis. It doesn’t. And tell me how banks that don’t clear and settle on a RMB payment system could even get the RMB.

My contacts are skeptical that any member of the emerging non-dollar bloc can or will engage in currency swaps, particularly to countries that won’t be credible in unwinding them. The dollar mechanism has existed for decades. It hasn’t even been set up anywhere for these currencies. There are operational and risk issues you are hand-waving away.

It’s one thing to give the EU FX swaps in the 2008 crisis so they can then issue euros, swap them for dollars, and rescue their banks that got sick eating US dollar subprime debt and CDOs. We were basically solving liquidity/solvency problems we had created. And the EU (and UK, Switzerland, Japan) was clearly going to be able to reverse the currency swap down the road and they did. Broke Sri Lanka is not credit worthy.

And your argument makes no sense. Foreign currency swaps, even if they could be arranged, would do zero to solve a dollar/dollarized payments issue.

Michael, with all due respect, your comment about arranging swaps is delusional. That would take years to set up.

And it would do nothing to solve their SOLVENCY problem. The reason the dollar swaps worked in the crisis is

1. The Fed was letting foreign banks provide emergency DOLLAR assistance for foreign bank DOLLAR liabilities. So the ECB created euros, swapped them for dollars, and lent dollars to the banks.

2. Some of the Eurobanks went bust but most soldiered on as the US bailed out the dodgy loans enough by inflating real estate prices via QE. QE was an asset swap targeting mortgage yields. Lower mortgage interest = higher housing prices = some of the underwater debt came back (via foreclosures and short sales at somewhat less distressed prices).

3. The countries were all expected to and did repay the currency swaps in full.

This isn’t remotely the scenario here. Tell me how the Sri Lanka central bank creates currency and uses RMB swaps to pay dollar or other non-RMB liabilities. The Chinese central bank can rescue Sri Lanka ONLY with respect to RMB debt. China might as well forgive any debt or renegotiate terms, like greatly lower the interest rate and extent the maturity. Ditto Russia and India.

The currency swaps were very controversial here (there were Congressional hearings on them) despite the high odds of them being repaid. How would Sri Lanka’s central bank be able to get the RMB to reverse a massive currency swap, even if one were to happen? That sort of default would not go over well in China. So I also doubt the Chinese officials would be comfortable with the credit risk.

The most China could do is sell some of its dollar reserves and provide dollar foreign aid to Sri Lanka. Please tell me how that would go over in China? I suspect not very well. The mere fact that China holds big dollar reserves that they can’t use domestically and have sometimes depreciated is already a sore topic.

Something will give and it’s Sri Lanka. People will die and billionaire carrion eaters will pick the country’s remains.

Yves, thanks. Isn’t the reason todays trade surplus countries would reject a new bancor (implicitly dollar inclusive) the connection between what these authors correctly call the real (trade in goods and services – with use values) and the financial? They have no theory of that connection. They point to the startling rise in the ratio in dollar terms between them, and (amazingly) conclude that therefore the real is of ever decreasing importance. And the rate of change is increasing, as they note. So soon the real will be insignificant (like the share of the Yuan in global central bank reserves), before disappearing – asymptote / jackpot. But i very much doubt todays trade surplus countries see this process with these authors complacency.

The potential bloc of trade surplus countries do need to find a way flexibly to link with the slow motion exploding dollar/financial system, which these authors are surely correct in seeing as analytic to the post-WW2 global capitalist system. In the last days of the USSR, i was sent by my lawfirm in NYC to Moscow Narodny in the city to deal with a Cuba-connected problem they had with the foreign assets control people in the US Treasury Dept. In a way an ancestor of the current problem on a much smaller scale. Vneshtorgbank owned Moscow Narodny and VTB had a strong institutional memory, and i bet it still does. Moscow Narodny people were proud of their role in creating the eurodollar market, some twenty years earlier. It could not be recreated (eurasiadollar market?), but a similar flexible link would be very useful to the new multipolar settlement/investment commodity (use value linked) backed system being worked on. Glazyev’s a very bright guy who knows this history; it doesn’t seem at all improbable to me that this could be up and running relatively soon.

I don’t entirely agree that “…to create a new reserve currency, the issuer would need to run sustained trade deficits to get its currency held widely abroad.”

The Dollar became a major trading currency before and during WWI. Then it became the world’s major reserve currency after WWII. Both were times when the US was running trade surpluses. In fact the US ran a steady trade surplus from1870 to 1970 https://files.stlouisfed.org/files/htdocs/publications/economic-synopses/2019/05/17/historical-u-s-trade-deficits.pdf.

Britain, after the 1870s, was in relative decline and the outside-the-empire trade balances in goods and invisibles show the trend although the reasons for the decline are debated. See: https://www.britishempire.me.uk/trade.html and https://www.jstor.org/stable/40721361. For a truly staggering review of world trade statistics see: http://www.ehes.org/EHES_93.pdf

In some sense the dollar didn’t become a reserve currency because of US action. It became a reserve currency by default when Great Britain, France and Germany’s saw their currencies became less desirable because of war and decolonization. In one sense, both the present US problems and the rise of China as an export power mimic the US between 1870 and 1914 when the US dollar became more important because foreigners had to acquire them to pay for US imports. The World Wars just amplified the US trade surpluses.

That being said, the present Ukraine crisis is not WWI or WWII- yet. So I’m not sure how a “slow but steady” vs “discontinuous because of World War” change in world reserve currencies will work. My guess is that for a time we will have a US-China reserve currency duopoly such as existed with the US-UK duopoly between WWI and WWII. But only time will tell.

There was so little trade during WWII that that period is meaningless.

The US made itself the reserve currency in Breton Woods by creating what amounted to a gold/dollar standard, with the dollar (and only the dollar) set at a gold price of $35:

https://www.hillsdale.edu/educational-outreach/free-market-forum/2012-archive/the-rise-and-fall-of-the-gold-standard-in-the-united-states/

And I do apologize for talking about trade deficits and not current account deficits, which is what matters. A current account deficit results in getting dollars into foreign hands. Moreover, there is reason to think that government transfers abroad, as Bretton Woods ($13 billion from 1948 to 1951) and our huge military spending abroad such as on overseas bases, are not always fully counted in current account stats when they ought to be (one reason is the US has very large black budget military spending). Those most assuredly have the same effect as trade deficits in getting dollars in the hands of foreigners. As you can see, the US was running a deficit from a gold perspective starting around 1960. Similarly, the growth of the Eurodollar market in the early 1960s was proof that dollar holding abroad were becoming significant.

When I took a required MBA course from George Cabot Lodge, Jr.’s son in 1979, he similarly discussed the joint budget and current account deficits of the 1960s as widely known fact.

A bit late to respond, and this discussion is buried so deep in NC that nobody will read it, but…

Good point on the gold connection which everyone seems to have forgotten. Right now I’m buried most days in the LBJ Presidentail Library here in Austin looking at 1964-66 ballance-of-payments/import of raw materials issues. LBJ was getting daily reports on our reserves of foreign currency to buy goods. Some days it was down to below $25 million which given the vast size of trade was essentially zero. He was strong-arming the banks to do a lot of pretending after the markets closed each day.

And we were using such “creative” methods to deal with the copper import cost crisis that we inadvertantly destabilized Chile and made it impossible for Great Britain to intervene in the Zambia- Southern Rhodesia independence crisis of 1965. I expect to submit an article on that for publication this fall.

And the “Black Budget” runs in both directions; long story I’ll save for later. HCL Jr.! That’s like getting to audit a class with Keynes.

Ancillary question – do you think this has anything to do with the recent Fed rate increase? Maybe countries with lots of US$ holdings were tiring of the choice between either low yield Treasuries or arcane higher yield assets with may have been designed by the likes of Goldman Sachs, etc. to blow up in the face of the purchasers. I just finished reading The Lords of Easy Money which is a pretty good overview for the layperson of how the Fed created the currently massive wealth gap. The amount of cash the Fed has pumped into the economy in the last couple years is truly astounding – don’t have the exact figures at my fingertips, but basically the Fed has created more more money in the last few years than in all the past history of the US. It’s amazing to me that after all that cash creation, which basically went to prop up the prices of a lot of dubious assets, coupled with ZIRP, the US$ is still worth anything in the eyes of the rest of the world. Sure feels like that is due to inertia more than any inherent superiority of the currency.

Side note: a pet theory on inflation after reading the above book. The recent bank bailouts during the pandemic were even bigger than those during the 2008 mortgage meltdown. The crucial difference – in 2008 the banks actually needed those bailouts to stay solvent (and I’m using the word “need” very loosely here, since I’m extremely opposed to bailouts not necessitated by force majeure situations, and maybe not even then when nationalization is an option). There were some restrictions in 2008, even if they were loose and not necessarily enforced. All that easy money essentially served its (dubious) purpose and more or less stayed out of the economy at large, and kept asset prices goosed. In 2020, with fewer restrictions on its actions, the Fed just pre-emptively shoveled trillions at the usual suspects whether they really needed it or not. This time due to the excess amount of the cash infusion, it did not stay withing the financial system and did make it into the economy at large, and at least in part caused the rampant inflation we see today. Clearly supply issues and other factors have also played a part, but surely Fed policy deserves its share of the blame.

So is it possible the Fed raised rates not only to slow inflation (using the only [bad] tool at their disposal), but also to try to keep the US$ relevant on the world stage considering how badly the sanctions against Russia have played out?

I don’t follow this stuff closely but just guessing – the reason ‘Europe’ (read its euro and dollar billionaires and their wholly owner politicians) are willing to shoot themselves in the foot and follow the US lead on Ukraine is ‘Europe’ too has decided to follow the US business model and offshore jobs – and the environmental pillage that is against the law in ‘western democracies’.

Maybe not to the extent of the US yet, but enough so they are willing to bet the farm (or at least other people’s farms) on doing what it takes to try to preserve dollar/euro hegemony. Having failed to break out of the dollar trap following the 1970s demise of Bretton Woods, the people holding all those “debts that can’t be repaid and won’t be” believe they have no choice but to continue supporting the system (AKA the rule of law) that ensures the money they and their politicians create will continue to be ‘accepted’.

It’s a common misapprehension that “Europe” has blindly followed the US in this area, but it’s not true. The European political class has a very deep-seated animosity to Russia, which represents for them the antithesis of the supranational normative Europe they are trying to build. (The UK is a special and even weirder case)

I suppose a ‘supranational normative Europe’ might work and even be a good idea – as opposed to the globalization that is burning up the world with its off-shoring of greenhouse gas emissions and transporting products produced by starvation wage labor halfway around the world. But, just as in the US with its MAGA crowd, Europe’s ‘deplorables’ are having trouble accepting they must starve or freeze for the sake of ‘peace’ so its elites can give Jeff Bezos millions to fly in space.

As for Russia, it seems to have a little trouble accepting its place in a ‘supranational normative Europe’ if that means just accepting its role as a natural resource and agricultural products supplier and being paid with ‘debt that can’t be repaid’ but can easily be confiscated when the interests of the global financial elites so require.

Am I missing something?

But at the same time European countries had economic relationships with Russia. For instance, it made better sense to trade NG from Russia via pipelines that LNG more expensively from any other place. As a matter of fact, it is possible to consider that having interdependence is best way to placate the bear but now Russia has all reasons to show being the demon we feared it might be. You might not agree with Mearsheimer but he says that in international organisations like NATO the big dog is typically the one that marks policy while the smaller can bark but will comply. In 2008 when under Bush Jr Georgia an Ukraine were announced to enter NATO, Merkel and Sarko, not being precisely pro-Russian types didn’t applaud but didn’t try forcefully to oppose the decision. Even the UK was hesitant though O.B. would never say a no to Master and Commander. So, saying blindly is quite possibly exaggerated but they might have tried some more resistance given the higher stakes in the EU about this. I think than now the whole European project as we know it is at risk and its Eastern flank (possibly others) will soon show fault lines while we are discussing the entry of the remains of Ukraine as a gesture for their sacrifice.

I’m still puzzled as to why the business interests in Europe have been so thoroughly cowed by the supposed political imperatives over Russia, but I’ve read a few sources that suggest that individually and collectively many industries assumed that one way or another Ukraine would be over and done with in 6 months, so they let the politicians and Russiaphobes run with it. They may have second thoughts about this once the leaves start turning brown (of course, it might be too late for this). I’m fascinated and horrified at how Germany has just thrown 50 years of co-operation with the CCCP and Russia over gas and minerals away in such a hissy fit.

I think its true that the big dogs of Nato and the EU have taken the running with this, but as we’ve seen, the veto does work (Hungary and Turkey over Sweden/Finland) and possibly Denmark/NL over Ukraine accession to the EU. I suspect that it is the smaller countries that will seek to reign in Germany in particular if they look to be about to blow the EU up in their determination to do whatever it takes to bring Kiev in the the EU.

Russia “defaults for the first time in over 100 years.” Technical default? Or related to the theft of what, $500 billion of Russian deposits by the “combined pirate West?” Financialization is a blimp with a big suction hose tether attached to the real economy, far as I can see.

What’s described, and of course difficult to see and absorb in its complexity, is what, MANDATORY and NECESSARY to conduct business transactions in real goods and labor? That system has collapsed and been refilled several times by recourse to the “full faith and credit” of the real economy of stuff and resources. Last really big one (the Great Depression) involved piracy of deposits by banks, which stole money and property on a large scale and then got all huffy when “depositors” had da noive to try to take their money, whatever that is, out of the banks. Had to get the chief pirates, the US government and central bank, to intervene (as I recall it) to “stabilize and restore confidence” in the confidence game that finance has become (as I see it.) and intervene again, to the tune of trillions of reserve currency fiat dollars, to prop up the superstructure that looks to have inherent instabilities and is subject to huge moral hazard, which the mopes have to underwrite, again and again.

My mind refuses to wrap around the notion of derivatives and related stuff. All of which seems to be an actually unnecessary and dangerous froth on the whole. And this is the stuff of which a trustworthy reserve currency is made? I guess it works so far, but to have faith in a system that produces people like C. Oran Mencik, https://www.chicagotribune.com/news/ct-xpm-1985-01-06-8501010832-story.html and Keating and Milken (the latter now completely rehabilitated just like Cheney and George Bush), https://en.wikipedia.org/wiki/Savings_and_loan_crisis, and many others who surf the wild financial waves? At some point the “sea of faith” starts to look like Lake Mead, https://abcnews.go.com/US/water-levels-lake-mead-dangerously-close-hitting-dead/story?id=85584196.

I know I am displaying my ignorance of the glorious, tranched and beautifully and advantageously complex space of “high finance,, but through my squinty eyes that’s how things look.

Well, JT, when the proles cannot buy food at a reasonable price, or there is no longer water in the commode, all the derivatives in the world will be worthless. High finance will be seen as Hijinx.

Tell me something I don’t know.

Finance, as part of the great neoliberal project, has stripped the country pretty bare, when it comes to making stuff and growing healthy food and sending potable water through pipes that don’t leach lead and “forever chemicals” into one’s iced tea. And what the mopes think of high finance is not worth a fig — the plutokleptocrats have rigged all the games, own all the edifices of legitimacy, enacted laws that render it “all perfectly legal, see?”

How much of all that complicated structure of mergers and share buybacks and credit default swaps and all those derivative transactions is in any way necessary to the basic functioning of a homeostatic political economy? Seems most of it is just froth generated by a predatory caste of finance mavens, generating phony dollars that too many of us are stupid enough to give them labor and stuff in return for. It’s become apparent that the only tool the Fed has to “whip inflation now” is to raise interest rates, which robs the already poor and kills jobs and funnels more money to the top tier. Well. Aside from the other tool of creating “facilities” of trillions of arbitrary dollars bulldozed into the banks and looters and corporate interests, to “save the economy” but only the part that has already stolen so much of the native wealth of the nation.

i got no idea how to fix this in any way that gives us suckers an even break.

Thank you for this post, Yves. Very illuminating for the likes of moi, Today is a great example why, for almost too many years, this blog and often the comments are my must read. Again, thank you for what for I view as a small island of sanity.

Could an exogenous event tip Humpty Dumpty $ off his throne?

Portugal had perhaps peaked and was on the downslope when an earthquake came calling in 1755-what effect would a similar 8.5 to 9.0 shaker in SoCal have?

In fact large gold coins of Portugal’s prior opulent era were called ‘Portugaloser’ no matter which European country, duchy, potentate, prince, king or queen issued them.

https://en.wikipedia.org/wiki/File:Erfurt_(German_States)_1645_10_Ducat_(Portugaloser).jpg

https://colnect.com/en/coins/coin/52203-5_Ducats_12_Portugaloser_-1587~1632_-_21st_King_Sigismund_III_Vasa-Poland_Gdansk

https://auctions.stacksbowers.com/lots/view/3-4QBV3/germany-hamburg-portugaloser-10-ducat-1689-ngc-ms-63

Thank you for this post, Yves. Very illuminating for likes of moi, Today is a great example why, for almost too many years, this blog and often the comments are my must read. Again, thank you for what for me is a small island of sanity.

What the financial froth has bought: https://www.lrb.co.uk/the-paper/v44/n13/iain-sinclair/diary

Thank you for this info, Yves. The US reserve status is strong because of strong securities markets; because of “the hard stuff of the financial securities markets, their constituent solid matter.” This is a very good description of the level of social cooperation required to have successful finance. It probably isn’t immortal, but stronger and more flexible than any other for now. What the US needs to do is create a level of employment, jobs guarantees and a good social contract that doesn’t interfere in the stability of the securities market so as to prevent high interest rates and unemployment which have a tendency to create suffering and inequality which in turn destroys sovereignty which in turn destroys currency. Because the future belongs to sovereign systems that can command social cooperation, imo. That means the world, all sovereigns, will have to do green planning and incentivize the circulation of money to keep the planet and the people healthy. It’s great to have a strong securities market, but it can only happen if the securities have intrinsic strength and that only comes from people and planet. It all depends how you spend all that “liquidity”. Money is as money does.

The little tidbit above about LBJ agonizing about sufficient foreign currency to get needed resources – copper being the example… this c. 1964 of course, was happening before we cut bait and dumped the gold standard in 1971. Or substituted the security of gold with the security of US Treasuries, aka the US Military. As John Conally (Treas. Sec) said to Nixon, (paraphrasing here) “If other countries don’t like it that’s their problem.” He could say that because we were a mega-buyer of all sortsa natural resources. If we had been so financially enlightened in 1964 we might never have gone crashing into Vietnam. It’s not so much that we have the “reserve currency” as we are/were a huge buyer, with plenty of industrial capacity. We are the Big Demand. Or were. That’s kinda over now. And our global military bases might become a drag on our diminished business model. Financialization has taken the place of war, not so much as the international extractor, but the international securitizer. Which makes sense as long as interest rates are low. Instead of going to war over various deprivations (or Wolfowitz anxieties of future deprivations), now we can pull out our multi-dimensional checkbook and do a balancing act that requires an advanced degree in calculus. But, I submit, it’s better than war. Look what a mess Ukraine is – it’s not accomplishing anything except pushing the EU away from Eurasia temporarily. Maybe.

This connected a few dots for me in my thinking on the subject really well. Thanks for the post

Dollar has been king for at least 75 years, and world trade runs on that. Such a big ship is slow to turn.

But 300b theft is enough for export surplus countries to ask, ‘what am I holding/saving $ for, given I’ve been running surpluses with the us for years? I’ll always get more. And maybe us is gonna want me to do something I don’t want to do…, and, now I think of it, while 300b is a record, there are other examples…’

I’ve heard China has been storing commodities for some time. Granted there’s a limit to that.

China has been urged to shift from exports to consumption. Perhaps an export tax could be used to improve universal health care and provide a retirement income to workers, persuading them to consume more and save less, both of financial assets and 2nd/3rd homes. This raises prices for importers (inflation) and probably shifts some low value demand away from China.

Imo the 300b issue begins a slow move towards balanced trade that will pick up speed over time. Our 800 foreign bases are an ‘import’. A big plus for me would be us discovering it can’t afford those bases or foreign wars. But fiat works on infra.

Separately, us/west militaries now know they can’t win a conventional war with Russia ( or China, given its army and industrial base), and that navies can easily be sunk from far away. The memo doesn’t seem to have reached the pols/think tanks, but it will. This means the realization nato is useless and that Russia is the power in Europe. Imo eu pop are working this out, but for policy to change leaders must be changed. Sadly, the us single party is not gonna offer anybody useful to non-oligarchs. Everybody runs on the platform ‘nothing will fundamentally change’.

Very interesting article.