Yves here. Actual data, something which is often not enough in evidence in discussions about China. The short version of this piece is quelle surprise, decoupling talk exceeds reality, even though some is happening.

By Caroline Freund, Director, Trade, Regional Integration and Investment Climate, The World Bank; Aaditya Mattoo, Chief Economist, East Asia and Pacific The World Bank; Alen Mulabdic, Economist – EFI Chief Economist’s Office The World Bank; and Michele Ruta, Deputy Division Chief International Monetary Fund. Originally published at VoxEU

Are the US and China decoupling? This column uses detailed US import data from 2017 to 2022 to shed some light on this question. It shows that some aspects of decoupling are real: US import growth from China was significantly slower than US import growth from other countries in the set of products subject to US tariffs. But there is no consistent evidence of reshoring or diversification of imports. In fact, supply chains – especially for strategic products – remain intertwined with China. Exporters that have replaced China in the US market have also increased their import-dependence on China.

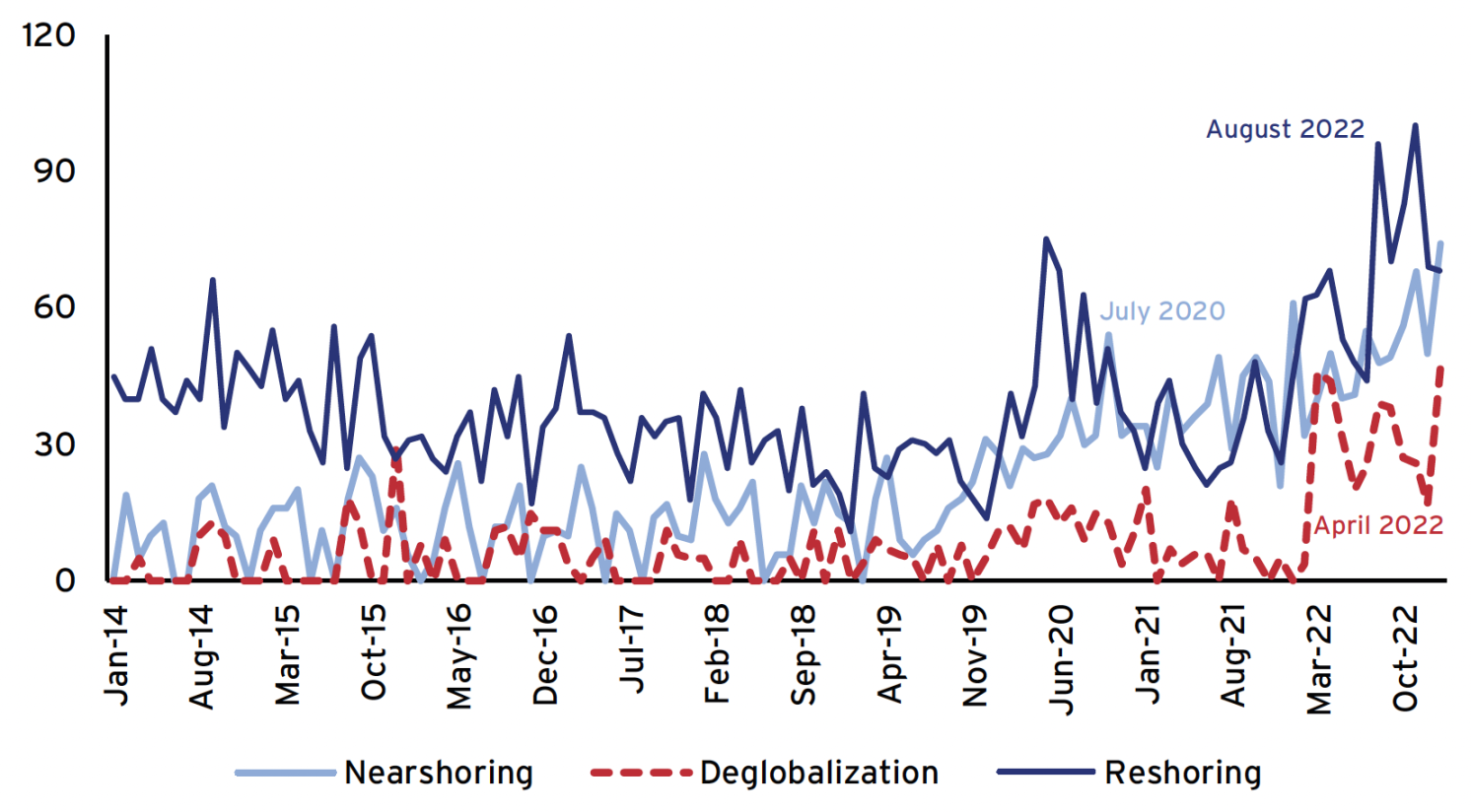

In the wake of US-China tensions, the supposed phenomena of reshoring, nearshoring, and deglobalisation are dominating the news. Google search trends show all three terms experiencing high levels of search activity since 2020 (Figure 1). The economic consequences of deglobalisation are a growing concern for policymakers (Aiyar et al. 2023, Aiyar and Ilyina 2023, Ottaviano et al. 2021) and economists have begun to estimate the economic costs for the world economy of different breakup scenarios (Bolhuis et al. 2023, Campos et al. 2023, Cerdeiro et al. 2021, Goes and Bekkers 2022, IMF 2023).

Figure 1 Google Searches for “nearshoring”, “deglobalisation”, and “reshoring”

Deglobalisation appears to be everywhere except in the (aggregate) trade statistics. Goods trade was at an all-time high in 2022, after years of slow growth. US imports in 2022 were close to 40% above pre-COVID levels, providing little support for the notion of reshoring. Even if we focus just on US-China bilateral trade relations, US merchandise imports from China in 2022 were more than 30% higher than levels in 2017, despite the tensions and the tit-for-tat tariffs imposed during the Trump administration.

In a recent paper (Freund et al. 2023), we investigate this disconnect between rhetoric and reality, focusing on the trade effects of the US-China trade war in 2018 and 2019. 1 In that period, US imposed tariffs on over 60% of imports from China, mostly at the 25% level (Bown 2023). We use granular trade and trade policy data from the US between 2017 and 2022 (i.e. pre- and post-trade war) and show that underneath the aggregate trends discussed above, trade and global supply chains are indeed responding to policy. US-China decoupling may be starting to take shape, but a close look at the data shows that this process may be unfolding in unexpected ways.

Five Little-Known Facts about US-China Decoupling

Let us start with a set of stylised facts illustrating how US trade policy is affecting trade and global supply chains.

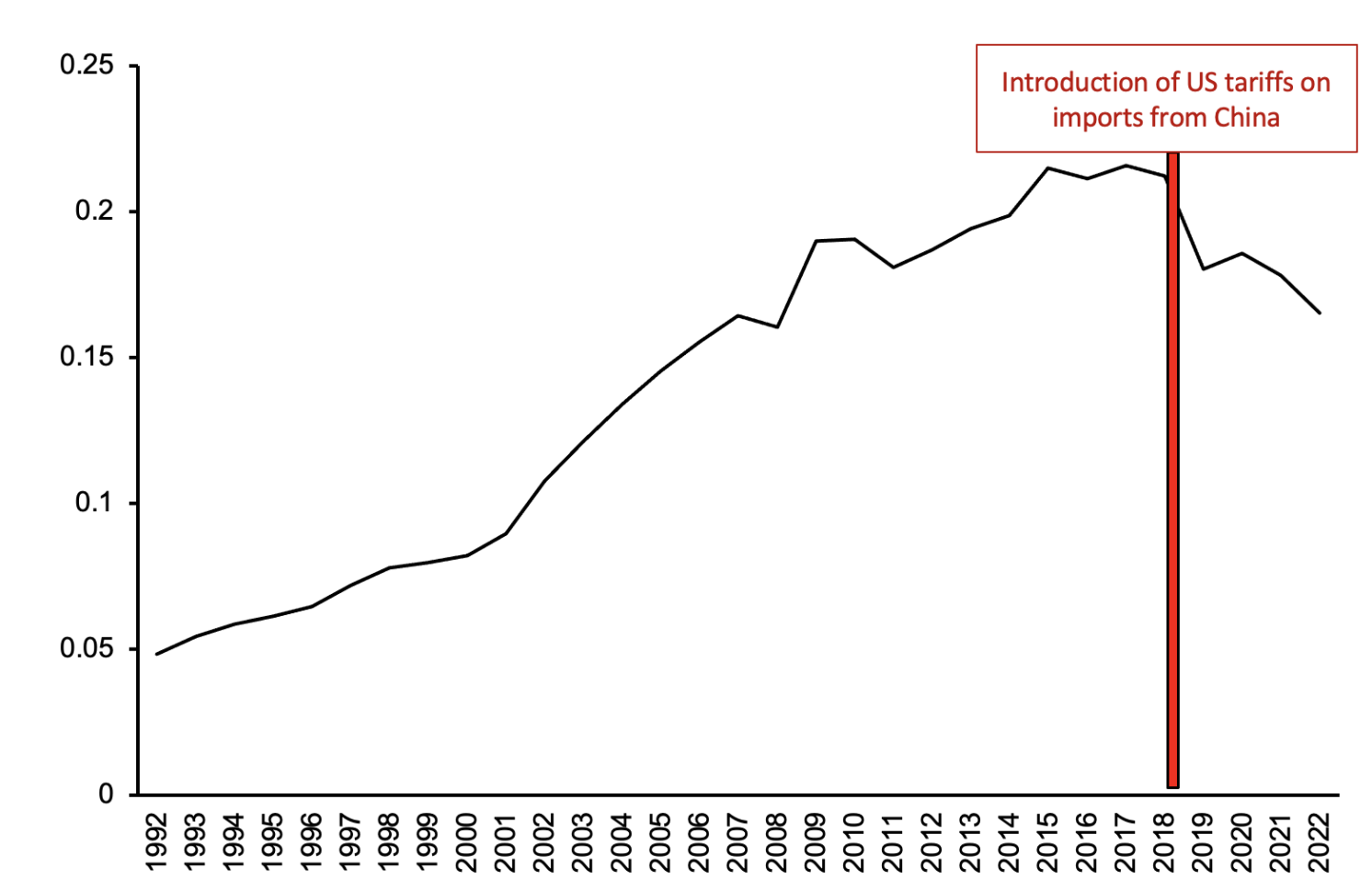

- First, US-China decoupling is happening as China’s share in US imports started declining in 2018 (Figure 2). China’s share in US imports fell from 21.6% to 16.3% between 2017 and 2022, and is now back at the level it was in 2007, before the global financial crisis. For strategic goods (i.e. the products the US government lists as Advanced Technology Products), this decline was dramatic, from 36.8% in 2017 to 23.1% in 2022 – a decline of over 13 percentage points.

Figure 2 China’s share of US imports

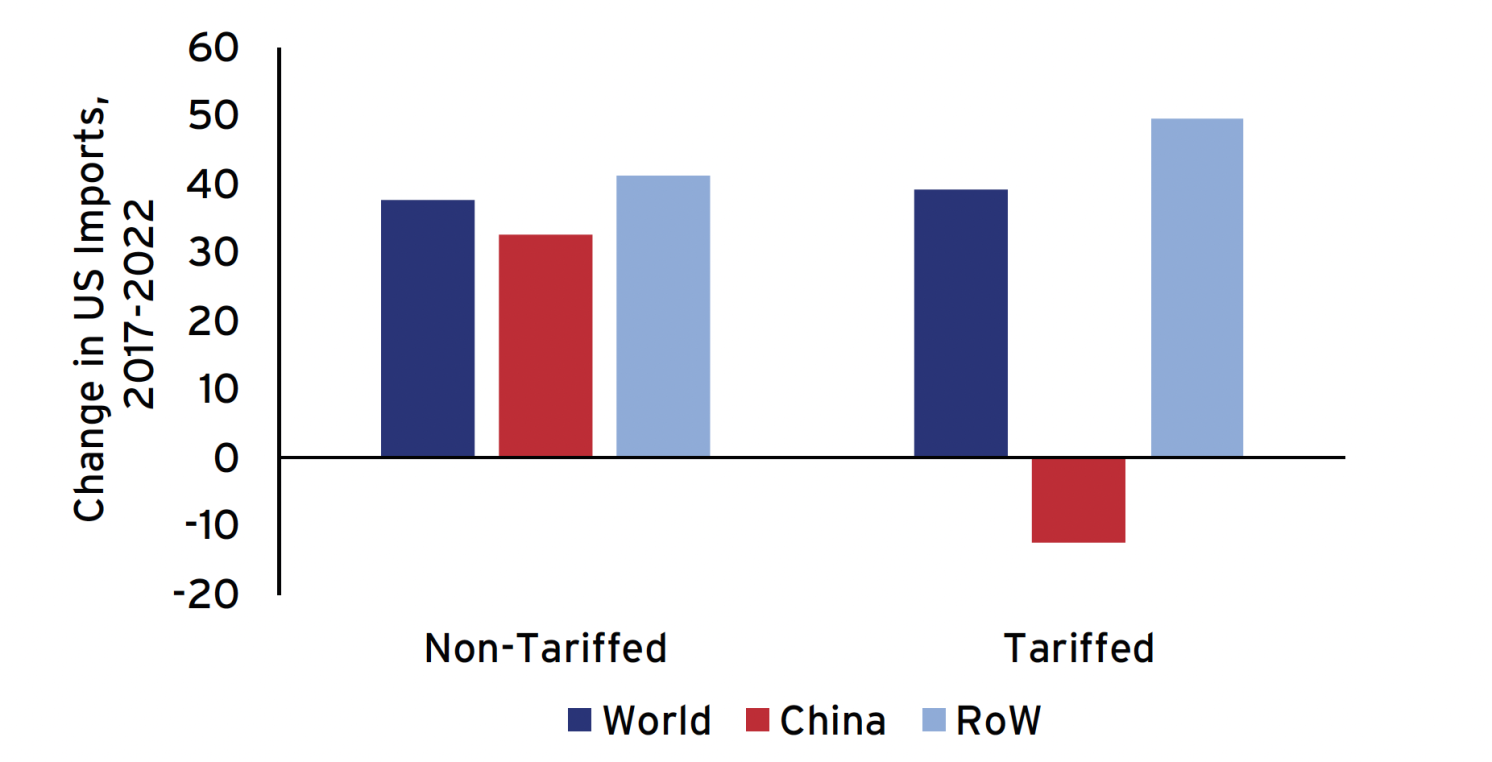

- Second, the decline in China’s share in US imports was concentrated in tariffed goods (Figure 3). In 2022, US imports from China in tariffed goods were 12.5% lower than in 2017, while imports from the rest of the world surged in those same products. No similar pattern can be detected in the products that were not hit by the tariffs, where the change in imports from China does not appear significantly different from the change in imports from the rest of the world. The sizeable reduction in China’s share in tariffed products and the increase in overall US imports together suggest that tariffs have induced importers to turn to new sources of supply.

Figure 3 Changes in US imports, tariffed and non-tariffed goods, 2017-2022

Source: US Customs

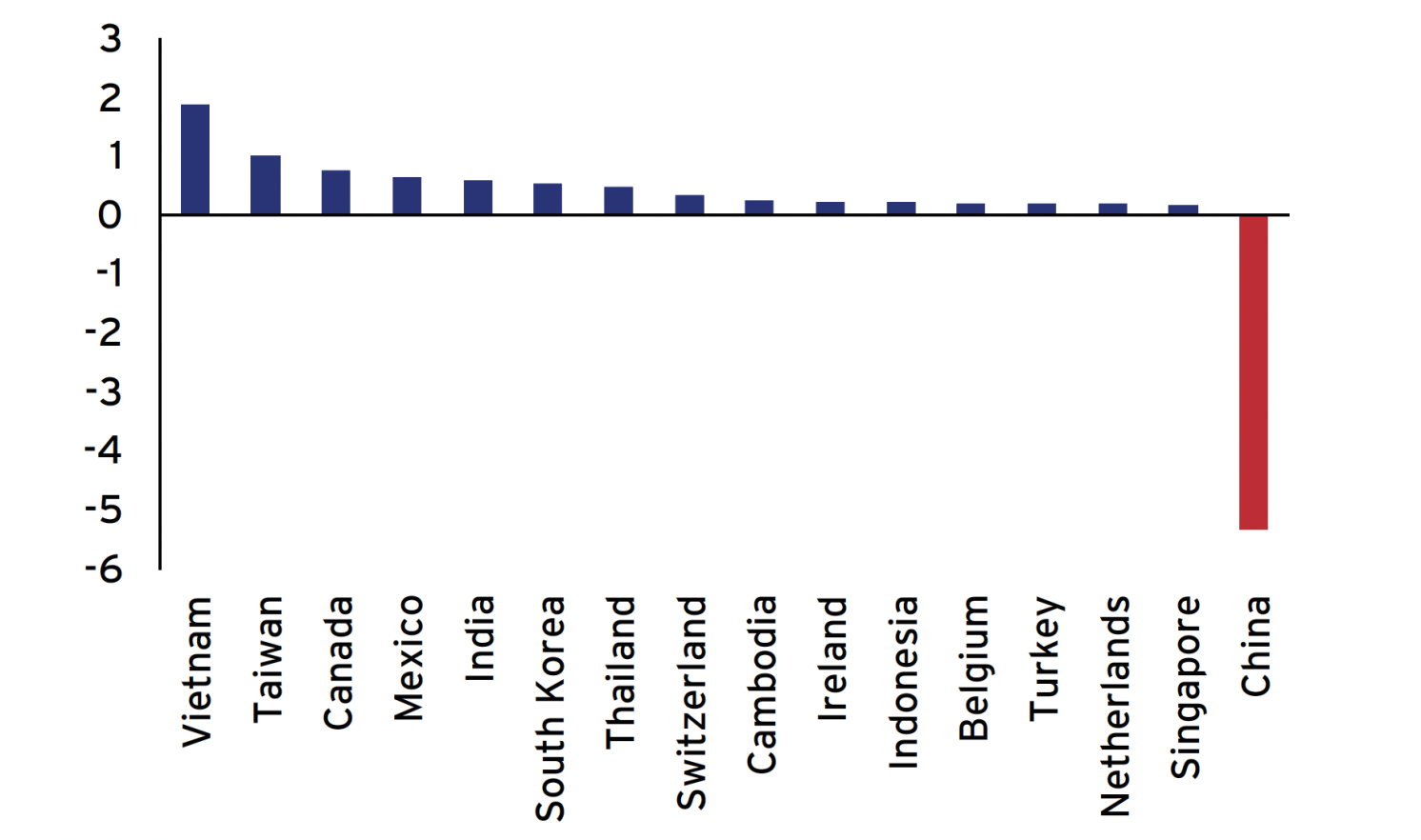

- Third, certain countries have more prominently replaced China in the US market (Figure 4). The figure shows prima facie evidence on the reshuffling of the top US trade partners from 2017 to 2022. Focusing on the overall shares, the countries with the biggest gains in market share were Vietnam (1.9 percentage points), Taiwan (1 percentage point), Canada (0.75 percentage points), Mexico (0.64 percentage points), India (0.57 percentage points), and Korea (0.53 percentage points). These six countries more than account for China’s 5.3 percentage point decline. 2 For strategic goods, Vietnam and Taiwan appear to have gained the largest market share in the US over the period.

Figure 4 Changes in US imports by partner country, 2017-2022

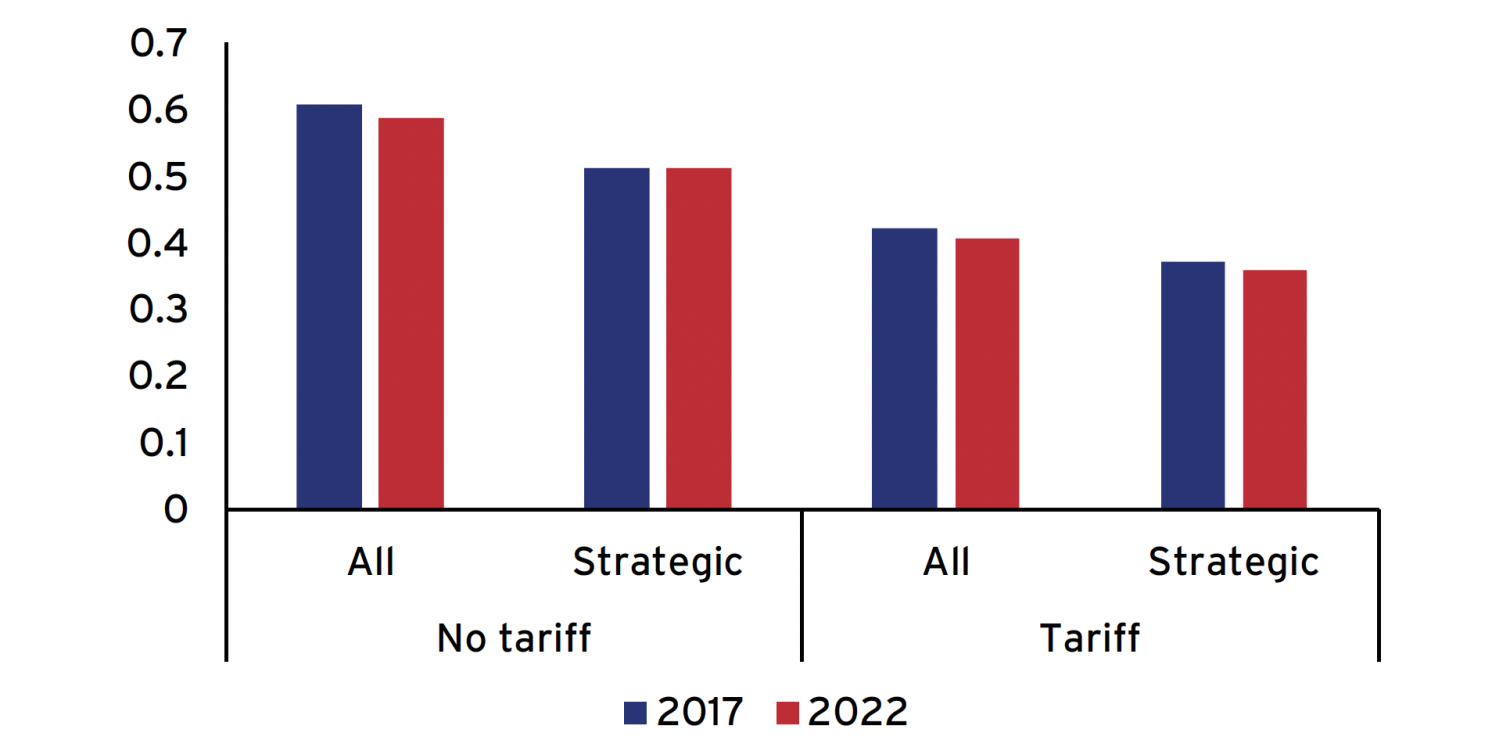

- Fourth, this reshuffling in US imports was not associated with an increase in diversification of US import sources (Figure 5). The average Herfindahl-Hirschman Indexes (HHIs) across products and time show little variation. Tariffed goods generally have a more diversified supplier base than non-tariffed goods (suggesting that limited diversification may not have been a key reason to impose the tariffs). But for both tariffed and non-tariffed products, HHIs have only marginally declined over the period, indicating that import diversification has remained fairly stable regardless of the imposition of the tariffs.

Figure 5 Average Herfindahl Indexes, tariffed and non-tariffed goods, 2017-2022

>

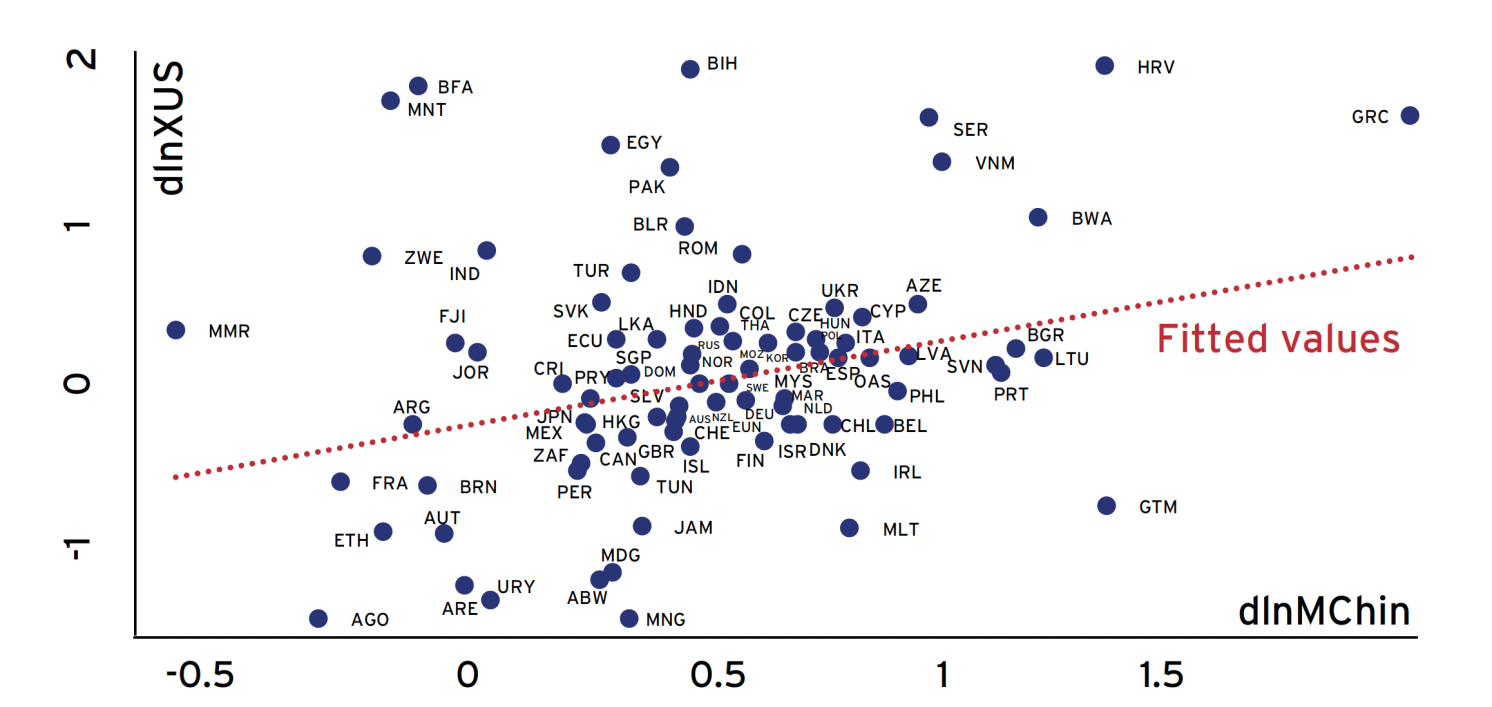

- Fifth, countries that exported more to the US, also increased their linkages with China (Figure 6). While China is being replaced by other exporters in the US market, the prima facie evidence points to the fact that US dependence on China may still be an issue. The figure shows that for electronics, the industry that contributed most to decoupling and which contains many strategic products, countries that increased exports to the US also increased imports from China in the sector. This high correlation suggests that linkages with China turn out to be especially important for those replacing China in the US market. Put differently, to displace China on the export side, countries have embraced industry-wide supply chains with China.

Figure 6 Trade in Electronics (HS85): Changes in exports to the US and imports from China

Tariffs Are Causing Decoupling, But Are Not Ending Dependence on China

In our recent work, we investigate these issues exploiting 10-digit import data at the country level from US Customs for 2017 and 2022. The analysis relies on a simple identification strategy. First, we focus on differences between trade in tariffed and non-tariffed goods, controlling for product and market characteristics. Second, we examine the country characteristics that are associated with replacing China, especially in strategic sectors. Apart from the change in imports from China, we also investigate whether the tariffs led to a diversification of imports, reshoring, nearshoring or friendshoring.

We find that the tariffs led to a decline in imports from China and stimulated export growth in other countries. But US import diversification of tariffed goods, or of goods with declining import shares from China, did not increase markedly. Given that overall imports in these products grew at rates similar to those of other goods, there is also little evidence that the US re-shored production. When we focus on strategic industries, defined as the eleven 2-digit sectors where the US government’s list of Advanced Technology Products reside, we find the impact of US tariffs on imports from China is higher. Though there is weak evidence of an increase in import diversification, there is no robust evidence of re-shoring even for these products.

Finally, we investigate which countries picked up the slack as US imports moved away from China. We perform a difference-in-differences analysis, comparing shifts in trade patterns of products where the import share of China fell markedly with the shifts in other products, while controlling for exporter and product specific time-varying shocks. We find that countries with revealed comparative advantage in a product improved their market share. We find evidence that countries that saw faster export growth to the US in strategic sectors also had more intense intra-industry trade with China in those same sectors. This finding is consistent with the view that the reshaping of US imports away from China in strategic sectors may not have reduced dependence on China as much as import numbers suggest. These countries also experienced faster import growth from China at the 6-digit level, which could reflect trans-shipment or additional supply chain effects. Other (non-strategic) goods conformed more to the predictions of a gravity model, flowing to large, developing countries that could offer competitive wages.

Conclusion

The evidence in our research highlights the tension between efficiency and decoupling. A full reshuffling of global supply chains is not only a long-term process, it is also costly and could only be induced by pronounced and prolonged government intervention. Moreover, decoupling in direct trade may only serve to deepen the indirect linkages between US and China through the industrial supply chains of their trade partners.

Authors’ note: This column will also appear as a chapter in a forthcoming CEPR ebook on Geoeconomic Fragmentation, edited by Shekhar Aiyar, Andrea Presbitero, and Michele Ruta.The views expressed are those of the authors and they do not necessarily represent the views of the institutions they work for.

See original post for references

So, now we order Chinese product through Vietnam and India to help end our dependency on China?

…

..

.

At higher prices no doubt. Supply chain Kayfabe at its finest, or maybe just BRI (Belt Road Initiative) in action.

its at the heart of the neolib catechism:”Transactions R Good”, therefore, maximalising the incidence of transactions is Better.

hence, the proliferation of Middle Men, all wetting their beak.

i derive this explicitly from this book:https://www.versobooks.com/products/2356-the-new-way-of-the-world

…which literally fell off the shelf at my feet at a Half-Priced bookstore in Sugarland, Texas…some 12-16 years ago.

Colonialism, mercantilism, liberalism, neocolonialism, neoliberalism. And are the neomercantilists lurking in the depths of corporatism where they control all the purchasing power of some very obscene “capital accumulation?” So to what end? Under the final logic of “Mother Nature always wins” a wise neo-ad-infinitum would be a saint. The transactional evolution of sustainability. If we are lucky. And it seems to require a generosity of capital. And neoliberalism has created an ocean of capital. And it has recently gone multi-lateral. Interesting times.

What makes it even more interesting is that Trump imposed the tariffs, leading to other countries getting involved in the supply chain, helping create and inflation that Joe Biden is getting blamed for. So it may be that Biden, by continuing the Trump trade stance, could help Trump get elected.

It’s like what Europe is doing when pretending not to be buying Russian oil and gas. They use intermediary nations like India.

Wasn’t the rhetoric during the Trump administration all about reshoring? They haven’t reshored anything haha. All they can do is move around the chairs on the Titanic.

Peter Lee’s latest Patreon missive (unlocked) after his just concluded trip to China, weighs in.

…”For me, the canary in the coal mine is Apple. My back of the envelope prediction is that total economic warfare against the PRC won’t happen until Apple has a flight path to exiting China and the US can bring out the big guns without cratering a US company whose valuation underpins a 10% chunk of NASDAQ and a big share of US retirement portfolios.”

https://www.patreon.com/posts/travelers-tales-88480944

Yeah, replacing a decade worth of factories and engineering expertise will be a pain.

And when that happens, all the equipment etc will be picked up by Chinese startups and established companies like Huawei.

There were already a video or two a some years back of how you could get a unbranded Apple phone assembled in Shenzhen from parts found in side street shops.

I would imagine that the Biden White House policy about decoupling from China would be based on their old foreign policy proposal to China. They went to them and proposed that they would cooperate with China on interests that they had in common with China but would otherwise criticize them on things like human rights while trying to put a spoke in their technological development. Oddly enough, the Chinese said no. So here, they are still trying to sabotage China’s technological development while trying to work out out how to disengage from China. As this would involve a multi-decade effort and would not only require an official US industrial policy but would also require investing in a well-trained American workforce receiving high wages, I think it safe to say that the Chinese can see that this will never happen. Certainly not under Biden’s watch.

Apple has moved some $8-12 Bn of production to Indian assembly lines and is growing it. Good for jobs, but does not move the needle in terms of China dependence for either Apple or India as over 90% of components (display/memory/screws/glue) still get made in China and the processor at TSMC. Btw Nokia had the biggest mobile assembly plant in the world some 15 years back or so in Chennai,India.

There’s more to it than that.

I bet many of the machinery in the Indian plants have parts that come from China. In my manufacturing experience, we may have the plants in North America for example, but critical subcomponents come from China. In our case, the tooling and dies come from China.

I’d bet that if the flow of goods from China stopped, even when the plants are in North America, producers would have to temporarily stop until they found other sources and often at much higher prices.

More importantly, the last few years have seen China become an innovator in many of the “capital goods” section. Not just price competitive, but now competitive, if not superior to the other nations’ alternatives on certain technologies. An example would be robotics, where for our application, they had made a very high speed robot that could boost productivity more than other companies from other countries.

China doesn’t dominate in top end capital goods across the board, but their dominance in certain cases is expanding with time.

This all goes back to Clinton’s actions on WTO membership for China and the PNTR. It gave the greenlight to corporate America to move production and sourcing to China wholesale, so to speak. Larry Summers is the epitome of this policy and yet at the start of Covid in 2020 he tweeted that he was incredulous America was facing supply problems on getting cotton-tipped swabs for nasal tests and why weren’t there factories here that could make them.

John Mearscheimer is flavor of the month for many PMCs who oppose the Ukrainian war but they ignore what he’s also been saying: the US support of China’s economic surge by opening America’s markets to Chinese imports and facilitating US manufacturers moving their facilities there will prove to be one of the greatest geopolitical mistakes of the last hundred years.

Pursuing that thought further, many China watchers are expecting Xi to move aggressively on ‘resolving’ the Taiwan question before his 3rd term ends in 2027. In 1941 the US was not dependent on German and Japanese exports for our economy to work.

Lenin wasn’t wrong when he said capitalists will sell you the rope to hang them withs.

I read a review of Carlos Martinez book “The East Is Still Red” (2023) wherein it was stated it that China deliberately chose the path of full integration with US globalisation – even prior to Clinton etc – as it was the best way to prevent the West’s historic impulse to hobble China….