Below we are republishing a 2019 post in which we excoriated the then Presidential candidate Kamala Harris for telling a whopper about her role in the get-banks-out-of-jail-almost-free card known at the National Mortgage Settlement in 2012. That deal was so bad that Gavin Newsom, at time the Lieutenant Governor of the Moonbeam Golden State, called it “deeply flawed” and “outrageous”.

Let us go back and explain why this settlement was so significant and how Harris and 13 other Democratic state attorney generals threw away a huge source of leverage with banks and mortgage servicers, which they could have used to extract much larger financial concessions as well are real reforms.

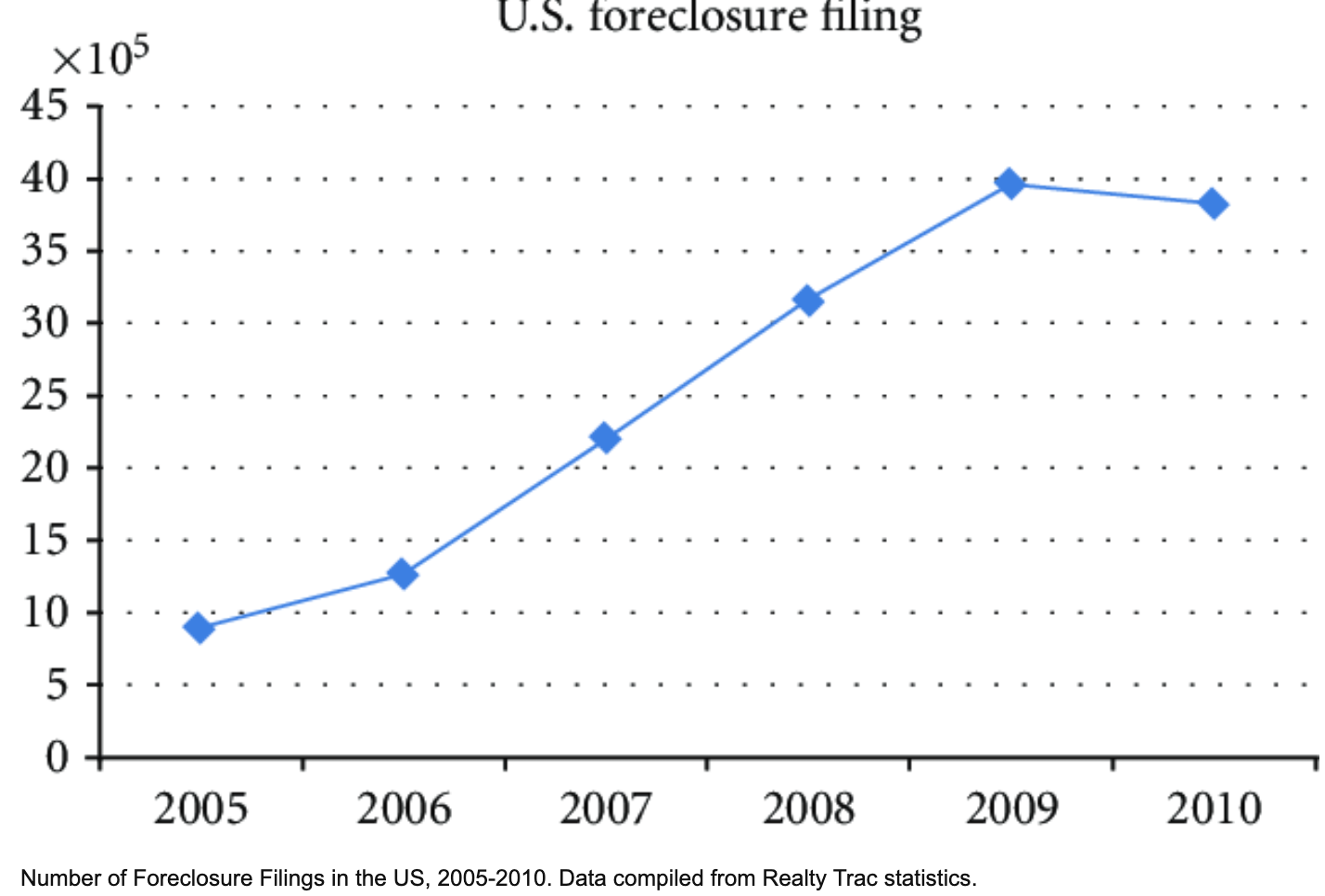

To this day, it is not well understood that Obama gave the banks a second monster bailout via this deal.1 Foreclosures kept rising after the crisis, peaking in 2009 and remained elevated in 2010.

To make a very long story short, some of these foreclosures were not warranted and many resulted in worse losses than a mortgage modification. This resulted from mortgage securitization and the rise of servicers who had no incentive to do their jobs all that well. In the hoary old days, the bank that issued your mortgage kept it on its books. When a homeowner got in arrears, the bank had an incentive to work out the loan if the borrower was at all salvageable.

Mortgage servicing was so bad that horror stories included foreclosures on homes where the borrower had never missed a payment, had never even had a mortgage, or the home had burned down and been paid off by insurance, yet the servicer was still pursuing the borrower. It was not simply that there were mistakes but that servicers would not fix them even when borrowers and their lawyers were persistent and provided documentation.

The looming problem was that servicers were paid to foreclose and not to make time-consuming mortgage modification. A group of loosely-affiliated lawyers who were defending borrowers discovered systematic flaws in how the mortgages had been securitized, calling into question whether the servicers were the party legally entitled to foreclose. And due to the rigid structure of the overwhelming majority of these securitizations, these problems could not be fixed via waivers or other actions. The robosigning scandal was an example of ex-post-facto but still impermissible efforts to remedy this mess.

These issues were not merely of documentation. They implied the securitizations had never been completed in the first place, meaning investors were holding a legal empty bag. As courts in many states, including some highly respected state supreme courts, validated many of the issues raised by foreclosure defense attorneys, it became clear to those watching closely that a tsunami of liability was bearing down on the originators of these mortgage securitications and the servicers.

The Obama administration had kinda-sorta woken up to the problem, forming a toothless effort to address the problem and work out a settlement. It was clear it was intended to be a sop to the banks. New York Attorney General Eric Schneiderman and 13 other Democratic state attorneys general, including Kamala, begin developing their own, more demanding, settlement deal, and it looked to have real odds of end-running the Federal effort (recall this makes sense because foreclosures are a state law matter). But Obama got Schneiderman to sell out for a mere seat next to Michelle at the State of the Union, and a promise to be part of a Federal task force. As we recounted at length, the Administration went out of its way later to humiliate Schneiderman. For instance, for months he had no office and when he got one, it had no phone.

As for the other attorneys general, if Kamala was the leader she pretended to be, with California being one of the most severely afflicted states, she could have stepped in after Schneiderman’s betrayal to lead the effort. Instead she got a few more gimmies to try to improve the stench of a bad deal.

This post first ran on January 10, 2019

The Big Whopper season is already upon us, in the form of presidential aspirants telling egregious lies about their track records. The Wall Street Journal tonight covers a section from Kamala Harris’ new book, in which she touts what a great deal she got for California homeowners in the so-called Federal-49 state National Mortgage Settlement in 2012.

The officials who played meaningful roles in the mortgage settlement negotiation should be run out of public life, rather than failing upwards, as Harris has. Hopefully, the millions who lost their homes to foreclosure will vigorously oppose her Presidential bid. But being a successful politician apparently means having no sense of shame.

Background: Why the National Mortgage Settlement Was a Bank Enrichment Scheme at the Expense of Homeowners and the General Public

In fact, as we and many others, like Dean Baker, Matt Stoller, David Dayen, Marcy Wheeler, Tom Adams, and Abigail Field recounted at the time, the settlement was a sellout to banks, a “get out of liability almost free” card. Due to widespread and probably pervasive corners-cutting during the mortgage securitization process, it appeared that the overwhelming majority of mortgages that had been securitized since the refi boom of 2003 had not had the mortgages conveyed to the securitization trusts as stipulated in the pooling and servicing agreements that governed these deals. Because these deals were designed to be rigid, for the ~80% that elected New York law to govern the trust, there was no way to straighten out these securitizations after the fact. Georgetown law professor Adam Levitin called these agreements “Frankenstein contracts” and argued that what had happened was “securitization fail,” that the securitizations had never been properly formed and thus the investors had bought what amounted to legal empty bags. Mind you, someone did have the right to collect the interest and principal from the mortgages, but that “someone” didn’t appear to be the servicers acting on behalf of the securitizations.

Nevertheless, in an early manifestation of what Lambert later called “Code is law,” everyone acted as if things had been done correctly. And weirdly, this might never have become a problem were it not for a tsunami of foreclosures. The dirty secret of mortgage servicing was it had been set up to be a high-volume, highly routinized business, which it could have been if servicers were dealing with on-time payments. But every time a servicer had a portfolio with a lot of delinquencies and defaults, it wound up engaging in a lot of fraud because it wasn’t paid enough to foreclose well, and certainly not enough to modify mortgages, as banks had done as a matter of course back in the stone ages when they kept mortgages on their books.

The securitizers and servicers all acted as if they could do the paperwork needed to convey the mortgage to the trust properly if and when they needed to foreclose. The wee problem with that was that for a whole bunch of good legal reasons we won’t bore you with (but we covered in gory detail back in the day) the mortgages had to have gotten to the trust by a date certain….which was inevitably well before the foreclosure. Only a time machine could fix this problem.

Servicers and foreclosure lawyers engaged in all sorts of creative frauds to try to make everything look OK. But with servicing so automated, botched, and too often deliberately abusive, quite a few of the people being foreclosed upon should have been salvaged. It would have been better for everyone, the investors, the homeowners, and the communities, except for those servicers (well, there was another bad incentive that we’ll get to in a minute). And many of the people who were foreclosed upon had missed only a payment or two, or would have been able to remain current with only a modest payment reduction. But some servicers like Wells Fargo would “pyramid” fees, impermissibly deducting a late fee first from borrower’s payment, guaranteeing that one late payment would result in all future payments being “short” and therefore late too, leading to more late fees.

And that’s before you get to mortgage horror stories of bad records combined with servicer refusals to make corrections. Foreclosures on houses that had never had a mortgage. Foreclosures on houses that had burned down where the servicer refused to take the insurer’s settlement check. Foreclosures by institutions the borrower had never dealt with. Foreclosures by multiple servicers on the same home. Foreclosures on active duty service members, which was prohibited by law.

Some homeowners who wanted modifications, aided by a small group of attorneys and activists, started to document the colossal mess of mortgage securitizations. Even though they usually lost in court, a few important cases did get to appeals and even state Supreme courts, and enough precedents were being set that the media was starting to treat the issue of foreclosure fraud seriously. It became national press in the fall of 2010 when GMAC halted all foreclosures due to what came to be called robosigning (which actually wound up being a huge break for the servicers, since it focused attention on false affidavits, which the banks spun as a mere paperwork problem for foreclosures which otherwise supposedly should go forward).

A sign that the problem of “securitization fail” was being seen as credible was when the Congressional Oversight Panel gave the issue prominent play in one of its reports.

Obama authorized a mortgage settlement initiative that was languishing in 2011. However, New York attorney general Eric Schneiderman and a group of about 14 other state attorneys general started working on a more ambitious settlement. Schneiderman’s campaign was gaining ground as of late 2011.

In early 2012, Obama succeeded in suborning Schneiderman. His price was getting to sit next to Michelle at the State of the Union Address and becoming co-chairman of a national mortgage task force that proved to be a complete joke. As we wrote in April 2012:

It was pretty obvious Schneiderman had been had. Obama tellingly did not mention his name in the SOTU. Schneiderman was only a co-chairman of the effort and would still stay on in his day job as state AG, begging the question of how much time he would be able to spend on the task force. His co-chairman is Lanny Breuer from the missing-in-action Department of Justice. And most important, no one on the committee was head of an agency, again demonstrating that this wasn’t a top Administration priority.

The Administration started undercutting Schneiderman almost immediately. He announced that the task force would have “hundreds” of investigators. Breuer said it would have only 55, a simply pathetic number (the far less costly savings & loan crisis had over 1000 FBI agents assigned to it). And they taunted him publicly by exposing that he hadn’t gotten a tougher release as he has claimed to justify his sabotage….

Mortgage Settlement Monitor Hires Firm that Has Worked on Countrywide Matters

But why, you might ask, was the settlement so bad? The headline amount was $25 billion across all banks and servicers, versus the potential liability of blowing up not just private mortgage securitizations, but even Fannie and Freddie deals. This was a meteor-with-the-potential-to-wipe-out-the-banks level liability. The Administration had all the leverage in the world to dictate terms. And instead it did what it liked to do best, a bailout with some gimmicks to improve the optics.

The banks didn’t come close to paying $25 billion. The cash portion of the settlement was under $5 billion. As we pointed out at the time, “That $26 billion is actually $5 billion of bank money and the rest is your money…That $5 billion divided among the big banks wouldn’t even represent a significant quarterly hit.” Contrast that with the $8.9 billion that one bank, BNP Paribas, paid to settle money laundering charges.

The rest was made up of non-cash items which cost the banks at best 10 cents on the dollar. It included giving them credit for things they were going to do anyhow, plus giving the banks credit for modifying mortgages they didn’t own, as in imposing costs on others.

Here’s one indicator of how well the settlement worked: Just 83,000 Homeowners Get First-Lien Principal Reductions from National Mortgage Settlement, 90 Percent Less Than Promised. And that gets to how the Administration likely rationalized it. Many of those securitized mortgages also had second mortgages on the same house. According to the lien priority, the second has to be modified first, and it has to be wiped out entirely before any modification of the first is to take place.

However, while banks securitized 75% of their subprime mortgages right before the crisis, they kept most of the seconds on their books. Yet the settlement explicitly allowed the seconds to stay put as the banks modified the firsts. From a February 2012 post:

As we had indicated earlier, one of the many leaks about the settlement showed that there had been a major shift its parameters. Of the $25 billion that has been bandied about as a settlement total for the biggest banks, comparatively little (less than $5 billion) is in cash. The rest comes in the form of credits for principal modifications of mortgages.

Originally, that was to come only from mortgages held by banks, meaning they would bear the costs. The fact that this meant that whether a homeowner might benefit would be random (were you one of the lucky ones whose mortgage had not been securitized?) was apparently used as an excuse to morph the deal into a huge win for them: allowing the banks to get credit for modifying mortgages that they don’t own.

The first rule of finance (well, maybe second, “fees are not negotiable” might be number one) is always use other people’s money before your own. So giving the banks permission to modify loans they don’t own guarantees that that is where the overwhelming majority of mortgage modifications will take place, ex those the banks would have done anyhow on their own loans. And the design of the program, that securitized loans will be given only half the credit towards the total, versus 100% for loans the banks own, merely assures that even more damage will be done to investors to pay for the servicers’ misdeeds.

Let me stress: this is a huge bailout for the banks. The settlement amounts to a transfer from retirement accounts (pension funds, 401 (k)s) and insurers to the banks. And without this subsidy, the biggest banks would be in serious trouble

Why? As leading mortgage analyst Laurie Goodman pointed out in a late 2010 presentation, just over half of the private label (non-Fannie/Freddie) securitizations have second liens behind them (overwhelmingly home equity lines of credit). Moreover, homes with first liens only have far lower delinquency rates than homes with both first and second liens. Separately, various studies have found that defaults are also correlated with how far underwater a borrower is. If a borrower is too far in negative equity territory, it makes less sense for them to struggle to stay current, no matter how much they love their home.

The second liens pose a huge problem to the banks. Courtesy Josh Rosner, this is data as of September 30 for Citi, Bank of America, JP Morgan, and Wells, respectively:

Compare these totals with the book value of their equity as of the same date: $42 billion in seconds for Citi versus $177 billion in equity; BofA, $121 billion in seconds versus $230 billion in equity: JP Morgan, $97 billion in seconds versus $182 billion in equity; Well, $109 billion in seconds versus $139 billion in equity. One of my mortgage investor mavens says that BofA’s seconds should bve written down by about $100 billion and JP Morgan’s by $60 billion. That writeoff would exceed BofA’s market cap and would make a major dent in Jamie Dimon’s touted “fortress balance sheet.” And a similar magnitude of haircut to Wells would expose it as being grossly undercapitalized.

And as Matt Stoller documented, one of the big ways that the settlement got better press than it deserved was that the states used some of the cash they’d gotten to buy off housing activists. Those organizations are chronically budget starved, so it took remarkably little to purchase their acquiescence.

Now you might be saying, “I understand how the settlement might have hurt people who were facing foreclosure. But I wasn’t one of them. How can you say it hurt me?”

Foreclosures hurt state and local tax revenues. A foreclosure depresses home values in the neighborhood, usually by 10%. Banks would typically do a terrible job of securing and maintaining the property. Private equity firms later swept in and tried acting as a landlords of single-family homes. For the most part, they did succeed in raising rents, but most have proven to be poor landlords, and don’t do a good job of maintaining the houses, even neglecting to address leaks, which do fast and serious damage. Having transient residents and not-well maintained properties isn’t good for housing values in the long term.

Kamala Harris’ Dodgy Role

Now it is fair to say that Harris got a better deal for California than the other state attorneys generals got. But that is what the Japanese would call a height competition among peanuts.

Ms. Harris writes that under the initial settlement offer, California would have received between $2 billion and $4 billion, calling it “crumbs on the table” that would have failed to properly compensate homeowners…

Ms. Harris describes a testy phone call in early 2012 with Mr. Dimon as they discussed the deal. “We were like dogs in a fight,” she writes.

“‘You’re trying to steal from my shareholders!’ he yelled, almost as soon as he heard my voice,” Ms. Harris writes of Mr. Dimon. “I gave it right back. ‘Your shareholders? Your shareholders? My shareholders are the homeowners of California! You come and see them. Talk to them about who got robbed.’”…

Two weeks later, Ms. Harris writes, the five banks relented and eventually agreed to a settlement that year of $26 billion, which ultimately provided about $50 billion in gross relief to homeowners. California’s share of the deal reached $20 billion in aid to the homeowners, a significant increase over the original settlement offer. The agreement involved 49 states and the District of Columbia and five major banks: Bank of America Corp. , Citigroup Inc., JPMorgan Chase, Wells Fargo & Co. and Ally Financial Inc.

This is nonsense. Harris did get a good bit more for California but the claim that she was responsible for a ginormous increase and that the total value of the settlement was on the order of $50 billion is unadulterated tripe. The larded settlement gross number was up to $19 billion with New York and California still dickering. Even though California, by virtue of having more foreclosures than any other state, did have more leverage than other states, Schneiderman filed a MERS suit that got folded into the settlement that also resulted in more concessions.

Curiously, Harris does not mention that Governor Jerry Brown raided most of the settlement money and diverted it to fill state budget gaps, with the legislature’s approval. Last year, a state appeals court ordered California to use the funds for their intended purpose: to help victims of foreclosures. This is now so many years after the fact that any monies will come after the former homeowners are past the point of their most acute distress.

But the piece de resistance comes from a Jacobin story on Harris’ record:

At the time [when Harris decided to push for a better deal], Harris was under pressure from union leaders, other politicians, and housing rights activists. As one member of the progressive coalition of groups put it, “It wasn’t like she was some hard-charging AG that wanted to take on the banks” — rather, “it took a lot of work to get her where we needed her to be.” Harris withdrew the day after these groups sent her a letter, signed on by Lt. Governor Gavin Newsom, a potential future rival, calling the deal “deeply flawed” and “outrageous.”

Even a Wall Street Journal reader was offended by the article:

Daniel Skoglund

MAGA idiots spamming this thread with BS talking points.I’m a “librul”, and I detest Harris for legitimate reasons:

-Didn’t prosecute Steve Mnuchin when she was CA AG.

-Is meeting with Wall Street donors while she claims to be AGAINST Wall Street?

-Endorsed Hillary and met with her donor network.She’s another corporate Democrat. I’m interested in grassroots people.

EDIT: Also, Hillary was rumored to make Jamie Dimon her Treasury Secretary, who apparently Harris despises, but she was okay with endorsing her? lol…

And if you need more proof of Harris’ puffery, we have lots more evidence in our archives. Some examples:

The Top Twelve Reasons Why You Should Hate the Mortgage Settlement

Abigail Field: Hiding the Enforcement Fraud at the Heart of the Mortgage Settlement

If this is the best story Harris has to tell, it doesn’t bode well to her holding up under meaningful oppo.

_____

.1 It is a mistake to think that Obama did not play a role in the rescues while Bush was still President. Obama and McCain were included in major Treasury briefings about rescue scheme after Lehman failed. When the first version of the TARP received fierce criticism from all across the political spectrum and Mr. Market went into another swan dive, Obama whipping for the second version was critical to its passage. As for QE (and do not tell me the Fed was independent during the crisis; the Fed and Treasury were coordinating tightly on salvage operations) for those who bothered listening to Bernanke, QE was to lower mortgage interest rates and their spreads over Treasuries. That was to try to goose housing prices. Borrowers who were in financial stress due to having lost their job or having their hours or pay cut would be less motivated to struggle to keep their house if it was deeply underwater (this is not theory; data at the time bore that concern out)

There is no worse State AG during “fraudclosure” that Massachusetts then State Attorney General who had Massachusetts case law behind her back to destroy the banks engaged in the practice. She folded like the cheap suit she wore back then.

Side note: She also was the AG who allowed Steward here in MA to takeover from Cerberus in 2011, after a $10K donation on her failed Senate run. Plenty of ink on the now $MPW/Steward debacle and hospital closures.

The fact that there was someone uglier, here Martha Coakley, in the beauty contest between Cinderella’s sisters, does not exculpate Kamala. Coakley did not have the Democratic party help her fail upwards after that.

Don’t let Governor Deval Patrick off the hook, either!

Nice timing on bringing up the Steward acquisition, they’re trying to shut Carney Hospital in Dorchester right now, after running it into the ground for a decade!

Wash, rinse, repeat…Dorchester, what we used to call “a poor neighborhood.” But, hey, we’re all woke now, and you have Maura Healy and Michelle Wu as gov and mayor, so it’s all good. Do a futile scan of the Boston Globe for a mention of Cerberus – “Your partner to improve performance and drive value.” Rather let’s pound on this Dr. de la Torre who spent a gazillion on a yacht instead of improving health care. Bernie is pounding this guy on social media…thanks Bernie…we needed a fall-guy.

As it turns out a bankruptcy judge just approved the closing of Carney and Nashoba Valley Hospital out in Ayer. Cerberus owns another half dozen healthcare facilities around the state. The state should take all of their hospitals under the Eminent Domain clause. If you mentioned that possibility, the pols would all have strokes and would need hospital care. In which case the mental health of the people of the Commonwealth would improve immediately.

But the whole thing was trouble from the start, which even I as someone without expertise in the field could see. I don’t think the hospitals were ever on the best ground, serving people in rural areas, poorer cities, suburbs, and neighborhoods, while the wealthy and the politically connected goes to the Harvard-affiliated “non-profit” hospitals. Funding for the safety net hospitals is less than for the research hospitals, and they are more reliant on Medicaid and Medicare so whenever the state plays games with reimbursement, which they often do, they are put on even worse footing. Yet someone the entire political leadership, Democrats and Republicans (one example had Obama holding Steward as a positive example), chose to ignore the hospitals, their employees, and patients.

Despite being barely competent and a friend of the super rich, Harris will win the election because she is neither of the above.

She will continue to do nothing for the poor, the vulnerable, the workers, she will keep aiding capitalists and the fossil fuel industry to rape the planet. As I have said before and as The Republic said, US democracy is far from fixed

…and how does this compare with other possible candidates? Name me a potential candidate for President now on the national scene who will ever do anything for the poor, the vulnerable, the workers…

Dr. Jill Stein?

I meant a candidate who might actually win.

Best line in the story: “In early 2012, Obama succeeded in suborning Schneiderman. His price was getting to sit next to Michelle at the State of the Union Address and becoming co-chairman of a national mortgage task force that proved to be a complete joke.”

If enough people vote for her, she will win. Fact.

The problem is, people let how they think others will vote affect their own vote.

And, if Caleb Maupin is right, she’ll start more color revolutions all around the world. Jimmy Dore, 4+minutes, utube.

Kamala Harris Is Hillary Clinton’s Hand-Picked Successor! w/ Caleb Maupin

https://www.youtube.com/watch?v=4X0S58es_WE

Thank you for reposting some of NC’s coverage of the ‘mortgage crisis.’ Every since the people have nominated Kamala Harris to be the D’s candidate in the 2024 Presidential election, I have had this niggling little thought at the back of my mind: didn’t NC write about the sellout of California’s AG during that crisis? And wasn’t Harris said AG?

I was absolutely glued to NC during that period. We were living in Denver, where rising home prices and influxes of new residents buying homes, led to large numbers of foreclosures. We had relocated from Long Beach, California a few years before, where the infamous Countrywide Mortgage (prime purveyor of NINJA loans) had a busy branch office next to the neighborhood grocery market.

At one point, our activist group ‘disrupted’ one of the frequent and heavily-attended Denver County foreclosure auctions: picture a ‘committee’ of enormous black vultures huddled in rows at the County Building, panting to feast on the crushed remains of homeowners’ hopes, harassed by a group of sparrows (led by the portly Jewish chairman of Denver’s Communist Party.)

I believe you wrote quite a bit on the suspect and newly developed computerized system to keep track (hah!) of the mortgages that had been sliced, diced and repackaged.

Kamala also did nothing as AG when the CALPERS Apollo scandal sending ExDir to Prison and a Trustee to commit suicide, you probably have much more detail than I do it on this.

Uh, I believe Florida is the “Sunshine State”. Perhaps Yves meant to write “Moonbeam State”?

Haha, fixing! Golden State!

Show me the California graph.

Now it is fair to say that Harris got a better deal for California than the other state attorneys generals got. But that is what the Japanese would call a height competition among peanuts.

That was the headline amount which was larded up with credits both at greatly inflated value and that never happened. The economic value was $5 billion at the outside. We went through that in gory detail in other posts.

This versus the liability of securitizations where the loans were never transferred properly to the securitization trusts and could never be, given the rigid-by-design contracts, absent a time machine.

Pull out a calculator.

Subprime market of $1.3 to $2.1 trillion (the bigger # is if you count the Alt-As).

About 80% elected New York Trusts, which no way no how could be fixed via waivers or any later remedies.

The liability is in theory 100% since the mortgages were actually never transferred to the mortgage trusts, so even the payments on non-defaulted mortgages were fraudulent.

That is before additional torts created by bad servicing.

If you assume 100% liability on the total, you have $1 trillion to $1.7 trillion.

If you decide to haircut that by the roughly 40% foreclosure rate on these mortgages, you get to $400 billion to $670 billion.

And keep in mind these numbers are big enough to put a lot of players in severely undercapitalized mode, as in in need of explicit bailouts or liquidations.

So yes, the banks got a huge gimmie. Even if they got only a financial wet-noodle lashing, they should have had a boot put on their neck in terms of reforms.

Excellent summation. The numbers got very large in such a short period, between 2003 to 2007. I’m always remembering not in a good way the events of September 2008…and the tumultuous period leading to that moment. Morgan Stanley was still very much on the brink as of middle October even. Treasury Secretary Paulson sure saved a wide swathe of finance professionals from feeling legitimate and harmful unemployment.

Hank Paulson. “No bailouts for Lehman!”

Hank Paulson on Tuesday. “Holy crap, gotta save AIG! Hand me a napkin, I’ll put my best plans together using duct tape and glue to Save Our Bankers.”

>Save Our Bankers.”

I understand SOB to mean Sons of B*****

In the casino we all live in, the house always wins. What more is there to say? I look back on the 2008 crisis and its aftermath now and mostly think how, at that point, this idea that the state and the market were in any way separate or that the law and rules meant anything when the house itself was faced with losses (literally when the term “to big to fail” was coined) died an ugly death. It should have put to bed this notion that there was ever anything resembling a “free market” that functioned according to a set of iron clad principles and rules to bed once and for all. After that, if you had your head on straight, you knew the rules would be rewritten on the fly until the oligarchy that really runs this country considered whatever losses were being imposed on it were acceptable.

More relevant to today, I used to get propaganda in the mail here in MN complaining about Nancy Pelosi implementing a “radical agenda,” and this is the same line of attack Trump seems to be taking against Harris. I can only think “in what world are any of these people radical.” It harkens back to the days when the Tea Party crowd legit believed Obama was a “communist,” when be barely qualified as a center-right neoliberal.

These days I’m mostly just tired of pretending as if these elections weren’t a hideous farce, or as if we have any meaningful input on policy or legislation as voters. We’re just straight up going through the motions. The two major parties pretend to listen to us and we pretend like we’re still in charge.

Roquentin. Exactly right.

Thanks for this post. A good reminder.

IMO, it is like the opiod settlement in that states AGs don’t really sue on behalf of individuals who were victimized by industry. They sue for the benefit of the state; the benefits are for the state, which was also injured (it feels). It is not trying to redistribute money back to injured individuals. The state sues on the behalf of its “population” which has been decimated (it feels), and cost them money in services for cleanup, which is a whole other thing. Individuals may be witnesses and victims cited by the state, but that doesn’t mean the state is going to make them whole with some kind of reparation. That was never their intention. They do not protect individuals from their individual contracts or activities. Nor do they want to be accused of redistributing tax payer money. They are just trying to cover their own budgetary losses.

I am sorry to come down on you despite your effort to offer what you thought was useful background. But I take umbrage at being straw manned. It appears you did not read the post or my other comments with care.

The liability resulted not from losses to homeowners but from a massive level of empty-bag securitizations. All states have their own securities laws and their own securities regulators. These are securities law violations by the issuers, who all sold paper in their states. Non-bank mortgage servicers must be licensed in every state in which they operate. Some states require that all mortgage servicers be licensed.

In addition, the desired restitution was not to get homeowners payouts for bad foreclosures (although there was an effort to do that for certain 2009 and 2010 foreclosures and we wrote a monster series on what a cock-up that was) but to get mortgage modifications and better servicing going forward. That was a big demand, since good servicing costs money and good default servicing, even more so).

This brought back at least two fundamental issues that plagued me, as a starry-eyed Pollyanna:

-please produce the ink signed promissory note;

-please bring Linda Green here with her ID, a pen and piece of paper

Fraud. I have converted all my debts to being non-assignable , held locally by small community banks.

Robo-signing, another addition to the lexicon.

“Mortgage servicing was so bad that horror stories included foreclosures on homes where the borrower had never missed a payment…”

Fond personal memories indeed. My bank was trying this one with me. I applied for a loan modification, which they kept telling me would be shortly forthcoming, and encouraging me to not pay the monthly. Advice that I ignored and there was in fact no loan modification in the works. For several months my mortgage payments, although paid, didn’t get posted as received, and foreclosure was threatened. I finally got our then congressman, Pete Stark, involved. His staff were most helpful and got the matter straightened out.

Bravo! It’s almost like some banks were running their version of an online scam, you know the ones, sort of like this:

How One Man Lost $740,000 to Online Scammers Targeting His Retirement Savings

https://www.nytimes.com/2024/07/29/business/retirement-savings-scams.html

You didn’t fall for it. Props to Pete Stark and his staff.

Congressman Pete Stark actually founded a small regional bank. He hated the TBTF banks. He understood on a personal level how they f*cked with people…

Graham Elwood i think did fall for this trap, banks made a fortune getting homes this way . USA is such a corrupt country i think the whole reason why 2008 bank crash affect Europe was because USA force Europe to buy these garbage loans what USA banks knew would fail. Many people are saying Trump is more dangerous than Kamala but they are wrong. Think of her as Hillary but two time worse. She will escalate all the wars and even add more

I had stopped voting for Democrats around ’93-’94 when it became clear the party had been captured by the ideological offspring of liberal Republicans post-Reagan. But it was at the time Yves recounts above that I started to really hate them. I lived through a foreclosure in California. Once it became obvious our home was irredeemably underwater we attempted to obtain a loan mod with Wells Fargo. Sure, no problem, we’ll take a look at your situation, we were told, send in your documentation. My partner, whose background is in finance, came up with a proposal based on local property values in the then current deflated market. The bank would take a haircut and we had already lost close to 150K in equity, much of which was in the form of $$ spent improving what had been a sh!tter. Anyway, proposal and supporting documents were sent, then…crickets. Waited a month, called in and were told it’s being reviewed, we’ll get back to you. Waited another month, called in and were told the paperwork had apparently gone missing, please resubmit. We went through this farce two more times all the while making the monthly payment to keep the loan current. Finally, it dawned on us that Wells Fargo never had any intention in modifying the loan and were simply doing whatever it took to keep our payments flowing. At that point, we walked. As far as I’m concerned, Wells Fargo perpetrated fraud. Had they told us from the outset the loan would not be modified we would have walked away then and saved around $20K.

Adding insult to injury, due to Obama Administration policy, Wells Fargo and the other largest banks came out of the market collapse doing quite well thank you very much. Was it really impossible to unwind the catastrophe in such away as to keep more people in their homes? Really?

Post Script: Over a year after our default the property sold in foreclosure for $45K less than we had proposed as the loan mode. May the Democrats ever burn in Hell.

Forgot to add that we later did receive a $3,000 settlement check which, thanks to Harris, was marginally higher than the poor schmucks elsewhere got. Better than nothing I suppose but so what. Compared to what the banks got it amounted to loose change in the couch. As I said, may they ever burn in Hell.

I was a local prosecutor during this time and spoke with our banking and securities fraud maven about the fraudulent lending and garbage securitizations that were driving flawed and improvident foreclosures.

He informed me that the state A.G.’s and local District Attorneys were being told by Holder, Breuer, Geithner, and Obama himself that they had no authority to prosecute the banks and their servicers, thanks to Ruth Bader Ginsburg’s (may she rot in hell) recent outrageous judicial overreach in Watters v. Wachovia Bank (2007) 550 U.S. 1. Over a stinging dissent by Justice J.P. Stevens, Ginsburg essentially ended any state regulation of federally chartered banks. Using Watters as a cudgel, Holder and Breuer were threatening to intervene on behalf of the banks to dismiss any state action against them or their servicers.

This came as a surprise to the state A.G.’s, who found themselves scrambling to save face. Schneiderman, Harris, and the others tried to “spin” it, but they were had by Obama — who essentially worked for Goldman Sachs and had handed the U.S. Department of Justice over to their white-collar defense team from Covington and Burling — Holder and Breuer.

Harris did as she was told. Obama and Holder are still pulling her strings. This is how Inverted Totalitarianism functions: the government is controlled by the financiers and not vice-versa. Harris understands how the power flows in this country, for better or worse.

I’d argue Trump also understands it. From my very limited knowledge provincial point of view, they are two very different sides of the same single coin.

re: “Ginsburg essentially ended any state regulation of federally chartered banks. ”

Another good reason to bank with a state chartered bank, imo.

adding from NYTimes, July 24th:

Ms. Harris has picked former Attorney General Eric H. Holder Jr., who once helped run Barack Obama’s vice-presidential vetting, to oversee her choice of a running mate.

https://www.nytimes.com › 2024 › 07 › 24 › us › politics › harris-vice-president-search.html

I was all over this story and this IMHO is spin by people connected to state AG offices as an excuse.

I met Schiederman and was close to attorneys who were working a big case with the Nevada AG, Masto.

The theories were securities law theories, not bank reg. I never heard anyone argue re bank regs. There’s pretty much nada in bank regs with respect to residential mortgage foreclosures.

And that was why NY was the lead despite not having the biggest AG office nor having as many foreclosures as CA and Nevada. It was the Martin Act, the New York securities law. Nothing the Feds could bluster would do anything to reduce the reach of the Martin Act.

My colleague was talking me out of getting involved, so what I heard from him about the AG was second hand, but as I understood it Holder and Breuer were using the sweeping scope of Ginsburg’s opinion to push against any and all forms of state regulation of federally chartered banks.

The politically ambitious among the AG’s could read the writing on the wall and rolled-over rather than face the prospect of having to litigate jurisdiction against the U.S. DOJ. Another colleague had to fight the DOJ all the way to the U.S. Supreme Court for jurisdiction over a mail driver who ran over and killed a kid riding his paper route. Meza v. California (1989) 489 U.S. 121. From what people who had been direct-reports to Harris told me at the time, she had her sights on higher office and was not going to rock that boat.

I don’t think that we’re disagreeing — foreclosures had always been a state issue and the federal banking regs didn’t address foreclosures via imperfect securitizations, robo-signing, and outright fraud. Under Ginsburg’s elitist reasoning state law is inapplicable to nationally chartered banks. That’s why that B.S. artist Obama could go on national television and claim with a straight face that no laws had been broken.

Again, this had NOTHING TO DO with bank regulation. NC writer and securitization expert Tom Adama was working directly with Adam Levitin, who was special counsel to the COP and Damon Silvers, who was on the COP and both were advising Scneiderman. I also had extensive contact with other lawyers and activists involved in this effort, such as attorneys who were acting as outsourced counsel to other state AGs. They were NOT bank experts and were NOT arguing theories that had anything to do with bank regulation.

The cases that were exposing bank liability, in addition to begin based on securities law, were also based on “dirt” as in real estate law. That is state law, and is outside bank regulation because it greatly predates it. Many foundational decisions go back to the later 1800s or early 1900s.

Servicing is also not a banking activity. There are tons of non-bank servicers such as then GMAC and they are subject to completely different regulation.

There was no state bank regulator involved in any of these talks. New York’s take no prisoners Benjamin Lawsky was not involved. in ANY way.

Your colleague was on the receiving end of spin.

This was the spin. I’m not saying that it would have held up in court if it had been vigorously litigated — I doubt it would have.

As I understood it, Holder, Breuer, Geithner, and Obama were threatening to intervene on behalf of the banks against the state AG’s, arguing that Ginsburg’s sweeping and over-broad language in Watters preempted application even of of state real estate and securities laws to nationally chartered banks and extended to MERS and to servicers of any loan that a nationally chartered bank had ever so much as touched.

Their argument was ridiculous, but as J.P. Stevens decries in his dissent, Ginsburg’s sweeping language in Watters easily lends itself to such absurd interpretations. Apparently Schneiderman and Harris in particular decided to cut and run rather than stare-down a president who was still politically popular and expose him as the cat’s-paw of the banks that we now know him to be.

Harris is still being amply rewarded for her fealty. It is clearly Obama who is pulling the strings of her coronation as the Democratic nominee — on behalf of the banks and financiers who really run the country.

“-Didn’t prosecute Steve Mnuchin when she was CA AG.”

That’s the one and only mention of the slime monster that foreclosed our house?

“Kamala Harris’s connections to billionaire Goerge Soros go much deeper than that as reported by both counterpunch.com and The Intercept. This is not corrupt nor abnormal, but what is concerning is that George Soros helped sell OneWest Bank in 2014 for 3.4 billion to CIT Group. In 2015 Steve Mnuchin maxed out a donation of 2,000 to Kamala Harris’s Senate campaign which came from Steve Mnuchin of CIT Group.”

“When she was the DA of California Steve and his wife both donated to Kamala Harris and then again when she ran for Senate. Steve Mnuchin has spent over half a billion dollars donating to Republican Committees and PACs across the United States, yet Kamala Harris seems to be the ONLY democrat he is interested in donating his money to.”

Tons of details about this:

https://wedacoalition.org/2019/09/27/this-is-why-kamala-harris-refused-to-prosecute-steve-mnuchin/

Your ire is not warranted. This post is clearly labeled as being about the 2012 foreclosure settlement which Kamala continues to tout as a major accomplishment. This is not and is not pretending to be a systematic takedown of Harris’ time as attorney general.

> Lanny Breuer

I cannot forbear from running this parody of Obama administration goon Lanny Breuer. Newer readers may not have seen it:

In retrospect, not really a parody….

Always reliable for those who remember that era of the post crisis response by the authorities at DOJ, etc…lawyers like these who had to care about laws being possibly broken? Which my cynical nature was harder to come by.

Or from Seinfeld, “that’s good, Jerry!”

i just heard/saw kamala claim she saved X huge number of mortgage holders during the Great Recession. thank you for this piece if only because when i saw that, i could not remember if it was her name that NC back then had connected with the state AGs’ inexcusable failure to help people. my memory is now pretty vague, but when i saw that claim the other day, i thought wait a minute, i thought she was the worst of them, or one of the worst. but i could not remember the names from back then.

. . . i do recall a fair amount of the mortgage breakdown clusterfuck because i lived it, my newly purchased condo was underwater from the crisis, and i read yves very closely during that period and in that way i’ve received (not for the only time but with the biggest $$ at stake from me) concrete material benefit from NC. (!)

i was able to obtain a modification, only, i believe, because i understood from my NC reading what was going on in the system i was seeking aid from. it really was a challenge, persisting to get that mod. i continued to make my payments though they instructed me to stop when i initiated the application. i do recall at one point by sheer luck reaching a guy, working for a servicer, who had some brains and knowledge and said to me: “if you get this mod, send me a copy and i’ll frame it and put it on the wall, because nobody is getting them.” that was valuable info that kept me from giving up. but had it not been for yves/NC, i would not have known to persist even far enough to get through to that guy.

the final confrontation was when i’d fedexed my application to the servicer, to be signed on delivery. and the servicer’s employee told me that they hadn’t received it. and i simply said, very firmly, i’ve fedexed it to you and delivery was signed for, which means it is in the building you are in, somewhere, so you have to go and find it and get back to me. she did, and the modification was quickly approved.

since then i’ve managed to hold on to my condo, my only nest egg, and have now been living in it for 17 years. being able to own my own home has made a great difference to me, as i am able to control my environment–i have chronic fatigue and multiple sensitivities to environmental contaminants.

thank you yves!!!

Yes, thank you, and thank Yves. I too, was offered a loan modification. Apparently, it went well. I was not underwater as I had purchased my condo, 2005, FSBO, with 20% down, and a payment that was mid 700’s. Bank financed. Managed by me, and my nursing career. Some notary gal came to the house, we sat at the table and I signed numerous documents. My interest rate decreased, I paid the loan off quickly. Took a 30 year note to 10 years. I have little formal education, sans, my MS in Nursing. I did know then, as I know now…no debt is best. (Rural Ore-gon)

Neither Ms. Harris reputation, nor her character, are, in my Superhero’s opinion, rehabilitatable.

She isn’t alone. There were numerous cowards who just threw homeowners under the bus. If I’d had even just a modicum of support … I’d have citizens arrested their asses. As many times as necessary to secure … impeachments, disbarments, convictions, tarring and feathering.

In May 2010 I provided significant, and substantial, data to the Assistant AG in KY, Harold Turner, that was heading the investigation in re robo-signing/FNIS/LPS/DocX, etc. His office was quite dismissive.

In fall 2011, after terms of the National Mortgage Settlement had leaked and been discussed here by Yves, Field, et. al., I contacted an Assistant AG in the Consumer Protection division, Todd Leatherman. In discussing how horrendous the terms were, and that the thousands of homeowners in distress that I’d communicated with would gladly forego the meager $1700 (or nearto) that was being proposed in order to see the criminals charged, arrested, prosecuted, convicted, and sentenced. Mr. Leatherman’s response was “There were numerous different scenarios in which homeowners may have been harmed, and they weren’t all harmed to the same degree. What we’re looking for is a global solution. The AGs office thinks that will be the best policy.” I interrupted him at that point, and said, “Mr. Leatherman, I’m no yocal. I’ve been to Memphis. But the majority of my life I’ve resided in Kentucky. As far as I know the best policy is act in accordance with the rule of law.”

You might say my relationship with the AGs office hasn’t been the same since.

When news broke that Harris, as CA AG, had let OneWest Bank/Steve Mnuchin off the hook … I was … as apoplectic as a Superhero can possibly be!! The appearance is that staff attorneys in her office had worked on a line-level investigation for over a year, and worked it to such a peak there was even a draft civil complaint … drafted. That must be among the best opportunities to mete out some accountability any state AG had. And she just pi**ed on it.

And now the DNC is putting her forward as the 2024 presidential candidate?! While I can’t vote for Donald Trump I also can’t vote for Kamala Harris. I’m reminded of Luther, and his testimony at the Diet of Worms. Even when faced with a penalty of death he maintained his position, stating “I cannot and will not recant anything since it is neither safe nor right to go against conscience. May God help me. Amen.”

Here’s the thing, and for me there’s really no getting around it: The refusal of those to whom we’ve handed the sacred trust of protecting us from criminals and predators to actually hold the criminals and predators accountable … is why we can’t have nice things.

My utterance above is really on the lighter side. If you recall your Dante … Well, even if you don’t … Dante reserved his 8th “Circle of Hell” for con-artists, and fraudsters. I think it’s clear that Dante would have placed Trump in the 8th circle. He reserved the 9th circle for those who engaged in treachery, and in betrayals of trust. I think it’s equally clear Dante would have placed Harris in the 9th circle.

Another contact of mine, a former assistant of/to/for O. Max Gardner, III, commented on a social media feed of mine that Trump “may well eliminate little things like due process entirely.” Here is my response to them:

“I wasn’t afforded due process beginning in January 2008, and still haven’t been. In fact I haven’t found anyone who cares about my rights to due process since then. Not anyone in media, law enforcement, the legal profession, or anyone in any of the three branches of government. And I looked for them. For more than a decade and a half I looked for them. At local, state, and federal levels I looked for them.

I was met uniformly with disregard, and often that disregard was also callous. Even worse is that while I was left alone in pursuit of my rights by all the authorities that were obligated to afford them to me – you know, those ‘little things like’ due process, equal protection, a level playing field, impartial proceedings – and not only were they denied to me but I was also punished for pursuing them.

So, if you’re thinking the elimination of ‘little things like due process’ is gonna be something new, and different, in my life you’re thinking is in error. You should also consider that there are 10’s of millions of people similarly situated in the US who’ve been treated similarly, to identically, as I’ve been. 10’s of millions.

As I said above Kamala Harris, as the highest ranking law enforcement official in the state of California, refused to properly discharge her duties. She refused to protect the citizens therein from a corporate marauder roving across the state in quest of plunder. In my opinion she isn’t worthy of any office, and she’ll not receive my vote.”

My conscience informs me that I can’t vote for FPOTUS Trump. At the same time it is also informing me that I can’t vote for VP Harris. Similar to Luther I don’t think it’s either safe, or right, to go against conscience.

In order to vote for the lesser of two evils in this cycle I’d have to vote for Trump as Harris is clearly … eviler than he. As I stated above I’m not gonna do that.

PS Yves, I’ve cited your 2019 piece in comments several times in the past week. I’m glad to see you’re rerunning it. You might also consider rerunning … a bunch of others, too … but perhaps most on point would be your piece from December 13, 2023, “Replacing Kamala Harris.”

Thank you x 10, Yves!!! I’ve been praying for this to get re-exposed. Her record is so blatantly anti-populist. Yet people fall for the hype. I despair more for our gullible citizenry than I do for one more lying politcian like Harris. Why shouldn’t she and Dems lie. People go it. Yum, yum, eat it up.