It was awfully conveniently timed that Trump announced the establishment of a “strategic” crypt fund in the middle of a crypto market sad that could have turned into a rout. As anyone with an operating brain cell knows, there is zero reason for a sovereign currency issuer like the US to hoard baseball cards crypto, particularly given its lack of use in the real economy for much beyond tax evasion, paying criminals, and money laundering. This is simply a particularly obvious payoff to a key group of Trump election campaign supporters, for an activity with not only no value, but actual negative consequences: facilitating crime, reducing tax receipts, diverting investments out of productive activity into speculation.

And this handout is taking place as Musk and DOGE are going on their ideologically-driven rampage though the Federal apparatus, routinely going well beyond their claim to be cutting fat and hacking out muscle, bones, and organs. See the post yesterday on the cost-cutting at the USDA, which seems guaranteed to hurt farmers and lower agricultural output. And the dumb chump public is supposed to applaud? When food prices are already seen as too high? Instead of the purported Klaus Schwab globalist “Eat zee bugs” scheme, we are seeing the direct operation of Lambert’s Second Rule of Neoliberalism: “Go die!”

But this grotesque handout actually represents continuity of policy, but with characteristic concern about plausible deniability, as in ability to posture about broader benefits. As we’ll describe below, there’s a long, proud history of seemingly cost free or low cost financial market subsidies to pet party backers on both sides of the aisle. Sometimes they actually have benefitted interest groups which support both political parties because they have the financial means to do so and have policy interests they want to move forward regardless of which party is in charge.

And that’s before getting to other elements of the lack of justification for the program (save the enriching friends of Trump part):

A U.S. crypto reserve makes no sense. No clear purpose, contradicts decentralization, opens laundering loopholes, concentrates control, chokes innovation, and feels like a slush fund or ETF setup for institutional bailouts. If crypto is decentralized, why centralize the reserve?

— Michael Gogel (@mgogel) March 2, 2025

But first, an overview of the crypto bro payoff scheme. The Financial Times headline flags that everything is going according to plan. From Crypto prices jump as Trump names tokens included in strategic reserve:

A reserve has been championed by crypto traders, who believe something akin to Fort Knox for gold — which would buy and hold bitcoin — would offer legitimacy to the asset class.

Proposals are already working their way through state and federal legislatures. One Republican-backed Senate bill seeks to direct the US Treasury to buy 1mn bitcoin, worth roughly $94bn based on current market prices.

The bills have faced opposition, including from some Republican lawmakers who say they put taxpayers’ funds at risk, and the reserve itself will raise concerns over potential conflicts of interest. Some Trump advisers have investments tied to the market….

Bitcoin rose as much as 11 per cent to $95,084 on Sunday before retreating slightly to $93,165 on Monday, while ethereum gained as much as 14 per cent to $2,541, before falling to $2,448 on Monday.

Solana, the token that represents the blockchain that hosts most memecoins — including Trump’s own coin, climbed 26 per cent to $180 but fell to $170 on Monday.

Ada, which represents the cardano blockchain, soared 71 per cent to $1.15 per token on Sunday. XRP, the coin affiliated to payments group Ripple, rose 37 per cent to $3.

The comments at the pink paper ranged from incredulous to scathing. A few examples:

Un addition to the bad optics of handouts to campaign backers, we have top Trump officials feeding at the trough:

Jaw-dropping corruption in the US:

Trump's billionaire crypto czar is heavily invested in a fund whose top 5 holdings are the 5 in the US government Crypto Strategic Reserve.

Mere hours before Trump announced it, someone bought $200 million in Ethereum & Bitcoin on 50X LEVERAGE pic.twitter.com/LQWZceeTvB

— Ben Norton (@BenjaminNorton) March 3, 2025

We’re all going to pay more in taxes to fund Sack’s exit from his crypto positions.

— Parker Conrad (@parkerconrad) March 2, 2025

David Sacks is up there among the biggest pieces of shit in the US

He literally cried for the government to save his bags when SVB collapsed…now did it again with his crypto fund

He’s a shitstain on America. The day he finally ends up in jail should become a national holiday https://t.co/PqMQaoI9RW

— Rho Rider (@RhoRider) March 2, 2025

Only one conservative Trump supporter has come out and said what an insane grift the Crypto Strategic Fund is as far as I can see

But 99% of them are thinking it but are too scared to disagree with Trump

Let’s pause: If you’re too scared to challenging the President when he… https://t.co/uCwYVyJW2T

— @jason (@Jason) March 2, 2025

We are pained to point out that this sort of grift has a proud history, particularly in recent years, although with the “cash for friends of buddies of the Administration” part a wee bit less obvious.

Let’s start with some original sins that pretty much everyone in the general public is unaware of: massive subsidies via underpriced insurance, which includes policies that allow market participants to set aside unduly low risk reserves. The mother of all is underpriced FDIC insurance. This is particularly troubling since many banks park their derivatives exposures in their FDIC insured entities. Now admittedly some “derivatives” like interest rate and foreign exchange swaps in major currencies are pretty plain vanilla. But after the crisis, and it appears to be continuing, there’s not enough official minding of this risk store.

Since the crisis, regulators in the major economies have made a concerted effort to move derivative transactions to central counterparty clearing houses for derivatives transactions. The theory is to reduce counterparty exposure and thus contagion in a crisis. However, the risk reserves in these clearing houses are margin posted on particular exposures. The margins are set too low because (you cannot make this up!) professionals claim that derivatives would become unaffordable if the margins were set high enough to cover the true risks. The official posture is that these clearing houses are not backstopped. No one in the markets believes that. In a crisis, they are sure to be treated as too big to fail.

Thanks to deregulation of the financial services industry, many activities that once were limited to banks moved to institutions that competed with banks without paying FDIC insurance. Money market funds are the prime example. During the financial crisis, the posture of government shifted from protecting the banking system to protecting an ever-growing list of market participants. Perry Mehrling has described the change in posture as going from “lender of the last resort” to “dealer of the last resort”. So in the crisis, money market fund holders got a massive gimmie via suddenly being guaranteed up to $250,000, just like FDIC depositors, to prevent runs on money market funds after a large fund, Reserve, famously “broke the buck” via holding subprime asset-backed commercial paper.1

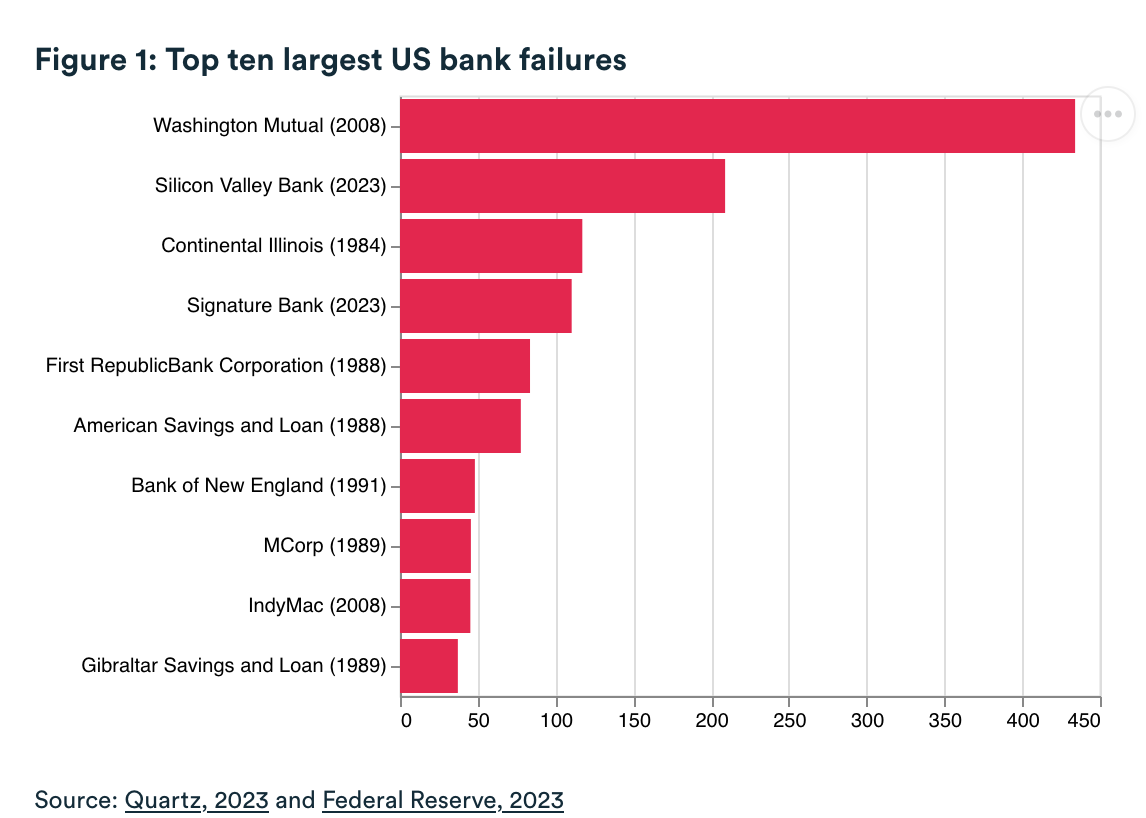

Back to the question of deposit guarantees. During the crisis, uninsured depositors at smaller banks that had big subprime origination business and failed with a lot of bad loans in their pipelines (as in set to be securitized) like IndyMac and New Century were not rescued.2 Fast forward to the recent shift from that policy with the unseemly salvation of uninsured depositors in the above mentioned SVB, Silicon Valley Bank and the crypto-catering Signature Bank.

To make a long story short, Silicon Valley Bank was too connected to fail. The excuse for the bailout of its unsecured depositors was that there were companies that had payroll on deposit and wiping that out would stiff the workers and potentially ruing the companies. While it is true that companies of any size pretty much always have more cash at their bank than deposit guarantee limits,3 no one harbored such tender concerns for the companies that had the misfortune to be IndyMac and New Century customers. Nor did anyone then or later suggest creating a special bailout facility solely to protect these companies’ funds. But those venture capital investees are so much more special than other businesses.

And despite those crisis wipeouts, no one suggested restoring the Fed payments facility to allow companies to hold pending payroll payments safely at the central bank. God forbid the prospect of competition or risk reduction!

Admittedly, another widely recognized but not-officially-admitted rationale was the wobbly state of many mid-sized and pretty big banks, due to a combo of wrong-footing the sudden Fed interest rate increases (as in having serious but not recognized interest rate losses) and/or having meaningful exposures to commercial office space, which were expected to show credit losses as current tenants did not renew leases as a result of “work from home” persisting beyond the Covid crisis.

But the biggest driver was that Silicon Valley Bank was too connected to fail. There were company executives that claimed that after receiving venture capital funding, they were required to conduct all their payments activities through Silicon Valley Bank so that the VCs could spy on them on an ongoing basis. Even more important, the venture capitalists themselves (the firms and their principals) had very large balances at Silicon Valley Bank. Peter Thiel said he had $50 billion “stuck” there.4

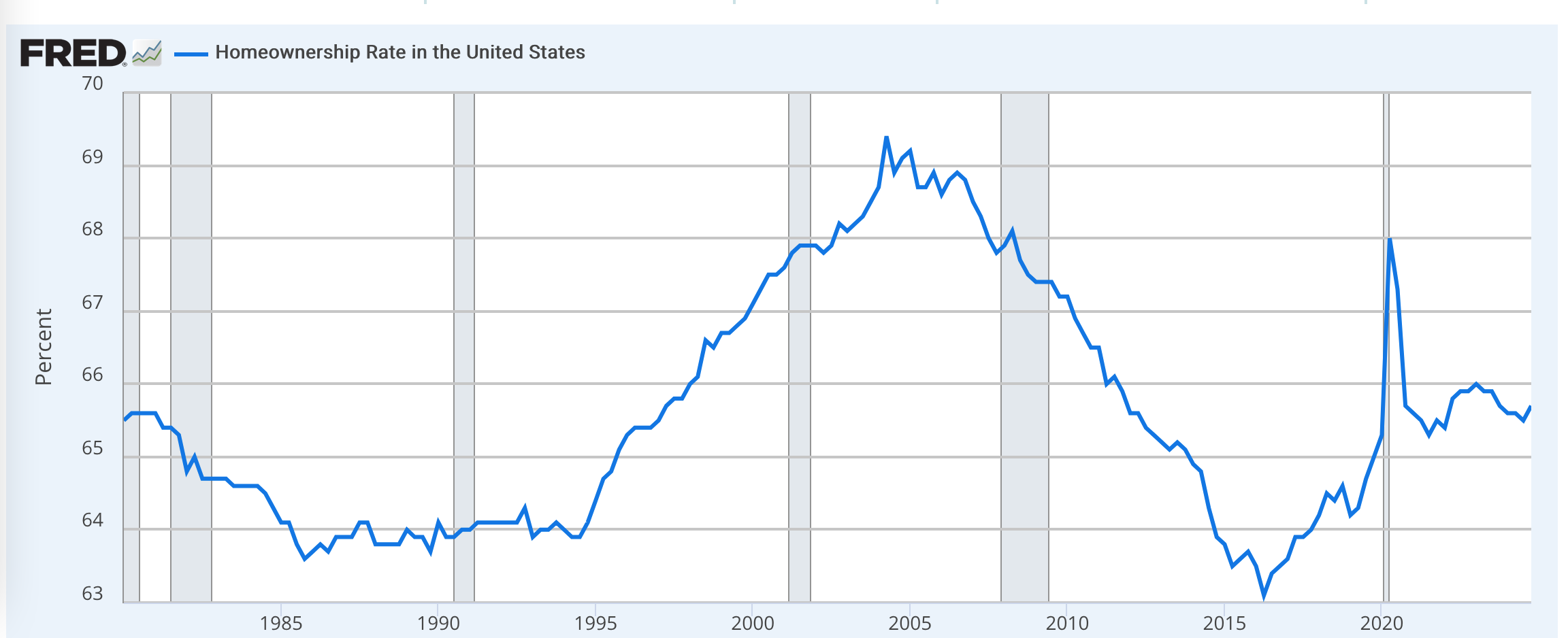

Readers can likely add to this walk down memory lane, but a final and very large example are the mortgage market subsidies via Fannie, Freddie, and the FHA. On paper, these are meant to boost homeownership since that leads to more conservative, as in establishment-favoring behavior. Note that it is not necessary to provide for stable residences (which also supports family formation) via supporting home buying. Germany (at least until neoliberalism started to eat into this system) gave tenants very strong property rights, so that many would live in the same rental apartment or home for decades. I have written repeatedly about the analogue in New York City’s rent stabilization system (which unlike rent control, allows landlords to increase rents in line with the allowed increases, which are set after much arm-wrestling to reflect increases in the owners’ costs.5). The key tenant protection was that the landlord had to offer a lease renewal to tenants that were current on their rent payments. The building I lived in in Manhattan had many tenants that had not only lived there for decades, but even made substantial improvements in their apartments, like putting in marble or granite flooring.

The aim of these German policies was to keep housing affordable. That in turn would support the competitiveness of German industry via wage payments not having to support housing rentierism.

But back to the key point of how the mortgage guarantors Freddie and Fannie served as Democratic party aligned influence machines. The case is set out long from in the Gretchen Morgenson and Josh Rosner book, Reckless Endangerment. They describe how the head of Fannie, Jim Johnson, used the massive mortgage guarantee fees to build what we would now see as NGO, with a big housing/mortgage research arm, and more important, the active creation of a pro-homeownership coalition, uniting many Democratic faction, particularly the Congressional Black Caucus. A piece by the respected writer/investigator Bethany McLean in Vanity Fair gives a sense of Johnson’s outsized influence and methods.

The pre-crisis homeownership rate was clearly a historical anomaly, particularly given that real wages have been stagnant for decades.6

Sadly I don’t have access to the Morgenson/Rosner book now, but they argued, credibly, that the Fannie/Freddie subsidize plus other successful initiatives by the Johnson-coordinated housing coalition played a meaningful role in the overly-permissive lending that led to the crisis. But lots of friends of the Democrats made out in the meantime.

So to come full circle: many are unhappy with the operation of the Federal government because they think a good bit of the money is going to bad or wasteful uses. But the employees, which are the focus of the DOGE slash and burn, are, as comparatively modestly paid workers, a small part of equation even when the actually are tasked to questionable initiatives. The big part of the grift are things these employees do not even remotely control, which is the approval of programs that are set out to enrich pet interests: Pentagon pork, tax breaks for activities the recipients would likely engage in anyhow, subsidized loans and activity guarantees, and now the big grift of payoffs not even credibly masquerading as a fund. But the Trump action is enough of a change in kind, as opposed to merely degree, as to sound large alarms about what might be next.

_____

1 Defenders point out that the Temporary Guarantee Program for Money Market Funds made money, since it collected fees and didn’t in the end have to make any payouts. But this ignores the three card monte of the rescue programs: of the massive and ultimately hugely distorting interest rate reductions to negative real interest rates, the Fed further subsidizing banks and mortgage/housing investors via QE (designed to lower longer-term Treasury and mortgage interest rates). A second factor was the $180 billion bailout of AIG. We will spare you mining our archives, but at the time, we (along with experts like Neil Barofsky, Special Counsel to the TARP) disputed Fed claims of the money they “made” from AIG.

2 WaMu depositors escaped this fate because JP Morgan bought the bank…and by all accounts got a monster bargain.

3 It would be an operational nightmare to fragment payroll across many banks to keep totals at risk below the FDIC ceiling.

4 Thiel was accused of triggering the run. Note it’s hard to evaluate this claim. Not that I am defending Thiel, but panic and rumors go through many channels. In other words, Thiel looks to have been intensified worries and thus transfers out of Silicon Valley Bank via his action, but it’s not clear similar behavior would have taken place mere hours or days later otherwise. From the Financial Times:

Peter Thiel said he had $50mn in Silicon Valley Bank when it went under, even after his venture fund warned portfolio companies that the tech-focused lender was at risk.

The veteran technology founder and investor was widely blamed for precipitating a bank run in which depositors tried to pull more than $40bn in 24 hours last week. His venture capital firm Founders Fund was among those that had advised clients to spread their deposits to other lenders as concerns about the bank mounted.

But Thiel told the Financial Times this week that he had maintained a substantial personal account at SVB even as fears mounted over its fate and later resulted in a run on the bank that ultimately toppled it.

“I had $50mn of my own money stuck in SVB,” said Thiel, who co-founded tech companies PayPal and Palantir in addition to Founders Fund.

5 In practice, the increases somewhat lagged inflation when inflation was high and exceeded the rate of inflation when inflation was low. The system was designed to preserve landlords’ profits on rentals.

6 I don’t have an explanation for the Covid spike and reversal. It looks like a data anomaly. Perhaps people buying homes in the exurbs/boonies for work from home, owning two homes for a bit that was mistakenly classified as two households owning a home, and that reversing as one of those residences was sold? Informed input would be appreciated.

On top of this, isn’t a US sovereign wealth fund coming as well? https://www.whitehouse.gov/presidential-actions/2025/02/a-plan-for-establishing-a-united-states-sovereign-wealth-fund/. That just sounds like a backdoor mechanism to bail out the stock market. Issue debt, then use the proceeds to prop up overpriced companies, and perhaps relieve the PE guys from their over leveraged, soon to be bankrupt portfolio companies. Sounds like a winner!!!

Someday Trump 2.0 will be known as the Trumput (for Put option) presidency, who knew the Art of the Deal means selling put options backed by IRS takings?

A Sovereign Wealth Fund for a country with huge fiscal and trade deficits = Logic!

I can handle only so many bad ideas in one day :-)

Here’a another: we officially name it the Mt. Gox Strategic Sovereign Wealth Fund.

This all looks to be a nice little pump and dump operation. It’s hard for me to imagine that banks are really going to let all the crypto shenanigans go through as that would destroy any faith remaining in the dollar. On the other hand, DOGE has been targeting all financial regulators for complete eradication so I don’t know what to think anymore.

There’s another long standing strategic reserve that’s been severely depleted lately and could use a top off after the draw downs from recent years. Oil had been quite cheap too. But I guess the oil producers did not contribute sufficiently to the Trump inauguration fund.

The officials can’t think their way out of the asset bubble trap.

I got an idea. Instead of a Crypto Strategic Fund, they should tell all Federal workers that if they want to stay, then they have to accept payment in crypto coins. That is one way to make this junk look respectable. I really do not know what other countries will be making of the US. I mean, wanting to take the real wealth of the nation and swap it for what Yves compares to baseball cards. Seriously? If the wheels start coming off this bright idea, will the US demand that other countries buy their crypto to help bail out any US crypto fund?

In short, someone from the casino business is easily convinced of the idea to turn the government into a casino. Then I have to stop and think that maybe, at this point, casinos have better safety and security controls for funds.

Yes, actually casinos have strict regulations to make sure they can pay out on wagers. Your jibe is not incorrect.

A carnival barker who dabbled at the casino business and was so bad at it that the casinos wound up in bankruptcy court four times!

Trump’s casinos were all confidence games using his name recognition for the fleecing of investors. As casinos they were failures from the get-go.

The crypto reserve is just another one of his confidence schemes. As always, the marks think that they’re in on the con…

Trump and dump has a long pedigree.

I wonder what the relationship of this fund is to this idea:

https://WWW.MARKETWATCH.COM/STORY/WALL-STREET-CANT-STOP-TALKING-ABOUT-THE-MAR-A-LAGO-ACCORD-HERES-HOW-THE-CURRENCY-DEAL-WOULD-WORK-F8FBBDA0?MOD=HOME_LN/

Wall Street can’t stop talking about the ‘Mar-a-Lago Accord.’ Here’s how the currency deal would work.

Alleged to be an idea that will “help create American manufacturing jobs.”

Meanwhile, thinks like education, training, and infrastructure…**crickets**

crickets….and then thunderous laughter and knee-slapping! At least the tragic humor is in no short supply eh.

Rainbows, unicorns and cotton-candy for everyone! Two chickens in every pot. Good-paying manufacturing jobs will magically come back to ‘merka and everything will be peachy keen!

So, they would correctly be seen as dangerous economic gambles? Huh, I guess truly nothing was learned with 2008. And here the goal is to wreck whatever remains of the federal government, which for good or ill gave some stability to the country, and simply give big paychecks to the fat cats gambling on crypto (when is it ever going to become the usable “money”, i.e. the medium of exchange it was touted on potentially being, instead of a very wobbly store of value?)

At this point I’m considering picking up and reading Gibbon as an exercise in futurology.

That bank failure chart included GFC luminaries contributing to the period where All the Devils are Here.

How many devils are there now circulating, hovering about Main Street, Wall Street and the occasional forest and chicken coop?

Whitney Webb has given several interviews lately explaining that the key to understanding this new enthusiasm for crypto is that they can be freely traded with stablecoins, which tend to buy US Treasuries. The hope seems to be that dollar denominated stablecoins will absorb US debt forevermore.

Given that nothing seems to make sense (grifting and looting aside) regarding the State’s emerging embrace of crypto, her reasoning seems to make sense. Tether seemed to be on the verge of failure/exposure a number of times, but now that shadowy operation seems too big to fail.

From what I understand of all this, it might be more accurate to say stablecoins allegedly buy US treasuries. Stablecoins are supposed to be stable since they are backed 1 to 1 by the US dollar or dollar equivalents (Tresuries). During the Sam Bankman Fried debacle, I remember it coming out that just maybe one of the largest stablecoins was backed by a few wooden nickels and a lot of vapor.

Thanks for the reference – I’ll have to check out some of Webb’s recent videos.

Rumor is tether is buying china $ denominated debt with a lie calling it us treasury equivalent.. Few in the US treasury space have seen them buying treasuries. Big mystery….

The question is who is going to buy them and who is going to store them, Treasury or Federal Reserve, otherwise this won’t take. They need to be exchangeable for Reichmarks……sorry I meant T Bills. Got confused with Mefo bills.

Visualize using physical gold to buy crypto. At what cost, if it can be done….

Michael Saylor needs price support for crypto and exit liquidity after betting the company on this thing. Seriously, Trump is subjecting the collective consciousness to a spectacle blitz with these schemes, he’s “flooding the zone” alright. First came “the US government must own half of Tiktok”, then the Sovereign Wealth Fund, now we have the crypto strategic reserve following hot on the heels of the $5m Gold Card to get the world’s wealthy to flock to the US. It’s hard to keep up…

Compare to how the Fed Reserve does this when buying assets. You know, for “price stability”.

This all makes sense: The aim of politics is to convince the plebs that their interests are the same as the interests of their overlords. The most sophisticated and pervasive system of misinformation and conditioning (“electronic lobotomization”) has produced millions who identify with the same people screwing them over and they identify with oligarchy and are taught to despise their peers and underlings. A nation of delusional sycophants?

Now that’s what I call successful political mobilization! If I were cynical, this would appear like a concerted effort to create a population of Stockholm Syndrome-stricken zombies while fleecing them of what ever assets they still have.

This also looks like more asset-stripping and kleptocracy, but millions will cheer-lead their own destruction. Eddy Bernays would be both proud and amazed.

Look at Intel. Rather than wait for investments in that infrastructure to pay off, the quick money is to be made by selling of parts of it. You know that’s a scam because what is the rush? If the investment didn’t start working as advertised in 5 years time or so, the parts would still be there to sell.

RE: “…taught to despise their peers and underlings.”

I’m reading the Odyssey all the way through for maybe the first time. Near the end, there’s a passage where Odysseus has just returned home to a bunch of hangers on eating up his estate and courting his wife. He is disguised as a beggar and so is berated by one of the flunkies who claims that the beggar would rather laze around and mooch off others than do an honest day’s work himself.

Not long after, Odysseus removes his disguise and engages in the wholesale slaughter of all those who had tried to scam him, with the berator taking the first arrow to the heart.

Just pointing out that this kick-down attitude has been around for a lot longer than I’d thought. And also that maybe there’s hope for restitution ;)

Great example!. The Collapse of Antiquity (2023, Michael Hudson) covers that in the classical Greco-Roman era, many other examples. History sure does rhyme…

Odyssey ends on a sombre note. The returned king puts to death most of his maidservants, who had for years been fair game for the lustful interlopers. He hangs the girls low, and watches them kick.

Then, in the last book, the war really comes home. The families of the butchered suitors take up arms. Now Ithaca is torn, and battle begins, with a scene reminiscent of the Iliad.

It only stops when Athena herself cries out. Like in a tragedy of Euripides, deus ex machina is the last hope for a vain and violent humanity.

“Taketh away from the many”

Is there anyone trying to track a stoppage of payments? A diarist on DKos wrote that they know someone who did not receive their social security payment, then found that the nearest social security office had been closed.

Could Trump somehow sneak his own memecoin into the reserve?

Does anyone have trademark on ShitCoin yet? Damn, I’m too late.

Looks like it’s really in the crapper, though:

What is the fully diluted valuation of Shitcoin on TON (SHIT)?

The fully diluted valuation (FDV) of Shitcoin on TON (SHIT) is $167,993. This is a statistical representation of the maximum market cap, assuming the maximum number of 100 Million SHIT tokens are in circulation today. Depending on how the emission schedule of SHIT tokens are designed, it might take multiple years before FDV is realized.

That’s from coingecko.

I am not sure this will have legs, support seems pretty narrow. For example, the co-founder of Palantir that isn’t Karp, blasted this as a giveaway to a few big crypto owners. CNBC anchors said it looked like blatant self-dealing. Graft needs to be a little better hidden I think.

I’m so glad to see that the crypto-con appears to have failed to launch

https://www.cnbc.com/cryptocurrency/

Big “sell the fact day”. No up on very good news, holders selling.