Yves here. We have warned for some time that for the Fed to stop this inflation, they would have to kill the economy stone cold dead. The recent bout of price rises was not the result of the stereotypical wage-driven cost spiral. Labor continues to have fairly weak bargaining power. Instead, the impetus was sector-specific Covid and other supply shocks (remember the chicken cull producing a price explosion in eggs in the US?), some additional supply squeezes due to sanction, companies raising prices because they could, and more recently, the Administration choosing to run the economy very hot via large fiscal deficits.

In crude terms, Fed would have to overshoot to curb inflation that simple interest rate increases are not well suited to check. As this post explains, this increasingly looks like what will happen.

By Thomas Ferguson, Research Director for the Institute for New Economic Thinking and Professor Emeritus, University of Massachusetts, Boston and Servaas Storm, Senior Lecturer of Economics, Delft University of Technology. Originally published at the Institute for New Economic Thinking website

On June 13th, financial markets discovered they had overestimated the likelihood that the Federal Reserve would soon be cutting interest rates. Federal Reserve Chair Jerome Powell’s remarks at his press conference and the Federal Open Market Committee’s freshly updated quarterly “Summary of Economic Projections” pointed forcibly to the conclusion that the Fed would likely cut rates only once before the end of 2024.

In the midst of their own historic surge, US financial markets could mostly afford just to sigh. Reactions elsewhere were less sanguine: Some international commentators worried that higher for longer US rates would make repaying foreign dollar loans harder and accelerate a movement of capital out of the developing world. But even in the US, a chorus of misgivings welled up about disappointing retail sales, slumping home construction, the effects of prolonging elevated interest rates on ordinary consumers, weaknesses in commercial real estate held by many banks, and other signs of a slowly tightening squeeze on the economy. Economist Claudia Sahm summed up many of these misgivings when she warned of slowly rising unemployment, commenting, “My baseline is not recession…but it’s a real risk, and I do not understand why the Fed is pushing that risk. I’m not sure what they’re waiting for…The worst possible outcome at this point is for the Fed to cause an unnecessary recession.”

The Fed has a ready answer: It fears that the U.S. inflation rate will remain elevated for some time to come. Overall inflation remains high, mostly because of the stubbornness of services inflation. As the Bureau of Labor Statistics reported, the Consumer Price Index (CPI) rose by 3.3% (year-over-year) in May, but service inflation, excluding energy services, rose by 5.3% year-over-year.

Many observers blame the ‘sticky’ services inflation on nominal wages, which are rising as workers strive to catch up with inflation. Chilling out services inflation would thus be socially very costly: it would require considerably more monetary tightening by the Fed and cause a spike in unemployment. Although the Fed is not (yet) willing to go down this road, the stubbornness of services inflation means that U.S. interest rates will remain elevated to achieve the Fed’s 2% inflation target.

But this answer, sanctified as it is by generations of warnings from inflation hawks about wage/price spirals, is too easy.

More than a year ago, we analyzed the wave of inflation that was rolling over most of the world. We forecast that efforts to cure inflation in the United States by raising interest rates could not succeed at anything remotely resembling acceptable cost. The problem at its starkest is this: services inflation is heavily driven by surging increases in consumer spending on restaurants, travel, healthcare, and other higher-priced services.

Most of this spending comes from the very rich: affluent, often older, Americans who have benefited from the outsized gains in the U.S. housing and stock markets in recent years. Record increases in household wealth have given the rich confidence to increase their spending, which is a big reason why the American economy has defied expectations of a slowdown in the face of considerably higher interest rates. This wealth effect is a major driver of persisting services inflation.

Let us look more closely at the relevant facts. Spurred on by the ultra-low interest rates set by the Fed, average U.S. house prices rose by 47% between the first quarter of 2020 and the first quarter of 2024 and reached another record in recent days. As a result, the value of household owners’ equity in real estate increased by $13.4 trillion. Stock prices, as measured by the S&P 500 index, are more than 80% higher than they were five years ago, adding trillions of dollars to household wealth. As a result, U.S. household wealth has shot up by a record $47 trillion during 2020Q1-2024Q1 and, recently topped out again.

The wealth gains are hardly universal. The wealthiest 1% of American households captured 30% of this spectacular rise in financial wealth, while the wealthiest 10% garnered 59% of the wealth gains (amounting to $21.7 trillion). The bottom 50% of the wealth distribution, in contrast, received a pitiful 5% of the recent aggregate increase in household wealth. Wealth is also disproportionately held by older Americans and, of course, whites. People aged 55 and over own nearly three-quarters of all household wealth. However, many older Americans face significant financial challenges: one-quarter of Americans over age 50 have no retirement savings (according to a survey by the AARP).

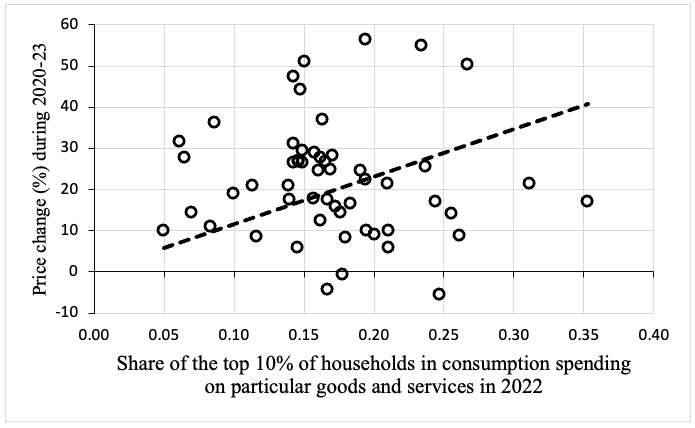

It is reasonable to expect that some part of this increase in household wealth will impact household consumption, especially spending by the wealthiest 1% or 10% of U.S. households, and through that, affect inflation. Our recent study relies on very conservative estimates of the effect of a $1 increase in household wealth on consumer spending to estimate the size of those effects: we find that the wealth effect accounts for almost all of the recent rise in American consumer spending. Economists at Moody Analytics and Visa concur, reporting similar impacts of higher household wealth on spending. In support of our argument, the figure (below) shows that prices have increased significantly faster during 2020-2023 for goods and services purchased by the richest 10% of U.S. households.

The Fed’s monetary tightening reinforces the dual nature of the American economy. On the one hand, a minority of very rich Americans who own houses, stocks and cars, remain relatively unaffected by the higher interest rates. Their spending is relatively immune to the Federal Reserve’s push to slow growth and tame inflation through higher borrowing rates, because it rarely requires borrowing and because their ability to provide collateral secures them preferential rates when they do add debt.

Prices have increased more for goods and services bought by the rich

Source: Ferguson and Storm (2024).

By contrast, the majority of Americans are enduring a combination of unaffordable house prices, increasing rents, high mortgage rates, and (despite many widely advertised claims to the contrary) stagnating (even declining) real wages, that make it close to impossible to buy a house unless you already own one. This bifurcation of the U.S. economy feeds on the increasing economic heft of the superrich, which is quickly transforming America’s economic structure: jobs in high-end restaurants were flourishing, while low-paid work in nursing homes, childcare, or education dries up. The outcome is not just distributionally regressive, but also plainly irrational.

In persisting with its high rates policy, the Fed is acting like James Dean in the famous “chicken run” auto race in Rebel Without a Cause. It is embarrassed by its failure to foresee the extent of inflation and is determined to control inflationary expectations. So, it persists in a policy that many analysts recognize is increasingly risky (or “data-driven” in the jargon, meaning that the Fed is sailing far beyond the Pillars of Hercules).

The problem is that sticking with the policy will send the economy over the cliff since the Fed refuses to recognize the link between the wealth effect, consumption spending by the rich, and inflation. Higher interest rates simply cannot cure this problem save through a Volcker-like tightening of monetary policy drastic enough to kill off the wealth effect. This would almost certainly throw the U.S. economy into a major recession, with no end of profound effects. Right now, the Fed is simply looking for something to turn up, while it persists with the current high interest rates and hopes for the best.

The sad truth is that this policy conundrum has been created by the Fed itself. It is time to take away the keys in this chicken run. We cannot rely on the Fed to get the economy out of this mess. We need fiscal and other policies, including serious efforts to regulate industries such as electricity production and transmission in the public interest, to address the underlying problems, not futile interest rate squeezes on the rest of the economy.

I feel like the interest rate hikes were designed to create unemployment and soften the labor market. Pain in the economy is the point, because the monied interests don’t like it when labor gets uppity when unemployment is low. Same reason the tech industry started laying everyone off. I bet this will all continue well past the point of recession, if that’s what it takes to make regular people desperate enough to make the monied interests happy. The fed takes care of their own.

That is not a bad observation that. Not bad at all. Going from memory, the Pandemic caused wages to grow as not everybody was keen to throw themselves into the firing line and plenty of employees told their employers that they were gunna work from home – or quit. And lots of people took early retirement rather than risk getting Covid which also reduced the number of employees available to work. There were soon rumblings how employees had to be brought into line again and it looks like this is it.

The Fed has done this numerous times, so the precedent has been set. Greenspan commented numerous times about keeping wages dampened so that the pesky “wage-price spiral” doesn’t occur. But the Fed these days doesn’t seem to have a problem with the asset-price spiral.

Because the unions have been decimated.

“I feel like the interest rate hikes were designed to create unemployment and soften the labor market.”

Didn’t Powell literally say this?

5% rates are historically not high. It’s that relative to the ZIRP rates we’ve had that 5% seems high.

I am currently trying to sell a townhouse. The price at which the last 3 which were sold in the complex averaged $410,000. I am currently listed just under 400k. Few showings, no offers in almost 3 months.

I did some math and at 3% with taxes, HOA fees and insurance the payment at 400k would be about 2850/mo…….. to get the same payment at 7% the price would need to be about $275k.

It seems to me the answer should be to let prices fall rather than lower interest rates. Because it was the low rates that drove prices up. Yes it will cause a recession. But it was our reluctance to have clearing recessions, by lowering rates anytime things got dicey which got here in the first place.

They had a perfect opportunity to adjust prices in 2008….. they pumped instead.

The Fed has learned from GameStop that they can keep pumping and the animals will keep coming back to drink

I recently sold my condo at a similar price in four days. I knew the market was hot, but was astounded at the speed of events. All the opposite of what I would have expected with interest rates higher. But, cash deal from a Boomer, no inspection, not a mortgage paying young person, who really should have been the new owner. I looked at those monthly costs in the Zillow ad, and thought, who can afford that?

I am very happy to park my gains in a 5.2% money market fund, liquid and federally protected. Finally, a safe place to put savings. Sure, inflation is eating it, but, can’t lose it to “events”.

So the people who has benefitted from the asset inflation will continue to benefit.

The affordability is the problem for the working people starting out. My current hone was bought 7 years ago, 170k, 20% down. Payments around 1200. It’s value compared to comps have doubled at least, so 20% down the payment is 2300. That is an insane change in living conditions, and my middle class earnings (currently about 120k) wouldn’t be able to afford that situation now.

If the Fed doesn’t keep these rates up permanently, then they are signalling they really don’t give a $#@% about it and let the peasants eat cake.

What we’re living through is the final burnout of the Boomer economy, as they die off. The laddered up this housing economy for forty years, with federal and sometimes state tax incentives, and they pretty much own most of the equity. Most aren’t moving, not because they can’t afford higher interest mortgages, like the preferred meme from the media pushes, but because old people, in general, don’t move. If they do, they ironically support this market with cash from equity, churning it all sideways. It will end, and the housing market will deflate, but may take another ten to even twenty years before they’re gone.

These rates aren’t that high. I lived through 18% fed rates as a young adult. 15% CDs from the bank, double your money in five years, if you had any. The world went on, and thrived, because a zillion Boomers entered the markets. Now that’s ending.

When rates were like that the median income to price ratio was like 1.5 or 2. Now it’s over 5.

Back when mammoths roamed the plains of Manitoba, $120,000 USD a year would put you near the top of the “Middle Class,” perhaps even into the “Wealthy” class.

In 1967, Dad got a pretty good job that paid about $32K a year. This single earner family could afford a fixer upper on Miami Beach. Fast forward to the mid 1990s, and when Mom sold the place, she got around $350K for it. It was torn down and a McMansion put up in its place, but, still worth well over a million in 2000. The big difference being that, in 1967, a mid-middle-class family could afford to move on up; by 2000, only the already rich could afford to move there. (The house was bought by a ‘Trust Fund Baby.’ Second generation wealth.)

I really do fear for America when the “middle class” finally wakes up to the buggering it is enduring from the wealth class. You think ‘things’ look bad now?

An old slogan went: Share the Wealth.

The new slogan will be: Share the Pain.

What money market fund is that?

I don’t know which MM but Fidelity is paying a hair under 5% and you can find CDs for 5.4%.

Echoing Paul Art — Would it be a faux pas to ask what liquid and federally protected money market fund you found that pays 5.2%? I can clap for Tinker Bell but … what liquid and federally protected money market fund did you find?

VMFXX

Check writing, too. But keep an eye on rates. Back into bonds if they drop.

Thanks! Will take a look at VMFXX — although it sounds like an online bank. I am extremely allergic to online banking.

Vanguard. You can trust them.

It seems to me the answer should be to let prices fall rather than lower interest rates. I am of this opinion as well, SteveB. ZIRP creates bubbles. Prices are inflated because of speculation. Stupid money gets thrown at unnecessary tech that exacts a cut. Allowing interest rates to stay at 5% would sort some of this. Importantly, it would have an effect on leverage and margin pools. I don’t consider 5% high.

My own take is that de-growth is better than inflation. Let the economy slow down and things will sort themselves out. The rich investors whine about high interest rates because they can’t sell at a higher profit. Hogs!

Your comment is ‘curious’. I would not call crashing the economy as the title of this post describes, a ‘slowdown’. You suggest that de-growth is better than inflation but I have difficulty in equating de-growth with the economic consequences of de-growth which you see as their ‘better’ part. Some further elaboration on your part might be helpful.

Though I sympathize with your lack sympathy for the whines of rich investors and the losses they feel as a consequence of high interest rates on their profit margins — as someone in the market for a house or property I am surprised by how little loss rich investors — property owners — might see as a consequence of high interest rates. The prices buyers see just seem to go up and never down. What losses are rich investors feeling? I do not believe rich investors are playing with the same money as ordinary buyers. Many rich buyers are cash buyers and little impacted by the interest rates affecting house mortgages, other than the effect those high interest rates may have on discouraging other less wealthy buyers. I suppose high interest rates and high prices might be very positive for the wealthy rentiers.

Mosler would point out also that the elevated interest rate levels further exacerbate the inequality outlined here, since the increased payments via the interest income channel are also payed out disproportionately to the rich — it’s welfare for rich people.

How so? Welfare for rich people is subsidized business and no to little taxes in my book. But how are historically reasonable interest rates helping the rich, other than they have a safe place to park their money, like most Americans?

A big chunk of the deficit at the moment is interest on the debt. In 2019 the government paid about $404B in interest to the public. In 2024 it’s going to pay well over $700B in interest. That’s more than a 75% increase. Much of that money is going to wealthy households via their financial asset holdings and pensions.

You should check out the bond market the past few years. It sucked, still sucks. Doubt that the waspy enclaves in eastern beach towns are raising a drink to that over discussions about the family trusts.

How are the current interest rate hikes ‘historically reasonable’? Most Americans — portions of the middle class — can park their money in banks, CDs, or other vehicles, iff they have money to park somewhere outside of the money they already have tied up in a house or parked perhaps in a small bank account paying ‘somewhat’ less than the interest rate their mortgages and credit cards charge. [Of course they could gamble on the Stock Market or craps.] The high interest rates also seems to lock renters into paying increasing rents with diminished prospect of saving-up to buy their own housing so they can escape from the rich people raising their rents.

How is private equity financed? As rates and “growth” grow sufficiently to price most of us out of the residential real estate market, the hedge funds keep bidding the prices up and bringing on the neo-feudalism of renter surfs we are becoming.

One does not see it mentioned often but private equity is emboldened by low rates. The PE types are likely pleased to see all the support for lowering rates for their operations.

John W.: How did Bezos finance his half billion dollar yacht ? I am hearing that he did not sell any of his stock (or other assets). Instead, he borrowed the money using his assets (stock) as collateral. I wonder how he views the new higher interest rates ?

I have also read that Elon Musk pays himself a small salary. He finances his lavish life style by borrowing and using TESLA stock as collateral. I wonder how a higher interest rate will change his world view?

Also, 5% interest rates not “high”. They are close to normal. At least now the savers will get something for their savings.

I have read elsewhere that the banks bundled up and sold their CRE loans to investors. So the banks (and the FED) are not worried about the collapse of Commercial Real Estate assets.

I think knowing this gives one a better idea of whose special interests might be hurt by further raising interest rates.

The US does not have a functioning central government able to overcome the special interests or regulate the casino on Wall Street. The USA needs to bring down the expense of education, health care, and housing, so that the commoners can afford the cost of living.

I don’t have any easy answers to these problems. But I suspect things will go on as they are now, or until something serious breaks. Some sort of equilibrium between higher wages and higher interest rates might be established. But I am not holding my breath.

The rich mainly borrow with their 401(K) stock funds as collateral.

I think the Fed has run out of road. This round of interest rate hikes seems to have hardly held back “the economy” at all. Outside of mortgage brokers, who are probably in their own personal depression, with transaction volumes so low. And then there is office CRE which is heading down below the earth’s crust into the mantle. But that’s a secular decline due to remote work and overbuilding during the post GFC era. No amount of rate cuts can fix that – a vacant, zombie office building full of vermin and spider webs is worth the land it sits on, minus the demolition cost.

This is the conclusion of the piece that I agree with:

Too bad we have a corrupt Congress that does nothing but insider trading and taking bribes from military industrial complex.

I think the Fed will really run out of road when they finally lower short rates and the long rates don’t come down.

They will bring them down by buying long term bonds as they have done already. Unless the plebs revolt because they cant afford food, the beating will continue.

But the Fed tactic of buying long term bonds at a high price to lower rates came at a delayed cost.

In 2023 the Fed had its largest ever operating loss (114.3 billion) as it sold securities it had bought at a higher price to keep long term interest rates low.

https://www.wsj.com/economy/central-banking/fed-posts-largest-ever-annual-operating-loss-6e249a39

Fed has no losses, we taxpayers do.

Instead of regulating electric production and transmission, the US grid is becoming ever more compromised by AI data centers and bitcoin mining. AI is now using as much electricity as a small country.

https://www.forbes.com/sites/arielcohen/2024/05/23/ai-is-pushing-the-world-towards-an-energy-crisis/

Wrong forum?

“effects of prolonging elevated interest rates on ordinary consumers”

oh please….

If this begging for easy money had anything to do with ‘ordinary consumers,’ there would be a willingness to address the usory rates that exist for the ‘ordinary’ even when others get to enjoy the delusionally inflated asset prices from the criminally low interest rates for the few.

Not to mention taking a chainsaw to the monopolies and oligopolies in the market

Does the FED really intend to reduce inflation by increasing rates or is it part of a system that intends to weaken China and other countries that do not recognize American supremacy at the risk of destroying itself also using monetary policy and the strengthening of the dollar? It would be in line with the policy of sanctions and seizure of other nations’ reserves. Or you can imagine that the FED is completely disconnected from the other centers of American power and genuinely interested only in its own objectives.

When the FED says it’s fighting inflation, the FED is talking about wage inflation and the people think they’re fighting price inflation.

Along with that is the Friedman targeted 2% IR has been called a quasi gold standard in the day. Add on to that after decades if fiddling around with IR that some note the market has become fixated on it and not in a good way. Most of all the U.S. had a hard time even getting a whiff of inflation for decades but it was thought a victory by the quasi monetarists ideologues. Now look at them.

Jim bailed out before the cliff edge, Buzz went over the cliff when he couldn’t bail because he got trapped in his faulty model. Right metaphor, wrong guy.

Is there another way to keep the dollar “strong” besides a high interest rate? Probably not since we are being so out-produced by China and emerging economies. And as long as we are dependent on oil and gas to run our economy. We and everyone else, which makes oil more expensive. So until the world settles into a new sustainable paradigm we will have to deal with price inflation. We’ve always used monetary policy to adjust fluctuations, but, I’d guess that’s not possible, not for long term trends. The assumption being that things will go back to normal. So now it is a paradigm shift that won’t ever be going back to “normal” so clearly higher interest rates are creating not just a bigger problem, but a permanent problem, unless they are offset by spending. Simon Michaux has a new podcast “Out of gas, but not out of fuel” which talks in practical detail about the necessity to shift away from oil and into a sustainable economy based on recycling resources, etc. But, clearly not a short term fix anymore.

These relationships are not set in stone.

The dollar was weak in the 1970s and it started a rise to new highs v. the pound and other currencies when Volcker cut rates in 1982

I maintain that the core issue is that elected leadership in the US continues to outsource more and more of the management of the economy to the Fed, or to put it another way expecting monetary to resolve the problems created by their fiscal policies. Raising interest rates are a absolutely a way to reduce inflation. That goal may come at far too high a price, but in a sense at least it works. If we had a functioning legislature and executive branch which was organized and competent enough to solve these issues on the fiscal rather than monetary side of things it would be a completely different ballgame.

Instead we get record high fiscal deficits and trying to bring in the Fed to combat this by raising rates. I am of the opinion that raising taxes would be more effective, sure, but the likelihood of this or any other sitting congress and president doing so in the next few years are slim and none. So we get what we have now. It’s easy to bash the Fed and most people do, but they’re only playing the role our broken system has carved out for them.

Didn’t bank of Canada just cut rates last month telling everyone that inflation was beaten and now the first inflation reading after the cut exploded higher?

https://www.bloomberg.com/news/articles/2024-06-25/canada-inflation-reaccelerates-to-2-9-raising-bar-for-july-cut

Thomas Ferguson ends his piece thusly: “We cannot rely on the Fed to get the economy out of this mess. We need fiscal and other policies….” Sadly that means Congress needs to act but there’s no hope in that, since our Congress is beyond dysfunctional and totally corrupted by the donor class. MMT, I believe, would prescribe tax increases to curb the wealth effect, so like I said, no hope there. That leaves the Fed, higher for longer and aggressive QT. The countdown to recession has begun.

There are several generations actually praying for a crash, as it is the only hope they have of affording real estate.

Amen.

How about a correction? A real crash is nothing I would hope for.

For people in their 30s 40s who have a good amount saved up with no debt, a HUGE crash is exactly what they are hoping for. For people who bought at the top? If there’s a crash hopefully they’ve put aside some money for buying handkerchiefs in bulk.

It sounds like what the economy needs, rather than higher interest rates from the Fed, is way higher tax rates on the uppermost income brackets enacted by Congress. Then a lot of this excess spending on high-priced goods and services will come to a halt.

(Ignore the fact that this is my same proposal to solve a raft of other problems with the US economy.)

Outsized political corruption, malinvestment, ect ect.

The rich are responsible for inflation? Raise their taxes and suck that extra buying power out of their treasure chests. All that money could be put to good use for the rest of us, Mike Liston

Think more like $1trillion of PPP forgiven to the rich , tax free.

Current interest rates may cause economic problems – but not in the way that many think.

Interest rates are currently not high, at least not in a historic sense. From 1990 through 2007 10-Year Treasury rates drifted between 9% highs and 3.5% lows. During this period in the 2000’s rates averaged 4.5%, and in the 1990’s they never went below 4.44%. It was not until the Great Financial Crisis, in combination with the Covid Pandemic, that the U.S. government instituted an unprecedented 13 year near zero interest rate policy (ZIRP) to stimulate our economy out of these economic shocks.

So 10-Year Treasury rates are not historically high at 4.25%. They were between 10% and 16% in the early 1980’s – that was high. Lowering these interest rates below their historic norms is something the Fed traditionally does to stimulate the economy in times of economic weakness. This action would be out of the ordinary for the Fed in our current environment where daily stock market highs don’t seem to indicate economic weakness.

When the Fed started to raise interest rates in March 2022, one of their stated reasons for this action was to help fight inflation. But the other reason which should be obvious is that this interest rate was at 0% before they successively raised it to a range of 5.25 – 5.5%. Zero percent is not a normal interest rate that we should expect in the future, nor is 5.5% an unusually high rate which requires government intervention to prevent disaster. Go back to the 1960’s and see for yourself (select Max on this chart). Current interest rates are not outside historic norms – it’s the 13 years of near zero interest rate policy that were unusual.

Media keeps pushing the idea that the Fed wants to lower interest rates for some undisclosed reason. What’s curious is no one ever says why the Fed wants to do this. Many are likely misinterpreting the quarterly ‘Dot Plot’ survey of Fed Open Market Committee Members, where they are asked to forecast interest rates at specific future dates. What this survey shows is not when Open Market Committee Members will make arbitrary or unwarranted changes to interest rates (they can’t raise or lower rates without a reason), but rather what they economically forecast at these future dates that will lead them to prudently raise rates (slow overheating) or to lower rates (stimulate weakness) accordingly. In this interpretation it’s worth asking specifically what certain Fed Committee Members believe will force them to stimulate a weak economy (by lowering rates) in the near or intermediate future.

Transitioning from near zero to historically normal interest rates can be tricky. Especially for large borrowers that consistently roll over their debt at maturity (think commercial real estate loans – with monthly payments which are ALL interest, and only pay principal at maturity). Those monthly payments on billons of dollars in principle will be going up significantly the next time their loan is rolled. It is also a challenge for Private Equity companies whose asset values are determined by how much purchasers can raise through significant borrowing (lower rates mean substantially higher levels of borrowing). Less borrowing means much lower purchase prices – which is bad because sellers need purchase prices to exceed their assets own significant debt. It is also a challenge for Interest Rate Derivatives (IRD) where big rate swings can cause substantial losses for one counterparty in IRD contracts (the IRD market has a notional value in the tens of trillions of dollars – and most of them are held by banks). It’s unclear if these IRD losses are currently unrealized, and will later be realized at contract expiration.

So any Fed decision to lower interest rates will not be arbitrary and will likely not be done when there are stock market highs, but they may be implemented in the near future if there is a negative economic shock to warrant them.

Even very dovish Lael Brainerd, now in Biden Admin, said that they intended to normalize rates all along the yield curve.

Inflation is in part an excuse to do something the punch drunk asset holding class doesn’t want them to do.

In last Fed presser, Powell stated that lower inflation was not sufficient reason to lower fed funds rate. They would look at inflation in context along with gdp and employment etc.

During the GFC “the market” thought the zlb in Europe was crazy town. More recently you see them redefining “policy normalization” to mean rates near zero.

The upshot of that would mean the next time there is an actual recession, “the market” would have no access to their preferred policy response to recession.

Think the Fed is going to time them out and take the longer term view, continuing to keep rate cuts just out of reach.

Also no one considers that part of their mandate is to keep people and institutions buying Treasuries. Why should they work towards a policy that that makes themselves the primary buyer of US debt?

“….Fed in our current environment where daily stock market highs don’t seem to indicate economic weakness…”

But but but what about them stock buy backs?

The only solution is to tax like it’s 1959, for the Common Good, remember?

We have a serious affordability problem in housing and a stock market near all time highs. That does not seem to be prime time for rate cuts.

Furthermore, inflation hurts the poor much more than the rich.

The FED needs to stay the course.

While high interest rates help those with assets, they hurt those without. Housing prices are skyrocketing not because wealthy people can afford high prices that other cannot, but because high interest rates are increasing the problem of not enough new homes being built. Even rich people will buy cheap when they can. Indeed, that is part of how many of them got rich. High interest rates have stopped capital-intensive development in many areas, such as off-shore wind electricity production. However, the effect is especially obvious and painful in the housing and rental areas where basic unit shortages are critical.